|

市場調查報告書

商品編碼

2034859

全球醫療保健產業數位雙胞胎市場(至2031年):按組件(軟體和服務)、應用(個人化醫療、藥物研發、醫學教育、工作流程最佳化)、最終用戶(醫療服務提供者、研究和學術機構、保險公司)和地區分類Digital Twins in Healthcare Market By Component (Software, Services), Application (Personalized Medicine, Drug Discovery, Medical Education, Workflow Optimization), End User (Providers, Research & Academia, Payers), and Region - Global Forecast to 2031 |

||||||

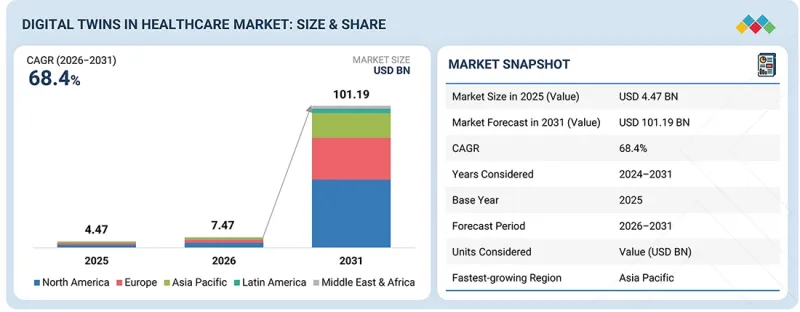

預計到 2025 年,全球醫療保健領域的數位雙胞胎市場將迎來顯著成長,這主要得益於醫療保健領域對數位雙胞胎的日益普及以及公共和私人投資的增加。

預計數位孿生市場規模將從2026年的74.7億美元成長到2031年的1,011.9億美元,預測期內複合年成長率(CAGR)為68.4%。由於其創新潛力,眾多公共和私營機構正在投資數位雙胞胎。

| 調查範圍 | |

|---|---|

| 調查期 | 2026-2031 |

| 基準年 | 2025 |

| 預測期 | 2026-2031 |

| 單元 | 金額(美元) |

| 部分 | 元件、類型、應用程式、最終用戶 |

| 目標區域 | 北美、歐洲、亞太地區、拉丁美洲、中東和非洲 |

總部位於瓦倫西亞的Quibim公司致力於推進影像生物標記在精準醫療上的應用。該公司宣布已成功資金籌措,旨在進軍美國市場。 Quibim表示,這標誌著其在人體數位雙胞胎是一種動態模型,能夠監測人體健康狀況,同時促進藥物的高效研發。

“按應用領域分類,預計在預測期內,外科手術規劃和醫學教育領域將佔第二大佔有率。”

該市場的成長得益於數位雙胞胎與虛擬實境(VR)應用的融合,使住院醫師能夠模擬和訓練針對每位患者特定解剖和生理特徵量身定做的手術流程。這有助於在實際臨床環境中重現手術操作,並便於評估術中指標。許多公司正在模擬人體解剖結構和手術流程,以減少對捐贈遺體的依賴。

“按組件分類,預計軟體在預測期內將實現最快成長。”

該領域的成長主要得益於數位雙胞胎平台的日益普及,這些平台能夠提供即時模擬和預測分析。醫療和研究機構越來越依賴軟體數位孿生解決方案,基於影像技術、電子健康記錄和穿戴式互聯設備收集的信息,構建患者、器官和醫療設施的虛擬模型。軟體數位雙胞胎數位雙胞胎不僅能夠實現持續監測,還能預測疾病進展並制定個人化治療方案。人工智慧和雲端運算平台的日益普及也推動了人們對數位雙胞胎技術和軟體解決方案的興趣。此外,以價值為導向的醫療和精準醫療的發展趨勢預計將進一步提升對數位雙胞胎軟體解決方案的需求。同時,對數位健康解決方案的持續投資以及建構能夠與醫院IT基礎設施相容的互通性操作系統的需求,也促進了這一成長。

“預計亞太地區在預測期內將錄得最高的成長率。”

亞太市場正快速成長,這主要得益於臨床研究活動的活性化以及醫療服務提供者對數位技術的應用。該地區正崛起為重要的研究中心,印度、日本、韓國和澳洲等國家由於法規環境的改善和成本結構的降低,正在不斷增強其在該領域的影響力。製藥和生物技術公司擴大參與利用數據和模擬的舉措項目,進一步推動了數位雙胞胎技術的應用。同時,包括人工智慧、雲端運算和醫療資訊技術系統在內的數位醫療基礎設施建設也獲得了大量投資,這些對於數位數位雙胞胎技術的實施至關重要。此外,亞太地區各國政府正致力於推動醫療產業的數位轉型,以提高效率和績效。例如,日本富士通有限公司開發了一種基於人工智慧的類比平台,用於個人化醫療和臨床決策,為醫療產業提供數位雙胞胎技術。

本報告考察了全球醫療保健領域的數位雙胞胎市場,提供了市場概述、影響市場成長的各種因素分析、技術和專利趨勢、法律制度、案例研究、歷史和預測的市場規模、按各個細分市場和地區/主要國家/地區進行的詳細分析、競爭格局以及主要公司的概況。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求和閒置頻段

- 與相關市場和不同產業相關的跨領域機遇

- 一級/二級/三級公司的策略性舉措

第5章 產業趨勢

- 波特五力分析

- 總體經濟指標

- GDP趨勢與預測

- 全球醫療保健IT產業趨勢

- 價值鏈分析

- 生態系分析

- 價格分析

- 2026-2027 年主要會議和活動

- 影響客戶業務的趨勢/顛覆性因素

- 投資和資金籌措場景

- 案例研究分析

- 2025年美國關稅的影響-醫療保健產業的數位雙胞胎市場

第6章:透過科技、專利、數位技術和人工智慧實施實現策略顛覆

- 主要新興技術

- 人工智慧/機器學習與模擬模型

- 雲端運算和高效能運算

- 數據整合平台

- 互補技術

- 醫療物聯網和互聯設備

- 醫療圖像處理和影像人工智慧

- 鄰近技術

- 臨床決策支援系統

- 用於手術模擬和培訓的擴增實境/虛擬實境技術

- 技術/產品藍圖

- 專利分析

- 未來應用

- 人工智慧驅動的預測建模和臨床決策支持

- 虛擬治療模擬與個人化干涉

- 虛擬臨床試驗和醫療保健系統最佳化

- 人口健康管理與疫情應對模型

- 人工智慧/生成式人工智慧對市場的影響

第7章 監理情勢

- 當地法規和合規性

第8章:顧客趨勢與購買行為

- 決策流程

- 買方相關利益者和採購評估標準

- 實施障礙和內部挑戰

- 各個終端用戶產業中尚未滿足的需求

- 市場盈利

第9章:醫療保健產業的數位雙胞胎市場:按組件分類

- 服務

- 軟體

第10章:醫療保健產業的數位雙胞胎市場:按類型分類

- 流程孿生

- 系統雙胞胎

- 全身雙胞胎

- 身體部位雙胞胎

第11章:醫療保健產業的數位雙胞胎市場:按應用領域分類

- 藥物發現與開發

- 個人化醫療

- 手術計劃和醫學教育

- 醫療設備的設計與測試

- 最佳化醫療工作流程與資產管理

- 其他

第12章:醫療保健產業數位雙胞胎市場:依最終用戶分類

- 製藥和生物製藥公司

- 研究和學術機構

- 醫護人員

- 醫療設備公司

- 其他

第13章:醫療保健產業的數位雙胞胎市場:按地區分類

- 北美洲

- 宏觀經濟展望

- 美國

- 加拿大

- 歐洲

- 宏觀經濟展望

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他

- 亞太地區

- 宏觀經濟展望

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 其他

- 拉丁美洲

- 宏觀經濟展望

- 巴西

- 墨西哥

- 其他

- 中東和非洲

- 宏觀經濟展望

- 海灣合作理事會國家

- 南非

- 其他

第14章 競爭格局

- 概述

- 主要參與企業的策略/優勢

- 主要公司的收入佔有率分析

- 市佔率分析

- 品牌/產品對比

- 評估和財務指標

- 企業估值象限:主要公司

- 公司估值矩陣:新創企業/中小企業

- 競爭格局

第15章:公司簡介

- 大公司

- MICROSOFT

- SIEMENS HEALTHINEERS AG

- KONINKLIJKE PHILIPS NV

- DASSAULT SYSTEMES

- AMAZON WEB SERVICES, INC.

- GE HEALTHCARE

- ORACLE

- IBM

- PTC

- SAP

- ATOS SE

- NVIDIA CORPORATION

- ANSYS INC.

- FASTSTREAM TECHNOLOGIES

- RESCALE, INC.

- 其他公司

- TWIN HEALTH

- VERTO HEALTH

- QBIO

- THOUGHTWIRE

- SIM&CURE

- OWKIN, INC

- NUREA

- UNLEARN.AI, INC.

- VIRTONOMY GMBH

- PREDISURGE

第16章調查方法

第17章附錄

The global digital twin healthcare market is experiencing significant growth in 2025, driven by the increasing adoption of digital twins in healthcare and rising investments by public & private entities. The market is projected to reach USD 101.19 billion by 2031 from USD 7.47 billion in 2026, at a CAGR of 68.4% during the forecast period. There have been many investments in digital twins by both public and private organizations due to their innovation potential.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Component, Type, Application, and End user. |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. |

For instance, Quibim, based in Valencia, is developing the use of imaging biomarkers in precision medicine. Quibim has made an announcement on its successful raising of funds amounting to USD 50.6 million as part of its series A investment round to establish a footprint in the USA market. According to Quibim, this will be a milestone in developing human digital twins. These are dynamic models that will make it possible to monitor the well-being of people while ensuring that drugs are developed efficiently.

"Surgical planning & medical education segment accounted for the second-largest share of the market during the forecast period, by application."

In 2025, the surgical planning & medical education segment accounted for the second-largest share of the digital twin in the healthcare market. The growth in this market was driven by the ability of digital twins to work with virtual reality applications that enable the residents to train by simulating surgical processes for the specific anatomical and physiological profile of the patients. This helps in generating a real-life performance depiction and facilitates the evaluation of the intraoperative metrics. Many companies have simulated human anatomy and surgery processes in order to reduce reliance on cadavers.

"By component, software accounted for the fastest growth during the forecast period."

Based on component, software is projected to witness the fastest growth in the digital twins in healthcare market during the forecast period. The reason behind such growth is associated with the rising number of adoptions of digital twin platforms in order to offer real-time simulation and predictive analytics. In particular, healthcare organizations and research institutions will start relying on software digital twin solutions to develop virtual models of patients, organs, and healthcare facilities based on information collected via imaging techniques, electronic health records, and wearable connected devices. Software digital twin solutions enable not only continuous monitoring but also predicting disease progression and creating personalized treatment plans. Rising interest in digital twin technology and software solutions is also explained by the growing adoption of platforms based on AI and cloud computing. In addition, the rising trend towards value-based care and precision medicine is anticipated to boost demand for digital twin software solutions. Furthermore, the ongoing investments in digital health solutions and the necessity of building interoperable systems capable of interacting with the IT infrastructures of hospitals contribute to such growth.

"Asia Pacific to witness the highest growth rate during the forecast period."

The market for digital twins in healthcare in the Asia Pacific region is growing at a fast pace, owing to increased clinical research activities and the adoption of digital technologies by healthcare providers. Asia Pacific has emerged as one of the major hubs for research activities, where countries like India, Japan, South Korea, and Australia have become prominent owing to improved regulation and lower cost structure. Pharmaceutical and biotechnology companies are increasingly engaging in research initiatives through the use of data and simulations, which is further driving the adoption of digital twin technologies. At the same time, significant investment is being made towards the development of digital health infrastructure in the form of artificial intelligence, cloud computing, and health IT systems, which are vital for the implementation of digital twin technologies. Furthermore, governments in the Asia Pacific region are working towards the digitalization of the healthcare industry to improve efficiency and performance. There have been recent developments in this regard. For example, the Japanese company Fujitsu Limited has developed digital twin technology in the healthcare sector using artificial intelligence-based simulation platforms for personalized medicine and decision-making in clinical processes.

The breakdown of primary participants is as follows:

- By Company Type - Tier 1: 45%, Tier 2: 30%, and Tier 3: 25%

- By Designation - C-level: 42%, Director-level: 31%, and Others: 27%

- By Region - North America: 45%, Europe: 30%, Asia Pacific: 20%, Latin America: 3%, and Middle East & Africa: 2%.

The key players operating in the digital twin in healthcare market include Microsoft Corporation (US), Siemens Healthineers AG (Germany), Koninklijke Philips N.V. (Netherlands), Amazon Web Services, Inc. (US), Dassault Systemes (France), GE Healthcare (US), IBM (US), NVIDIA Corporation (US), Oracle Corporation (US), PTC (US), SAP (Germany), Atos SE (France), ANSYS, Inc. (US), Faststream Technologies (US), Rescale, Inc. (US), Twin Health (US), NUREA (France), Predictiv (US), Verto (Canada), Qbio (US), Virtonomy GmbH (Germany), Unlearn.ai, Inc. (US), ThoughtWire (Canada), Sim and Cure (France), and PrediSurge (France).

- The study includes an in-depth competitive analysis of these key players in the digital twin in healthcare market, with their company profiles, recent developments, and key market strategies.

Research Coverage

The report analyzes the digital twins in healthcare market and aims to estimate the market size and future growth potential of various market segments, based on components, application, end user, and region. The report also provides a competitive analysis of the key players operating in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to buy this report

This report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the following strategies to strengthen their positions in the market.

This report provides insights into:

- Analysis of key drivers (increasing Investments in digital twins in developed as well as emerging technology adoption, rising demand for personalized medicine, increasing funding and investments in digital twin startups), restraints (accuracy and privacy issues with digital twin systems and high implementation costs), opportunities (growing importance of digital twin Iin emerging market, increasing focus on cutting edge real-time data analytics), and challenges (lack of technical expertise & data management issues) influencing the growth of the digital twin market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the digital twins in healthcare market

- Market Development: Comprehensive information on the lucrative emerging markets, components, applications, end users, and regions

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the digital twins in healthcare market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players in the digital twins in healthcare market like Microsoft Corporation (US), Siemens Healthineers AG (Germany), Koninklijke Philips N.V. (Netherlands), Amazon Web Services, Inc. (US), Dassault Systemes (France), GE Healthcare (US), IBM (US), NVIDIA Corporation (US), Oracle Corporation (US), PTC (US), SAP (Germany), Atos SE (France), ANSYS, Inc. (US), Faststream Technologies (US), Rescale, Inc. (US), Twin Health (US), NUREA (France), Predictiv (US), Verto (Canada), Qbio (US), Virtonomy GmbH (Germany), Unlearn.ai, Inc. (US), ThoughtWire (Canada), Sim and Cure (France), and PrediSurge (France)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 DIGITAL TWINS IN HEALTHCARE MARKET OVERVIEW

- 3.2 DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT & REGION

- 3.3 DIGITAL TWINS IN HEALTHCARE MARKET: REGIONAL SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing investments by public and private entities

- 4.2.1.2 Growing applications of digital twins

- 4.2.1.3 Technological advancements

- 4.2.1.4 Growing funding and investments in digital twin startups

- 4.2.2 RESTRAINTS

- 4.2.2.1 Managing data quality, privacy issues, and high implementation costs

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing focus on cutting-edge real-time data analytics

- 4.2.3.2 Growing importance of digital twins in emerging economies

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of skilled professionals

- 4.2.4.2 Integration with existing systems and outdated digital infrastructure

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY (HIGH)

- 5.1.2 BARGAINING POWER OF SUPPLIERS (LOW)

- 5.1.3 BARGAINING POWER OF BUYERS (HIGH)

- 5.1.4 THREAT OF NEW ENTRANTS (LOW)

- 5.1.5 THREAT OF SUBSTITUTES (LOW)

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH & PRODUCT DEVELOPMENT

- 5.3.2 TECHNOLOGY INPUTS AND INFRASTRUCTURE

- 5.3.3 PLATFORM DEVELOPMENT AND INTEGRATION

- 5.3.4 DISTRIBUTION

- 5.3.5 MARKETING AND SALES

- 5.3.6 POST-SALE SERVICES

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE FOR DIGITAL TWIN IN HEALTHCARE MARKET, BY TYPE (2025)

- 5.5.2 INDICATIVE PRICE FOR DIGITAL TWIN IN HEALTHCARE MARKET, BY REGION (2025)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.10 IMPACT OF 2025 US TARIFF - DIGITAL TWIN IN HEALTHCARE MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END USERS

- 5.10.5.1 Pharma & biopharma companies

- 5.10.5.2 Research & academia

- 5.10.5.3 Healthcare providers

- 5.10.5.4 Medical device companies

- 5.10.5.5 Other end users

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 AI/ML AND SIMULATION MODELS

- 6.1.2 CLOUD COMPUTING AND HIGH-PERFORMANCE COMPUTING

- 6.1.3 DATA INTEGRATION PLATFORMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INTERNET OF MEDICAL THINGS (IOMT) AND CONNECTED DEVICES

- 6.2.2 MEDICAL IMAGING AND IMAGING AI

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CLINICAL DECISION SUPPORT SYSTEMS

- 6.3.2 AR/VR FOR SURGICAL SIMULATION AND TRAINING

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR DIGITAL TWIN IN HEALTHCARE MARKET

- 6.5.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN PREDICTIVE MODELING AND CLINICAL DECISION SUPPORT

- 6.6.2 VIRTUAL THERAPEUTIC SIMULATION AND PERSONALIZED INTERVENTIONS

- 6.6.3 VIRTUAL CLINICAL TRIALS AND HEALTH SYSTEM OPTIMIZATION

- 6.6.4 POPULATION HEALTH MANAGEMENT AND PANDEMIC RESPONSE MODELING

- 6.7 IMPACT OF AI/GEN AI ON DIGITAL TWIN IN HEALTHCARE MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 MARKET POTENTIAL OF AI/GEN AI IN DIGITAL TWIN IN HEALTHCARE MARKET

- 6.7.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.7.3.1 AI-driven cardiac digital twin for personalized treatment planning

- 6.7.4 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 6.7.4.1 Digital twin analytics & AI-driven simulation platforms

- 6.7.4.2 Digital twin platform integration & regulatory infrastructure

- 6.7.4.3 Clinical care, virtual monitoring & personalized therapeutics

- 6.7.5 USER READINESS AND IMPACT ASSESSMENT

- 6.7.5.1 User readiness

- 6.7.5.1.1 User A: Pharma & biopharma companies

- 6.7.5.1.2 User B: Research & academia

- 6.7.5.2 Impact assessment

- 6.7.5.2.1 User A: Pharma & biopharma companies

- 6.7.5.2.2 User B: Research & academia

- 6.7.5.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Latin America

- 7.1.2.5 Middle East & Africa

- 7.1.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5.1 UNMET NEEDS

- 8.5.2 END USER EXPECTATIONS

- 8.6 MARKET PROFITABILITY

9 DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 SERVICES

- 9.2.1 INTRODUCTION OF COMPLEX SOFTWARE TO DRIVE DEMAND FOR SERVICES

- 9.3 SOFTWARE

- 9.3.1 SHIFT TO WEB/CLOUD-BASED MODELS TO SUPPORT GROWTH

10 DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 PROCESS TWINS

- 10.2.1 RISING DEMAND FOR HEALTHCARE WORKFLOWS AND OPERATIONAL PROCESSES TO BOOST ADOPTION

- 10.3 SYSTEM TWINS

- 10.3.1 INCREASED DEMAND FOR OPERATIONAL EFFICIENCY IN HOSPITALS TO BOOST SEGMENT

- 10.4 WHOLE BODY TWINS

- 10.4.1 ADVANCEMENTS IN AI AND ML TECHNOLOGIES TO BOOST MARKET

- 10.5 BODY PART TWINS

- 10.5.1 RISING DEMAND FOR PERSONALIZED & PRECISION MEDICINE TO FUEL MARKET GROWTH

11 DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 DRUG DISCOVERY & DEVELOPMENT

- 11.2.1 ABILITY OF DIGITAL TWINS TO ENHANCE DRUG DISCOVERY & DEVELOPMENT TO BOOST MARKET

- 11.3 PERSONALIZED MEDICINE

- 11.3.1 QUICK AND COST-EFFECTIVE DEVELOPMENT AND TESTING OF PERSONALIZED DIAGNOSTICS TO SUPPORT MARKET

- 11.4 SURGICAL PLANNING & MEDICAL EDUCATION

- 11.4.1 ABILITY TO ENHANCE SURGICAL TRAINING AND SIMULATE SURGICAL PROCEDURES TO BOOST ADOPTION

- 11.5 MEDICAL DEVICE DESIGN & TESTING

- 11.5.1 POTENTIAL OF DIGITAL TWINS TO STREAMLINE OPERATIONS, MINIMIZE RISK, AND REDUCE DOWNTIME TO PROMOTE USE

- 11.6 HEALTHCARE WORKFLOW OPTIMIZATION & ASSET MANAGEMENT

- 11.6.1 IMPROVED EFFICIENCY AND VALUABLE INSIGHTS TO SUPPORT DEMAND

- 11.7 OTHER APPLICATIONS

12 DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 PHARMA & BIOPHARMA COMPANIES

- 12.2.1 RISING DEMAND TO REDUCE TIME AND COST OF DRUG DEVELOPMENT TO BOOST ADOPTION

- 12.3 RESEARCH & ACADEMIA

- 12.3.1 INTERACTIVE AND IMMERSIVE LEARNING EXPERIENCES OFFERED BY DIGITAL TWINS TO BOOST ADOPTION

- 12.4 HEALTHCARE PROVIDERS

- 12.4.1 LOWER COSTS AND BETTER PATIENT TREATMENT TO FAVOR MARKET GROWTH

- 12.5 MEDICAL DEVICE COMPANIES

- 12.5.1 GROWING USE OF DIGITAL TWINS FOR SOFTWARE OPTIMIZATION OF MEDICAL DEVICES TO FUEL GROWTH

- 12.6 OTHER END USERS

13 DIGITAL TWINS IN HEALTHCARE MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 US

- 13.2.2.1 Expanding applications of digital twins in healthcare to bolster market growth

- 13.2.3 CANADA

- 13.2.3.1 National digital health strategy and AI-driven clinical research accelerating adoption

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 GERMANY

- 13.3.2.1 Hospital digitalization mandates and engineering-healthcare convergence drive market

- 13.3.3 UK

- 13.3.3.1 NHS digital transformation and in silico trial leadership advances digital twin market

- 13.3.4 FRANCE

- 13.3.4.1 National AI health strategy and clinical research infrastructure support digital twin integration

- 13.3.5 ITALY

- 13.3.5.1 National recovery plan investments and clinical research modernization drive adoption

- 13.3.6 SPAIN

- 13.3.6.1 Health system digital transformation and biomedical research network enables digital twin growth

- 13.3.7 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 JAPAN

- 13.4.2.1 National Digital Health Mission and pharma innovation ecosystem emerging as digital twin growth frontier

- 13.4.3 CHINA

- 13.4.3.1 National AI strategy and smart hospital infrastructure to drive large-scale digital twin deployment

- 13.4.4 INDIA

- 13.4.4.1 Improvement in healthcare infrastructure to support market growth

- 13.4.5 AUSTRALIA

- 13.4.5.1 National Digital Health Strategy 2023-2028 and Medical Research Future Fund advance digital twin adoption

- 13.4.6 SOUTH KOREA

- 13.4.6.1 Smart Hospital Policy and deep tech industrial ecosystem position country as regional leader

- 13.4.7 REST OF ASIA PACIFIC

- 13.5 LATIN AMERICA

- 13.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 13.5.2 BRAZIL

- 13.5.2.1 Country to dominate regional market

- 13.5.3 MEXICO

- 13.5.3.1 Favorable government strategies to drive market growth

- 13.5.4 REST OF LATIN AMERICA

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 13.6.2 GCC COUNTRIES

- 13.6.2.1 Increasing healthcare infrastructure development and investment to support market growth

- 13.6.2.2 Saudi Arabia

- 13.6.2.2.1 Government-led digital transformation and strong investments in AI-driven healthcare

- 13.6.2.3 UAE

- 13.6.2.3.1 Advancing digital health innovation and strategic collaborations to drive digital biomarkers adoption

- 13.6.2.4 Other GCC countries

- 13.6.2.4.1 Regulatory initiatives, national health visions, and digital health infrastructure driving digital biomarkers adoption

- 13.6.3 SOUTH AFRICA

- 13.6.3.1 Rising healthcare demand and need for cost-efficient, data-driven care delivery drive adoption

- 13.6.4 REST OF MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN DIGITAL TWINS IN HEALTHCARE MARKET

- 14.3 REVENUE SHARE ANALYSIS OF TOP MARKET PLAYERS

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 VALUATION & FINANCIAL METRICS

- 14.6.1 FINANCIAL METRICS

- 14.6.2 COMPANY VALUATION

- 14.7 COMPANY EVALUATION QUADRANT: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Component footprint

- 14.7.5.4 Type footprint

- 14.7.5.5 Application footprint

- 14.7.5.6 End user footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Detailed list of key startups/SME players

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT/SERVICE LAUNCHES, ENHANCEMENTS, AND APPROVALS

- 14.9.2 DEALS

- 14.9.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 MICROSOFT

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 SIEMENS HEALTHINEERS AG

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 KONINKLIJKE PHILIPS N.V.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 DASSAULT SYSTEMES

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product/Service launches & enhancements

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 AMAZON WEB SERVICES, INC.

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product/Service launches & enhancements

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 GE HEALTHCARE

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.7 ORACLE

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.8 IBM

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.9 PTC

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.10 SAP

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.3.2 Other developments

- 15.1.11 ATOS SE

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.12 NVIDIA CORPORATION

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product/Service launches & enhancements

- 15.1.12.3.2 Deals

- 15.1.13 ANSYS INC.

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product/Service launches & enhancements

- 15.1.13.3.2 Deals

- 15.1.14 FASTSTREAM TECHNOLOGIES

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Services offered

- 15.1.15 RESCALE, INC.

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Services offered

- 15.1.15.2.1 Other developments

- 15.1.1 MICROSOFT

- 15.2 OTHER PLAYERS

- 15.2.1 TWIN HEALTH

- 15.2.2 VERTO HEALTH

- 15.2.3 QBIO

- 15.2.4 THOUGHTWIRE

- 15.2.5 SIM&CURE

- 15.2.6 OWKIN, INC

- 15.2.7 NUREA

- 15.2.8 UNLEARN.AI, INC.

- 15.2.9 VIRTONOMY GMBH

- 15.2.10 PREDISURGE

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH APPROACH

- 16.1.1 SECONDARY RESEARCH

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY RESEARCH

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Breakdown of primaries

- 16.1.2.3 Insights from primary experts

- 16.1.1 SECONDARY RESEARCH

- 16.2 RESEARCH METHODOLOGY DESIGN

- 16.3 MARKET SIZE ESTIMATION

- 16.4 MARKET BREAKDOWN DATA TRIANGULATION

- 16.5 MARKET SHARE ESTIMATION

- 16.6 STUDY ASSUMPTIONS

- 16.7 RESEARCH LIMITATIONS

- 16.7.1 METHODOLOGY-RELATED LIMITATIONS

- 16.7.2 SCOPE-RELATED LIMITATIONS

- 16.8 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS

List of Tables

- TABLE 1 DIGITAL TWINS IN HEALTHCARE MARKET: INCLUSIONS & EXCLUSIONS

- TABLE 2 DIGITAL TWINS IN HEALTHCARE MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 3 DIGITAL TWIN IN HEALTHCARE MARKET: ROLE IN ECOSYSTEM

- TABLE 4 INDICATIVE PRICE FOR DIGITAL TWIN IN HEALTHCARE MARKET, BY TYPE (2025)

- TABLE 5 INDICATIVE PRICE FOR DIGITAL TWIN IN HEALTHCARE MARKET, BY REGION (2025)

- TABLE 6 DIGITAL TWIN IN HEALTHCARE: KEY CONFERENCES & EVENTS, 2026-2027

- TABLE 7 CASE 1: UNLEARN.AI - DIGITAL TWIN SYNTHETIC CONTROL ARMS IN ALS CLINICAL TRIALS

- TABLE 8 CASE 2: TWIN HEALTH - WHOLE BODY DIGITAL TWIN FOR TYPE 2 DIABETES REMISSION

- TABLE 9 CASE 3: INHEART/PREDISURGE - AI-POWERED CARDIAC DIGITAL TWIN FOR SURGICAL PLANNING

- TABLE 10 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 11 JURISDICTION ANALYSIS OF TOP APPLICANT COUNTRIES FOR DIGITAL TWIN IN HEALTHCARE MARKET

- TABLE 12 DIGITAL TWIN IN HEALTHCARE MARKET: LIST OF PATENTS/PATENT APPLICATIONS

- TABLE 13 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 REGULATORY SCENARIO IN NORTH AMERICA

- TABLE 19 REGULATORY SCENARIO IN EUROPE

- TABLE 20 REGULATORY SCENARIO IN ASIA PACIFIC

- TABLE 21 REGULATORY SCENARIO IN LATIN AMERICA

- TABLE 22 REGULATORY SCENARIO IN MIDDLE EAST & AFRICA

- TABLE 23 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF TOP THREE END USERS (%)

- TABLE 24 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 25 UNMET NEEDS IN DIGITAL TWIN IN HEALTHCARE MARKET

- TABLE 26 END USER EXPECTATIONS IN DIGITAL TWIN IN HEALTHCARE MARKET

- TABLE 27 DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 28 DIGITAL TWINS IN HEALTHCARE SERVICES MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 29 KEY SOFTWARE SOLUTIONS OFFERED BY PLAYERS

- TABLE 30 DIGITAL TWINS IN HEALTHCARE SOFTWARE MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 31 DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 32 PROCESS TWINS OFFERED BY MARKET PLAYERS

- TABLE 33 DIGITAL TWINS IN HEALTHCARE MARKET FOR PROCESS TWINS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 34 SYSTEM TWINS OFFERED BY MARKET PLAYERS

- TABLE 35 DIGITAL TWINS IN HEALTHCARE MARKET FOR SYSTEM TWINS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 36 WHOLE BODY TWINS OFFERED BY MARKET PLAYERS

- TABLE 37 DIGITAL TWINS IN HEALTHCARE MARKET FOR WHOLE BODY TWINS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 38 BODY PART TWINS OFFERED BY PLAYERS

- TABLE 39 DIGITAL TWINS IN HEALTHCARE MARKET FOR BODY PART TWINS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 40 DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 41 DIGITAL TWINS IN HEALTHCARE MARKET FOR DRUG DISCOVERY & DEVELOPMENT, BY REGION, 2024-2031 (USD MILLION)

- TABLE 42 DIGITAL TWINS IN HEALTHCARE MARKET FOR PERSONALIZED MEDICINE, BY REGION, 2024-2031 (USD MILLION)

- TABLE 43 DIGITAL TWINS IN HEALTHCARE MARKET FOR SURGICAL PLANNING & MEDICAL EDUCATION, BY REGION, 2024-2031 (USD MILLION)

- TABLE 44 DIGITAL TWINS IN HEALTHCARE MARKET FOR MEDICAL DEVICE DESIGN & TESTING, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 45 DIGITAL TWINS IN HEALTHCARE MARKET FOR HEALTHCARE WORKFLOW OPTIMIZATION & ASSET MANAGEMENT, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 46 DIGITAL TWINS IN HEALTHCARE MARKET FOR OTHER APPLICATIONS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 47 DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 48 DIGITAL TWINS IN HEALTHCARE MARKET FOR PHARMA & BIOPHARMA COMPANIES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 49 DIGITAL TWINS IN HEALTHCARE MARKET FOR RESEARCH & ACADEMIA, BY REGION, 2024-2031 (USD MILLION)

- TABLE 50 DIGITAL TWINS IN HEALTHCARE MARKET FOR HEALTHCARE PROVIDERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 51 DIGITAL TWINS IN HEALTHCARE MARKET FOR MEDICAL DEVICE COMPANIES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 52 DIGITAL TWINS IN HEALTHCARE MARKET FOR OTHER END USERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 53 DIGITAL TWINS IN HEALTHCARE MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 54 NORTH AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 55 NORTH AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 56 NORTH AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 57 NORTH AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 58 NORTH AMERICA: DIGITAL TWINS IN MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 59 US: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 60 US: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 61 US: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 62 US: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 63 CANADA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 64 CANADA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 65 CANADA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 66 CANADA: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 67 EUROPE: DIGITAL TWINS IN HEALTHCARE MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 68 EUROPE: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 69 EUROPE: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 70 EUROPE: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 71 EUROPE: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 72 GERMANY: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 73 GERMANY: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 74 GERMANY: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 75 GERMANY: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 76 UK: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 77 UK: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 78 UK: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 79 UK: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 80 FRANCE: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 81 FRANCE: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 82 FRANCE: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 83 FRANCE: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 84 ITALY: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 85 ITALY: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 86 ITALY: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 87 ITALY: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 88 SPAIN: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 89 SPAIN: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 90 SPAIN: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 91 SPAIN: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 92 REST OF EUROPE: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 93 REST OF EUROPE: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 94 REST OF EUROPE: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 95 REST OF EUROPE: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 96 ASIA PACIFIC: DIGITAL TWINS IN HEALTHCARE MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 97 ASIA PACIFIC: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 98 ASIA PACIFIC: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 99 ASIA PACIFIC: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 100 ASIA PACIFIC: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 101 JAPAN: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 102 JAPAN: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 103 JAPAN: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 104 JAPAN: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 105 CHINA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 106 CHINA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 107 CHINA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 108 CHINA: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 109 INDIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 110 INDIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 111 INDIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 112 INDIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 113 AUSTRALIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 114 AUSTRALIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 115 AUSTRALIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 116 AUSTRALIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 117 SOUTH KOREA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 118 SOUTH KOREA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 119 SOUTH KOREA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 120 SOUTH KOREA: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 121 REST OF ASIA PACIFIC: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 122 REST OF ASIA PACIFIC: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 123 REST OF ASIA PACIFIC: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 124 REST OF ASIA PACIFIC: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 125 LATIN AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 126 LATIN AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 127 LATIN AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 128 LATIN AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 129 LATIN AMERICA: DIGITAL TWINS IN MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 130 BRAZIL: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 131 BRAZIL: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 132 BRAZIL: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 133 BRAZIL: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 134 MEXICO: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 135 MEXICO: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 136 MEXICO: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 137 MEXICO: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 138 REST OF LATIN AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 139 REST OF LATIN AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 140 REST OF LATIN AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 141 REST OF LATIN AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 142 MIDDLE EAST & AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 143 MIDDLE EAST & AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 144 MIDDLE EAST & AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 145 MIDDLE EAST & AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 146 MIDDLE EAST & AFRICA: DIGITAL TWINS IN MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 147 GCC COUNTRIES: DIGITAL TWINS IN HEALTHCARE MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 148 GCC COUNTRIES: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 149 GCC COUNTRIES: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 150 GCC COUNTRIES: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 151 GCC COUNTRIES: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 152 SAUDI ARABIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 153 SAUDI ARABIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 154 SAUDI ARABIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 155 SAUDI ARABIA: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 156 UAE: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 157 UAE: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 158 UAE: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 159 UAE: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 160 OTHER GCC COUNTRIES: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 161 OTHER GCC COUNTRIES: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 162 OTHER GCC COUNTRIES: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 163 OTHER GCC COUNTRIES: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 164 SOUTH AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 165 SOUTH AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 166 SOUTH AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 167 SOUTH AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 168 REST OF MIDDLE EAST & AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 169 REST OF MIDDLE EAST & AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 170 REST OF MIDDLE EAST & AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 171 REST OF MIDDLE EAST & AFRICA: DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 172 OVERVIEW OF STRATEGIES DEPLOYED BY KEY PLAYERS IN DIGITAL TWINS IN HEALTHCARE MARKET, JANUARY 2023-MAY 2026

- TABLE 173 DIGITAL TWINS IN HEALTHCARE MARKET: DEGREE OF COMPETITION

- TABLE 174 DIGITAL TWIN IN HEALTHCARE MARKET: REGION FOOTPRINT (15 COMPANIES)

- TABLE 175 DIGITAL TWIN IN HEALTHCARE MARKET: COMPONENT FOOTPRINT (15 COMPANIES)

- TABLE 176 DIGITAL TWIN IN HEALTHCARE MARKET: TYPE FOOTPRINT (15 COMPANIES)

- TABLE 177 DIGITAL TWIN IN HEALTHCARE MARKET: APPLICATION FOOTPRINT (15 COMPANIES)

- TABLE 178 DIGITAL TWIN IN HEALTHCARE MARKET: END USER FOOTPRINT (15 COMPANIES)

- TABLE 179 DIGITAL TWINS IN HEALTHCARE MARKET: PRODUCT/SERVICE LAUNCHES, ENHANCEMENTS, AND APPROVALS, JANUARY 2023-MAY 2026

- TABLE 180 DIGITAL TWINS IN HEALTHCARE MARKET: DEALS, JANUARY 2023-MAY 2026

- TABLE 181 DIGITAL TWINS IN HEALTHCARE MARKET: OTHER DEVELOPMENTS, JANUARY 2023-MAY 2026

- TABLE 182 MICROSOFT: COMPANY OVERVIEW

- TABLE 183 MICROSOFT CORPORATION: PRODUCTS/SERVICES OFFERED

- TABLE 184 MICROSOFT: DEALS, JANUARY 2023-MAY 2026

- TABLE 185 SIEMENS HEALTHINEERS AG: COMPANY OVERVIEW

- TABLE 186 SIEMENS HEALTHINEERS AG: PRODUCTS/SERVICES OFFERED

- TABLE 187 SIEMENS HEALTHINEERS AG: DEALS, JANUARY 2023-MAY 2026

- TABLE 188 KONINKLIJKE PHILIPS N.V.: COMPANY OVERVIEW

- TABLE 189 KONINKLIJKE PHILIPS N.V.: PRODUCTS/SERVICES OFFERED

- TABLE 190 KONINKLIJKE PHILIPS N.V.: DEALS, JANUARY 2023-MAY 2026

- TABLE 191 DASSAULT SYSTEMES: COMPANY OVERVIEW

- TABLE 192 DASSAULT SYSTEMES: PRODUCTS/SERVICES OFFERED

- TABLE 193 DASSAULT SYSTEMES: PRODUCT/SERVICE LAUNCHES & ENHANCEMENTS, JANUARY 2023-MAY 2026

- TABLE 194 DASSAULT SYSTEMES: DEALS, JANUARY 2023-MAY 2026

- TABLE 195 AMAZON WEB SERVICES, INC.: COMPANY OVERVIEW

- TABLE 196 AMAZON WEB SERVICES, INC.: PRODUCTS/SERVICES OFFERED

- TABLE 197 AMAZON WEB SERVICES, INC.: PRODUCT/SERVICE LAUNCHES & ENHANCEMENTS, JANUARY 2023-MAY 2026

- TABLE 198 AMAZON WEB SERVICES, INC.: DEALS, JANUARY 2023-MAY 2026

- TABLE 199 GE HEALTHCARE: COMPANY OVERVIEW

- TABLE 200 GE HEALTHCARE: PRODUCTS/SERVICES OFFERED

- TABLE 201 GE HEALTHCARE: DEALS, JANUARY 2023-MAY 2026

- TABLE 202 ORACLE: COMPANY OVERVIEW

- TABLE 203 ORACLE: PRODUCTS/SERVICES OFFERED

- TABLE 204 ORACLE: DEALS, JANUARY 2023-MAY 2026

- TABLE 205 IBM: COMPANY OVERVIEW

- TABLE 206 IBM: PRODUCTS/SERVICES OFFERED

- TABLE 207 IBM: DEALS, JANUARY 2023-MAY 2026

- TABLE 208 PTC: COMPANY OVERVIEW

- TABLE 209 PTC: PRODUCTS/SERVICES OFFERED

- TABLE 210 PTC: DEALS, JANUARY 2023-MAY 2026

- TABLE 211 SAP: COMPANY OVERVIEW

- TABLE 212 SAP: PRODUCTS/SERVICES OFFERED

- TABLE 213 SAP: DEALS, JANUARY 2023-MAY 2026

- TABLE 214 SAP: OTHER DEVELOPMENTS, JANUARY 2023-MAY 2026

- TABLE 215 ATOS SE: COMPANY OVERVIEW

- TABLE 216 ATOS SE: PRODUCTS/SERVICES OFFERED

- TABLE 217 ATOS SE: DEALS, JANUARY 2023-MAY 2026

- TABLE 218 NVIDIA CORPORATION: COMPANY OVERVIEW

- TABLE 219 NVIDIA CORPORATION: PRODUCTS/SERVICES OFFERED

- TABLE 220 NVIDIA CORPORATION: PRODUCT/SERVICE LAUNCHES & ENHANCEMENTS, JANUARY 2023-MAY 2026

- TABLE 221 NVIDIA CORPORATION: DEALS, JANUARY 2023-MAY 2026

- TABLE 222 ANSYS INC.: COMPANY OVERVIEW

- TABLE 223 ANSYS INC.: PRODUCTS/SERVICES OFFERED

- TABLE 224 ANSYS INC.: PRODUCT/SERVICE LAUNCHES & ENHANCEMENTS, JANUARY 2023-MAY 2026

- TABLE 225 ANSYS INC.: DEALS, JANUARY 2023-MAY 2026

- TABLE 226 FASTSTREAM TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 227 FASTSTREAM TECHNOLOGIES: PRODUCTS/SERVICES OFFERED

- TABLE 228 RESCALE, INC.: COMPANY OVERVIEW

- TABLE 229 RESCALE, INC.: PRODUCTS/SERVICES OFFERED

- TABLE 230 RESCALE, INC.: OTHER DEVELOPMENTS, JANUARY 2023-MAY 2026

- TABLE 231 TWIN HEALTH: COMPANY OVERVIEW

- TABLE 232 VERTO HEALTH: COMPANY OVERVIEW

- TABLE 233 QBIO: COMPANY OVERVIEW

- TABLE 234 THOUGHTWIRE: COMPANY OVERVIEW

- TABLE 235 SIM&CURE: COMPANY OVERVIEW

- TABLE 236 OWKIN, INC: COMPANY OVERVIEW

- TABLE 237 NUREA: COMPANY OVERVIEW

- TABLE 238 UNLEARN.AI, INC.: COMPANY OVERVIEW

- TABLE 239 VIRTONOMY GMBH: COMPANY OVERVIEW

- TABLE 240 PREDISURGE: COMPANY OVERVIEW

- TABLE 241 DIGITAL TWINS IN HEALTHCARE MARKET: RISK ASSESSMENT

List of Figures

- FIGURE 1 DIGITAL TWINS IN HEALTHCARE MARKET SEGMENTATION & REGIONAL SCOPE

- FIGURE 2 DIGITAL TWINS IN HEALTHCARE MARKET: YEARS CONSIDERED

- FIGURE 3 MARKET SCENARIO

- FIGURE 4 GLOBAL DIGITAL TWINS IN HEALTHCARE MARKET, 2024-2031

- FIGURE 5 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN DIGITAL TWIN IN HEALTHCARE MARKET, 2023-2026

- FIGURE 6 DISRUPTIONS INFLUENCING GROWTH OF DIGITAL TWIN IN HEALTHCARE MARKET

- FIGURE 7 HIGH-GROWTH SEGMENTS IN DIGITAL TWIN IN HEALTHCARE MARKET, 2026-2031

- FIGURE 8 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN DIGITAL TWIN IN HEALTHCARE MARKET DURING FORECAST PERIOD

- FIGURE 9 INCREASING USE OF DIGITAL TWINS AND GROWING IMPORTANCE OF PATIENT-CENTRIC CARE TO DRIVE MARKET GROWTH

- FIGURE 10 SOFTWARE ACCOUNTED FOR LARGEST MARKET SHARE IN NORTH AMERICA IN 2025

- FIGURE 11 CHINA TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 12 DIGITAL TWIN IN HEALTHCARE MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 13 DIGITAL TWIN IN MARKET: VALUE CHAIN ANALYSIS (2025)

- FIGURE 14 DIGITAL TWIN IN HEALTHCARE MARKET: ECOSYSTEM ANALYSIS

- FIGURE 15 REVENUE SHIFT IN DIGITAL TWIN IN HEALTHCARE MARKET

- FIGURE 16 RECENT FUNDING OF PLAYERS IN DIGITAL TWIN IN HEALTHCARE MARKET

- FIGURE 17 PATENT PUBLICATION TRENDS IN DIGITAL TWIN IN HEALTHCARE MARKET, 2015-2026

- FIGURE 18 JURISDICTION AND TOP APPLICANT ANALYSIS FOR DIGITAL TWIN IN HEALTHCARE MARKET

- FIGURE 19 TOP APPLICANTS & OWNERS (COMPANIES/INSTITUTIONS) FOR DIGITAL TWIN IN HEALTHCARE MARKET (JANUARY 2015 TO FEBRUARY 2026)

- FIGURE 20 MARKET POTENTIAL OF AI/GEN AI ON DIGITAL TWIN IN HEALTHCARE ACROSS INDUSTRIES

- FIGURE 21 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- FIGURE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR END USERS

- FIGURE 23 KEY BUYING CRITERIA FOR TOP THREE END USERS

- FIGURE 24 NORTH AMERICA: DIGITAL TWINS IN HEALTHCARE MARKET SNAPSHOT

- FIGURE 25 ASIA PACIFIC: DIGITAL TWINS IN HEALTHCARE MARKET SNAPSHOT

- FIGURE 26 DIGITAL TWIN IN HEALTHCARE MARKET: REVENUE ANALYSIS OF KEY PLAYERS

- FIGURE 27 MARKET SHARE ANALYSIS OF KEY PLAYERS IN DIGITAL TWINS IN HEALTHCARE (2025)

- FIGURE 28 DIGITAL TWIN IN HEALTHCARE MARKET: BRAND COMPARATIVE ANALYSIS

- FIGURE 29 EV/EBITDA OF KEY VENDORS

- FIGURE 30 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 31 DIGITAL TWINS IN HEALTHCARE MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 32 DIGITAL TWIN IN HEALTHCARE MARKET: COMPANY FOOTPRINT

- FIGURE 33 DIGITAL TWINS IN HEALTHCARE MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 34 MICROSOFT: COMPANY SNAPSHOT (2025)

- FIGURE 35 SIEMENS HEALTHINEERS AG: COMPANY SNAPSHOT (2025)

- FIGURE 36 KONINKLIJKE PHILIPS N.V.: COMPANY SNAPSHOT (2025)

- FIGURE 37 DASSAULT SYSTEMES: COMPANY SNAPSHOT (2025)

- FIGURE 38 AMAZON WEB SERVICES, INC.: COMPANY SNAPSHOT (2025)

- FIGURE 39 GE HEALTHCARE: COMPANY SNAPSHOT (2025)

- FIGURE 40 ORACLE: COMPANY SNAPSHOT (2024)

- FIGURE 41 IBM: COMPANY SNAPSHOT (2025)

- FIGURE 42 PTC: COMPANY SNAPSHOT (2025)

- FIGURE 43 SAP: COMPANY SNAPSHOT (2025)

- FIGURE 44 ATOS SE: COMPANY SNAPSHOT (2025)

- FIGURE 45 NVIDIA CORPORATION: COMPANY SNAPSHOT (2025)

- FIGURE 46 ANSYS INC. (SYNOPSYS, INC.): COMPANY SNAPSHOT (2025)

- FIGURE 47 RESEARCH DESIGN

- FIGURE 48 PRIMARY SOURCES

- FIGURE 49 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 50 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 51 BOTTOM-UP APPROACH

- FIGURE 52 TOP-DOWN APPROACH

- FIGURE 53 CAGR PROJECTIONS FROM ANALYSIS OF MARKET DYNAMICS

- FIGURE 54 CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS

- FIGURE 55 DIGITAL TWINS IN HEALTHCARE MARKET: DATA TRIANGULATION

醫療保健領域的數位雙胞胎市場:按產品、組件、技術、部署模式、應用、疾病領域和最終用戶分類-2026-2032年全球市場預測

醫療保健領域的數位雙胞胎市場:按產品、組件、技術、部署模式、應用、疾病領域和最終用戶分類-2026-2032年全球市場預測 2026年全球數位雙胞胎心肺體外迴圈市場報告

2026年全球數位雙胞胎心肺體外迴圈市場報告 數位高程模型市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型及功能分類醫療產業數位雙胞胎市場分析及預測(至2035年),依類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶及解決方案分類

數位高程模型市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型及功能分類醫療產業數位雙胞胎市場分析及預測(至2035年),依類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶及解決方案分類 醫療保健數位雙胞胎市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、最終用途、應用、地區和競爭格局分類,2021-2031年)醫療保健領域數位孿生市場-全球產業規模、佔有率、趨勢、機會和預測,按組件、應用、最終用戶、地區和競爭格局分類,2021-2031年預測2025年醫療保健數位雙胞胎全球市場報告

醫療保健數位雙胞胎市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、最終用途、應用、地區和競爭格局分類,2021-2031年)醫療保健領域數位孿生市場-全球產業規模、佔有率、趨勢、機會和預測,按組件、應用、最終用戶、地區和競爭格局分類,2021-2031年預測2025年醫療保健數位雙胞胎全球市場報告 2032 年腦建模數位雙胞胎市場預測:按組件、應用、最終用戶和地區進行的全球分析

2032 年腦建模數位雙胞胎市場預測:按組件、應用、最終用戶和地區進行的全球分析 醫療保健市場的數位孿生:行業趨勢和全球預測 - 依治療領域、數位孿生類型、應用領域、最終用戶和關鍵地區

醫療保健市場的數位孿生:行業趨勢和全球預測 - 依治療領域、數位孿生類型、應用領域、最終用戶和關鍵地區 全球醫療保健數位雙胞胎市場

全球醫療保健數位雙胞胎市場