|

市場調查報告書

商品編碼

2033992

全球造影劑市場:按類型、劑型、診斷方法、給藥途徑、適應症、應用、最終用戶和地區分類-預測至2031年Contrast Media Market By Type, Form, Modality, Route of Administration, Indication & Region - Global Forecast to 2031 |

||||||

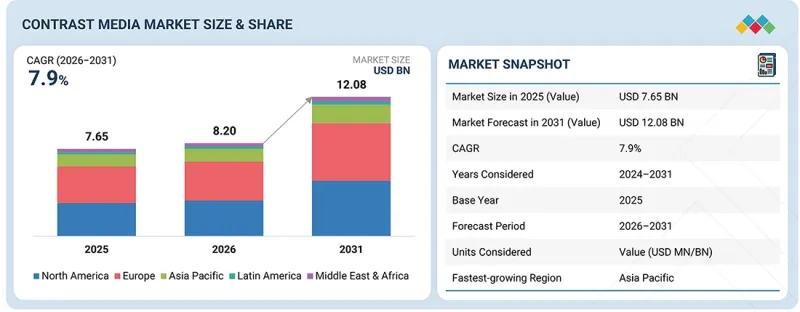

全球造影劑市場預計將從 2025 年的 76.5 億美元成長到 2031 年的 120.8 億美元,2026 年至 2031 年的複合年成長率為 7.9%。

造影劑市場主要受造影劑配方創新以及定向和可激活造影劑的開發所驅動,這些創新提高了診斷成像的準確性,並滿足了對精確診斷日益成長的需求。

| 調查範圍 | |

|---|---|

| 調查期 | 2024-2031 |

| 基準年 | 2025 |

| 預測期 | 2025-2031 |

| 目標單元 | 金額(10億美元) |

| 部分 | 按類型、劑型、診斷方法、給藥途徑、適應症、用途、最終用戶和地區 |

| 目標區域 | 北美、歐洲、亞太地區、拉丁美洲、中東和非洲 |

此外,政府對醫療保健舉措的投入,例如擴大影像服務和簽署框架協議,正在提升人們獲得先進影像檢查服務的機會。同時,隨著癌症和心血管疾病等慢性病的盛行率上升,造影增強影像檢查對於早期發現、後續觀察和治療方案製定至關重要。

“到2026年,心血管疾病領域將佔據最大的市場佔有率。”

依應用領域分類,造影市場可分為心血管疾病、癌症、胃腸道疾病、肌肉骨骼疾病、神經系統疾病和腎臟疾病。由於心血管疾病領域診斷和介入手術量龐大,包括冠動脈攝影術、CT血管攝影檢查和心臟導管介入術,預計到2026年,該領域將佔據最大的市場佔有率。全球心臟病盛行率的不斷上升,使得造影影像成為精準診斷和治療方案製定的標準技術。此外,心血管手術中對血管即時可視化的迫切需求也支撐了對造影劑的穩定需求。先進成像技術在循環系統的應用也是該領域保持領先地位的重要因素。

“在預測期內,介入性心臟病學領域預計將錄得最高的複合年成長率。”

依應用領域分類,造影劑市場可分為放射學、介入放射學和介入性心臟病學三大板塊。預計在2026年至2031年期間,介入性心臟病學板塊將呈現最高的複合年成長率,這主要得益於微創心臟治療(包括血管成形術、支架置入術和導管介入治療)的快速成長。冠狀動脈疾病和文明病導致的心臟疾病的增加,推動了相關手術數量的成長。此外,導管檢查室和影像引導技術的進步也擴大了造影劑在心臟介入治療的應用。同時,患者對早期復健和縮短住院時間的日益重視也進一步促進了該板塊的發展。

“預計亞太市場在預測期內將呈現最高的成長率。”

中國、印度和日本等國醫療基礎設施的快速發展正在推動亞太地區造影劑市場的成長。醫療成本的上升和先進影像系統的普及提高了病患接受造影增強檢查的機會。此外,慢性病盛行率的上升和醫療旅遊的蓬勃發展也增加了全部區域的影像檢查數量。同時,政府對醫院現代化和早期診斷的大力支持也加速了市場擴張的腳步。

造影劑市場的主要參與者包括 Bracco Imaging SpA(義大利)、拜耳股份公司(德國)、Guerbet(美國)、Lantheus Medical Imaging(美國)、GE HealthCare(美國)、Unijules Life Sciences Ltd.(印度)、JB Chemicals & Pharmaceuticals Limited(印度)、SanoHchemia Pharmailanos、SanoH. Diagnostic Imaging Limited(愛爾蘭)、YZJ Group(中國)、北京北陸藥業(中國)和 Livealth Biopharma Pvt. Ltd.(印度)。

調查範圍

本報告基於類型、適應症、給藥方式、給藥途徑、應用、最終用戶和地區,對造影劑市場進行了分析。該報告還涵蓋了影響市場成長的因素,分析了市場中的各種機會和挑戰,並詳細介紹了市場領導的競爭格局。此外,報告也基於趨勢分析了微觀市場,並預測了五大主要地區(以及這些地區內的各個國家)各細分市場的收入。

購買本報告的理由

本報告透過提供關於造影劑市場及其細分市場整體銷售額的最準確預測,為市場領導和新參與企業提供協助。它有助於相關人員了解競爭格局,獲得更深入的洞察,合理定位自身業務,並制定有效的打入市場策略。此外,它還幫助相關人員了解市場趨勢,並深入分析關鍵促進因素、限制因素、挑戰和機會。

本報告深入分析了以下幾點:

- 影響造影劑市場成長的因素包括:關鍵促進因素分析(使用造影劑的掃描數量增加、造影劑配方的進步、用於精準診斷的靶向和激活造影劑的開發不斷擴大,以及政府投資和英國國家醫療服務體系 (NHS)框架協議支持診斷成像的擴展);阻礙因素(副作用風險、成像程序的高成本、造影劑循環時間和穩定性的限制以及钆基造影的環境持久性);機遇(介入放射學和圖像引導手術的成長、微氣泡和超音波造影劑的開發以及造影超音波(CEUS) 在兒童腹部成像中的核准過程)兒童複雜的造影造影短缺的管理人員;

- 產品開發與創新:深入了解造影劑市場的未來技術、研發活動、新產品/服務的推出。

- 市場發展:盈利市場的全面資訊-本報告分析了各個地區的造影劑市場。

- 市場多元化:有關造影劑市場的新產品和服務、未開發的地區、近期趨勢和投資的全面資訊。

- 競爭分析:對 Bracco Imaging SpA(義大利)、拜耳股份公司(德國)、Guerbet(美國)和 GE HealthCare(美國)等主要公司的市場佔有率、成長策略和服務產品進行詳細評估。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求

- 1/2/3級玩家的策略舉措

第5章 產業趨勢

- 波特五力分析

- 總體經濟指標

- 供應鏈分析

- 生態系分析

- 價格分析

- 貿易數據分析

- 2026-2027 年主要會議和活動

- 影響客戶業務的趨勢/顛覆性因素

- 投資和資金籌措場景

- 案例研究分析

- 2025年美國關稅的影響-造影劑市場

第6章:顧客趨勢與購買行為

- 買方相關人員和採購評估標準

- 實施障礙和內部挑戰

- 最終用戶未被滿足的需求

第7章:透過科技、專利和人工智慧實施實現策略顛覆

- 主要技術

- 專利分析

- 未來應用

- 人工智慧/生成式人工智慧對造影劑市場的影響

- 成功案例和實際應用

第8章:造影劑市場(按類型)

- 碘造影劑

- 钆基造影劑

- 微氣泡造影劑

- 鋇造影劑

第9章:造影市場(依劑型分類)

- 液體

- 粉末

- 其他

第10章:造影劑市場(依考察法)

- X光

- CT

- MRI

- 超音波

第11章:造影劑市場(依給藥途徑)

- 血管內給藥

- 口服

- 直腸途徑

- 其他

第12章:造影劑市場(依適應症分類)

- 心血管疾病

- 癌症

- 胃腸道疾病

- 肌肉骨骼疾病

- 神經系統疾病

- 腎臟疾病

第13章:造影劑市場(依應用領域造影)

- 放射科

- 介入放射學

- 介入性心臟病學

第14章:造影劑市場(依最終用戶造影)

- 醫院、診所、門診手術中心

- 診斷影像中心

第15章:造影劑市場(依地區造影)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲

- 中東和非洲

- 海灣合作理事會國家

- 其他

第16章 競爭格局

- 主要公司的策略/優勢

- 造影劑市場主要公司收入分析(2021-2025)

- 2024年市佔率分析

- 企業估值和財務指標

- 品牌/產品對比

- 企業估值矩陣:主要公司,2025 年

- 公司估值矩陣:新創企業/中小企業,2025 年

- 競爭格局

第17章:公司簡介

- 大公司

- GE HEALTHCARE

- BRACCO IMAGING

- BAYER AG

- GUERBET

- LANTHEUS HOLDINGS, INC.

- UNIJULES LIFE SCIENCES LTD.

- JB CHEMICALS & PHARMACEUTICALS LIMITED

- SANOCHEMIA PHARMAZEUTIKA

- TAEJOON PHARM CO., LTD.

- JODAS EXPOIM

- IMAX DIAGNOSTIC IMAGING LIMITED

- YANGTZE RIVER PHARMACEUTICAL GROUP

- LIVEALTH

- BEIJING BEILU PHARMACEUTICAL CO., LTD.

- 其他公司

- ARCO LIFESCIENCES(I)PVT. LTD.

- STANEX DRUGS & CHEMICALS PVT. LTD.

- ONKO ILAC SAN. VE TIC. AS

- FRESENIUS KABI

- BIEM ILAC SAN. VE

- ADVACARE PHARMA

- FUJIFILM WAKO PURE CHEMICAL CORPORATION

- UNISPIRE BIOPHARMA PRIVATE LIMITED

- TRIVITRON HEALTHCARE

- NANOPET PHARMA GMBH

第18章:調查方法

第19章附錄

The global contrast media market is projected to reach USD 12.08 billion by 2031 from USD 7.65 billion in 2025, at a CAGR of 7.9% from 2026 to 2031. The contrast media market is mainly driven by innovation in contrast agent formulations and the development of targeted and activatable contrast agents, which enhance the accuracy of imaging studies and meet the increasing demand for precise diagnostics.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Type, Form, Indication, Modality, Route of Administration, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East, and Africa |

Additionally, government investments in healthcare initiatives, such as expanding diagnostic imaging services and establishing framework agreements, support access to advanced imaging options. Moreover, the rising prevalence of chronic diseases like cancer and cardiovascular conditions necessitates contrast imaging studies for early detection, monitoring, and treatment planning.

"The cardiovascular disease segment held the largest share of the market in 2026."

By indication, the contrast media market is segmented into cardiovascular disease, cancer, gastrointestinal disorders, musculoskeletal disorders, neurological disorders, and nephrological disorders. The cardiovascular disease segment held the largest market share in 2026, driven by the high volume of diagnostic and interventional procedures such as coronary angiography, CT angiography, and cardiac catheterization. The increasing prevalence of heart disorders worldwide has made contrast-enhanced imaging a standard practice for accurate diagnosis and treatment planning. Additionally, the urgent need for real-time visualization of vessels during cardiac surgery has sustained a steady demand for contrast agents. Furthermore, the introduction of advanced imaging technology in cardiology is a key driver of this segment's dominance.

"The interventional cardiology segment is projected to register the highest CAGR during the forecast period."

By application, the contrast media market is segmented into radiology, interventional radiology, and interventional cardiology. The interventional cardiology segment is expected to have the highest CAGR from 2026 to 2031, driven by the rapid growth of minimally invasive cardiac procedures, including angioplasty, stent placement, and catheter-based interventions. The number of procedures is increasing because of a rise in coronary artery disease and lifestyle-related cardiac disorders. Additionally, the development of catheterization labs and imaging-guided technologies has led to greater use of contrast agents in cardiac interventions. Furthermore, the segment is being further supported by patients' increasing preference for quick recovery and shorter hospital stays.

"The market in the Asia Pacific region is expected to witness the highest growth during the forecast period."

The rapid development of healthcare infrastructure in nations such as China, India, and Japan is driving growth in the contrast media market in the Asia Pacific region. Access to contrast-enhanced procedures is becoming better due to rising healthcare costs and the growing use of sophisticated diagnostic imaging systems. Imaging volumes are also being driven throughout the region by the rising prevalence of chronic illnesses and the growth of medical tourism. Additionally, the market is expanding faster due to the government's strong support for hospital modernization and early diagnosis.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1-48%, Tier 2-36%, and Tier 3- 16%

- By Designation: C-level-10%, Director-level-14%, and Others-76%

- By Region: North America-40%, Europe-32%, Asia Pacific-20%, Latin America-5%, and the Middle East & Africa-3%

The prominent players in the contrast media market are Bracco Imaging S.p.A. (Italy), Bayer AG (Germany), Guerbet (US), Lantheus Medical Imaging (US), GE HealthCare (US), Unijules Life Sciences Ltd. (India), J.B. Chemicals & Pharmaceuticals Limited (India), Sanochemia Pharmazeutika GmbH (Germany), Taejoon Pharm Co., Ltd. (South Korea), Jodas Expoim (India), iMax Diagnostic Imaging Limited (Ireland), YZJ Group (China), Beijing Beilu Pharmaceutical Co., Ltd. (China), and Livealth Biopharma Pvt. Ltd. (India) among others.

Research Coverage

This report studies the contrast media market based on type, indication, modality, route of administration, application, end user, and region. It also covers the factors affecting market growth, analyzes the various opportunities and challenges in the market, and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micromarkets by growth trends. It forecasts market segment revenue across five main regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will help market leaders/new entrants with information on the closest approximations of revenue for the overall contrast media market and its subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides insights into key drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (Rising number of contrast- mediated scan, Advancements in contrast agent formulations, increasing development of targeted and activatable contrast agents for precision diagnostics and Government Investment and NHS Framework Agreements Supporting Diagnostic Imaging Expansion), restraints (Risk of Adverse Reactions, High Cost of Imaging Procedures, Limited circulation time and stability of contrast agents, environmental persistence of gadolinium-based contrast agents), opportunities (Growth of Interventional Radiology and Image-Guided Procedures, Development of Microbubble and Ultrasound Contrast Agents, Expansion of Contrast-Enhancced Ultrasound (CEUS) Applications in Pediatric Abdominal Imaging), and challenges (Workforce Shortages in Radiology, Supply Chain Vulnerabilities, Complex Regulatory Approval Pathways for Novel and Multimodal Contrast Agents) influencing the growth of the contrast media market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the contrast media market

- Market Development: Comprehensive information about lucrative markets-the report analyses the contrast media market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the contrast media market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Bracco Imaging S.p.A. (Italy), Bayer AG (Germany), Guerbet (US), GE HealthCare (US), and others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 OBJECTIVES OF THE STUDY

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED AND REGIONS CONSIDERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 MARKET STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN CONTRAST MEDIA MARKET

- 2.4 HIGH GROWTH SEGMENTS

3 PREMIUM INSIGHTS

- 3.1 CONTRAST MEDIA MARKET OVERVIEW

- 3.2 CONTRAST MEDIA MARKET, BY REGION

- 3.3 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY COUNTRY AND END USER

- 3.4 GEOGRAPHIC SNAPSHOT OF CONTRAST MEDIA MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Advancements in contrast agent formulations

- 4.2.1.2 Precision Diagnostics Enabled by Targeted and Activatable Contrast Agents

- 4.2.1.3 Government Investments and Healthcare Procurement Initiatives

- 4.2.1.4 Rising number of contrast-mediated scans

- 4.2.2 RESTRAINTS

- 4.2.2.1 Limited Circulation Time and Stability of Certain Contrast Agents

- 4.2.2.2 Environmental persistence of gadolinium-based contrast agents

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of Multimodal Imaging Technologies

- 4.2.3.2 Expansion of Contrast-enhanced ultrasound (CEUS) applications in pediatric imaging

- 4.2.3.3 Increasing demand for low-dose, high-relaxivity contrast agents for neonates and infants

- 4.2.4 CHALLENGES

- 4.2.4.1 Safety and toxicity concerns associated with gadolinium and nanoparticle-based contrast agents

- 4.2.4.2 Complex regulatory approval pathways for novel and multimodal contrast agents

- 4.2.4.3 Complexity in scalable synthesis and standardization of nanoparticle-based contrast agents

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 HEALTHCARE EXPENDITURE AND INFRASTRUCTURE OUTLOOK

- 5.2.2.1 Macroeconomic outlook for NORTH AMERICA

- 5.2.3 MACROECONOMIC OUTLOOK FOR EUROPE

- 5.2.4 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 5.2.5 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 5.2.6 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.2 AVERAGE SELLING PRICE OF CONTRAST MEDIA PRODUCTS, BY KEY PLAYER

- 5.5.3 AVERAGE SELLING PRICE TREND OF CONTRAST MEDIA PRODUCTS, BY KEY PLAYER, 2024

- 5.6 TRADE DATA ANALYSIS

- 5.6.1 IMPORT DATA (HS CODE 300630)

- 5.6.2 EXPORT DATA (HS CODE 300630)

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CASE STUDY 1: MACROCYCLIC CONTRAST AGENTS FOR IMPROVED MRI SAFETY

- 5.10.2 CASE STUDY 2: IODINATED CONTRAST MEDIA OPTIMIZATION IN CT IMAGING

- 5.10.3 CASE STUDY 3: LOW-DOSE MRI CONTRAST AGENT FOR PEDIATRIC MRI IMAGING

- 5.11 IMPACT OF 2025 US TARIFF- CONTRAST MEDIA MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.5 IMPACT ON END USERS

6 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 6.1 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 6.1.1 BUYING CRITERIA

- 6.1.2 DECISION-MAKING PROCESS

- 6.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 6.3 UNMET NEEDS FROM END USERS

- 6.3.1 UNMET NEEDS FROM END USERS

7 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, AND AI ADOPTION

- 7.1 KEY TECHNOLOGIES

- 7.1.1 CONTRAST-ENHANCED ULTRASOUND (CEUS) ADVANCEMENTS

- 7.1.1.1 Targeted and molecular contrast agents

- 7.1.1.2 Advanced gadolinium-based agents and hyperpolarized techniques

- 7.1.2 COMPLEMENTARY TECHNOLOGIES

- 7.1.2.1 Automated contrast injector systems

- 7.1.1 CONTRAST-ENHANCED ULTRASOUND (CEUS) ADVANCEMENTS

- 7.2 PATENT ANALYSIS

- 7.2.1 CONTRAST MEDIA MARKET: LIST OF PATENTS

- 7.3 FUTURE APPLICATIONS

- 7.4 IMPACT OF AI/GEN AI ON CONTRAST MEDIA MARKET

- 7.4.1 TOP USE CASES AND MARKET POTENTIAL

- 7.4.2 BEST PRACTICES IN CONTRAST MEDIA.

- 7.4.3 CASE STUDIES OF AI IMPLEMENTATION IN CONTRAST MEDIA MARKET

- 7.4.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 7.4.5 CLIENT READINESS TO ADOPT GENERATIVE AI IN CONTRAST MEDIA MARKET

- 7.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

8 CONTRAST MEDIA MARKET, BY TYPE

- 8.1 INTRODUCTION

- 8.2 IODINATED CONTRAST MEDIA

- 8.2.1 RISING ADOPTION OF CT IMAGING INCREASES DEMAND

- 8.3 GADOLINIUM-BASED CONTRAST MEDIA

- 8.3.1 SAFETY CONCERNS ASSOCIATED WITH GADOLINIUM-BASED CONTRAST AGENTS RESTRAIN MARKET GROWTH

- 8.4 MICROBUBBLE CONTRAST MEDIA

- 8.4.1 GROWING PHYSICIAN PREFERENCE FOR CONTRAST-ENHANCED ULTRASOUND DRIVES ADOPTION

- 8.5 BARIUM-BASED CONTRAST MEDIA

- 8.5.1 ADVERSE EFFECTS ASSOCIATED WITH BARIUM SULFATE CONTRAST MEDIA LIMIT CLINICAL USAGE

9 CONTRAST MEDIA MARKET, BY FORM

- 9.1 INTRODUCTION

- 9.2 LIQUID

- 9.2.1 CONVENIENCE OF USE IN HOSPITALS AND DIAGNOSTIC CENTERS TO DRIVE MARKET GROWTH

- 9.3 POWDER

- 9.3.1 CONVENIENT HANDLING, STORAGE, AND TRANSPORTATION DRIVES INCREASED ADOPTION

- 9.4 OTHER FORMS

10 CONTRAST MEDIA MARKET, BY MODALITY

- 10.1 INTRODUCTION

- 10.2 X-RAY

- 10.2.1 DEVELOPMENT OF SAFER, LOW-CONCENTRATION CONTRAST AGENTS FOR X-RAY - KEY OPPORTUNITY

- 10.3 CT

- 10.3.1 INCREASING NUMBER OF CT EXAMINATIONS TO PROPEL MARKET

- 10.4 MRI

- 10.4.1 INCREASING FOCUS ON NEXT-GENERATION GADOLINIUM-BASED CONTRAST AGENTS TO ENHANCE SAFETY AND IMAGING PERFORMANCE

- 10.5 ULTRASOUND

- 10.5.1 FLEXIBLE AND LOW-COST DIAGNOSTIC IMAGING MODALITY - KEY FACTORS DRIVING MARKET GROWTH

11 CONTRAST MEDIA MARKET, BY ROUTE OF ADMINISTRATION

- 11.1 INTRODUCTION

- 11.2 INTRAVASCULAR ROUTE

- 11.2.1 INCREASING CLINICAL RELIANCE FOR ENHANCED DIAGNOSTIC IMAGING AND TREATMENT OUTCOMES TO DRIVE SEGMENT

- 11.2.1.1 Intravenous (IV) route

- 11.2.1.2 Intra-arterial (IA) route

- 11.2.1 INCREASING CLINICAL RELIANCE FOR ENHANCED DIAGNOSTIC IMAGING AND TREATMENT OUTCOMES TO DRIVE SEGMENT

- 11.3 ORAL ROUTE

- 11.3.1 ENHANCING GASTROINTESTINAL VISUALIZATION WITH ORAL CONTRAST AGENTS IN DIAGNOSTIC IMAGING

- 11.4 RECTAL ROUTE

- 11.4.1 RISING DEMAND FOR ACCURATE POST-SURGICAL COMPLICATION DETECTION TO DRIVE ADOPTION

- 11.5 OTHER ROUTES

12 CONTRAST MEDIA MARKET, BY INDICATION

- 12.1 INTRODUCTION

- 12.2 CARDIOVASCULAR DISEASE

- 12.2.1 HIGH BURDEN OF CVD TO DRIVE MARKET

- 12.3 CANCER

- 12.3.1 ADVANCED ONCOLOGIC DIAGNOSTICS THROUGH CONTRAST-ENHANCED ULTRASOUND IMAGING TO BOOST SEGMENT

- 12.4 GASTROINTESTINAL DISORDERS

- 12.4.1 EXPANDING ROLE OF CEUS IN PEDIATRIC GASTROINTESTINAL DISORDERS AND NEONATAL IMAGING TO PROPEL GROWTH

- 12.5 MUSCULOSKELETAL DISORDERS

- 12.5.1 RISING INCIDENCE OF WORK-RELATED MUSCULOSKELETAL DISORDERS TO SUPPORT MARKET GROWTH

- 12.6 NEUROLOGICAL DISORDERS

- 12.6.1 INCREASING BURDEN OF NEUROLOGICAL DISORDERS DRIVES DEMAND

- 12.7 NEPHROLOGICAL DISORDERS

- 12.7.1 RISING PREVALENCE OF END-STAGE RENAL DISEASE TO DRIVE DEMAND

13 CONTRAST MEDIA MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 RADIOLOGY

- 13.2.1 GROWING NUMBER OF DIAGNOSTIC PROCEDURES TO DRIVE MARKET

- 13.3 INTERVENTIONAL RADIOLOGY

- 13.3.1 RISING ADOPTION OF MINIMALLY INVASIVE INTERVENTIONS TO DRIVE MARKET

- 13.4 INTERVENTIONAL CARDIOLOGY

- 13.4.1 RISING INCIDENCE OF CARDIAC DISEASES TO DRIVE MARKET

14 CONTRAST MEDIA MARKET, BY END USER

- 14.1 INTRODUCTION

- 14.2 HOSPITALS, CLINICS, AND AMBULATORY SURGERY CENTERS

- 14.2.1 INCREASING ADOPTION OF DIAGNOSTIC IMAGING MODALITIES TO DRIVE MARKET

- 14.3 DIAGNOSTIC IMAGING CENTERS

- 14.3.1 INCREASING NUMBER OF PRIVATE IMAGING CENTERS TO PROPEL MARKET

15 CONTRAST MEDIA MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Rising incidence of chronic diseases to drive market

- 15.2.2 CANADA

- 15.2.2.1 Growth influenced by supply expansion and increasing market competition

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 GERMANY

- 15.3.1.1 Presence of well-established players to support market growth

- 15.3.2 FRANCE

- 15.3.2.1 Growth supported by high imaging utilization and expanding clinical applications

- 15.3.3 UK

- 15.3.3.1 Innovation in next-generation MRI contrast agents to drive growth

- 15.3.4 ITALY

- 15.3.4.1 Growth driven by innovation in ultrasound contrast agents and product expansion

- 15.3.5 SPAIN

- 15.3.5.1 Shift toward safer and cost-efficient low-osmolar contrast agents in CT imaging to boost market

- 15.3.6 REST OF EUROPE

- 15.3.1 GERMANY

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Strong domestic capabilities and strategic supply chain position drive market growth

- 15.4.2 JAPAN

- 15.4.2.1 Advanced imaging infrastructure and strategic industry expansion to drive demand

- 15.4.3 INDIA

- 15.4.3.1 Expanding domestic manufacturing and increasing imaging demand to propel market growth

- 15.4.4 AUSTRALIA

- 15.4.5 SOUTH KOREA

- 15.4.5.1 AI-driven imaging optimization and rising early-onset cancer burden reshaping demand

- 15.4.6 REST OF ASIA PACIFIC

- 15.4.7 LATIN AMERICA

- 15.4.7.1 Cost-sensitive procurement and rising CT imaging volumes drive contrast media utilization

- 15.4.8 BRAZIL

- 15.4.8.1 Rising disease burden drives demand amid safety and access challenges

- 15.4.9 MEXICO

- 15.4.9.1 Rising CKD burden, low healthcare spending, and environmental concerns influence contrast media utilization

- 15.4.10 REST OF LATIN AMERICA

- 15.4.10.1 Fragmented access, import dependence, and public-private imbalance shaping contrast media utilization

- 15.4.11 MIDDLE EAST & AFRICA

- 15.4.11.1 High burden of chronic diseases to drive market

- 15.4.12 GCC COUNTRIES

- 15.4.12.1 Increasing government investments in healthcare sector and growing pharmaceuticals industry to drive market

- 15.4.13 REST OF MIDDLE EAST & AFRICA

- 15.4.13.1 Import dependence and unbalanced imaging access driving selective contrast media utilization

- 15.4.1 CHINA

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 16.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN CONTRAST MEDIA MARKET

- 16.3 REVENUE ANALYSIS OF KEY PLAYERS IN CONTRAST MEDIA MARKET 2021-2025

- 16.4 MARKET SHARE ANALYSIS, 2024

- 16.4.1 MARKET RANKING OF KEY PLAYERS, 2024

- 16.5 COMPANY VALUATION & FINANCIAL METRICS

- 16.5.1 FINANCIAL METRICS

- 16.5.2 COMPANY VALUATION

- 16.6 BRAND/PRODUCT COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 PERVASIVE PLAYERS

- 16.7.3 EMERGING LEADERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Product type footprint

- 16.7.5.4 MODALITY FOOTPRINT

- 16.7.5.5 ROUTE OF ADMINISTRATION FOOTPRINT

- 16.7.5.6 INDICATION FOOTPRINT

- 16.7.5.7 END USER FOOTPRINT

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING OF STARTUPS/SMES, 2025

- 16.8.5.1 CONTRAST MEDIA MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES & APPROVALS

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 GE HEALTHCARE

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses & competitive threats

- 17.1.2 BRACCO IMAGING

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses & competitive threats

- 17.1.3 BAYER AG

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Expansions

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses & competitive threats

- 17.1.4 GUERBET

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product approvals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses & competitive threats

- 17.1.5 LANTHEUS HOLDINGS, INC.

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 MnM view

- 17.1.5.3.1 Key strengths

- 17.1.5.3.2 Strategic choices

- 17.1.5.3.3 Weaknesses & competitive threats

- 17.1.6 UNIJULES LIFE SCIENCES LTD.

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.7 J.B. CHEMICALS & PHARMACEUTICALS LIMITED

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.8 SANOCHEMIA PHARMAZEUTIKA

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.9 TAEJOON PHARM CO., LTD.

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.10 JODAS EXPOIM

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.11 IMAX DIAGNOSTIC IMAGING LIMITED

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Pipeline products

- 17.1.12 YANGTZE RIVER PHARMACEUTICAL GROUP

- 17.1.12.1 Business overview

- 17.1.12.2 Pipeline products

- 17.1.13 LIVEALTH

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.14 BEIJING BEILU PHARMACEUTICAL CO., LTD.

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.1 GE HEALTHCARE

- 17.2 OTHER PLAYERS

- 17.2.1 ARCO LIFESCIENCES (I) PVT. LTD.

- 17.2.2 STANEX DRUGS & CHEMICALS PVT. LTD.

- 17.2.3 ONKO ILAC SAN. VE TIC. A.S.

- 17.2.4 FRESENIUS KABI

- 17.2.5 BIEM ILAC SAN. VE

- 17.2.6 ADVACARE PHARMA

- 17.2.7 FUJIFILM WAKO PURE CHEMICAL CORPORATION

- 17.2.8 UNISPIRE BIOPHARMA PRIVATE LIMITED

- 17.2.9 TRIVITRON HEALTHCARE

- 17.2.10 NANOPET PHARMA GMBH

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.2 RESEARCH DESIGN

- 18.2.1 SECONDARY RESEARCH

- 18.2.1.1 Objectives of secondary research

- 18.2.1.2 Key data from secondary sources

- 18.2.2 PRIMARY RESEARCH

- 18.2.2.1 Objectives of primary research

- 18.2.2.2 Key industry insights

- 18.2.1 SECONDARY RESEARCH

- 18.3 MARKET SIZE ESTIMATION METHODOLOGY

- 18.3.1 BOTTOM-UP APPROACH

- 18.3.1.1 Approach 1: Company revenue estimation approach

- 18.3.1.2 Approach 4: Primary interviews

- 18.3.2 TOP-DOWN APPROACH

- 18.3.1 BOTTOM-UP APPROACH

- 18.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 18.5 MARKET SHARE ASSESSMENT

- 18.6 RESEARCH ASSUMPTIONS

- 18.7 RESEARCH LIMITATIONS

- 18.8 RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS

List of Tables

- TABLE 1 CONTRAST MEDIA MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 CONTRAST MEDIA MARKET: IMPACT ANALYSIS OF MARKET DYNAMICS

- TABLE 3 KEY TECHNOLOGICAL ADVANCEMENTS IN CONTRAST AGENT FORMULATIONS AND THEIR CLINICAL BENEFITS

- TABLE 4 EMERGING TARGETED AND ACTIVATABLE CONTRAST AGENTS SUPPORTING PRECISION DIAGNOSTICS

- TABLE 5 EMERGING AND CLINICAL APPLICATIONS OF CONTRAST-ENHANCED ULTRASOUND (CEUS) IN PEDIATRIC ABDOMINAL IMAGING

- TABLE 6 CONTRAST AGENT MARKET: UNMET NEEDS

- TABLE 7 STRATEGIC MOVES BY TIER 1, TIER 2, AND TIER 3 PLAYERS IN CONTRAST MEDIA MARKET

- TABLE 8 CONTRAST MEDIA MARKET: PORTER'S FIVE FORCES

- TABLE 9 NORTH AMERICA: MACROECONOMIC OUTLOOK

- TABLE 10 EUROPE: MACROECONOMIC OUTLOOK

- TABLE 11 ASIA PACIFIC: MACROECONOMIC INDICATORS

- TABLE 12 LATIN AMERICA: MACROECONOMIC OUTLOOK

- TABLE 13 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- TABLE 14 CONTRAST MEDIA MARKET: ROLE OF ECOSYSTEM

- TABLE 15 AVERAGE SELLING PRICE OF CONTRAST MEDIA PRODUCT TYPES, BY REGION, 2024-2026(USD)

- TABLE 16 AVERAGE SELLING PRICE TREND OF CONTRAST MEDIA PRODUCTS, BY KEY PLAYER, (USD)

- TABLE 17 IMPORT DATA FOR HS CODE 300630, BY COUNTRY, 2021-2025 (USD THOUSAND)

- TABLE 18 EXPORT DATA FOR HS CODE 300630 BY COUNTRY, 2021-2025 (USD THOUSAND)

- TABLE 19 CONTRAST MEDIA MARKET: KEY CONFERENCES & EVENTS (2026-2027)

- TABLE 20 CONTRAST MEDIA APPLICATION IN MRI SAFETY AND STABILITY

- TABLE 21 CONTRAST MEDIA APPLICATION IN CT IMAGING OPTIMIZATION

- TABLE 22 CONTRAST MEDIA APPLICATION IN PEDIATRIC MRI IMAGING

- TABLE 23 US ADJUSTED RECIPROCAL TARIFF RATES IN MEDTECH INDUSTRY

- TABLE 24 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR CONTRAST MEDIA MARKET, BY PRODUCT

- TABLE 25 KEY BUYING CRITERIA FOR CONTRAST MEDIA MARKET, BY END USER

- TABLE 26 CONTRAST MEDIA MARKET: UNMET NEED ANALYSIS

- TABLE 27 KEY AGENTS USED IN CONTRAST-ENHANCED ULTRASOUND (CEUS)

- TABLE 28 CONTRAST MEDIA MARKET: KEY PATENTS, 2016-2020

- TABLE 29 KEY COMPANIES IMPLEMENTING AI IN CONTRAST MEDIA ECOSYSTEM

- TABLE 30 CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 31 IODINATED CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 32 GADOLINIUM-BASED CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 33 MICROBUBBLE CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 34 BARIUM-BASED CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 35 CONTRAST MEDIA MARKET, BY FORM, 2024-2031 (USD MILLION)

- TABLE 36 LIQUID CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 37 POWDER CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 38 OTHER FORMS: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 39 CONTRAST MEDIA MARKET, BY MODALITY, 2024-2031 (USD MILLION)

- TABLE 40 ENGLAND: COUNT OF X-RAY IMAGING ACTIVITY ON NHS PATIENTS, MAY 2023-MAY 2024

- TABLE 41 X-RAY: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 42 ENGLAND: COUNT OF CT IMAGING ACTIVITY ON NHS PATIENTS, MAY 2023-MAY 2024

- TABLE 43 CT: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 44 ENGLAND: COUNT OF MRI IMAGING ACTIVITY ON NHS PATIENTS, MAY 2023-MAY 2024

- TABLE 45 MRI: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 46 ENGLAND: COUNT OF ULTRASOUND IMAGING ACTIVITY ON NHS PATIENTS, MAY 2023-MAY 2024

- TABLE 47 ULTRASOUND: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 48 CONTRAST MEDIA MARKET, BY ROUTE OF ADMINISTRATION, 2024-2031 (USD MILLION)

- TABLE 49 INTRAVASCULAR ROUTE: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 50 IV ROUTE: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 51 IA ROUTE: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 52 TYPES OF ORAL CT CONTRAST AGENTS, INCLUDING AGENTS CURRENTLY AVAILABLE AND AGENTS UNDER DEVELOPMENT

- TABLE 53 ORAL ROUTE: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 54 RECTAL ROUTE: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 55 OTHER ROUTES: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 56 CONTRAST MEDIA MARKET, BY INDICATION, 2024-2031 (USD MILLION)

- TABLE 57 CARDIOVASCULAR DISEASE: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 58 CANCER: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 59 GASTROINTESTINAL DISORDERS: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 60 MUSCULOSKELETAL DISORDERS: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 61 NEUROLOGICAL DISORDERS: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 62 NEPHROLOGICAL DISORDERS: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 63 CONTRAST MEDIA MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 64 RADIOLOGY: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 65 INTERVENTIONAL RADIOLOGY: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 66 INTERVENTIONAL CARDIOLOGY: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 67 CONTRAST MEDIA MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 68 HOSPITALS, CLINICS, AND AMBULATORY SURGERY CENTERS: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 69 DIAGNOSTIC IMAGING CENTERS: CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 70 CONTRAST MEDIA MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 71 NORTH AMERICA: CONTRAST MEDIA MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 72 NORTH AMERICA: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 73 NORTH AMERICA: CONTRAST MEDIA MARKET, BY FORM, 2024-2031 (USD MILLION)

- TABLE 74 NORTH AMERICA: CONTRAST MEDIA MARKET, BY MODALITY, 2024-2031 (USD MILLION)

- TABLE 75 NORTH AMERICA: CONTRAST MEDIA MARKET, BY ROUTE OF ADMINISTRATION, 2024-2031 (USD MILLION)

- TABLE 76 NORTH AMERICA: CONTRAST MEDIA MARKET, BY INTRAVASCULAR ROUTE, 2024-2031 (USD MILLION)

- TABLE 77 NORTH AMERICA: CONTRAST MEDIA MARKET, BY INDICATION, 2024-2031 (USD MILLION)

- TABLE 78 NORTH AMERICA: CONTRAST MEDIA MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 79 NORTH AMERICA: CONTRAST MEDIA MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 80 US: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 81 CANADA: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 82 EUROPE: CONTRAST MEDIA MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 83 EUROPE: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 84 EUROPE: CONTRAST MEDIA MARKET, BY FORM, 2024-2031 (USD MILLION)

- TABLE 85 EUROPE: CONTRAST MEDIA MARKET, BY MODALITY, 2024-2031 (USD MILLION)

- TABLE 86 EUROPE: CONTRAST MEDIA MARKET, BY ROUTE OF ADMINISTRATION, 2024-2031 (USD MILLION)

- TABLE 87 EUROPE: CONTRAST MEDIA MARKET, BY INTRAVASCULAR ROUTE, 2024-2031 (USD MILLION)

- TABLE 88 EUROPE: CONTRAST MEDIA MARKET, BY INDICATION, 2024-2031 (USD MILLION)

- TABLE 89 EUROPE: CONTRAST MEDIA MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 90 EUROPE: CONTRAST MEDIA MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 91 GERMANY: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 92 FRANCE: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 93 UK: COUNT OF IMAGING ACTIVITY ON NHS PATIENTS, MAY 2023-MAY 2024

- TABLE 94 UK: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 95 ITALY: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 96 SPAIN: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 97 REST OF EUROPE: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 98 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 99 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 100 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY FORM, 2024-2031 (USD MILLION)

- TABLE 101 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY MODALITY, 2024-2031 (USD MILLION)

- TABLE 102 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY ROUTE OF ADMINISTRATION, 2024-2031 (USD MILLION)

- TABLE 103 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY INTRAVASCULAR ROUTE, 2024-2031 (USD MILLION)

- TABLE 104 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 105 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY INDICATION, 2024-2031 (USD MILLION)

- TABLE 106 ASIA PACIFIC: CONTRAST MEDIA MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 107 CHINA: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 108 JAPAN: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 109 INDIA: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 110 HIGH CANCER BURDEN AND STRONG HEALTHCARE SPENDING - KEY DEMAND DRIVERS

- TABLE 111 AUSTRALIA: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 112 SOUTH KOREA: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 113 REST OF ASIA PACIFIC: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 114 LATIN AMERICA: CONTRAST MEDIA MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 115 LATIN AMERICA: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 116 LATIN AMERICA: CONTRAST MEDIA MARKET, BY FORM, 2024-2031 (USD MILLION)

- TABLE 117 LATIN AMERICA: CONTRAST MEDIA MARKET, BY MODALITY, 2024-2031 (USD MILLION)

- TABLE 118 LATIN AMERICA: CONTRAST MEDIA MARKET, BY ROUTE OF ADMINISTRATION, 2024-2031 (USD MILLION)

- TABLE 119 LATIN AMERICA: CONTRAST MEDIA MARKET, BY INTRAVASCULAR ROUTE, 2024-2031 (USD MILLION)

- TABLE 120 LATIN AMERICA: CONTRAST MEDIA MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 121 LATIN AMERICA: CONTRAST MEDIA MARKET, BY INDICATION, 2024-2031 (USD MILLION)

- TABLE 122 LATIN AMERICA: CONTRAST MEDIA MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 123 BRAZIL: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 124 MEXICO: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 125 REST OF LATIN AMERICA: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 126 MIDDLE EAST & AFRICA: CONTRAST MEDIA MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 127 MIDDLE EAST & AFRICA: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 128 MIDDLE EAST & AFRICA: CONTRAST MEDIA MARKET, BY FORM, 2024-2031 (USD MILLION)

- TABLE 129 MIDDLE EAST & AFRICA: CONTRAST MEDIA MARKET, BY MODALITY, 2024-2031 (USD MILLION)

- TABLE 130 MIDDLE EAST & AFRICA: CONTRAST MEDIA MARKET, BY ROUTE OF ADMINISTRATION, 2024-2031 (USD MILLION)

- TABLE 131 MIDDLE EAST & AFRICA: CONTRAST MEDIA MARKET, BY INTRAVASCULAR ROUTE, 2024-2031 (USD MILLION)

- TABLE 132 MIDDLE EAST & AFRICA: CONTRAST MEDIA MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 133 MIDDLE EAST & AFRICA: CONTRAST MEDIA MARKET, BY INDICATION, 2024-2031 (USD MILLION)

- TABLE 134 MIDDLE EAST & AFRICA: CONTRAST MEDIA MARKET, BY END USER, 2024-2031 (USD MILLION)

- TABLE 135 GCC COUNTRIES: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 136 REST OF MIDDLE EAST & AFRICA: CONTRAST MEDIA MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 137 OVERVIEW OF STRATEGIES DEPLOYED BY KEY PLAYERS IN CONTRAST MEDIA MARKET, 2022-2025

- TABLE 138 CONTRAST MEDIA MARKET: DEGREE OF COMPETITION

- TABLE 139 CONTRAST MEDIA MARKET: REGION FOOTPRINT

- TABLE 140 CONTRAST MEDIA MARKET: PRODUCT TYPE FOOTPRINT

- TABLE 141 CONTRAST MEDIA MARKET: MODALITY FOOTPRINT

- TABLE 142 CONTRAST MEDIA MARKET: ROUTE OF ADMINISTRATION FOOTPRINT

- TABLE 143 CONTRAST MEDIA MARKET: INDICATION FOOTPRINT

- TABLE 144 CONTRAST MEDIA MARKET: END USER FOOTPRINT

- TABLE 145 CONTRAST MEDIA MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/ SME PLAYERS, BY PRODUCT TYPE, AND REGION

- TABLE 146 CONTRAST MEDIA MARKET: PRODUCT LAUNCHES & APPROVALS, JANUARY 2023-JUNE 2026

- TABLE 147 CONTRAST MEDIA MARKET: DEALS, JANUARY 2023-JUNE 2026

- TABLE 148 CONTRAST MEDIA MARKET: EXPANSIONS, JANUARY 2023-JUNE 2026

- TABLE 149 GE HEALTHCARE: COMPANY OVERVIEW

- TABLE 150 GE HEALTHCARE: PRODUCTS OFFERED

- TABLE 151 GE HEALTHCARE: PRODUCT LAUNCHES, JANUARY 2023-JANUARY 2026

- TABLE 152 BRACCO IMAGING: COMPANY OVERVIEW

- TABLE 153 BRACCO IMAGING: PRODUCTS OFFERED

- TABLE 154 BRACCO IMAGING: PRODUCT LAUNCHES, JANUARY 2023-JANUARY 2026

- TABLE 155 BRACCO IMAGING: DEALS, JANUARY 2023-JANUARY 2026

- TABLE 156 BAYER AG: COMPANY OVERVIEW

- TABLE 157 BAYER AG: PRODUCTS OFFERED

- TABLE 158 BAYER AG: EXPANSIONS, JANUARY 2023-JANUARY 2026

- TABLE 159 GUERBET : COMPANY OVERVIEW

- TABLE 160 GUERBET: PRODUCTS OFFERED

- TABLE 161 GUERBET : PRODUCT APPROVALS, JANUARY 2023-JANUARY 2026

- TABLE 162 LANTHEUS HOLDINGS, INC.: COMPANY OVERVIEW

- TABLE 163 LANTHEUS HOLDINGS, INC.: PRODUCTS OFFERED

- TABLE 164 UNIJULES LIFE SCIENCES LTD.: COMPANY OVERVIEW

- TABLE 165 UNIJULES LIFE SCIENCES LTD. PRODUCTS OFFERED

- TABLE 166 J.B. CHEMICALS & PHARMACEUTICALS LIMITED: COMPANY OVERVIEW

- TABLE 167 J.B. CHEMICALS & PHARMACEUTICALS LIMITED: PRODUCTS OFFERED

- TABLE 168 SANOCHEMIA PHARMAZEUTIKA: BUSINESS OVERVIEW

- TABLE 169 SANOCHEMIA PHARMAZEUTIKA GMBH : PRODUCTS OFFERED

- TABLE 170 TAEJOON PHARM CO., LTD.: BUSINESS OVERVIEW

- TABLE 171 TAEJOON PHARM CO., LTD: PRODUCTS OFFERED

- TABLE 172 JODAS EXPOIM: BUSINESS OVERVIEW

- TABLE 173 JODAS EXPOIM : PRODUCTS OFFERED

- TABLE 174 IMAX DIAGNOSTIC IMAGING LIMITED: BUSINESS OVERVIEW

- TABLE 175 IMAX DIAGNOSTIC IMAGING LIMITED : PRODUCTS OFFERED

- TABLE 176 IMAX DIAGNOSTIC IMAGING LIMITED : PIPELINE PRODUCTS

- TABLE 177 YANGTZE RIVER PHARMACEUTICAL GROUP: BUSINESS OVERVIEW

- TABLE 178 YANGTZE RIVER PHARMACEUTICAL GROUP: PIPELINE PRODUCTS

- TABLE 179 LIVEALTH: BUSINESS OVERVIEW

- TABLE 180 LIVEALTH: PRODUCTS OFFERED

- TABLE 181 BEIJING BEILU PHARMACEUTICAL CO., LTD.: BUSINESS OVERVIEW

- TABLE 182 BEIJING BEILU PHARMACEUTICAL CO., LTD.: PRODUCTS OFFERED

- TABLE 183 BEIJING BEILU PHARMACEUTICAL CO., LTD.: OTHER DEVELOPMENTS, JANUARY 2023-JANUARY 2026

- TABLE 184 ARCO LIFESCIENCES (I) PVT. LTD.: COMPANY OVERVIEW

- TABLE 185 STANEX DRUGS & CHEMICALS PVT. LTD.: COMPANY OVERVIEW

- TABLE 186 ONKO ILAC SAN. VE TIC. A.S.: COMPANY OVERVIEW

- TABLE 187 FRESENIUS KABI: COMPANY OVERVIEW

- TABLE 188 BIEM ILAC SAN. VE: COMPANY OVERVIEW

- TABLE 189 ADVACARE PHARMA: COMPANY OVERVIEW

- TABLE 190 FUJIFILM WAKO CHEMICAL CORPORATION: COMPANY OVERVIEW

- TABLE 191 TRIVITRON HEALTHCARE: COMPANY OVERVIEW

- TABLE 192 NANOPET PHARMA GMBH: COMPANY OVERVIEW

- TABLE 193 CONTRAST MEDIA MARKET: RESEARCH ASSUMPTIONS

List of Figures

- FIGURE 1 CONTRAST MEDIA MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 MARKET SCENARIO

- FIGURE 3 GLOBAL CONTRAST MEDIA MARKET, 2023-2031

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN CONTRAST MEDIA MARKET, 2020-2025

- FIGURE 5 DISRUPTIONS INFLUENCING GROWTH OF CONTRAST MEDIA MARKET

- FIGURE 6 HIGH-GROWTH SEGMENTS IN CONTRAST MEDIA MARKET, 2025-2031

- FIGURE 7 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN CONTRAST MEDIA MARKET DURING FORECAST PERIOD

- FIGURE 8 CONTRAST MEDIA MARKET DRIVEN BY RISING IMAGING VOLUMES, LOW-DOSE INNOVATIONS, AND EXPANDING ADOPTION ACROSS KEY REGIONS

- FIGURE 9 NORTH AMERICA TO COMMAND LARGEST MARKET SHARE

- FIGURE 10 HOSPITALS, CLINICS, AND AMBULATORY SURGERY CENTERS ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 11 CHINA TO REGISTER HIGHEST GROWTH RATE FROM 2025 TO 2031

- FIGURE 12 CONTRAST AGENT MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 13 CONTRAST MEDIA MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 14 CONTRAST MEDIA MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 15 CONTRAST MEDIA MARKET: ECOSYSTEM ANALYSIS

- FIGURE 16 AVERAGE SELLING PRICE TREND OF CONTRAST MEDIA PRODUCTS, BY REGION, 2026-2024 (USD)

- FIGURE 17 AVERAGE SELLING PRICE OF CONTRAST MEDIA PRODUCTS, BY KEY PLAYER

- FIGURE 18 CONTRAST MEDIA MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 19 CONTRAST MEDIA MARKET: FUNDING SCENARIO, 2019-2023 (USD MILLION)

- FIGURE 20 NUMBER OF DEALS IN CONTRAST MEDIA MARKET, BY KEY PLAYER, 2019-2023

- FIGURE 21 VALUE OF DEALS IN CONTRAST MEDIA MARKET, BY KEY PLAYER, 2019-2023 (USD)

- FIGURE 22 INFLUENCE OF KEY STAKEHOLDERS ON BUYING PROCESS FOR CONTRAST MEDIA MARKET, BY PRODUCT

- FIGURE 23 KEY BUYING CRITERIA FOR END USERS

- FIGURE 24 CONTRAST MEDIA MARKET: UNMET NEED ANALYSIS

- FIGURE 25 PATENT ANALYSIS FOR CONTRAST MEDIA MARKET, JANUARY 2015-DECEMBER 2025

- FIGURE 26 KEY AI USE CASES IN CONTRAST MEDIA ECOSYSTEM

- FIGURE 27 NORTH AMERICA: CONTRAST MEDIA MARKET SNAPSHOT

- FIGURE 28 ASIA PACIFIC: CONTRAST MEDIA MARKET SNAPSHOT

- FIGURE 29 REVENUE ANALYSIS OF KEY PLAYERS IN CONTRAST MEDIA MARKET, 2021-2025 (USD MILLION)

- FIGURE 30 CONTRAST MEDIA MARKET SHARE ANALYSIS OF KEY PLAYERS, 2024

- FIGURE 31 RANKING OF KEY PLAYERS IN CONTRAST MEDIA MARKET (2024)

- FIGURE 32 EV/EBITDA OF TOP PLAYERS (2026)

- FIGURE 33 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF TOP PLAYERS (2026)

- FIGURE 34 CONTRAST MEDIA MARKET: BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 35 CONTRAST MEDIA MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 36 CONTRAST MEDIA MARKET: COMPANY FOOTPRINT

- FIGURE 37 CONTRAST MEDIA MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 38 GE HEALTHCARE: COMPANY SNAPSHOT (2025)

- FIGURE 39 BAYER AG: COMPANY SNAPSHOT (2025)

- FIGURE 40 GUERBET: COMPANY SNAPSHOT (2025)

- FIGURE 41 LANTHEUS HOLDINGS, INC.: COMPANY SNAPSHOT (2025)

- FIGURE 42 J.B. CHEMICALS & PHARMACEUTICALS LIMITED: COMPANY SNAPSHOT (2025)

- FIGURE 43 CONTRAST MEDIA MARKET: RESEARCH DATA

- FIGURE 44 CONTRAST MEDIA MARKET: RESEARCH DESIGN

- FIGURE 45 PRIMARY SOURCES

- FIGURE 46 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 47 BREAKDOWN OF PRIMARY INTERVIEWS: SUPPLY-SIDE AND DEMAND-SIDE PARTICIPANTS

- FIGURE 48 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 49 CONTRAST MEDIA MARKET SIZE ESTIMATION: APPROACH 1 (COMPANY REVENUE ESTIMATION)

- FIGURE 50 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 51 DATA TRIANGULATION

造影劑市場:2026-2032年全球市場預測(依產品類型、影像方法、劑型、給藥途徑、應用及最終用戶分類)

造影劑市場:2026-2032年全球市場預測(依產品類型、影像方法、劑型、給藥途徑、應用及最終用戶分類) 2026年全球磁振造影(MRI)造影劑市場報告

2026年全球磁振造影(MRI)造影劑市場報告 MRI造影劑市場規模及預測(2021-2034年),全球及區域佔有率、趨勢和成長機會分析報告:按類型、給藥途徑、應用、適應症、最終用戶和地區分類

MRI造影劑市場規模及預測(2021-2034年),全球及區域佔有率、趨勢和成長機會分析報告:按類型、給藥途徑、應用、適應症、最終用戶和地區分類 MRI造影劑市場規模、佔有率和趨勢分析報告:按產品、產品類型、應用、最終用途、地區和細分市場預測(2026-2033年)

MRI造影劑市場規模、佔有率和趨勢分析報告:按產品、產品類型、應用、最終用途、地區和細分市場預測(2026-2033年) 診斷放射性藥物和造影劑市場:按放射性藥物、造影劑和地區分類

診斷放射性藥物和造影劑市場:按放射性藥物、造影劑和地區分類 2035年MRI造影劑市場分析與預測:類型、產品、技術、成分、應用、劑型、製程、最終用戶、功能

2035年MRI造影劑市場分析與預測:類型、產品、技術、成分、應用、劑型、製程、最終用戶、功能 造影劑市場報告:按類型、模式、應用、給藥途徑、最終用戶和地區分類(2026-2034 年)

造影劑市場報告:按類型、模式、應用、給藥途徑、最終用戶和地區分類(2026-2034 年) 離子導入設備市場規模、佔有率和成長分析:按產品類型、電源、電流類型、最終用戶和地區分類-2026-2033年產業預測2026年全球钆基造影劑市場報告造影劑市場:依藥物類型、給藥方式、應用、最終用戶和通路分類-2026-2032年全球預測

離子導入設備市場規模、佔有率和成長分析:按產品類型、電源、電流類型、最終用戶和地區分類-2026-2033年產業預測2026年全球钆基造影劑市場報告造影劑市場:依藥物類型、給藥方式、應用、最終用戶和通路分類-2026-2032年全球預測