|

市場調查報告書

商品編碼

2034862

全球電動車無線充電市場:按充電系統、充電類型、應用、組件、供電範圍、推進系統、車輛類型和地區分類-預測至2032年Wireless Charging Market for Electric Vehicles by Charging System (Inductive, Capacitive, Magnetic Power Transfer), Propulsion, Charging Type (Stationary, Dynamic Wireless Charging), Component, Power Supply, and Vehicle Type - Global Forecast to 2032 |

||||||

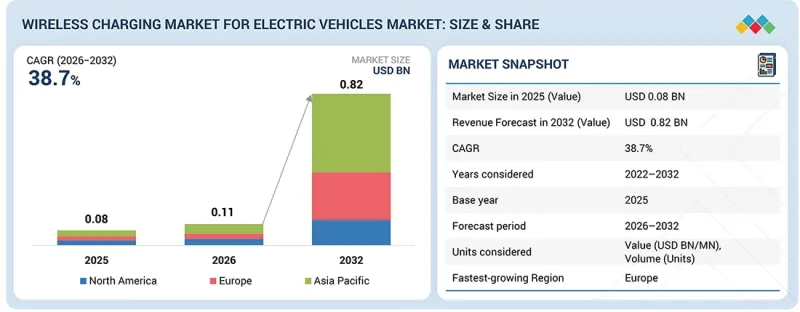

預計到 2032 年,電動車無線充電市場規模將達到 8.2 億美元,高於 2026 年的 1.1 億美元,複合年成長率為 38.7%。

這一成長主要得益於電動車的日益普及以及人們對更便捷充電方式的日益關注。汽車製造商正與技術供應商合作,探索將無線充電技術整合到汽車平臺中。無線充電能夠實現自動能量傳輸,減少對線纜的依賴,並顯著提升便利性,尤其是在都市區和車隊應用中。

| 調查範圍 | |

|---|---|

| 調查期 | 2026-2032 |

| 基準年 | 2025 |

| 預測期 | 2026-2032 |

| 目標單元 | 10億美元 |

| 部分 | 按充電系統、充電類型、應用、組件、供電範圍、推進方式、車輛類型和區域分類 |

| 目標區域 | 亞太地區、北美地區、歐洲 |

感應式充電系統、對準技術和標準化的進步正在提升系統效能並加速初期部署。隨著車輛與基礎設施融合程度的提高,無線充電可望在高頻應用場景中逐步普及。

“按充電系統類型分類,感應式電力傳輸預計將成為最大的細分市場。”

感應式電力傳輸是目前電動車無線充電應用最廣泛的方式。它基於電磁感應原理,透過地面發射墊和車輛接收墊之間的電力傳輸來實現。在SAE J2954等標準化標準的推動下,感應式充電系統正日益普及,廣泛應用於住宅、職場和公共充電環境。現代、沃爾沃集團、寶馬和豐田等汽車製造商,以及安波福和馬勒等一級供應商,都在致力於將感應式充電整合到汽車平臺中。例如,2026年3月,Electreon公司在美國密西根州擴大了其感應式充電部署,用於公共交通和車隊應用。在此之前,2025年6月,ENRX公司與沃爾沃集團合作,為電動巴士和卡車部署感應式充電,並支援機械式充電。感應式電力傳輸的主要優點包括電力傳輸穩定、易於整合以及系統複雜度低。感應式電力傳輸的效率通常可達90-95%,從而降低能量損耗並實現穩定的充電性能。這些優勢推動了感應式電力傳輸的廣泛應用,使其成為市場上的領先技術。

“按充電方式分類,固定式無線充電預計將成為最大的細分市場。”

固定式無線充電作為一種適用於住宅、職場和公共停車場的自動化充電實用解決方案,正日益受到關注。該系統基於感應式電力傳輸,在地面安裝的充電板和車輛上的接收器之間傳輸能量。這使得車輛停放時無需手動操作即可充電,從而提高了便利性並減少了對插電式充電系統的依賴。這項技術非常適合長時間停放的乘用車和車隊應用。該技術支援穩定的充電,改善用戶體驗,並減少實體連接器帶來的磨損和損壞。汽車製造商 (OEM) 和無線充電供應商正致力於將這些系統整合到汽車平臺和停車基礎設施中。 2026 年 3 月,WiTricity 與西門子合作,推動固定式無線充電解決方案在住宅和車隊停車應用中的部署,並專注於可擴展的基礎設施整合。隨著系統效率和標準化程度的提高,預計固定式無線充電將在關鍵應用場景中得到更廣泛的應用。

“預計在預測期內,歐洲將成為成長最快的市場。”

在歐盟嚴格的排放氣體法規和明確的脫碳目標的支持下,歐洲汽車產業正大力轉型為零排放出行。歐洲各國積極透過獎勵、基礎設施投資和政策支持來推廣電動車,為無線充電技術的發展創造了有利環境。高階電動車的興起以及用戶對便利性和先進車輛功能日益成長的需求也推動了無線充電的需求成長。汽車製造商和技術供應商正在攜手合作,將無線充電技術整合到下一代汽車平臺中,同時確保符合區域標準和互通性要求。該地區的主要參與者包括德國的IPT Technology GmbH和Robert Bosch GmbH、業務遍及多個歐洲市場的Electreon以及挪威的ENRX。 2025年4月,Electreon擴大了在德國的無線充電道路項目,支援公共交通感應式充電基礎設施的部署。這些解決方案正透過先導計畫和早期商業計畫進行推廣,尤其是在公共交通和車隊應用領域。隨著對智慧城市和互聯基礎設施的投資不斷增加,歐洲有望在推動電動車無線充電技術的廣泛應用方面發揮核心作用。

電動車無線充電市場由Electreon(以色列)、Witricity(美國)、ENRX(挪威)、HEVO Inc.(美國)及Plugless Power Inc.(美國)等老字型大小企業主導。這些公司開發並提供各種無線充電解決方案,從工廠整合系統到高功率車隊基礎設施,應有盡有。

調查範圍:

本研究從充電系統(感應式、磁力式、傳導式)、驅動系統(純電動車、插電式混合動力車)、充電型式(固定式無線充電、動態無線充電)、組件(底座充電板、電源控制單元、車用充電板)、功率(<3.7 kW、3.8-7.7 kW、7.8-11 kW、7.8-11 kW、7.8-11> kW)和車輛類型(乘用車、商用車)等方面分析了電動車無線充電市場。此外,本研究也涵蓋了無線充電生態系統中主要參與者的競爭格局和公司概況。

本報告的主要益處:

本報告為市場領導和新參與企業提供電動汽車無線充電市場及其細分市場整體收入的最準確預測。這有助於相關人員了解競爭格局,更有效地進行業務定位,並獲得制定合適打入市場策略所需的洞察。此外,本報告還幫助相關人員掌握市場趨勢,並提供關鍵市場促進因素、限制因素、挑戰和機會的資訊。

本報告深入分析了以下幾點:

- 關鍵促進因素(更多原始設備製造商進入無線充電生態系統、無線充電與自動化和智慧停車系統的整合、政府對排放排放和永續電動出行的大力支持)、阻礙因素(整合式車載無線充電系統高成本且複雜、與傳統有線充電解決方案相比能量傳輸效率較低)、機會(智慧城市基礎設施中無線充電的普及、對動態無線充電技術的投資增加、高頻電動汽車車隊營運中無縫充電的潛力)以及影響市場成長的挑戰(缺乏標準化的車輛整合框架、公共無線充電基礎設施的安裝和部署成本高)。

- 產品開發/創新:深入了解未來技術、研發活動以及市場上的新產品發布。

- 市場發展:盈利市場的全面資訊-本報告分析了各個地區的市場。

- 市場多元化:提供有關新產品、未開發市場、最新趨勢和市場投資機會的全面資訊。

- 競爭分析:對 Electreon(以色列)、Witricity(美國)、ENRX(挪威)、HEVO Inc.(美國)和 Plugless Power Inc.(美國)等領先公司的市場佔有率、成長策略和服務產品進行詳細評估。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 價格分析

- 生態系分析

- 價值鏈分析

- 案例研究分析

- 投資和資金籌措場景

- 專利分析

- 技術分析

- 市場結構與競爭重點

- 無線電動汽車充電基礎設施和整合中的依賴關係

- 投資和資本支出分析

- 監管概述

- 2026-2027 年主要會議和活動

- 全球電動車發展趨勢

- 主要相關人員和採購標準

- 影響客戶業務的趨勢/顛覆性因素

- OEM分析

第5章:電動車無線充電市場(依充電系統分類)

- 磁力傳輸

- 感應式電力傳輸

- 電容式功率傳輸

- 關鍵見解

第6章:電動車無線充電市場(以充電方式分類)

- 桌面無線充電

- 動態無線充電

- 關鍵見解

第7章:電動車無線充電市場(依應用領域分類)

- 家用充電單元

- 商業充電站

- 關鍵見解

第8章:電動車無線充電市場(按組件分類)

- 底座充電板

- 電源控制單元

- 車輛充電板

- 關鍵見解

第9章:電動車無線充電市場(依供電範圍分類)

- 小於3.7千瓦

- 3.7~7.7kW

- 7.8~11kW

- 11千瓦或以上

- 關鍵見解

第10章:電動車無線充電市場(依動力系統分類)

- BEV

- PHEV

- 關鍵見解

第11章:電動車無線充電市場(依車輛類型分類)

- 搭乘用車

- 商用車輛

- 關鍵見解

第12章:電動車無線充電市場(按地區分類)

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 歐洲

- 法國

- 德國

- 荷蘭

- 挪威

- 西班牙

- 瑞典

- 瑞士

- 英國

- 北美洲

- 加拿大

- 美國

第13章 競爭格局

- 主要參與企業的策略/優勢,2022-2025年

- 2025年市佔率分析

- 2021-2025年收入分析

- 企業估值和財務指標

- 品牌/產品對比

- 企業估值矩陣:主要公司,2026 年

- 公司估值矩陣:新創企業/中小企業,2026 年

- 競爭格局

第14章:公司簡介

- 主要參與企業

- ELECTREON

- WITRICITY AI TECH, LLC

- ENRX

- HEVO INC.

- PLUGLESS POWER INC.

- MITSUBISHI ELECTRIC CORPORATION

- TGOOD ELECTRIC CO., LTD.

- TOYOTA MOTOR CORPORATION

- ROBERT BOSCH GMBH

- CONTINENTAL AG

- TOSHIBA CORPORATION

- HELLA GMBH & CO. KGAA

- 其他公司

- IDEANOMICS INC.

- VOLTERIO GMBH

- MOJO MOBILITY INC.

- BMW

- FORTUM CORPORATION

- HYUNDAI MOTOR COMPANY

- PULS GMBH

- DAIHEN CORPORATION

- VIE GROUP CO., LTD.

- IPT TECHNOLOGY GMBH

- EASELINK GMBH

- MAHLE GMBH

- NISSAN MOTOR CO., LTD.

第15章:調查方法

第16章附錄

The wireless charging market for electric vehicles is expected to reach USD 0.82 billion by 2032, from USD 0.11 billion in 2026, with a CAGR of 38.7%. This growth is supported by increasing EV adoption and rising focus on improving charging convenience. OEMs are evaluating the integration of wireless charging into vehicle platforms, which is influenced by partnerships with technology providers. Wireless charging enables automated energy transfer, reducing reliance on cables and improving ease of use, especially in urban and fleet applications.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | USD Billion |

| Segments | Charging Type, Component, Application, Charging System, Propulsion, Power Supply Range, Vehicle Type |

| Regions covered | Asia Pacific, North America, Europe |

Advancements in inductive systems, alignment, and standardization are enhancing system performance and supporting early-stage deployments. As integration across vehicles and infrastructure improves, wireless charging is expected to see gradual adoption in high-utilization use cases.

"Inductive power transfer is expected to be the largest segment by charging system."

Inductive power transfer is the most widely used method for wireless charging of EVs. It operates on the principle of electromagnetic induction, where power is transferred between a transmitter pad on the ground and a receiver pad installed in the vehicle. Inductive systems are being deployed across residential, workplace, and public charging environments, supported by standardization efforts like SAE J2954. OEMs such as Hyundai, Volvo Group, BMW, and Toyota, along with Tier-1 suppliers like Aptiv and Mahle, are working on integrating inductive charging into vehicle platforms. For instance, in March 2026, Electreon expanded its inductive charging deployment in Michigan, US, for public transport and fleet applications. Earlier, in June 2025, ENRX partnered with Volvo Group to deploy inductive charging for electric buses and trucks, supporting opportunity charging. Key advantages of inductive power transfer include stable power transfer, ease of integration, and lower system complexity. The efficiency of inductive power transfer typically ranges between 90-95%, supporting reduced energy losses and consistent charging performance. These factors support widespread adoption of inductive power transfer and position it as the leading technology in the market.

"Stationary wireless charging is expected to be the largest segment by charging type."

Stationary wireless charging is gaining traction as a practical solution for automated charging in residential, workplace, and public parking environments. Based on inductive power transfer, the system enables energy transfer between a ground-based charging pad and a receiver installed in the vehicle. This allows vehicles to charge without manual intervention while parked, improving convenience and reducing reliance on plug-in systems. The technology is well-suited for passenger cars and fleet applications where vehicles remain stationary for defined periods. It supports consistent charging, improves user experience, and reduces wear and tear associated with physical connectors. OEMs and wireless charging providers are focusing on integrating these systems into vehicle platforms and parking infrastructure. In March 2026, WiTricity, in collaboration with Siemens, advanced the deployment of stationary wireless charging solutions across residential and fleet parking applications, focusing on scalable infrastructure integration. As system efficiency and standardization improve, stationary wireless charging is expected to see wider adoption across key use cases.

"Europe is expected to be the fastest-growing market during the forecast period."

The European automotive industry is witnessing a strong shift toward zero-emission mobility, supported by strict emission regulations and clear decarbonization targets set by the European Union. European countries are actively promoting EV adoption through incentives, infrastructure investments, and policy support, creating a favorable environment for wireless charging technologies. Demand for wireless charging is also supported by the growing presence of premium EVs and increasing focus on user convenience and advanced vehicle features. OEMs and technology providers are working together to integrate wireless charging into next-generation vehicle platforms, with alignment toward regional standards and interoperability requirements. Key players in the region include IPT Technology GmbH and Robert Bosch GmbH in Germany, Electreon operating across multiple European markets, and ENRX in Norway. In April 2025, Electreon expanded its wireless charging road projects in Germany, supporting the deployment of inductive charging infrastructure for public transport applications. These solutions are being deployed through pilot and early commercial projects, particularly in public transport and fleet applications. As investments in smart cities and connected infrastructure increase, Europe is expected to play a central role in advancing wireless EV charging adoption.

In-depth interviews were conducted with CXOs, managers, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 24%, Tier 1 - 67%, Tier 2 - 9%,

- By Designation: CXOs - 33%, Managers- 52%, Executives - 15%

- By Region: North America - 32%, Europe - 27 %, Asia Pacific - 41%

The wireless charging market for electric vehicles is dominated by established players such as Electreon (Israel), Witricity (US), ENRX (Norway), HEVO Inc. (US), and Plugless Power Inc. (US). These companies develop and supply wireless charging solutions, ranging from factory-integrated systems to high-power fleet infrastructure.

Research Coverage:

The study analyzes the wireless charging for electric vehicles market by charging system (inductive power transfer, magnetic power transfer, conductive power transfer), propulsion (BEV, PHEV), charging type (stationary wireless charging, dynamic wireless charging), component (base charging pads, power control unit, vehicle charging pads), power supply (<3.7 kW, 3.8-7.7 kW, 7.8-11 kW, >11 kW), and vehicle type (passenger cars, commercial vehicles). It also covers the competitive landscape and company profiles of the major players in the wireless charging ecosystem.

Key Benefits of Report:

The report will provide market leaders and new entrants with the closest approximations of revenue figures for the overall wireless charging market for electric vehicles and its subsegments. It will help stakeholders understand the competitive landscape and gain insights to position their businesses more effectively and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (Increased participation of OEMs in wireless charging ecosystem, Integration of wireless charging with automated and smart parking systems, Strong government support for emission free and sustainable electric mobility), restraints (High cost and complexity associated with integrating in vehicle wireless charging systems, Lower energy transfer efficiency compared to conventional wired charging solutions), opportunities (Growing adoption of wireless charging within smart city infrastructure, Rising investments in dynamic wireless charging technology, Potential for seamless charging in high utilization electric fleet operations), and challenges (Lack of standardized vehicle integration frameworks, High setup and installation costs for public wireless charging infrastructure) influencing the growth of market

- Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and new product launches in the market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the market across various regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Electreon (Israel), Witricity (US), ENRX (Norway), HEVO Inc. (US), and Plugless Power Inc. (US), among others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.2 DISRUPTIVE TRENDS SHAPING WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES

- 2.3 HIGH-GROWTH SEGMENTS

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES

- 3.2 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE

- 3.3 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION

- 3.4 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY POWER SUPPLY RANGE

- 3.5 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY CHARGING SYSTEM

- 3.6 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COMPONENT

- 3.7 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Ability to combine user-centric design with long-term cost efficiency

- 4.2.1.2 Active participation of OEMs in wireless charging ecosystem

- 4.2.1.3 Integration of wireless charging with automated smart parking systems

- 4.2.2 RESTRAINTS

- 4.2.2.1 High integration cost and design complexity of in-vehicle wireless charging systems

- 4.2.2.2 Lower energy transfer efficiency compared to conventional wired charging solutions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rapid adoption of wireless charging within smart city infrastructure

- 4.2.3.2 Rising investments in dynamic wireless charging technologies

- 4.2.3.3 Potential for seamless charging in high-utilization electric fleet operations

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of standardization and interoperability across vehicles and wireless charging infrastructure

- 4.2.4.2 High setup and installation costs for public wireless charging infrastructure

- 4.2.1 DRIVERS

- 4.3 PRICING ANALYSIS

- 4.3.1 AVERAGE SELLING PRICE TREND, BY PROPULSION, 2023-2025

- 4.3.2 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025

- 4.4 ECOSYSTEM ANALYSIS

- 4.4.1 OEMS

- 4.4.2 WIRELESS EV CHARGING SYSTEM PROVIDERS

- 4.4.3 CHARGING STATION SERVICE PROVIDERS

- 4.4.4 ENERGY SUPPLIERS

- 4.4.5 PAYMENT PROCESSING COMPANIES

- 4.4.6 END USERS

- 4.5 VALUE CHAIN ANALYSIS

- 4.6 CASE STUDY ANALYSIS

- 4.6.1 ELECTREON'S WIRELESS CHARGING ROAD PROJECT

- 4.6.2 WITRICITY'S HALO WIRELESS CHARGING SYSTEM

- 4.6.3 HEVO'S WIRELESS CHARGING PAD

- 4.6.4 ENRX'S INDUCTIVE CHARGING SYSTEM

- 4.6.5 PLUGLESS POWER'S RESIDENTIAL WIRELESS CHARGING SYSTEM

- 4.6.6 WITRICITY'S DRIVE 11 WIRELESS CHARGING TECHNOLOGY

- 4.6.7 PLUGLESS POWER'S WIRELESS LEVEL 2 CHARGING SYSTEM

- 4.6.8 ELECTREON'S DYNAMIC AND STATIONARY EV CHARGING INFRASTRUCTURE

- 4.6.9 HEVO AND VEHYA'S WIRELESS EV CHARGING SOLUTION

- 4.7 INVESTMENT AND FUNDING SCENARIO

- 4.8 PATENT ANALYSIS

- 4.9 TECHNOLOGY ANALYSIS

- 4.9.1 KEY TECHNOLOGIES

- 4.9.1.1 Moving-field inductive power transfer

- 4.9.1.2 Resonant charging

- 4.9.1.3 Dynamic wireless charging

- 4.9.1.4 Power electronics and conversion

- 4.9.2 COMPLEMENTARY TECHNOLOGIES

- 4.9.2.1 Capacitive wireless power transfer

- 4.9.2.2 Thermal management

- 4.9.2.3 Foreign object detection

- 4.9.3 ADJACENT TECHNOLOGIES

- 4.9.3.1 Bidirectional charging

- 4.9.3.2 Renewable energy integration

- 4.9.1 KEY TECHNOLOGIES

- 4.10 MARKET STRUCTURING AND COMPETITIVE PRIORITIES

- 4.10.1 GLOBAL ALIGNMENT OF WIRELESS CHARGING STANDARDS

- 4.10.2 ADOPTION OF WIRELESS EV CHARGING IN PASSENGER AND COMMERCIAL SEGMENTS

- 4.10.3 AUTOMOTIVE OEM POSITIONING IN WIRELESS EV CHARGING ECOSYSTEM

- 4.10.4 TECHNICAL CONSTRAINTS IN WIRELESS POWER TRANSFER

- 4.10.5 INFRASTRUCTURE MATURITY AND COMMERCIALIZATION TIMELINES

- 4.10.6 PUBLIC SECTOR INVESTMENT VS. PRIVATE SECTOR OPERATIONS

- 4.11 WIRELESS EV CHARGING INFRASTRUCTURE AND INTEGRATION DEPENDENCIES

- 4.11.1 SUPPLIER ECOSYSTEM AND TECHNOLOGY DIFFERENTIATION

- 4.11.2 UTILITY COORDINATION AND SMART GRID INTEGRATION

- 4.11.3 WIRELESS CHARGING APPLICATIONS IN HIGH-DUTY FLEET ENVIRONMENTS

- 4.11.4 INFRASTRUCTURE REQUIREMENTS FOR DYNAMIC ON-ROAD WIRELESS EV CHARGING SYSTEMS

- 4.12 INVESTMENT AND CAPEX ANALYSIS

- 4.12.1 CAPITAL EXPENDITURE VS. OPERATIONAL EFFICIENCY MODELS

- 4.12.2 REAL ESTATE AND PARKING PARTNERSHIPS

- 4.12.3 INSURANCE AND WARRANTY CONSIDERATIONS

- 4.13 REGULATORY OVERVIEW

- 4.13.1 NETHERLANDS

- 4.13.2 GERMANY

- 4.13.3 FRANCE

- 4.13.4 UK

- 4.13.5 CHINA

- 4.13.6 US

- 4.13.7 REGULATORY POLICIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 4.14 KEY CONFERENCES AND EVENTS, 2026-2027

- 4.15 GLOBAL EV TRENDS

- 4.16 KEY STAKEHOLDERS AND BUYING CRITERIA

- 4.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 4.16.2 BUYING CRITERIA

- 4.17 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 4.18 OEM ANALYSIS

- 4.18.1 OEM-TECHNOLOGY PARTNER MAPPING FOR WIRELESS CHARGING BY VEHICLE MODEL

- 4.18.2 VALUE PROPOSITION FOR WIRELESS VS. WIRED CHARGING

- 4.18.3 PLAYER INTERRELATIONSHIPS: PLATFORM LEADERS VS. SYSTEM PROVIDERS VS. DYNAMIC CHARGING INNOVATORS

- 4.18.4 OEM READINESS AND INTEGRATION STRATEGY

- 4.18.4.1 Strategic trends in wireless EV charging adoption

- 4.18.4.2 Futuristic strategic insights: Road to 2030

- 4.18.5 DATA MONETIZATION STRATEGIES

5 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY CHARGING SYSTEM

- 5.1 INTRODUCTION

- 5.1.1 WIRELESS CHARGING SYSTEM OFFERINGS BY KEY PLAYERS

- 5.2 MAGNETIC POWER TRANSFER

- 5.2.1 ADVANTAGES OF MAGNETIC RESONANCE COUPLING TO DRIVE MARKET

- 5.3 INDUCTIVE POWER TRANSFER

- 5.3.1 LOWER COST AND MINIMAL MAINTENANCE REQUIREMENTS TO DRIVE MARKET

- 5.4 CAPACITIVE POWER TRANSFER

- 5.5 PRIMARY INSIGHTS

6 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY CHARGING TYPE

- 6.1 INTRODUCTION

- 6.1.1 COMPARISON BETWEEN WIRELESS CHARGING TYPES

- 6.2 STATIONARY WIRELESS CHARGING

- 6.3 DYNAMIC WIRELESS CHARGING

- 6.4 PRIMARY INSIGHTS

7 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY APPLICATION

- 7.1 INTRODUCTION

- 7.1.1 POWER SUPPLY RANGE OF HOME CHARGING UNITS OFFERED BY LEADING PLAYERS

- 7.2 HOME CHARGING UNITS

- 7.2.1 HEIGHTENED PASSENGER CAR SALES AMID GROWING CONCERNS AROUND EMISSIONS TO DRIVE MARKET

- 7.3 COMMERCIAL CHARGING STATIONS

- 7.4 PRIMARY INSIGHTS

8 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COMPONENT

- 8.1 INTRODUCTION

- 8.2 BASE CHARGING PADS

- 8.2.1 SIMPLE DESIGN, RELIABLE PERFORMANCE, AND REDUCED NEED FOR USER INTERACTION TO DRIVE MARKET

- 8.3 POWER CONTROL UNITS

- 8.3.1 INCREASED INVESTMENTS IN WIRELESS CHARGING INFRASTRUCTURE TO DRIVE MARKET

- 8.4 VEHICLE CHARGING PADS

- 8.4.1 RAPID DEPLOYMENT INTO NEWER EV MODELS TO DRIVE MARKET

- 8.5 PRIMARY INSIGHTS

9 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY POWER SUPPLY RANGE

- 9.1 INTRODUCTION

- 9.1.1 POWER SUPPLY RANGE OFFERED BY KEY PLAYERS

- 9.2 <3.7 KW

- 9.2.1 LOWER POWER REQUIREMENT TO DRIVE GROWTH

- 9.3 3.7-7.7 KW

- 9.3.1 FOCUS ON INTEGRATING MID-POWER WIRELESS CHARGING SYSTEMS INTO VEHICLE PLATFORMS TO DRIVE MARKET

- 9.4 7.8-11 KW

- 9.4.1 NEED FOR HIGH-POWER WIRELESS CHARGING IN HEAVY-DUTY OPERATIONS TO DRIVE MARKET

- 9.5 >11 KW

- 9.5.1 EXPANSION OF LOGISTICS AND COMMERCIAL FLEETS TO DRIVE MARKET

- 9.6 PRIMARY INSIGHTS

10 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION

- 10.1 INTRODUCTION

- 10.2 BEV

- 10.2.1 EMPHASIS ON ZERO-EMISSION MOBILITY AND IMPROVEMENTS IN DRIVING RANGE AND BATTERY PERFORMANCE TO DRIVE MARKET

- 10.3 PHEV

- 10.3.1 NEED TO IMPROVE CHARGING CONVENIENCE AND SUPPORT REGULAR TOP-UP CHARGING TO DRIVE MARKET

- 10.4 PRIMARY INSIGHTS

11 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE

- 11.1 INTRODUCTION

- 11.2 PASSENGER CARS

- 11.2.1 CONSUMER DEMAND FOR CONVENIENCE, AUTOMATION, AND SEAMLESS USER EXPERIENCE TO DRIVE MARKET

- 11.3 COMMERCIAL VEHICLES

- 11.3.1 INCREASING ELECTRIFICATION OF PUBLIC TRANSPORT SYSTEMS AND LAST-MILE DELIVERY FLEETS TO DRIVE MARKET

- 11.3.2 ELECTRIC BUSES

- 11.3.3 ELECTRIC VANS

- 11.3.4 ELECTRIC PICKUP TRUCKS

- 11.3.5 ELECTRIC TRUCKS

- 11.4 PRIMARY INSIGHTS

12 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Government subsidies for EV adoption to drive market

- 12.2.2 INDIA

- 12.2.2.1 Strong government backing and regulatory push for electrification to drive market

- 12.2.3 JAPAN

- 12.2.3.1 High demand for electric vehicles and focus on clean mobility to drive market

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Emphasis on penetration of electric vehicles and related charging infrastructure to drive market

- 12.2.1 CHINA

- 12.3 EUROPE

- 12.3.1 FRANCE

- 12.3.1.1 Public transport electrification and low-emission targets to drive market

- 12.3.2 GERMANY

- 12.3.2.1 OEM-led innovation to drive market

- 12.3.3 NETHERLANDS

- 12.3.3.1 Focus on increasing charging infrastructure to drive market

- 12.3.4 NORWAY

- 12.3.4.1 Transition toward electric mobility to drive market

- 12.3.5 SPAIN

- 12.3.5.1 National targets and policy measures focused on decarbonization to drive market

- 12.3.6 SWEDEN

- 12.3.6.1 Emphasis on innovation and clean transport to drive market

- 12.3.7 SWITZERLAND

- 12.3.7.1 Pilot projects and early wireless charging deployments to drive market

- 12.3.8 UK

- 12.3.8.1 Government-funded trials and fleet electrification to drive market

- 12.3.1 FRANCE

- 12.4 NORTH AMERICA

- 12.4.1 CANADA

- 12.4.1.1 Targeted fleet applications to drive market

- 12.4.2 US

- 12.4.2.1 Transit and logistics fleet demand to drive market

- 12.4.1 CANADA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 13.3 MARKET SHARE ANALYSIS, 2025

- 13.4 REVENUE ANALYSIS, 2021-2025

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 BRAND/PRODUCT COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2026

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Charging system footprint

- 13.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2026

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING

- 13.8.5.1 List of start-ups/SMEs

- 13.8.5.2 Competitive benchmarking of start-ups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

- 13.9.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 ELECTREON

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Deals

- 14.1.1.3.2 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 WITRICITY AI TECH, LLC

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches/developments

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.3.4 Other developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 ENRX

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches/developments

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Expansions

- 14.1.3.3.4 Other developments

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 HEVO INC.

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches/developments

- 14.1.4.3.2 Deals

- 14.1.4.3.3 Expansions

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses AND competitive threats

- 14.1.5 PLUGLESS POWER INC.

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches/developments

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 MITSUBISHI ELECTRIC CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.7 TGOOD ELECTRIC CO., LTD.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.8 TOYOTA MOTOR CORPORATION

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Deals

- 14.1.9 ROBERT BOSCH GMBH

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.10 CONTINENTAL AG

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Deals

- 14.1.11 TOSHIBA CORPORATION

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.12 HELLA GMBH & CO. KGAA

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.1 ELECTREON

- 14.2 OTHER PLAYERS

- 14.2.1 IDEANOMICS INC.

- 14.2.2 VOLTERIO GMBH

- 14.2.3 MOJO MOBILITY INC.

- 14.2.4 BMW

- 14.2.5 FORTUM CORPORATION

- 14.2.6 HYUNDAI MOTOR COMPANY

- 14.2.7 PULS GMBH

- 14.2.8 DAIHEN CORPORATION

- 14.2.9 VIE GROUP CO., LTD.

- 14.2.10 IPT TECHNOLOGY GMBH

- 14.2.11 EASELINK GMBH

- 14.2.12 MAHLE GMBH

- 14.2.13 NISSAN MOTOR CO., LTD.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 List of secondary sources

- 15.1.1.2 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Primary interviewees from demand and supply sides

- 15.1.2.2 Breakdown of primary interviews

- 15.1.2.3 List of primary participants

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 DATA TRIANGULATION

- 15.4 FACTOR ANALYSIS

- 15.5 RESEARCH ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

- 15.7 RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.3.1 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY POWER SUPPLY, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 16.3.2 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 16.3.3 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COMPONENT, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 16.3.4 COMPANY INFORMATION

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS

List of Tables

- TABLE 1 MARKET DEFINITION, BY APPLICATION

- TABLE 2 MARKET DEFINITION, BY COMPONENT

- TABLE 3 MARKET DEFINITION, BY CHARGING SYSTEM

- TABLE 4 MARKET DEFINITION, BY CHARGING TYPE

- TABLE 5 MARKET DEFINITION, BY POWER SUPPLY RANGE

- TABLE 6 MARKET DEFINITION, BY VEHICLE TYPE

- TABLE 7 MARKET DEFINITION, BY PROPULSION

- TABLE 8 USD EXCHANGE RATES, 2021-2025

- TABLE 9 ADOPTION OF WIRELESS CHARGING-ENABLED VEHICLES, 2022-2025

- TABLE 10 IMPACT OF MARKET DYNAMICS

- TABLE 11 AVERAGE SELLING PRICE TREND, BY PROPULSION, 2023-2025 (USD)

- TABLE 12 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD)

- TABLE 13 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 14 PATENT ANALYSIS

- TABLE 15 SUPPLIER ECOSYSTEM AND TECHNOLOGY DIFFERENTIATION

- TABLE 16 UTILITY COORDINATION AND SMART GRID INTEGRATION

- TABLE 17 INFRASTRUCTURE REQUIREMENTS FOR DYNAMIC ON-ROAD WIRELESS EV CHARGING SYSTEMS

- TABLE 18 NETHERLANDS: EV INCENTIVES

- TABLE 19 NETHERLANDS: EV CHARGING STATION INCENTIVES

- TABLE 20 GERMANY: EV INCENTIVES

- TABLE 21 GERMANY: EV CHARGING STATION INCENTIVES

- TABLE 22 FRANCE: EV INCENTIVES

- TABLE 23 FRANCE: EV CHARGING STATION INCENTIVES

- TABLE 24 UK: EV INCENTIVES

- TABLE 25 UK: EV CHARGING STATION INCENTIVES

- TABLE 26 CHINA: EV INCENTIVES

- TABLE 27 CHINA: EV CHARGING STATION INCENTIVES

- TABLE 28 US: EV INCENTIVES

- TABLE 29 US: EV CHARGING STATION INCENTIVES

- TABLE 30 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 31 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 32 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 33 KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 34 REGION-WISE EV AND CHARGING STATION SCENARIO

- TABLE 35 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS (%)

- TABLE 36 KEY BUYING CRITERIA

- TABLE 37 OEM-TECHNOLOGY PARTNER MAPPING FOR WIRELESS CHARGING BY VEHICLE MODEL

- TABLE 38 VALUE PROPOSITION FOR WIRELESS VS. WIRED CHARGING

- TABLE 39 PLAYER INTERRELATIONSHIPS: PLATFORM LEADERS VS. SYSTEM PROVIDERS VS. DYNAMIC CHARGING INNOVATORS

- TABLE 40 OEM READINESS AND INTEGRATION STRATEGY

- TABLE 41 DATA MONETIZATION STRATEGIES

- TABLE 42 WIRELESS CHARGING SYSTEM EFFICIENCY VS. COST

- TABLE 43 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY CHARGING SYSTEM, 2022-2025 (UNITS)

- TABLE 44 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY CHARGING SYSTEM, 2026-2032 (UNITS)

- TABLE 45 MAGNETIC POWER TRANSFER: WIRELESS CHARGING SYSTEM MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 46 MAGNETIC POWER TRANSFER: WIRELESS CHARGING SYSTEM MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 47 INDUCTIVE POWER TRANSFER: WIRELESS CHARGING SYSTEM MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 48 INDUCTIVE POWER TRANSFER: WIRELESS CHARGING SYSTEM MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 49 STATIONARY WIRELESS CHARGING FEATURES

- TABLE 50 DYNAMIC WIRELESS CHARGING FEATURES

- TABLE 51 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY APPLICATION, 2022-2025 (UNITS)

- TABLE 52 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY APPLICATION, 2026-2032 (UNITS)

- TABLE 53 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY APPLICATION, 2022-2025 (USD THOUSAND)

- TABLE 54 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY APPLICATION, 2026-2032 (USD THOUSAND)

- TABLE 55 HOME CHARGING UNITS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 56 HOME CHARGING UNITS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 57 HOME CHARGING UNITS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (USD THOUSAND)

- TABLE 58 HOME CHARGING UNITS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (USD THOUSAND)

- TABLE 59 WIRELESS CHARGING ROAD PROJECTS

- TABLE 60 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COMPONENT, 2022-2025 (USD THOUSAND)

- TABLE 61 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COMPONENT, 2026-2032 (USD THOUSAND)

- TABLE 62 BASE CHARGING PADS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (USD THOUSAND)

- TABLE 63 BASE CHARGING PADS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (USD THOUSAND)

- TABLE 64 POWER CONTROL UNITS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (USD THOUSAND)

- TABLE 65 POWER CONTROL UNITS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (USD THOUSAND)

- TABLE 66 VEHICLE CHARGING PADS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (USD THOUSAND)

- TABLE 67 VEHICLE CHARGING PADS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (USD THOUSAND)

- TABLE 68 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY POWER SUPPLY RANGE, 2022-2025 (UNITS)

- TABLE 69 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY POWER SUPPLY RANGE, 2026-2032 (UNITS)

- TABLE 70 <3.7 KW: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 71 <3.7 KW: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 72 3.7-7.7 KW: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 73 3.7-7.7 KW: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 74 7.8-11 KW: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 75 7.8-11 KW: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 76 >11 KW: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 77 >11 KW: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 78 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 79 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 80 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION 2022-2025 (USD THOUSAND)

- TABLE 81 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 82 BEV: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 83 BEV: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 84 BEV: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (USD THOUSAND)

- TABLE 85 BEV: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (USD THOUSAND)

- TABLE 86 PHEV: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 87 PHEV: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 88 PHEV: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (USD THOUSAND)

- TABLE 89 PHEV: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (USD THOUSAND)

- TABLE 90 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE, 2022-2025 (UNITS)

- TABLE 91 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE, 2026-2032 (UNITS)

- TABLE 92 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE, 2022-2025 (USD THOUSAND)

- TABLE 93 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE, 2026-2032 (USD THOUSAND)

- TABLE 94 PASSENGER CARS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 95 PASSENGER CARS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 96 PASSENGER CARS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (USD THOUSAND)

- TABLE 97 PASSENGER CARS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (USD THOUSAND)

- TABLE 98 COMMERCIAL VEHICLES: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 99 COMMERCIAL VEHICLES: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 100 COMMERCIAL VEHICLES: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (USD THOUSAND)

- TABLE 101 COMMERCIAL VEHICLES: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (USD THOUSAND)

- TABLE 102 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (UNITS)

- TABLE 103 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (UNITS)

- TABLE 104 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2022-2025 (USD THOUSAND)

- TABLE 105 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026-2032 (USD THOUSAND)

- TABLE 106 ASIA PACIFIC: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2022-2025 (UNITS)

- TABLE 107 ASIA PACIFIC: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2026-2032 (UNITS)

- TABLE 108 ASIA PACIFIC: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2022-2025 (USD THOUSAND)

- TABLE 109 ASIA PACIFIC: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2026-2032 (USD THOUSAND)

- TABLE 110 CHINA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 111 CHINA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 112 CHINA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 113 CHINA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 114 INDIA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 115 INDIA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 116 JAPAN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 117 JAPAN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 118 JAPAN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 119 JAPAN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 120 SOUTH KOREA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 121 SOUTH KOREA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 122 SOUTH KOREA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 123 SOUTH KOREA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 124 EUROPE: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2022-2025 (UNITS)

- TABLE 125 EUROPE: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2026-2032 (UNITS)

- TABLE 126 EUROPE: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2022-2025 (USD THOUSAND)

- TABLE 127 EUROPE: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2026-2032 (USD THOUSAND)

- TABLE 128 FRANCE: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 129 FRANCE: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 130 FRANCE: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 131 FRANCE: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 132 GERMANY: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 133 GERMANY: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 134 GERMANY: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 135 GERMANY: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 136 NETHERLANDS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 137 NETHERLANDS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 138 NETHERLANDS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 139 NETHERLANDS: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 140 NORWAY: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 141 NORWAY: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 142 NORWAY: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 143 NORWAY: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 144 SPAIN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 145 SPAIN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 146 SPAIN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 147 SPAIN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 148 SWEDEN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 149 SWEDEN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 150 SWEDEN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 151 SWEDEN: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 152 SWITZERLAND: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 153 SWITZERLAND: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 154 SWITZERLAND: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 155 SWITZERLAND: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 156 UK: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 157 UK: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 158 UK: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 159 UK: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 160 NORTH AMERICA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2022-2025 (UNITS)

- TABLE 161 NORTH AMERICA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2026-2032 (UNITS)

- TABLE 162 NORTH AMERICA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2022-2025 (USD THOUSAND)

- TABLE 163 NORTH AMERICA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COUNTRY, 2026-2032 (USD THOUSAND)

- TABLE 164 CANADA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 165 CANADA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 166 CANADA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 167 CANADA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 168 US: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (UNITS)

- TABLE 169 US: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (UNITS)

- TABLE 170 US: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2022-2025 (USD THOUSAND)

- TABLE 171 US: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026-2032 (USD THOUSAND)

- TABLE 172 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- TABLE 173 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2025

- TABLE 174 REGION FOOTPRINT

- TABLE 175 CHARGING SYSTEM FOOTPRINT

- TABLE 176 LIST OF START-UPS/SMES

- TABLE 177 COMPETITIVE BENCHMARKING OF START-UPS/SMES

- TABLE 178 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES: PRODUCT LAUNCHES/DEVELOPMENTS, 2022-2026

- TABLE 179 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES: DEALS, 2022-2026

- TABLE 180 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES: EXPANSIONS, 2022-2026

- TABLE 181 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES: OTHER DEVELOPMENTS, 2022-2026

- TABLE 182 ELECTREON: COMPANY OVERVIEW

- TABLE 183 ELECTREON: PRODUCTS OFFERED

- TABLE 184 ELECTREON: DEALS

- TABLE 185 ELECTREON: OTHER DEVELOPMENTS

- TABLE 186 WITRICITY AI TECH, LLC: COMPANY OVERVIEW

- TABLE 187 WITRICITY AI TECH, LLC: PRODUCTS OFFERED

- TABLE 188 WITRICITY AI TECH, LLC: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 189 WITRICITY AI TECH, LLC: DEALS

- TABLE 190 WITRICITY AI TECH, LLC.: EXPANSIONS

- TABLE 191 WITRICITY AI TECH, LLC: OTHER DEVELOPMENTS

- TABLE 192 ENRX: COMPANY OVERVIEW

- TABLE 193 ENRX: PRODUCTS OFFERED

- TABLE 194 ENRX: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 195 ENRX: DEALS

- TABLE 196 ENRX: EXPANSIONS

- TABLE 197 ENRX: OTHER DEVELOPMENTS

- TABLE 198 HEVO INC.: COMPANY OVERVIEW

- TABLE 199 HEVO INC.: PRODUCTS OFFERED

- TABLE 200 HEVO INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 201 HEVO INC.: DEALS

- TABLE 202 HEVO INC.: EXPANSIONS

- TABLE 203 PLUGLESS POWER INC.: COMPANY OVERVIEW

- TABLE 204 PLUGLESS POWER INC.: PRODUCTS OFFERED

- TABLE 205 PLUGLESS POWER INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 206 PLUGLESS POWER INC.: DEALS

- TABLE 207 MITSUBISHI ELECTRIC CORPORATION: COMPANY OVERVIEW

- TABLE 208 MITSUBISHI ELECTRIC CORPORATION: PRODUCTS OFFERED

- TABLE 209 TGOOD ELECTRIC CO., LTD.: COMPANY OVERVIEW

- TABLE 210 TGOOD ELECTRIC CO., LTD.: PRODUCTS OFFERED

- TABLE 211 TOYOTA MOTOR CORPORATION: COMPANY OVERVIEW

- TABLE 212 TOYOTA MOTOR CORPORATION: PRODUCTS OFFERED

- TABLE 213 TOYOTA MOTOR CORPORATION: DEALS

- TABLE 214 ROBERT BOSCH GMBH: COMPANY OVERVIEW

- TABLE 215 ROBERT BOSCH GMBH: PRODUCTS OFFERED

- TABLE 216 CONTINENTAL AG.: COMPANY OVERVIEW

- TABLE 217 CONTINENTAL AG: PRODUCTS OFFERED

- TABLE 218 CONTINENTAL AG: DEALS

- TABLE 219 TOSHIBA CORPORATION: COMPANY OVERVIEW

- TABLE 220 TOSHIBA CORPORATION: PRODUCTS OFFERED

- TABLE 221 HELLA GMBH & CO. KGAA: COMPANY OVERVIEW

- TABLE 222 HELLA GMBH & CO. KGAA: PRODUCTS OFFERED

- TABLE 223 IDEANOMICS INC.: COMPANY OVERVIEW

- TABLE 224 VOLTERIO GMBH: COMPANY OVERVIEW

- TABLE 225 MOJO MOBILITY INC.: COMPANY OVERVIEW

- TABLE 226 BMW: COMPANY OVERVIEW

- TABLE 227 FORTUM CORPORATION: COMPANY OVERVIEW

- TABLE 228 HYUNDAI MOTOR COMPANY: COMPANY OVERVIEW

- TABLE 229 PULS GMBH: COMPANY OVERVIEW

- TABLE 230 DAIHEN CORPORATION: COMPANY OVERVIEW

- TABLE 231 VIE GROUP CO., LTD.: COMPANY OVERVIEW

- TABLE 232 IPT TECHNOLOGY GMBH: COMPANY OVERVIEW

- TABLE 233 EASELINK GMBH: COMPANY OVERVIEW

- TABLE 234 MAHLE GMBH: COMPANY OVERVIEW

- TABLE 235 NISSAN MOTOR CO., LTD.: COMPANY OVERVIEW

List of Figures

- FIGURE 1 MARKET SCENARIO

- FIGURE 2 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026 VS. 2032

- FIGURE 3 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026 VS. 2032

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLE, 2022-2026

- FIGURE 5 DISRUPTIONS INFLUENCING GROWTH OF WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES

- FIGURE 6 HIGH-GROWTH SEGMENTS IN WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, 2026-2032

- FIGURE 7 GOVERNMENT SUPPORT AND FLEET ELECTRIFICATION TO DRIVE MARKET

- FIGURE 8 PASSENGER CARS TO CAPTURE HIGHER SHARE THAN COMMERCIAL VEHICLES IN 2026

- FIGURE 9 PHEV TO REGISTER FASTER DEMAND FOR WIRELESS CHARGERS DURING FORECAST PERIOD

- FIGURE 10 >11 KW TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 11 INDUCTIVE POWER TRANSFER SEGMENT TO BE LARGER THAN MAGNETIC POWER TRANSFER SEGMENT IN 2026

- FIGURE 12 VEHICLE CHARGING PADS SEGMENT TO BE DOMINANT DURING FORECAST PERIOD

- FIGURE 13 EUROPE TO EXHIBIT FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 14 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES DYNAMICS

- FIGURE 15 SYSTEM LAYOUT OF WIRELESS CHARGING INFRASTRUCTURE

- FIGURE 16 EFFICIENCY OF WIRED AND WIRELESS CHARGING

- FIGURE 17 AVERAGE SELLING PRICE TREND, BY PROPULSION, 2023-2025 (USD)

- FIGURE 18 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD)

- FIGURE 19 ECOSYSTEM ANALYSIS

- FIGURE 20 VALUE CHAIN ANALYSIS

- FIGURE 21 INVESTMENT AND FUNDING SCENARIO, 2021-2025

- FIGURE 22 PATENT ANALYSIS

- FIGURE 23 BIDIRECTIONAL EV CHARGING ENERGY FLOW CYCLE

- FIGURE 24 EV SHIFT AND GLOBAL TARGETS

- FIGURE 25 NATIONAL SUBSIDIES FOR ELECTRIC VEHICLE PURCHASE, 2025

- FIGURE 26 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS

- FIGURE 27 KEY BUYING CRITERIA

- FIGURE 28 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 29 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY CHARGING SYSTEM, 2026 VS. 2032 (UNITS)

- FIGURE 30 MAGNETIC RESONANCE TECHNOLOGY FOR ELECTRIC VEHICLES

- FIGURE 31 INDUCTIVE POWER TRANSFER FOR ELECTRIC VEHICLES

- FIGURE 32 WIRELESS CHARGING SOLUTION BY IPT TECHNOLOGY IN EUROPE

- FIGURE 33 CAPACITIVE POWER TRANSFER FOR ELECTRIC VEHICLES

- FIGURE 34 STATIONARY WIRELESS CHARGING TECHNOLOGY

- FIGURE 35 DYNAMIC WIRELESS CHARGING TECHNOLOGY

- FIGURE 36 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COMPONENT, 2026 VS. 2032 (USD THOUSAND)

- FIGURE 37 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY POWER SUPPLY RANGE, 2026 VS. 2032 (UNITS)

- FIGURE 38 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION, 2026 VS. 2032 (USD THOUSAND)

- FIGURE 39 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE, 2026 VS. 2032 (USD THOUSAND)

- FIGURE 40 OPERATING CONDITIONS OF WIRELESS-CHARGED DOUBLE-DECKER BUSES

- FIGURE 41 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION, 2026 VS. 2032 (USD THOUSAND)

- FIGURE 42 ASIA PACIFIC: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES SNAPSHOT

- FIGURE 43 EUROPE: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES SNAPSHOT

- FIGURE 44 NORTH AMERICA: WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES SNAPSHOT

- FIGURE 45 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2025

- FIGURE 46 REVENUE ANALYSIS OF TOP-LISTED/PUBLIC PLAYERS, 2021-2025 (USD BILLION)

- FIGURE 47 COMPANY VALUATION (USD BILLION)

- FIGURE 48 FINANCIAL METRICS (EV/EBITDA)

- FIGURE 49 BRAND/PRODUCT COMPARISON

- FIGURE 50 COMPANY EVALUATION MATRIX (KEY PLAYERS), 2026

- FIGURE 51 COMPANY FOOTPRINT

- FIGURE 52 COMPANY EVALUATION MATRIX (START-UPS/SMES), 2026

- FIGURE 53 ELECTREON: COMPANY SNAPSHOT

- FIGURE 54 EV OWNERS' INTEREST IN WIRELESS CHARGING

- FIGURE 55 EV OWNERS' OPINION ABOUT WIRELESS CHARGING

- FIGURE 56 MITSUBISHI ELECTRIC CORPORATION: COMPANY SNAPSHOT

- FIGURE 57 TOYOTA MOTOR CORPORATION: COMPANY SNAPSHOT

- FIGURE 58 ROBERT BOSCH GMBH: COMPANY SNAPSHOT

- FIGURE 59 CONTINENTAL AG: BUSINESS LOCATIONS AND EMPLOYEES

- FIGURE 60 CONTINENTAL AG: COMPANY SNAPSHOT

- FIGURE 61 TOSHIBA CORPORATION: COMPANY SNAPSHOT

- FIGURE 62 HELLA GMBH & CO. KGAA: COMPANY SNAPSHOT

- FIGURE 63 RESEARCH DESIGN

- FIGURE 64 RESEARCH DESIGN MODEL

- FIGURE 65 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 66 BOTTOM-UP APPROACH

- FIGURE 67 TOP-DOWN APPROACH

- FIGURE 68 DATA TRIANGULATION

- FIGURE 69 FACTOR ANALYSIS FOR MARKET SIZING: DEMAND AND SUPPLY SIDES

Qi無線充電-2026-2032年全球市佔率及排名、總收入及需求預測

Qi無線充電-2026-2032年全球市佔率及排名、總收入及需求預測 無線充電市場-2026-2032年全球市場預測家用電子電器無線充電市場:依產品、組件、技術、銷售管道和應用分類-2026-2032年全球市場預測

無線充電市場-2026-2032年全球市場預測家用電子電器無線充電市場:依產品、組件、技術、銷售管道和應用分類-2026-2032年全球市場預測 無線充電市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年

無線充電市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年 無線充電市場:未來預測(至2034年)-按組件、充電方式、技術、應用、最終用戶和地區分類的全球分析

無線充電市場:未來預測(至2034年)-按組件、充電方式、技術、應用、最終用戶和地區分類的全球分析 無線充電市場報告:按技術、傳輸距離、應用和地區分類,2026-2034年

無線充電市場報告:按技術、傳輸距離、應用和地區分類,2026-2034年 無線充電市場:按組件、技術、應用和地區分類

無線充電市場:按組件、技術、應用和地區分類 2026年全球無線充電市場報告

2026年全球無線充電市場報告 無線充電市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、設備、最終用戶、安裝類型及解決方案分類

無線充電市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、設備、最終用戶、安裝類型及解決方案分類 全球無線充電市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球無線充電市場規模、佔有率、趨勢和成長分析報告(2026-2034年)