|

市場調查報告書

商品編碼

2033996

全球牙科耗材市場:按產品、最終用戶和地區分類-預測至2031年Dental Consumables Market by Product, By End User - Global Forecast to 2031 |

||||||

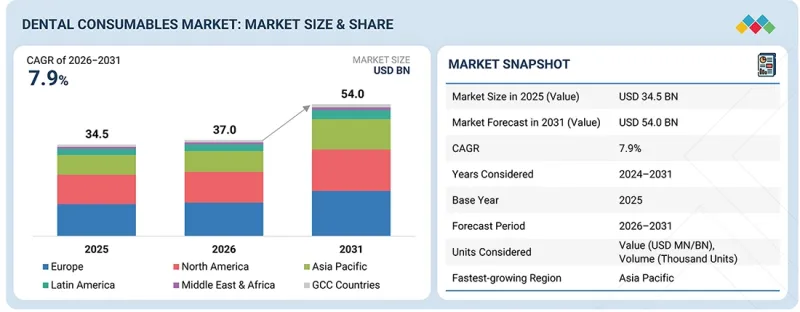

全球牙科耗材市場規模預計在預測期內將以 7.9% 的複合年成長率成長,從 2026 年的 370 億美元成長到 2031 年的 540 億美元。

| 調查範圍 | |

|---|---|

| 調查期 | 2026-2031 |

| 基準年 | 2025 |

| 預測期 | 2026-2031 |

| 目標單元 | 金額(10億美元) |

| 部分 | 按產品、最終用戶、地區 |

| 目標區域 | 北美、歐洲、亞太地區、拉丁美洲、中東和非洲 |

受人口結構變化、臨床需求和技術進步的推動,牙科耗材市場預計將快速成長。隨著越來越多的人面臨牙齒問題,尤其是老年人需要修復和義齒治療,全球需求持續上升。牙科材料的改進和創新技術(例如數位化牙科、生物相容性複合材料和CAD/CAM系統)顯著改善了治療效果,並推動了產品的普及。此外,口腔衛生意識的提高、牙科保健服務的可及性改善以及美容牙科的日益普及也促進了市場成長。預計未來幾年,這些趨勢將在已開發地區和新興地區保持強勁勢頭。

按產品類型分類,牙科修復材料領域正在推動牙科耗材市場的發展。

牙科耗材市場依產品類型分為修復牙科、矯正、牙周治療、感染控制、牙髓治療、美白產品、拋光產品等。

在這一細分市場中,修復牙科領域推動了牙科耗材市場的發展,這主要得益於齲齒和牙齒缺失等疾病的高發生率,以及對補牙、牙冠和牙橋等治療的需求。此外,對美容牙科日益成長的需求也促進了外觀和耐用性更佳的先進修復材料的使用。材料和數位化牙科技術的進步也提高了治療效果和效率。口腔衛生意識的提高和牙科保健服務的可近性改善也促進了該領域需求的持續成長。

按最終用戶分類,牙醫醫院和診所在牙科耗材市場中佔據最大佔有率。

牙科耗材市場細分為牙科醫院和診所、牙體技術所、牙科服務機構 (DSO) 以及其他終端用戶,包括牙科教育和研究機構以及法醫牙科。預計到 2025 年,牙科醫院和診所將佔據牙科耗材市場最大的佔有率,這主要基於其龐大的患者數量、廣泛的治療方法以及最新牙科技術的普及。這些機構通常需要處理大量的根管治療、修復和外科手術病例,因此對耗材的需求量很大。經驗豐富的牙醫的存在以及公立和私立診所對基礎設施的持續投入進一步鞏固了這一細分市場的主導地位。診所對美容牙科和預防牙科的日益重視也鞏固了主導地位。

預計在預測期內,亞太地區牙科耗材市場將錄得最高的複合年成長率。

預計在預測期內,亞太地區牙科耗材市場將呈現最高的成長率,這主要得益於新興經濟體牙科保健服務的可近性提高以及醫療基礎設施的快速發展。口腔衛生意識的增強,以及齲齒和牙周病等疾病盛行率的上升,推動了對預防性和修復性牙科治療的需求。此外,可支配收入的增加、中產階級的壯大以及生活方式的改變,不僅增加了人們對基本牙科保健的支出,也增加了對美容牙科的支出。政府為改善口腔保健服務可及性而採取的舉措,以及私人企業投資的增加,進一步促進了市場擴張。此外,數位成像和CAD/CAM系統等先進技術的應用提高了治療效率和效果,從而增加了對高品質牙科耗材的需求。

牙科耗材市場的主要參與者包括Institut Straumann AG(瑞士)、Envista(美國)、Dentsply Sirona(美國)、ZimVie Inc.(美國)、Solventum(美國)、Henry Schein, Inc.(美國)、Kuraray(日本)、Mitsui Chemicals, Inc.(日本)、Geistd Corporation Vivc] (日本)、Keystone Dental Inc. (美國)、BEGO GmbH & Co. KG (德國)、Septodont Holding (法國)、Ultradent Products (美國)、VOCO GmbH (德國)、COLTENE Group (瑞士)、SDI Limited (澳洲)、Young Innovations, Inc. (美國)、Dazeiad-Prik-K-Kra-Kra)(德國) INC.(日本)、Glidewell(美國)、 BISCO, Inc.(美國)和 Dental Technologies Inc.(美國)。

調查範圍

本報告對牙科耗材市場進行了分析,重點關注市場規模、預測以及在產品類型、地區和最終用戶等各個細分市場的未來成長潛力。此外,報告還對市場主要參與者進行了競爭分析,詳細介紹了每家公司的概況、產品和服務、近期發展以及關鍵市場策略。

購買本報告的理由

本報告為牙科耗材行業的市場領導和新參與企業提供了寶貴的見解,並提供了整體市場及其細分市場的近似銷售數據。這有助於相關人員了解競爭格局,更好地定位自身業務,並制定有效的打入市場策略。此外,報告還指出了關鍵的市場促進因素、限制、挑戰和機遇,幫助相關人員掌握當前的市場狀況。

本報告深入分析了以下幾點:

- 關鍵促進因素(齲齒病例增加導致牙科修復程序增加、對先進美容牙科的需求不斷成長、新興國家牙科旅遊市場擴張以及先進解決方案的開發)、阻礙因素(保險報銷不足和牙科服務成本高昂)、機遇(對 CAD/CAM 技術的投資增加、對新興市場的日益關注和可支配日參與企業的增加以及對當專業人員的主要需求增加)。

- 市場滲透率:本報告詳細介紹了全球牙科耗材市場主要參與者提供的產品系列。報告涵蓋了產品類型、最終用戶和地區等多個細分市場。

- 產品改進與創新:全面介紹全球牙科耗材市場的新產品發布與預測趨勢。

- 市場開發:我們按產品類型、最終用戶和地區提供盈利成長市場的深入見解和分析。

- 市場多元化:提供全球牙科耗材市場新產品和服務推出、市場擴張、當前發展和投資的全面資訊。

- 競爭分析:對全球牙科耗材市場主要競爭對手的市場佔有率、成長計畫、產品和服務以及生產能力進行全面評估。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求和未開發的領域

- 相互關聯的市場與跨產業機遇

- 參與企業一級/二級/三級市場的策略性舉措。

第5章 產業趨勢

- 波特五力分析

- 宏觀經濟展望

- 價值鏈分析

- 生態系分析

- 供應鏈分析

- 價格分析

- 貿易分析

- 2026年重大會議和活動

- 影響客戶業務的趨勢/顛覆性因素

- 投資和資金籌措場景

- 案例研究分析

- 2025年美國關稅對牙科耗材市場的影響。

第6章:技術進步、人工智慧的影響、專利、創新與未來應用

- 主要新興技術

- 技術/產品藍圖

- 專利分析

- 人工智慧/生成式人工智慧對牙科耗材市場的影響

- 成功案例和實際應用

第7章 監理情勢

- 監管機構、政府機構和其他組織

- 認證、標籤檢視和環境標準

第8章:顧客趨勢與購買行為

- 決策流程

- 買方相關人員和採購評估標準

- 實施障礙和內部挑戰

- 各個終端用戶產業中尚未滿足的需求

第9章:牙科耗材市場(依產品分類)

- 人工植牙

- 牙齒修復

- 正畸

- 牙周病學

- 感染控制產品

- 根管治療

- 美白產品

- 精加工和拋光產品

- 其他

第10章:牙科耗材市場(依最終用戶分類)

- 牙醫醫院和診所

- 牙體技術所

- 牙科保健服務機構

- 其他

第11章:牙科耗材市場(按地區分類)

- 歐洲

- 歐洲宏觀經濟展望

- 德國

- 義大利

- 西班牙

- 法國

- 英國

- 其他

- 北美洲

- 北美宏觀經濟展望

- 美國

- 加拿大

- 亞太地區

- 亞太地區宏觀經濟展望

- 日本

- 澳洲

- 韓國

- 中國

- 印度

- 其他

- 拉丁美洲

- 拉丁美洲宏觀經濟展望

- 巴西

- 墨西哥

- 阿根廷

- 其他

- 中東和非洲

- 人們口腔衛生意識的提高正在推動市場成長。

- 中東和非洲宏觀經濟展望

- 海灣合作理事會國家

- 會議、高峰會和培訓課程增加

- 海灣合作理事會國家宏觀經濟展望

第12章 競爭格局

- 主要參與企業的策略/優勢

- 2021-2025年收入分析

- 2025年市佔率分析

- 企業估值矩陣:主要公司,2025 年

- 公司估值矩陣:新創企業/中小企業,2025 年

- 企業估值和財務指標

- 品牌/產品對比

- 主要公司的研發支出

- 競爭格局

第13章:公司簡介

- 主要參與企業

- INSTITUT STRAUMANN AG

- ENVISTA

- DENTSPLY SIRONA

- SOLVENTUM

- ZIMVIE INC.

- HENRY SCHEIN

- KURARAY CO., LTD.

- MITSUI CHEMICALS, INC.

- SHOFU

- IVOCLAR VIVADENT AG

- 其他公司

- GC CORPORATION

- KEYSTONE DENTAL GROUP

- BEGO GMBH & CO. KG

- SEPTODONT HOLDING

- ULTRADENT PRODUCTS

- VOCO GMBH

- COLTENE GROUP

- SDI LIMITED

- YOUNG INNOVATIONS, INC.

- DMG CHEMISCH-PHARMAZEUTISCHE FABRIK GMBH

- BRASSELER USA

- GEISTLICH PHARMA AG

- GLIDEWELL

- BISCO INC.

- DENTAL TECHNOLOGIES INC.

第14章調查方法

第15章附錄

The global dental consumables market is projected to reach USD 54.0 billion by 2031, up from USD 37.0 billion in 2026, at a CAGR of 7.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product Type, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

The market for dental consumables is set to grow quickly, influenced by demographic shifts, clinical needs, and technological advancements. As more people experience dental issues and the aging population increases, especially those requiring restorative and prosthetic care, global demand continues to rise. Improvements in dental materials and innovative technologies like digital dentistry, biocompatible composites, and CAD/CAM systems have significantly improved treatment results, encouraging more widespread product use. Additionally, greater attention to oral health, easier access to dental care, and the growing popularity of cosmetic dentistry are all contributing to market growth. These trends are expected to sustain positive momentum in both developed and emerging regions in the years ahead.

By product type, the dental restoration segment dominated the dental consumables market.

The dental consumables market is segmented by product type into dental restoration, orthodontics, periodontics, infection control, endodontics, whitening products, finishing & polishing products, and others.

Among these, the dental restoration segment dominated the dental consumables market due to the high prevalence of conditions such as dental caries and tooth loss, which require procedures such as fillings, crowns, and bridges. Increasing demand for aesthetic dentistry has also driven the use of advanced restorative materials that offer improved appearance and durability. Moreover, technological advancements in materials and digital dentistry have enhanced treatment outcomes and efficiency. Rising awareness of oral health and greater access to dental care have further contributed to sustained demand in this segment.

Based on end user, the dental hospitals and clinics segment accounted for the largest share of the dental consumables market.

The dental consumables market is segmented into dental hospitals and clinics, dental laboratories, dental service organizations (DSOs), and other end users, including dental academic & research institutes and forensic dentistry. Dental hospitals and clinics accounted for the largest share of the dental consumables market in 2025 based on their high inflow of patients, extensive assortment of procedures offered, and availability of the latest dental technology. These institutions tend to manage a large volume of endodontic, restorative, and surgical cases, necessitating the high demand for consumables. Also, the presence of experienced dental practitioners and increasing investments in infrastructure at public and private clinics have augmented segment dominance further. The growing focus on cosmetic and preventive dental care in clinics supports their market leadership.

Asia Pacific is expected to register the highest CAGR in the dental consumables market during the forecast period.

The Asia Pacific is projected to experience the highest growth rate in the dental consumables market over the forecast period, driven by improving access to dental care and rapidly expanding healthcare infrastructure in emerging economies. Rising awareness of oral health, coupled with the increasing prevalence of conditions such as dental caries and periodontal diseases, is driving demand for both preventive and restorative dental treatments. Additionally, growing disposable incomes, a rising middle-class population, and changing lifestyle habits are encouraging higher spending on essential as well as cosmetic dental procedures. Government initiatives to improve oral healthcare access, along with increasing investments from private players, are further supporting market expansion. Furthermore, the growing adoption of advanced technologies, such as digital imaging and CAD/CAM systems, is enhancing treatment efficiency and outcomes, boosting demand for high-quality dental consumables.

A breakdown of the primary participants (supply side) for the dental consumables market referred to in this report is provided below:

- By Company Type: Tier 1 (30%), Tier 2 (35%), and Tier 3 (35%)

- By Designation: C-level Executives (20%), Directors (35%), and Others (45%)

- By Region: North America (30%), Europe (25%), Asia Pacific (20%), Latin America (20%), Middle East & Africa (2%), GCC Countries (3%)

Prominent players in the dental consumables market include Institut Straumann AG (Switzerland), Envista (US), Dentsply Sirona (US), ZimVie Inc. (US), Solventum (US), Henry Schein, Inc. (US), Kuraray Co., Ltd. (Japan), Mitsui Chemicals, Inc. (Japan), Geistlich Pharma AG (Switzerland), Ivoclar Vivadent (Liechtenstein), GC Corporation (Japan), Keystone Dental Inc. (US), BEGO GmbH & Co. KG (Germany), Septodont Holding (France), Ultradent Products (US), VOCO GmbH (Germany), COLTENE Group (Switzerland), SDI Limited (Australia), Young Innovations, Inc. (US), DMG Chemisch-Pharmazeutische Fabrik (Germany), Brasseler USA (US), SHOFU INC. (Japan), Glidewell (US), BISCO, Inc. (US), and Dental Technologies Inc. (US).

Research Coverage

The report provides an analysis of the dental consumables market, focusing on estimating market size and potential future growth across segments, including product types, regions, and end users. Additionally, the report features a competitive analysis of the key players in the market, detailing their company profiles, product & service offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report provides valuable insights for both market leaders and new entrants in the dental consumables industry, offering approximate revenue figures for the overall market and its subsegments. It helps stakeholders understand the competitive landscape, enabling them to better position their businesses and develop effective go-to-market strategies. Additionally, the report highlights key market drivers, restraints, challenges, and opportunities, helping stakeholders gauge the current state of the market.

This report provides insights into the following points:

- Analysis of key drivers (rising cases of dental caries and subsequent increase in tooth repair procedures, rising demand for advanced cosmetic dental procedures, growing market for dental tourism in emerging countries, and development of advanced solutions), restraints (inadequate reimbursement and high cost of dental services), opportunities (increasing investments in CAD/CAM technologies, growing focus on emerging markets and rising disposable income levels, and increasing demand for same-day dentistry) and challenges (pricing pressure faced by prominent market players, and dearth of skilled lab professionals)

- Market Penetration: It provides detailed information on the product portfolios offered by major players in the global dental consumables market. The report covers various segments, including product types, end users, and regions.

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global dental consumables market.

- Market Development: Thorough knowledge and analysis of the profitable rising markets by product types, end users, and regions.

- Market Diversification: Comprehensive information about newly launched products and services, expanding markets, current advancements, and investments in the global dental consumables market.

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products and services, and capacities of the major competitors in the global dental consumables market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY MARKET PARTICIPANTS: INSIGHTS & DEVELOPMENTS

- 2.2 DISRUPTIVE TRENDS SHAPING MARKET GROWTH

- 2.3 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.4 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 DENTAL CONSUMABLES MARKET OVERVIEW

- 3.2 EUROPE: DENTAL CONSUMABLES MARKET, BY END USER AND COUNTRY

- 3.3 DENTAL CONSUMABLES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 DENTAL CONSUMABLES MARKET, BY REGION

- 3.5 DENTAL CONSUMABLES MARKET: DEVELOPED VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing prevalence of dental caries leading to higher demand for tooth restoration procedures

- 4.2.1.2 Growing preference for advanced cosmetic dental treatments

- 4.2.1.3 Expanding dental tourism market in developing nations

- 4.2.1.4 Introduction of innovative and advanced dental solutions

- 4.2.2 RESTRAINTS

- 4.2.2.1 Limited reimbursement policies and high cost associated with dental treatments

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising funding and adoption of CAD/CAM dental technologies

- 4.2.3.2 Expanding opportunities in emerging markets supported by rising disposable incomes

- 4.2.3.3 Growing popularity of same-day dental treatment services

- 4.2.4 CHALLENGES

- 4.2.4.1 Intense pricing competition among leading market players

- 4.2.4.2 Shortage of qualified and experienced dental laboratory professionals

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER- 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN DENTAL CONSUMABLES MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF DENTAL CONSUMABLES, BY TYPE, 2023-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF DENTAL IMPLANTS, BY COUNTRY, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.8 KEY CONFERENCES & EVENTS, 2026

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.12 IMPACT OF 2025 US TARIFFS ON DENTAL CONSUMABLES MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON REGION

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USER INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 CAD/CAM TECHNOLOGY

- 6.1.2 CARIES DETECTION TECHNOLOGY

- 6.1.3 COMPLEMENTARY TECHNOLOGIES

- 6.1.3.1 Robot dentists and AI

- 6.1.4 ADJACENT TECHNOLOGIES

- 6.1.4.1 Novel biocompatible materials

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM |RECENT TECHNOLOGIES| FOUNDATION & EARLY COMMERCIALIZATION

- 6.2.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.2.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.3 PATENT ANALYSIS

- 6.3.1 PATENT PUBLICATION TRENDS FOR DENTAL CONSUMABLES

- 6.3.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.3.3 TOP APPLICANTS & OWNERS (COMPANIES/INSTITUTIONS) FOR DENTAL CONSUMABLES PATENTS (JANUARY 2015-DECEMBER 2025)

- 6.3.4 TOP APPLICANT COUNTRIES/REGIONS PATENTS FOR DENTAL CONSUMABLES (JANUARY 2015-DECEMBER 2025)

- 6.4 IMPACT OF AI/GEN AI ON DENTAL CONSUMABLES MARKET

- 6.4.1 TOP USE CASES & MARKET POTENTIAL

- 6.4.2 INTERCONNECTED ADJACENT ECOSYSTEMS & IMPACT ON MARKET PLAYERS

- 6.4.3 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DENTAL CONSUMABLES MARKET

- 6.5 SUCCESS STORIES & REAL-WORLD APPLICATIONS

- 6.5.1 INSTITUT STRAUMANN: AI-DRIVEN DIGITAL WORKFLOW & SMILE DESIGN

- 6.5.2 DENTSPLY SIRONA: AI-POWERED CAD/CAM & SINGLE-VISIT DENTISTRY

- 6.5.3 ENVISTA: AI-ENABLED IMAGE ANALYSIS & DIGITAL WORKFLOW INTEGRATION

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1 INDUSTRY STANDARDS

- 7.1.1.1 North America

- 7.1.1.1.1 US

- 7.1.1.1.2 Canada

- 7.1.1.2 Europe

- 7.1.1.3 Asia Pacific

- 7.1.1.3.1 China

- 7.1.1.3.2 Japan

- 7.1.1.4 Latin America

- 7.1.1.4.1 Brazil

- 7.1.1.4.2 Mexico

- 7.1.1.5 Middle East

- 7.1.1.6 Africa

- 7.1.1.1 North America

- 7.1.1 INDUSTRY STANDARDS

- 7.2 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.2.1 INFLUENCE OF KEY STAKEHOLDERS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 DENTAL CONSUMABLES MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 DENTAL IMPLANTS

- 9.2.1 TITANIUM IMPLANTS

- 9.2.1.1 High biocompatibility and cost-effectiveness to drive usage in implants

- 9.2.2 ZIRCONIUM IMPLANTS

- 9.2.2.1 Superior esthetics to drive preference for zirconium over titanium implants

- 9.2.1 TITANIUM IMPLANTS

- 9.3 DENTAL RESTORATIONS

- 9.3.1 DIRECT RESTORATIVE MATERIALS

- 9.3.1.1 Amalgams

- 9.3.1.1.1 Presence of mercury in amalgams to restrain market growth

- 9.3.1.2 Composites

- 9.3.1.2.1 Need for minimal tooth preparation and effective bonding to propel growth

- 9.3.1.3 Glass ionomers

- 9.3.1.3.1 Low load-bearing strength to restrain growth

- 9.3.1.4 Other direct restorative materials

- 9.3.1.1 Amalgams

- 9.3.2 INDIRECT RESTORATIVE MATERIALS

- 9.3.2.1 Metals

- 9.3.2.1.1 High durability and fracture resistance to drive demand

- 9.3.2.2 Ceramics

- 9.3.2.2.1 Appeal and translucency to propel adoption

- 9.3.2.3 Other indirect restorative materials

- 9.3.2.1 Metals

- 9.3.3 DENTAL BIOMATERIALS

- 9.3.3.1 Dental bone grafts & substitutes

- 9.3.3.1.1 Growing number of dental implant procedures to drive market

- 9.3.3.2 Dental membranes

- 9.3.3.2.1 Growing procedural volumes to drive market

- 9.3.3.3 Tissue regenerative materials

- 9.3.3.3.1 Rising number of cosmetic dentistry procedures to support segment growth

- 9.3.3.1 Dental bone grafts & substitutes

- 9.3.1 DIRECT RESTORATIVE MATERIALS

- 9.4 ORTHODONTICS

- 9.4.1 CLEAR ALIGNERS/REMOVABLE BRACES

- 9.4.1.1 Esthetic concerns among teens and adults to drive adoption

- 9.4.2 FIXED BRACES

- 9.4.2.1 Brackets

- 9.4.2.1.1 Advancements in orthodontic brackets to support market growth

- 9.4.2.2 Archwires

- 9.4.2.2.1 Increasing number of orthodontic procedures to drive growth

- 9.4.2.3 Anchorage appliances

- 9.4.2.3.1 Huge patient population base with malocclusions and jaw diseases to propel market growth

- 9.4.2.4 Ligatures

- 9.4.2.4.1 Advantages such as low cost, ease of use, and comfort to increased adoption of ligatures

- 9.4.2.1 Brackets

- 9.4.3 ACCESSORIES

- 9.4.3.1 Increasing number of orthodontic procedures to support demand for accessories

- 9.4.1 CLEAR ALIGNERS/REMOVABLE BRACES

- 9.5 PERIODONTICS

- 9.5.1 DENTAL ANESTHETICS

- 9.5.1.1 Injectable anesthetics

- 9.5.1.1.1 Safety and efficacy to drive the market

- 9.5.1.2 Topical anesthetics

- 9.5.1.2.1 Rising volume of pediatric dental procedures to boost usage

- 9.5.1.1 Injectable anesthetics

- 9.5.2 DENTAL HEMOSTATS

- 9.5.2.1 Oxidized regenerated cellulose-based hemostats

- 9.5.2.1.1 Superior hemostasis and bactericidal effectiveness during surgical procedures to propel demand

- 9.5.2.2 Gelatin-based hemostats

- 9.5.2.2.1 Innovations in gelatin-based hemostats to support market growth

- 9.5.2.3 Collagen-based hemostats

- 9.5.2.3.1 Reduced blood loss and effectiveness to support adoption

- 9.5.2.1 Oxidized regenerated cellulose-based hemostats

- 9.5.3 DENTAL SUTURES

- 9.5.3.1 Non-absorbable dental sutures

- 9.5.3.1.1 Possibility of discomfort during removal to restrain adoption

- 9.5.3.2 Absorbable dental sutures

- 9.5.3.2.1 Great tensile strength and high comfort for patients to promote growth

- 9.5.3.1 Non-absorbable dental sutures

- 9.5.1 DENTAL ANESTHETICS

- 9.6 INFECTION CONTROL PRODUCTS

- 9.6.1 SANITIZING GELS

- 9.6.1.1 Sanitizing gels to hold largest market share

- 9.6.2 PERSONAL PROTECTIVE WEAR

- 9.6.2.1 Government mandates for using personal protective wear to support segment growth

- 9.6.3 DISINFECTANTS

- 9.6.3.1 Emphasis on environmental disinfection in dental settings to support growth

- 9.6.1 SANITIZING GELS

- 9.7 ENDODONTICS

- 9.7.1 SHAPING & CLEANING CONSUMABLES

- 9.7.1.1 Importance of shaping & cleaning consumables in root canal treatment to propel adoption

- 9.7.2 OBTURATION CONSUMABLES

- 9.7.2.1 Increasing root canal procedures to drive demand

- 9.7.3 ACCESS PREPARATION CONSUMABLES

- 9.7.3.1 Growing demand for access preparation consumables in endodontic treatment to drive market

- 9.7.1 SHAPING & CLEANING CONSUMABLES

- 9.8 WHITENING PRODUCTS

- 9.8.1 IN-OFFICE WHITENING CONSUMABLES

- 9.8.1.1 Gels

- 9.8.1.1.1 Safety and effectiveness of gels to drive market growth

- 9.8.1.2 Resin barriers

- 9.8.1.2.1 Easy application and no patient discomfort to propel usage

- 9.8.1.3 Other in-office whitening consumables

- 9.8.1.1 Gels

- 9.8.2 TAKE-HOME WHITENING CONSUMABLES

- 9.8.2.1 Whitening trays

- 9.8.2.1.1 Lower effectiveness than other modes to restrain market growth

- 9.8.2.2 Pens

- 9.8.2.2.1 Convenience to support adoption

- 9.8.2.3 Pocket trays

- 9.8.2.3.1 Regular intake of tobacco and tannin-containing products to boost adoption

- 9.8.2.4 Other take-home whitening consumables

- 9.8.2.1 Whitening trays

- 9.8.1 IN-OFFICE WHITENING CONSUMABLES

- 9.9 FINISHING & POLISHING PRODUCTS

- 9.9.1 PROPHYLAXIS PRODUCTS

- 9.9.1.1 Pastes

- 9.9.1.1.1 High dental polishing procedure volumes to drive demand for pastes

- 9.9.1.2 Disposable agents

- 9.9.1.2.1 Greater flexibility in polishing and finishing to boost usage

- 9.9.1.3 Cups

- 9.9.1.3.1 High flexibility and stability to drive adoption

- 9.9.1.4 Brushes

- 9.9.1.4.1 Durability and ease of use to propel market

- 9.9.1.1 Pastes

- 9.9.2 FLUORIDES

- 9.9.2.1 Varnishes

- 9.9.2.1.1 Effective protection against tooth decay to boost adoption

- 9.9.2.2 Rinses

- 9.9.2.2.1 Product development efforts to drive launch of innovative offerings

- 9.9.2.3 Topical gels/oral solutions

- 9.9.2.3.1 Highly acidic nature of fluoride gels to hinder growth

- 9.9.2.4 Foams

- 9.9.2.4.1 Reduced risk of dulling and etching of restorations to propel growth

- 9.9.2.5 Trays

- 9.9.2.5.1 Rising awareness on reducing risk of caries to drive market

- 9.9.2.1 Varnishes

- 9.9.1 PROPHYLAXIS PRODUCTS

- 9.10 OTHER DENTAL CONSUMABLES

- 9.10.1 DENTAL SPLINTS

- 9.10.1.1 Rising treatment of occlusion-related disorders to propel market

- 9.10.2 DENTAL SEALANTS

- 9.10.2.1 Growing popularity and usage to support segment growth

- 9.10.3 DENTAL IMPRESSION MATERIALS

- 9.10.3.1 Frequent, repetitive usage in dental hospitals & clinics to ensure sustained demand

- 9.10.4 BONDING AGENTS/ADHESIVES

- 9.10.4.1 Applications in bonding direct and indirect restorative materials to drive market

- 9.10.5 OTHER CONSUMABLES

- 9.10.1 DENTAL SPLINTS

10 DENTAL CONSUMABLES MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 DENTAL HOSPITALS & CLINICS

- 10.2.1 RISING NUMBER OF DENTAL HOSPITALS & CLINICS IN EMERGING MARKETS TO DRIVE MARKET GROWTH

- 10.3 DENTAL LABORATORIES

- 10.3.1 INCREASING INTEREST IN COSMETIC DENTISTRY TO PROPEL MARKET GROWTH

- 10.4 DENTAL SERVICE ORGANIZATIONS

- 10.5 OTHER END USERS

11 DENTAL CONSUMABLES MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 EUROPE

- 11.2.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 11.2.2 GERMANY

- 11.2.2.1 Favorable government policies to drive demand for dental consumables

- 11.2.3 ITALY

- 11.2.3.1 Low-cost treatment and growing penetration of dental products to drive market

- 11.2.4 SPAIN

- 11.2.4.1 Increasing demand for cosmetic dentistry and growing medical tourism drive demand

- 11.2.5 FRANCE

- 11.2.5.1 Favorable government healthcare strategies to fuel market growth

- 11.2.6 UK

- 11.2.6.1 Increasing incidence of dental disorders to drive demand for dental consumables

- 11.2.7 REST OF EUROPE

- 11.3 NORTH AMERICA

- 11.3.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 11.3.2 US

- 11.3.2.1 US to dominate North American dental consumables market

- 11.3.3 CANADA

- 11.3.3.1 Rising incidence of dental caries to drive demand for dental consumables

- 11.4 ASIA PACIFIC

- 11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 11.4.2 JAPAN

- 11.4.2.1 Rising geriatric population and favorable reimbursement to support market growth

- 11.4.3 AUSTRALIA

- 11.4.3.1 Increasing incidence of dental disorders to drive demand for dental consumables

- 11.4.4 SOUTH KOREA

- 11.4.4.1 High penetration of dental implants to drive market in South Korea

- 11.4.5 CHINA

- 11.4.5.1 Growing prevalence of dental diseases to drive market

- 11.4.6 INDIA

- 11.4.6.1 India to offer lucrative growth opportunities for market players

- 11.4.7 REST OF ASIA PACIFIC

- 11.5 LATIN AMERICA

- 11.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 11.5.2 BRAZIL

- 11.5.2.1 Rising investments in R&D and growing popularity of 3D dental printing to promote market growth

- 11.5.3 MEXICO

- 11.5.3.1 Focus on improving healthcare infrastructure and availability of skilled dentists to drive the market

- 11.5.4 ARGENTINA

- 11.5.4.1 Growing demand for personalized dentistry to drive market

- 11.5.5 REST OF LATIN AMERICA

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 GROWING AWARENESS ABOUT DENTAL HYGIENE TO DRIVE MARKET GROWTH

- 11.6.2 MACROECONOMIC OUTLOOK FOR THE MIDDLE EAST & AFRICA

- 11.7 GCC COUNTRIES

- 11.7.1 RISING NUMBER OF CONFERENCES, SUMMITS AND TRAINING COURSES

- 11.7.2 MACROECONOMIC OUTLOOK FOR GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.2.1 OVERVIEW OF MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN DENTAL CONSUMABLES MARKET

- 12.3 REVENUE ANALYSIS, 2021-2025

- 12.4 MARKET SHARE ANALYSIS, 2025

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 12.5.5.1 Company footprint

- 12.5.5.2 Region footprint

- 12.5.5.3 Product footprint

- 12.5.5.4 End-user footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 12.6.5.1 Detailed list of key startups/SMEs

- 12.6.5.2 Competitive benchmarking of key startups/SMEs

- 12.7 COMPANY VALUATION & FINANCIAL METRICS

- 12.7.1 FINANCIAL METRICS

- 12.7.2 COMPANY VALUATION

- 12.8 BRAND/PRODUCT COMPARISON

- 12.9 R&D EXPENDITURE OF KEY PLAYERS

- 12.10 COMPETITIVE SCENARIO

- 12.10.1 PRODUCT LAUNCHES

- 12.10.2 DEALS

- 12.10.3 EXPANSIONS

- 12.10.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 INSTITUT STRAUMANN AG

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 ENVISTA

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches & approvals

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 DENTSPLY SIRONA

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 SOLVENTUM

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 ZIMVIE INC.

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches

- 13.1.5.3.2 Deals

- 13.1.5.3.3 Expansions

- 13.1.6 HENRY SCHEIN

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches

- 13.1.6.3.2 Deals

- 13.1.6.3.3 Expansions

- 13.1.6.3.4 Other developments

- 13.1.7 KURARAY CO., LTD.

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.7.3.2 Expansions

- 13.1.8 MITSUI CHEMICALS, INC.

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 DEALS

- 13.1.9 SHOFU

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.10 IVOCLAR VIVADENT AG

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches

- 13.1.10.3.2 Deals

- 13.1.1 INSTITUT STRAUMANN AG

- 13.2 OTHER PLAYERS

- 13.2.1 GC CORPORATION

- 13.2.2 KEYSTONE DENTAL GROUP

- 13.2.3 BEGO GMBH & CO. KG

- 13.2.4 SEPTODONT HOLDING

- 13.2.5 ULTRADENT PRODUCTS

- 13.2.6 VOCO GMBH

- 13.2.7 COLTENE GROUP

- 13.2.8 SDI LIMITED

- 13.2.9 YOUNG INNOVATIONS, INC.

- 13.2.10 DMG CHEMISCH-PHARMAZEUTISCHE FABRIK GMBH

- 13.2.11 BRASSELER USA

- 13.2.12 GEISTLICH PHARMA AG

- 13.2.13 GLIDEWELL

- 13.2.14 BISCO INC.

- 13.2.15 DENTAL TECHNOLOGIES INC.

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key data from primary sources

- 14.1.2.2 Key industry insights

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 14.4 MARKET SHARE ESTIMATION

- 14.5 RESEARCH ASSUMPTIONS

- 14.6 RESEARCH LIMITATIONS

- 14.6.1 SCOPE-RELATED LIMITATIONS

- 14.6.2 METHODOLOGY-RELATED LIMITATIONS

- 14.7 RISK ASSESSMENT

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS

List of Tables

- TABLE 1 STANDARD CURRENCY CONVERSION RATES

- TABLE 2 PROJECTED INCREASE IN ABOVE-65 AGE GROUP, BY REGION (2019-2050)

- TABLE 3 US: AVERAGE PATIENT SPENDING ON COSMETIC DENTISTRY SERVICES

- TABLE 4 AVERAGE PROCEDURAL COSTS IN TOP TEN DENTAL TOURISM DESTINATIONS (2023)

- TABLE 5 AVERAGE COST OF DENTAL TREATMENT, BY COUNTRY (2020)

- TABLE 6 PER CAPITA NATIONAL INCOME, 2021-2023 (USD)

- TABLE 7 DENTAL CONSUMABLES MARKET: UNMET NEEDS

- TABLE 8 INTERCONNECTED MARKETS

- TABLE 9 DENTAL CONSUMABLES MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 10 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2030

- TABLE 11 DENTAL CONSUMABLES MARKET: ECOSYSTEM ANALYSIS

- TABLE 12 AVERAGE SELLING PRICE TREND OF DENTAL CONSUMABLES, BY TYPE, 2023-2025 (USD)

- TABLE 13 AVERAGE SELLING PRICE TREND OF DENTAL IMPLANTS, BY COUNTRY, 2023-2025

- TABLE 14 IMPORT DATA FOR DENTAL CONSUMABLES (HS CODE 9021), BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 15 EXPORT DATA FOR DENTAL CONSUMABLES (HS CODE 9021), BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 16 DENTAL CONSUMABLES MARKET: KEY CONFERENCES & EVENTS (2026)

- TABLE 17 CAE STUDY 1: SELF-DRILLING IMPLANTS FOR IMMEDIATE LOADING OF FULL-ARCH PROSTHESES

- TABLE 18 CASE STUDY 2: ORAQIX TOPICAL ANESTHETIC SIGNIFICANTLY REDUCED PAIN DURING SRP, ENHANCING COMFORT AND PATIENT ACCEPTANCE OF PERIODONTAL THERAPY

- TABLE 19 CASE STUDY 3: TREATMENT OF LOWER ANTERIOR CROWDING WITH SELF-LIGATING DAMON SYSTEM

- TABLE 20 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 21 KEY PRODUCT-RELATED TARIFFS EFFECTIVE FOR DENTAL CONSUMABLES PRODUCTS

- TABLE 22 LIST OF PATENTS IN DENTAL CONSUMABLES MARKET (2022-2025)

- TABLE 23 TOP USE CASES & MARKET POTENTIAL

- TABLE 24 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- TABLE 25 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 26 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 27 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 28 LATIN AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 29 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 30 CERTIFICATIONS, LABELING, AND ECO-STANDARDS IN DENTAL CONSUMABLES MARKET

- TABLE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE PRODUCTS (%)

- TABLE 32 KEY BUYING CRITERIA FOR TOP THREE PRODUCTS

- TABLE 33 DENTAL CONSUMABLES MARKET: UNMET NEEDS/END-USER EXPECTATIONS

- TABLE 34 DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 35 KEY PLAYERS OFFERING DENTAL IMPLANTS

- TABLE 36 DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 37 DENTAL IMPLANTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 38 TITANIUM IMPLANTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 39 ZIRCONIUM IMPLANTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 40 DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 41 DENTAL RESTORATIONS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 42 DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 43 DIRECT RESTORATIVE MATERIALS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 44 AMALGAMS OFFERED BY KEY MARKET PLAYERS

- TABLE 45 AMALGAMS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 46 COMPOSITES OFFERED BY KEY MARKET PLAYERS

- TABLE 47 COMPOSITES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 48 GLASS IONOMERS OFFERED BY KEY MARKET PLAYERS

- TABLE 49 GLASS IONOMERS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 50 OTHER DIRECT RESTORATIVE MATERIALS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 51 INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 52 INDIRECT RESTORATIVE MATERIALS MARKET, BY COUNTRY, 2024-2031 (USD MILLION

- TABLE 53 METALS OFFERED BY KEY MARKET PLAYERS

- TABLE 54 METALS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 55 CERAMICS OFFERED BY KEY MARKET PLAYERS

- TABLE 56 CERAMICS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 57 OTHER INDIRECT RESTORATIVE MATERIALS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 58 DENTAL BIOMATERIALS OFFERED BY KEY MARKET PLAYERS

- TABLE 59 DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 60 DENTAL BIOMATERIALS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 61 DENTAL BONE GRAFTS & SUBSTITUTES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 62 DENTAL MEMBRANES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 63 TISSUE REGENERATIVE MATERIALS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 64 ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 65 ORTHODONTICS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 66 CLEAR ALIGNERS/REMOVABLE BRACES OFFERED BY KEY PLAYERS

- TABLE 67 CLEAR ALIGNERS/REMOVABLE BRACES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 68 FIXED BRACES OFFERED BY KEY PLAYERS

- TABLE 69 FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 70 FIXED BRACES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 71 BRACKETS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 72 ARCHWIRES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 73 ANCHORAGE APPLIANCES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 74 LIGATURES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 75 ACCESSORIES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 76 PERIODONTICS OFFERED BY KEY PLAYERS

- TABLE 77 PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 78 PERIODONTICS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 79 DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 80 DENTAL ANESTHETICS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 81 INJECTABLE ANESTHETICS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 82 TOPICAL ANESTHETICS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 83 DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 84 DENTAL HEMOSTATS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 85 OXIDIZED REGENERATED CELLULOSE-BASED HEMOSTATS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 86 GELATIN-BASED HEMOSTATS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 87 COLLAGEN-BASED HEMOSTATS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 88 DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 89 DENTAL SUTURES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 90 NON-ABSORBABLE DENTAL SUTURES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 91 ABSORBABLE DENTAL SUTURES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 92 INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 93 INFECTION CONTROL PRODUCTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 94 SANITIZING GELS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 95 PERSONAL PROTECTIVE WEAR MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 96 DISINFECTANTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 97 ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 98 ENDODONTICS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 99 SHAPING & CLEANING CONSUMABLES OFFERED BY KEY MARKET PLAYERS

- TABLE 100 SHAPING & CLEANING CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 101 OBTURATION CONSUMABLES OFFERED BY KEY MARKET PLAYERS

- TABLE 102 OBTURATION CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 103 ACCESS PREPARATION CONSUMABLES OFFERED BY KEY MARKET PLAYERS

- TABLE 104 ACCESS PREPARATION CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 105 WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 106 WHITENING PRODUCTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 107 IN-OFFICE WHITENING CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 108 IN-OFFICE WHITENING CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 109 GELS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 110 RESIN BARRIERS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 111 OTHER IN-OFFICE WHITENING CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 112 TAKE-HOME WHITENING CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 113 TAKE-HOME WHITENING CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 114 WHITENING TRAYS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 115 PENS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 116 POCKET TRAYS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 117 OTHER TAKE-HOME WHITENING CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 118 FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 119 FINISHING & POLISHING PRODUCTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 120 PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 121 PROPHYLAXIS PRODUCTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 122 PASTES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 123 DISPOSABLE AGENTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 124 CUPS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 125 BRUSHES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 126 FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 127 FLUORIDES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 128 VARNISHES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 129 RINSES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 130 TOPICAL GELS/ORAL SOLUTIONS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 131 FOAMS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 132 TRAYS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 133 OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 134 OTHER DENTAL CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 135 DENTAL SPLINTS OFFERED BY KEY MARKET PLAYERS

- TABLE 136 DENTAL SPLINTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 137 DENTAL SEALANTS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 138 DENTAL IMPRESSION MATERIALS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 139 BONDING AGENTS/ADHESIVES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 140 OTHER CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 141 DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 142 TOP DESTINATIONS FOR COST-EFFECTIVE DENTAL TREATMENT

- TABLE 143 DENTAL CONSUMABLES MARKET FOR DENTAL HOSPITALS & CLINICS, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 144 DENTAL CONSUMABLES MARKET FOR DENTAL LABORATORIES, BY COUNTRY, 2024-2031 (USD MILLION

- TABLE 145 US: TOP DENTAL SERVICE ORGANIZATIONS FOR DENTAL PRACTICES

- TABLE 146 DENTAL CONSUMABLES MARKET FOR DENTAL SERVICE ORGANIZATIONS, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 147 US: TOP 10 NIDCR GRANTS TO US DENTAL INSTITUTIONS (USD MILLION)

- TABLE 148 DENTAL CONSUMABLES MARKET FOR OTHER END USERS, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 149 DENTAL CONSUMABLES MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 150 EUROPE: DENTAL CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 151 EUROPE: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 152 EUROPE: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 153 EUROPE: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 154 EUROPE: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 155 EUROPE: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 156 EUROPE: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 157 EUROPE: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 158 EUROPE: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 159 EUROPE: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 160 EUROPE: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 161 EUROPE: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 162 EUROPE: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 163 EUROPE: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 164 EUROPE: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 165 EUROPE: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 166 EUROPE: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 167 EUROPE: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 168 EUROPE: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 169 EUROPE: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 170 EUROPE: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 171 EUROPE: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 172 EUROPE: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 173 GERMANY: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 174 GERMANY: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 175 GERMANY: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 176 GERMANY: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 177 GERMANY: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 178 GERMANY: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 179 GERMANY: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 180 GERMANY: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 181 GERMANY: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 182 GERMANY: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 183 GERMANY: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 184 GERMANY: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 185 GERMANY: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 186 GERMANY: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 187 GERMANY: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 188 GERMANY: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 189 GERMANY: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 190 GERMANY: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 191 GERMANY: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 192 GERMANY: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 193 GERMANY: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 194 GERMANY: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 195 ITALY: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 196 ITALY: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 197 ITALY: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 198 ITALY: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 199 ITALY: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 200 ITALY: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 201 ITALY: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 202 ITALY: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 203 ITALY: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 204 ITALY: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 205 ITALY: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 206 ITALY: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 207 ITALY: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 208 ITALY: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 209 ITALY: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 210 ITALY: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 211 ITALY: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 212 ITALY: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 213 ITALY: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 214 ITALY: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 215 ITALY: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 216 ITALY: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 217 SPAIN: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 218 SPAIN: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 219 SPAIN: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 220 SPAIN: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 221 SPAIN: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 222 SPAIN: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 223 SPAIN: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 224 SPAIN: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 225 SPAIN: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 226 SPAIN: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 227 SPAIN: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 228 SPAIN: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 229 SPAIN: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 230 SPAIN: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 231 SPAIN: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 232 SPAIN: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 233 SPAIN: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 234 SPAIN: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 235 SPAIN: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 236 SPAIN: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 237 SPAIN: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 238 SPAIN: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 239 FRANCE: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 240 FRANCE: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 241 FRANCE: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 242 FRANCE: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 243 FRANCE: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 244 FRANCE: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 245 FRANCE: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 246 FRANCE: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 247 FRANCE: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 248 FRANCE: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 249 FRANCE: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 250 FRANCE: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 251 FRANCE: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 252 FRANCE: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 253 FRANCE: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 254 FRANCE: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 255 FRANCE: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 256 FRANCE: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 257 FRANCE: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 258 FRANCE: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 259 FRANCE: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 260 FRANCE: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 261 UK: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 262 UK: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 263 UK: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 264 UK: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 265 UK: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 266 UK: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 267 UK: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 268 UK: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 269 UK: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 270 UK: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 271 UK: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 272 UK: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 273 UK: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 274 UK: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 275 UK: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 276 UK: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 277 UK: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 278 UK: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 279 UK: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 280 UK: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 281 UK: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 282 UK: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 283 REST OF EUROPE: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 284 REST OF EUROPE: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 285 REST OF EUROPE: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 286 REST OF EUROPE: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 287 REST OF EUROPE: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 288 REST OF EUROPE: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 289 REST OF EUROPE: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 290 REST OF EUROPE: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 291 REST OF EUROPE: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 292 REST OF EUROPE: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 293 REST OF EUROPE: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 294 REST OF EUROPE: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 295 REST OF EUROPE: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 296 REST OF EUROPE: FINISHING & POLISHING THE CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 297 REST OF EUROPE: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 298 REST OF EUROPE: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 299 REST OF EUROPE: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 300 REST OF EUROPE: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 301 REST OF EUROPE: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 302 REST OF EUROPE: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 303 REST OF EUROPE: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 304 REST OF EUROPE: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 305 NORTH AMERICA: DENTAL CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 306 NORTH AMERICA: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 307 NORTH AMERICA: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 308 NORTH AMERICA: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 309 NORTH AMERICA: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 310 NORTH AMERICA: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 311 NORTH AMERICA: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 312 NORTH AMERICA: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 313 NORTH AMERICA: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 314 NORTH AMERICA: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 315 NORTH AMERICA: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 316 NORTH AMERICA: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 317 NORTH AMERICA: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 318 NORTH AMERICA: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 319 NORTH AMERICA: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 320 NORTH AMERICA: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 321 NORTH AMERICA: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 322 NORTH AMERICA: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 323 NORTH AMERICA: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 324 NORTH AMERICA: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 325 NORTH AMERICA: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 326 NORTH AMERICA: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 327 NORTH AMERICA: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 328 US: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 329 US: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 330 US: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 331 US: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 332 US: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 333 US: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 334 US: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 335 US: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 336 US: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 337 US: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 338 US: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 339 US: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 340 US: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 341 US: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 342 US: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 343 US: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 344 US: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 345 US: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 346 US: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 347 US: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 348 US: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 349 US: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 350 CANADA: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 351 CANADA: DENTAL RESTORATION PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 352 CANADA: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 353 CANADA: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 354 CANADA: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 355 CANADA: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 356 CANADA: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 357 CANADA: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 358 CANADA: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 359 CANADA: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 360 CANADA: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 361 CANADA: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 362 CANADA: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 363 CANADA: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 364 CANADA: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 365 CANADA: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 366 CANADA: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 367 CANADA: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 368 CANADA: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 369 CANADA: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 370 CANADA: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 371 CANADA: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 372 ASIA PACIFIC: DENTAL CONSUMABLES MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 373 ASIA PACIFIC: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 374 ASIA PACIFIC: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 375 ASIA PACIFIC: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 376 ASIA PACIFIC: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 377 ASIA PACIFIC: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 378 ASIA PACIFIC: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 379 ASIA PACIFIC: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 380 ASIA PACIFIC: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 381 ASIA PACIFIC: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 382 ASIA PACIFIC: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 383 ASIA PACIFIC: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 384 ASIA PACIFIC: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 385 ASIA PACIFIC: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 386 ASIA PACIFIC: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 387 ASIA PACIFIC: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 388 ASIA PACIFIC: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 389 ASIA PACIFIC: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 390 ASIA PACIFIC: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 391 ASIA PACIFIC: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 392 ASIA PACIFIC: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 393 ASIA PACIFIC: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 394 ASIA PACIFIC: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 395 JAPAN: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 396 JAPAN: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 397 JAPAN: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 398 JAPAN: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 399 JAPAN: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 400 JAPAN: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 401 JAPAN: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 402 JAPAN: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 403 JAPAN: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 404 JAPAN: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 405 JAPAN: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 406 JAPAN: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 407 JAPAN: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 408 JAPAN: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 409 JAPAN: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 410 JAPAN: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 411 JAPAN: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 412 JAPAN: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 413 JAPAN: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 414 JAPAN: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 415 JAPAN: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 416 JAPAN: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 417 AUSTRALIA: ORAL HEALTH STATUS OF CHILDREN AND ADULTS

- TABLE 418 AUSTRALIA: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 419 AUSTRALIA: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 420 AUSTRALIA: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 421 AUSTRALIA: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 422 AUSTRALIA: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 423 AUSTRALIA: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 424 AUSTRALIA: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 425 AUSTRALIA: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 426 AUSTRALIA: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 427 AUSTRALIA: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 428 AUSTRALIA: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 429 AUSTRALIA: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 430 AUSTRALIA: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 431 AUSTRALIA: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 432 AUSTRALIA: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 433 AUSTRALIA: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 434 AUSTRALIA: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 435 AUSTRALIA: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 436 AUSTRALIA: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 437 AUSTRALIA: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 438 AUSTRALIA: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 439 AUSTRALIA: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 440 SOUTH KOREA: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 441 SOUTH KOREA: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 442 SOUTH KOREA: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 443 SOUTH KOREA: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 444 SOUTH KOREA: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 445 SOUTH KOREA: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 446 SOUTH KOREA: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 447 SOUTH KOREA: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 448 SOUTH KOREA: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 449 SOUTH KOREA: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 450 SOUTH KOREA: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 451 SOUTH KOREA: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 452 SOUTH KOREA: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 453 SOUTH KOREA: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 454 SOUTH KOREA: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 455 SOUTH KOREA: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 456 SOUTH KOREA: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 457 SOUTH KOREA: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 458 SOUTH KOREA: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 459 SOUTH KOREA: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 460 SOUTH KOREA: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 461 SOUTH KOREA: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 462 CHINA: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 463 CHINA: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 464 CHINA: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 465 CHINA: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 466 CHINA: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 467 CHINA: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 468 CHINA: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 469 CHINA: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 470 CHINA: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 471 CHINA: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 472 CHINA: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 473 CHINA: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 474 CHINA: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 475 CHINA: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 476 CHINA: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 477 CHINA: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 478 CHINA: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 479 CHINA: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 480 CHINA: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 481 CHINA: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 482 CHINA: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 483 CHINA: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 484 INDIA: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 485 INDIA: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 486 INDIA: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 487 INDIA: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 488 INDIA: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 489 INDIA: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 490 INDIA: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 491 INDIA: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 492 INDIA: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 493 INDIA: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 494 INDIA: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 495 INDIA: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 496 INDIA: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 497 INDIA: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 498 INDIA: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 499 INDIA: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 500 INDIA: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 501 INDIA: IN-OFFICE WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 502 INDIA: TAKE-HOME WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 503 INDIA: INFECTION CONTROL PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 504 INDIA: OTHER DENTAL CONSUMABLES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 505 INDIA: DENTAL CONSUMABLES MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 506 REST OF ASIA PACIFIC: DENTAL CONSUMABLES MARKET, BY PRODUCT, 2024-2031 (USD MILLION)

- TABLE 507 REST OF ASIA PACIFIC: DENTAL IMPLANTS MARKET, BY MATERIAL, 2024-2031 (USD MILLION)

- TABLE 508 REST OF ASIA PACIFIC: DENTAL RESTORATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 509 REST OF ASIA PACIFIC: INDIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 510 REST OF ASIA PACIFIC: DENTAL BIOMATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 511 REST OF ASIA PACIFIC: DIRECT RESTORATIVE MATERIALS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 512 REST OF ASIA PACIFIC: ORTHODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 513 REST OF ASIA PACIFIC: FIXED BRACES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 514 REST OF ASIA PACIFIC: ENDODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 515 REST OF ASIA PACIFIC: PERIODONTICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 516 REST OF ASIA PACIFIC: DENTAL SUTURES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 517 REST OF ASIA PACIFIC: DENTAL ANESTHETICS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 518 REST OF ASIA PACIFIC: DENTAL HEMOSTATS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 519 REST OF ASIA PACIFIC: FINISHING & POLISHING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 520 REST OF ASIA PACIFIC: PROPHYLAXIS PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 521 REST OF ASIA PACIFIC: FLUORIDES MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 522 REST OF ASIA PACIFIC: WHITENING PRODUCTS MARKET, BY TYPE, 2024-2031 (USD MILLION)