|

市場調查報告書

商品編碼

2027368

全球非公路用流體管理市場:按安裝類型和地區分類 - 預測至 2032 年Fluid Management Market For Off-highway, by Equipment Type, System Type, Component Type, and Region - Global Forecast to 2032 |

|||||||

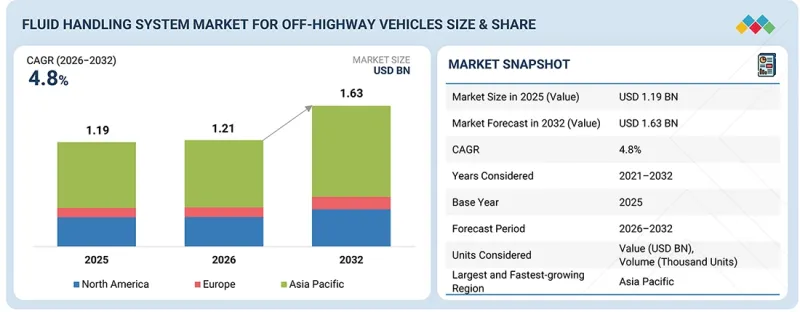

非公路用流體管理市場預計將從 2026 年的 12.1 億美元成長到 2032 年的 16.3 億美元,複合年成長率為 4.8%。

推動這一市場發展的因素是人們對設備運作和可靠性的日益關注。營運商需要高度耐用且不易發生故障的流體系統,以最大限度地減少高運轉率環境下的停機時間。同時,隨著租賃等設備利用模式的擴展,對能夠承受多位業者連續使用的堅固耐用且易於維護的流體處理組件的需求也日益成長。

| 調查範圍 | |

|---|---|

| 調查期 | 2026-2032 |

| 基準年 | 2025 |

| 預測期 | 2026-2032 |

| 目標單元 | 10億美元 |

| 部分 | 依設備類型,依地區 |

| 目標區域 | 亞太地區、北美地區、歐洲 |

原始設備製造商 (OEM) 轉向採購整合系統也推動了這個市場的發展。製造商傾向於選擇完整的流體處理組件而非單一零件,這促進了系統級需求的成長。此外,緊湊型和高壓系統設計的進步正在加速高效能流體管路解決方案的普及,尤其是在空間受限的設備中。同時,日益嚴格的安全性和合規性要求促使人們選擇具有防漏性和高可靠性的流體系統,尤其是在注重環保的場所和危險的工作環境中。

“液壓系統在機器運作中的核心作用決定了其優越性。”

液壓系統憑藉其在實現核心機械功能方面的關鍵作用以及在各類設備中的廣泛應用,成為非公路用液壓管理市場的主要驅動力。其在動力傳輸和運作中的基礎性作用是其主要驅動力。液壓系統對於建築、採礦和農業機械的起重、挖掘、裝載、轉向和煞車等功能至關重要,構成了非公路用機械的支柱,並創造了對流體傳輸組件的穩定需求。高功率密度和高效率優勢鞏固了其市場主導地位。與機械和電氣系統相比,液壓系統提供更強大的動力和更精確的控制,使其成為重型應用的首選解決方案。液壓系統在各種機械類型中的廣泛應用推動了挖土機、裝載機、曳引機、收割機和其他設備的需求。液壓系統的普遍應用確保了其廣泛而穩定的需求基礎。

系統複雜性的不斷提升和性能要求的不斷提高正在推動市場進一步成長。現代設備採用高壓系統、先進的控制機制和精密液壓技術,從而帶動了對高性能軟管、管件、閥門和接頭的需求成長。在高壓和惡劣條件下持續運作會導致液壓元件的嚴重磨損和頻繁更換,進而支撐了強勁的售後市場需求。成本效益和完善的基礎設施也是關鍵因素。與全電動系統相比,液壓系統具備技術成熟、供應鏈完善、成本更低等優點。

“監管壓力和先進工程技術正在推動歐洲對流體系統的需求。”

歐洲非公路用流體管理市場的發展主要受監管壓力、先進設備應用和強大的工業基礎的驅動。嚴格的環境和排放氣體法規是歐洲市場的主要驅動力。有關流體洩漏、排放氣體和設備效率的法規迫使原始設備製造商 (OEM) 採用高性能、低滲透性軟管、先進的密封系統和高效的液壓架構。對設備效率和永續性的日益重視也增加了對先進流體系統的需求。德國、法國和義大利等國的 OEM 將燃油效率、降低能量損失和最佳化液壓性能作為優先事項,這推動了流體處理組件的創新。主要 OEM 和一級供應商的強大實力也支撐了市場成長。歐洲擁有眾多大型建築、農業和工業設備製造商,因此對高品質、技術先進的流體輸送系統有穩定的需求。電動和混合動力設備的日益普及正在加速對溫度控管解決方案的需求。建築和農業機械的電氣化轉型正在推動對冷卻系統、電池溫度控管和專用流體輸送技術的需求。先進的製造和工程能力使得高精度、耐用系統的開發成為可能。歐洲供應商專注於高壓系統、緊湊型設計以及針對複雜機械量身定做的整合解決方案。穩定的替換和售後市場需求也推動了市場的穩定成長。全部區域部署的大量非公路用車輛對軟管、接頭和密封件的維護和更換產生了持續的需求。

非公路車輛流體管理市場的主要參與者包括派克漢尼汾公司(美國)、蓋茲公司(美國)、庫柏標準公司(美國)、住友理工公司(日本)和ADM集團(印度)。這些公司採用多種策略來維持其市場地位。主要策略包括推出新產品、建立合作關係和拓展業務。透過分析這些策略,可以了解每家公司在市場中的地位。製造商致力於透過提供先進且多樣化的非公路用車輛流體管理系統來滿足不斷變化的法規和消費者需求,從而保持其在市場中的戰略地位。

購買本報告的主要好處:

- 本報告提供了非公路生態系統及其細分市場中流體管理市場收入的最準確估算,有助於該市場的市場領導和新參與企業。

- 本報告將幫助相關人員了解競爭格局,更好地定位其業務,並獲得進一步的見解,以製定合適的打入市場策略。

- 此外,本報告可協助相關人員了解市場趨勢,並提供關鍵市場促進因素、限制因素、挑戰和機會的資訊。

本報告深入分析了以下幾點:

- 對關鍵促進因素(建築、採礦和農業領域設備運轉率提高;由於功能改進導致液壓系統日益複雜)、阻礙因素(成本敏感型設備領域價格敏感性高;惡劣的運作環境導致頻繁故障)、機遇(電氣化帶來的溫度控管系統)和挑戰(橡膠和金屬等原料供應鏈波動)的分析。

- 產品開發/創新:深入了解非公路流體管理市場的未來技術、研發活動和新產品發布。

- 市場發展:盈利市場的全面資訊(本報告分析了各地區的非公路用流體管理市場。)

- 市場多元化:提供有關非公路流體管理市場的新產品、未開發市場、近期趨勢和投資的全面資訊。

- 競爭分析:對非公路流體管理市場主要參與者的市場排名、成長策略和服務產品進行詳細評估,包括派克漢尼汾公司(美國)、蓋茲公司(美國)、庫柏標準公司(美國)、住友理工公司(日本)和ADM集團(印度)。

目錄

第1章 詞彙表

第2章執行摘要

第3章:越野車輛:電氣化與定位分析

第4章 市場動態與監理環境

- MNM的主要市場促進因素和阻礙因素

- 帝國汽車公司越野車零件部門的政策影響評估

- 法規結構:印度施工機械排放氣體法規(CEV)第五階段標準

- 法規結構:印度農業機械第五階段排放標準

- SAE印度非公路設備液壓軟管標準

- 印度

- 中國

- 亞太其他地區

- 歐洲

- 北美洲

第6章:FTP產品套件規模分析(依裝置分類)

- 後鏟式裝載機- 套件尺寸

- 液壓挖土機/裝載機 - 套件尺寸

- 平土機機/裝載機 - 套件尺寸

- 履帶式推土機/裝載機 - 套件尺寸

- 農業曳引機 - 套件尺寸

- 堆高機(1-3級)- 套件尺寸

- 堆高機(4-5級)- 套件尺寸

第7章 競爭情勢

- 按設備類型分類的OEM市場佔有率

- 按原始設備製造商分類的建築和採礦機械市場佔有率(2024 年)

- 按原始設備製造商分類的農業曳引機市場佔有率(2024 年)

- 按OEM廠商分類的堆高機市場佔有率(2024年)

- 主要供應商流體傳輸產品對比

第8章 競爭分析

- PARKER HANNIFIN CORP.

- GATES CORPORATION

- COOPER STANDARD

- SUMITOMO RIKO

- JAYSHREE POLYMERS PVT. LTD.

- JK FENNER

- ADM GROUP

- BONY POLYMERS (P) LTD.

- POLYHOSE

- TVH PARTS HOLDING NV

- JAYEM AUTO INDUSTRIES PVT. LTD.

- SEBROS GROUP

- MANULI HYDRAULICS

- DAYCO

- ARTH RUBBERS

- BHATIA PIPE INDUSTRIES

- KINGDAFLEX

- ALFAGOMMA

- BRIDGESTONE

- AR HYDRAULIC

The fluid management market for off-highway is projected to grow from USD 1.21 billion in 2026 to USD 1.63 billion by 2032 at a CAGR of 4.8%. The market is driven by increasing focus on equipment uptime and reliability, as operators are demanding durable and failure-resistant fluid systems to minimize downtime in high-utilization environments. In parallel, growth in rental and leasing equipment models is pushing demand for robust and easy-to-maintain fluid handling components that can withstand continuous usage across multiple operators.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | USD Billion |

| Segments | by Equipment Type, System Type, Component Type, and Region |

| Regions covered | Asia Pacific, North America, Europe |

The market is further supported by OEMs' shift toward integrated system sourcing, where manufacturers are preferring complete fluid handling assemblies over individual components, increasing system-level demand. Additionally, advancements in compact and high-pressure system design are driving the adoption of efficient fluid routing solutions, especially in space-constrained equipment. At the same time, rising safety and compliance requirements are encouraging the use of leak-proof and high-integrity fluid systems, particularly in environmentally sensitive and hazardous operating conditions.

"Core Role in Machine Operations Driving Hydraulic System Dominance"

The hydraulic fluid system segment leads the fluid management market for off-highway due to its critical role in enabling core machine functions and its widespread adoption across equipment types. Fundamental role in power transmission and actuation is the primary driver, as hydraulic systems are essential for functions such as lifting, digging, loading, steering, and braking across construction, mining, and agricultural equipment, making them the backbone of off-highway machinery and driving consistent demand for fluid transfer components. High power density and efficiency advantages are supporting dominance. Hydraulic systems provide superior force output and precise control compared to mechanical or electric alternatives, making them the preferred solution for heavy-duty applications. Extensive use across multiple equipment types is increasing demand for volume across excavators, loaders, tractors, and harvesters. Hydraulic systems are universally integrated, ensuring a broad and stable demand base.

Increasing system complexity and performance requirements are further driving growth. Modern equipment is incorporating higher-pressure systems, advanced control mechanisms, and precision hydraulics, increasing the need for high-performance hoses, tubing, valves, and connectors. High wear and replacement frequency contribute significantly to continuous operation under high pressure and harsh conditions, leading to frequent maintenance and replacement of hydraulic fluid components and supporting strong aftermarket demand. Cost effectiveness and established infrastructure are also key factors. Hydraulic systems benefit from mature technology, well-developed supply chains, and lower cost than fully electric alternatives.

"Regulatory Pressure and Advanced Engineering Driving Fluid System Demand in Europe."

The European fluid management market for off-highway is driven by regulatory pressure, advanced equipment adoption, and strong industrial capabilities. Stringent environmental and emission regulations are a primary market driver across Europe. Regulations related to fluid leakage, emissions, and equipment efficiency are pushing OEMs to adopt high-performance, low-permeability hoses, advanced sealing systems, and efficient hydraulic architectures. High focus on equipment efficiency and sustainability is increasing demand for advanced fluid systems. OEMs in countries such as Germany, France, and Italy are emphasizing fuel efficiency, reduced energy loss, and optimized hydraulic performance, driving innovation in fluid handling components. Strong presence of leading OEMs and Tier 1 suppliers is supporting market growth. Europe hosts major construction, agricultural, and industrial equipment manufacturers, creating consistent demand for high-quality and technologically advanced fluid transfer systems. The rising adoption of electric and hybrid equipment is accelerating demand for thermal management solutions. The transition to electric construction and agricultural machinery is increasing demand for coolant systems, battery thermal management, and specialized fluid-transfer technologies. Advanced manufacturing and engineering capabilities are enabling the development of high-precision and durable systems. European suppliers are focusing on high-pressure systems, compact designs, and integrated solutions tailored to complex machinery. Stable replacement and aftermarket demand are also contributing to steady growth. A large installed base of off-highway vehicles across the region is generating continuous demand for maintenance and replacement of hoses, fittings, and seals.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEM - 50%, Tier 1 - 40%, Tier 2 - 10%

- By Designation: Directors - 30%, Managers - 40%, Others - 30%

- By Country: Asia Pacific - 50%, North America - 20%, Europe - 30%

Major players in the fluid management market for off-highway are Parker Hannifin Corp. (US), Gates Corporation (US), Cooper Standard (US), Sumitomo Riko (Japan), and ADM Group (India). These players have been adopting various strategies to sustain their positions in the market. Major strategies adopted are product launches, deals, and expansions. These strategies have been analyzed to understand the positions of these companies in the market. Manufacturers focus on maintaining their strategic position in the market by offering advanced, various fluid management systems for off-highway vehicles to meet evolving regulatory and consumer demands.

Key Benefits of Buying the Report:

- This report will help market leaders/new entrants in this market with information on the closest approximations of revenue numbers for the fluid management market for the off-highway ecosystem and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies.

- This report will also help stakeholders understand the market's pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (rising equipment utilization in construction, mining, and agriculture, growth in hydraulic system complexity with improved features), restraints (high price sensitivity in cost-driven equipment segments, harsh operating environments leading to frequent failures), opportunities (electrification-driven thermal management systems), and challenges (supply chain volatility in raw materials like rubber and metals)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the fluid management market for off-highway

- Market Development: Comprehensive information about lucrative markets (the report analyzes the fluid management market for off-highway across varied regions)

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the fluid management market for off-highway

- Competitive Assessment: In-depth assessment of market ranking, growth strategies, and service offerings of leading players like Parker Hannifin Corp. (US), Gates Corporation (US), Cooper Standard (US), Sumitomo Riko (Japan), and ADM Group (India) in the fluid management market for off-highway

TABLE OF CONTENTS

1 GLOSSARY

- 1.1 LIST OF ABBREVIATIONS

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS AND EXCLUSIONS

- 1.4 PICTORIAL REPRESENTATION OF SELECTED COMPONENTS UNDER STUDY SCOPE

2 EXECUTIVE SUMMARY

- 2.1 OFF-HIGHWAY VEHICLE GLOBAL & INDIA SALES FORECAST (2024-2030)

- 2.2 OFF-HIGHWAY INDIA VS. REST OF WORLD FTP MARKET FORECAST (2024-2030)

- 2.3 INDIA CONSTRUCTION & MINING EQUIPMENT FTP MARKET, BY PROPULSION (2024 VS. 2030)

- 2.4 INDIA AGRICULTURAL EQUIPMENT AND FORKLIFT FTP MARKET, BY PROPULSION (2024 VS. 2030)

- 2.6 OPPORTUNITIES IN FTP MARKET FOR INDIA CONSTRUCTION & MINING EQUIPMENT

- 2.7 OPPORTUNITIES IN FTP MARKET FOR INDIA AGRICULTURAL EQUIPMENT

- 2.8 OPPORTUNITIES IN FTP MARKET FOR INDIA FORKLIFT

3 OFF-HIGHWAY VEHICLE: ELECTRIFICATION & LOCALIZATION ANALYSIS

- 3.1 INDIA: CONSTRUCTION EQUIPMENT OEMS - ZERO-EMISSION VEHICLE RELATED DEVELOPMENTS AND LOCALIZATION PLANS

- 3.2 INDIA: AGRICULTURE EQUIPMENT OEMS - ZERO-EMISSION VEHICLE RELATED DEVELOPMENTS AND LOCALIZATION PLANS

- 3.3 INDIA: FORKLIFTS OEMS - ZERO-EMISSION VEHICLE RELATED DEVELOPMENTS AND LOCALIZATION PLANS

- 3.4 FLUID TRANSFER PRODUCT SHIFT WITH ELECTRIFICATION FOR FORKLIFT

4 MARKET DYNAMICS & REGULATORY LANDSCAPE

- 4.1 MNM PERSPECTIVES ON KEY MARKET DRIVERS AND CONSTRAINTS

- 4.2 POLICY IMPACT ASSESSMENT ON IMPERIAL AUTO'S OHV COMPONENTS SEGMENT

- 4.3 REGULATORY FRAMEWORK: INDIA CEV STAGE V EMISSION STANDARDS FOR CONSTRUCTION EQUIPMENT

- 4.4 REGULATORY FRAMEWORK: INDIA TREM STAGE V EMISSION STANDARDS FOR AGRICULTURAL EQUIPMENT

- 4.5 SAE INDIA STANDARDS FOR HYDRAULIC HOSES IN OFF-HIGHWAY EQUIPMENT

5 COUNTRY & REGION-WISE OHV SALES AND FTP MARKET ANALYSIS

- 5.1 INDIA

- 5.1.1 INDIAN CONSTRUCTION & MINING EQUIPMENT SALES

- 5.1.2 INDIAN CONSTRUCTION & MINING EQUIPMENT WISE EXPORTS 2024

- 5.1.3 INDIA AGRICULTURAL EQUIPMENT-WISE SALES

- 5.1.4 INDIA AGRICULTURAL TRACTOR & COMBINE HARVESTER EXPORT SALES, 2024

- 5.1.5 INDIA FORKLIFT CLASS-WISE SALES

- 5.1.6 FTP COMPONENTS - INDIA CONSTRUCTION & MINING EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- 5.1.7 FTP COMPONENTS - INDIA AGRICULTURAL EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- 5.1.8 FTP COMPONENTS - INDIA FORKLIFT PRODUCT MIX, 2024 VS. 2030

- 5.2 CHINA

- 5.2.1 CHINA OFF-HIGHWAY EQUIPMENT FTP MARKET, BY EQUIPMENT TYPE AND BY SYSTEM, 2024 VS. 2030

- 5.2.2 FTP COMPONENTS - CHINA CONSTRUCTION & MINING EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- 5.2.3 FTP COMPONENTS - CHINA AGRICULTURAL EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- 5.2.4 FTP COMPONENTS - CHINA FORKLIFT PRODUCT MIX, 2024 VS. 2030

- 5.3 REST OF ASIA PACIFIC

- 5.3.1 REST OF ASIA PACIFIC FTP PRODUCT MARKET FOR OFF-HIGHWAY EQUIPMENT, BY EQUIPMENT CATEGORY, 2024 VS. 2030

- 5.3.2 FTP COMPONENTS - REST OF ASIA PACIFIC CONSTRUCTION & MINING EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- 5.3.3 FTP COMPONENTS - REST OF ASIA PACIFIC AGRICULTURAL EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- 5.3.4 FTP COMPONENTS - REST OF ASIA PACIFIC FORKLIFT PRODUCT MIX 2024 VS. 2030

- 5.4 EUROPE

- 5.4.1 EUROPE CONSTRUCTION & MINING EQUIPMENT SALES - 2024 VS. 2030

- 5.4.2 EUROPE AGRICULTURAL EQUIPMENT-WISE SALES - 2024 VS. 2030

- 5.4.3 EUROPE FORKLIFT WISE SALES - 2024 VS. 2030

- 5.4.4 EUROPE OFF-HIGHWAY EQUIPMENT FTP MARKET , BY EQUIPMENT CATEGORY, 2024 VS. 2030

- 5.4.5 FTP COMPONENTS - EUROPE CONSTRUCTION & MINING EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- 5.4.6 FTP COMPONENTS - EUROPE AGRICULTURAL EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- 5.4.7 FTP COMPONENTS - EUROPE FORKLIFT PRODUCT MIX, 2024 VS. 2030

- 5.5 NORTH AMERICA

- 5.5.1 CONSTRUCTION & MINING EQUIPMENT SALES - NORTH AMERICA

- 5.5.2 AGRICULTURAL EQUIPMENT & FORKLIFT SALES - NORTH AMERICA

- 5.5.3 NORTH AMERICA OFF-HIGHWAY EQUIPMENT FTP MARKET, BY EQUIPMENT CATEGORY, 2024 VS. 2030

- 5.5.4 FTP COMPONENTS - NORTH AMERICA CONSTRUCTION & MINING EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- 5.5.5 FTP COMPONENTS - NORTH AMERICA AGRICULTURAL EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- 5.5.6 FTP COMPONENTS - NORTH AMERICA FORKLIFT PRODUCT MIX, 2024 VS. 2030

6 FTP PRODUCTS KIT SIZE ANALYSIS, BY EQUIPMENT

- 6.1 BACKHOE LOADERS - KIT SIZES

- 6.2 EXCAVATORS LOADERS - KIT SIZES

- 6.3 MOTOR GRADERS LOADERS - KIT SIZES

- 6.4 CRAWLER DOZERS LOADERS - KIT SIZES

- 6.5 AGRICULTURE TRACTORS - KIT SIZERS

- 6.6 FORKLIFTS (CLASS 1-3) - KIT SIZES

- 6.7 FORKLIFTS (CLASS 4-5) - KIT SIZES

7 COMPETITIVE LANDSCAPE

- 7.1 EQUIPMENT TYPE OEM MARKET SHARE

- 7.1.1 CONSTRUCTION & MINING EQUIPMENT OEM-WISE MARKET SHARE (2024)

- 7.1.1.1 INDIA

- 7.1.1.2 GLOBAL

- 7.1.2 AGRICULTURE TRACTOR OEM-WISE MARKET SHARE (2024)

- 7.1.2.1 INDIA

- 7.1.2.2 GLOBAL

- 7.1.3 FORKLIFT OEM-WISE MARKET SHARE (2024)

- 7.1.3.1 INDIA

- 7.1.3.2 GLOBAL

- 7.1.1 CONSTRUCTION & MINING EQUIPMENT OEM-WISE MARKET SHARE (2024)

- 7.2 FLUID TRANSFER PRODUCT COMPARISON BY KEY SUPPLIERS

8 COMPETITOR ANALYSIS

- 8.1 PARKER HANNIFIN CORP.

- 8.2 GATES CORPORATION

- 8.3 COOPER STANDARD

- 8.4 SUMITOMO RIKO

- 8.5 JAYSHREE POLYMERS PVT. LTD.

- 8.6 JK FENNER

- 8.9 ADM GROUP

- 8.8 BONY POLYMERS (P) LTD.

- 8.9 POLYHOSE

- 8.10 TVH PARTS HOLDING NV

- 8.11 JAYEM AUTO INDUSTRIES PVT. LTD.

- 8.12 SEBROS GROUP

- 8.13 MANULI HYDRAULICS

- 8.14 DAYCO

- 8.15 ARTH RUBBERS

- 8.16 BHATIA PIPE INDUSTRIES

- 8.19 KINGDAFLEX

- 8.18 ALFAGOMMA

- 8.19 BRIDGESTONE

- 8.20 AR HYDRAULIC

List of Tables

- TABLE 1 GLOSSARY - LIST OF ABBREVIATIONS

- TABLE 2 GLOSSARY - MARKET DEFINITION

- TABLE 3 GLOSSARY - INCLUSIONS AND EXCLUSIONS

- TABLE 4 INDIA VS. GLOBAL OFF-HIGHWAY VEHICLE SALES, BY EQUIPMENT (UNITS)

- TABLE 5 INDIA DOMESTIC SALES VS. EXPORTS OF OFF-HIGHWAY VEHICLES, BY EQUIPMENT (UNITS)

- TABLE 6 INDIA CONSTRUCTION & MINING EQUIPMENT FTP MARKET, BY EQUIPMENT (INR CRORE)

- TABLE 7 INDIA AGRICULTURAL EQUIPMENT FTP MARKET, BY EQUIPMENT (INR CRORE)

- TABLE 8 REST OF THE WORLD CONSTRUCTION & MINING EQUIPMENT FTP MARKET, BY EQUIPMENT (INR CRORE)

- TABLE 9 REST OF THE WORLD AGRICULTURAL EQUIPMENT FTP MARKET, BY EQUIPMENT (INR CRORE)

- TABLE 10 INDIA FORKLIFT FTP MARKET, BY CLASS (INR CRORE)

- TABLE 11 REST OF THE WORLD FORKLIFT FTP MARKET, BY CLASS (INR CRORE)

- TABLE 12 INDIA CONSTRUCTION & MINING EQUIPMENT SALES, BY PROPULSION (UNITS)

- TABLE 13 INDIA CONSTRUCTION & MINING FTP MARKET VALUE, 2024 VS. 2030 (INR CRORE)

- TABLE 14 INDIA AGRICULTURAL EQUIPMENT SALES, BY PROPULSION (UNITS)

- TABLE 15 INDIA AGRICULTURAL EQUIPMENT FTP MARKET VALUE, BY EQUIPMENT TYPE, 2024 VS. 2030 (INR CRORE)

- TABLE 16 INDIA FORKLIFT SALES, BY PROPULSION (UNITS)

- TABLE 17 INDIA FORKLIFT FTP MARKET VALUE, BY PROPULSION (INR CRORE)

- TABLE 18 OPPORTUNITIES IN FTP MARKET FOR INDIA CONSTRUCTION & MINING EQUIPMENT

- TABLE 19 OPPORTUNITIES IN FTP MARKET FOR INDIA AGRICULTURAL EQUIPMENT

- TABLE 20 OPPORTUNITIES IN FTP MARKET FOR INDIA FORKLIFT

- TABLE 21 INDIA AGRICULTURE EQUIPMENT OEMS - ZERO-EMISSION VEHICLE DEVELOPMENTS (TIMELINE 1)

- TABLE 22 INDIA AGRICULTURE EQUIPMENT OEMS - ZERO-EMISSION VEHICLE DEVELOPMENTS (TIMELINE 2)

- TABLE 23 MNM PERSPECTIVES ON KEY MARKET DRIVERS

- TABLE 24 MNM PERSPECTIVES ON KEY MARKET CONSTRAINTS

- TABLE 25 CEV STAGE V REGULATION OVERVIEW

- TABLE 26 EMISSION STANDARDS: CEV V - CONSTRUCTION EQUIPMENT

- TABLE 27 TREM STAGE V REGULATION OVERVIEW

- TABLE 28 EMISSION STANDARDS: TREM V - TRACTOR AND RELATED EQUIPMENT

- TABLE 29 TREM STAGE V ADDITIONAL STANDARDS

- TABLE 30 SAE INDIA STANDARDS FOR HYDRAULIC HOSES

- TABLE 31 PARKER HANNIFIN - SEGMENT OVERVIEW

- TABLE 32 EATON CORPORATION - SEGMENT OVERVIEW

- TABLE 33 GATES INDUSTRIAL CORPORATION - SEGMENT OVERVIEW

- TABLE 34 CONTINENTAL AG - SEGMENT OVERVIEW

- TABLE 35 DANFOSS - SEGMENT OVERVIEW

- TABLE 36 BOSCH REXROTH - SEGMENT OVERVIEW

- TABLE 37 BRIDGESTONE CORPORATION - SEGMENT OVERVIEW

- TABLE 38 SEMPERIT AG - SEGMENT OVERVIEW

- TABLE 39 MANULI HYDRAULICS - SEGMENT OVERVIEW

List of Figures

- FIGURE 1 PICTORIAL REPRESENTATION OF SELECTED COMPONENTS UNDER STUDY SCOPE

- FIGURE 2 FTP COMPONENTS - INDIA CONSTRUCTION & MINING EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- FIGURE 3 FTP COMPONENTS - INDIA AGRICULTURAL EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- FIGURE 4 FTP COMPONENTS - INDIA FORKLIFT PRODUCT MIX, 2024 VS. 2030

- FIGURE 5 INDIA CONSTRUCTION EQUIPMENT OEMS - ZERO-EMISSION VEHICLE DEVELOPMENTS

- FIGURE 6 INDIA AGRICULTURE EQUIPMENT OEMS - ZERO-EMISSION VEHICLE DEVELOPMENTS

- FIGURE 7 INDIA FORKLIFTS OEMS - ZERO-EMISSION VEHICLE DEVELOPMENTS

- FIGURE 8 FLUID TRANSFER PRODUCT SHIFT WITH ELECTRIFICATION FOR FORKLIFT

- FIGURE 9 POLICY IMPACT ASSESSMENT ON IMPERIAL AUTO'S OHV COMPONENTS SEGMENT

- FIGURE 10 INDIAN CONSTRUCTION & MINING EQUIPMENT SALES

- FIGURE 11 INDIAN CONSTRUCTION & MINING EQUIPMENT-WISE EXPORTS, 2024

- FIGURE 12 INDIA AGRICULTURAL EQUIPMENT-WISE SALES

- FIGURE 13 INDIA AGRICULTURAL TRACTOR & COMBINE HARVESTER EXPORT SALES, 2024

- FIGURE 14 INDIA FORKLIFT CLASS-WISE SALES

- FIGURE 15 INDIA CONSTRUCTION & MINING EQUIPMENT OEM-WISE MARKET SHARE, 2024

- FIGURE 16 INDIA AGRICULTURAL TRACTOR OEM-WISE MARKET SHARE (2024) AND HP-WISE TREND

- FIGURE 17 INDIA CONSTRUCTION & MINING EQUIPMENT OEM-WISE MARKET SHARE (2024) AND CLASS-WISE TREND

- FIGURE 18 CHINA OFF-HIGHWAY EQUIPMENT FTP MARKET, BY EQUIPMENT TYPE AND SYSTEM, 2024 VS. 2030

- FIGURE 19 FTP COMPONENTS - CHINA CONSTRUCTION & MINING EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- FIGURE 20 FTP COMPONENTS - CHINA AGRICULTURAL EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- FIGURE 21 FTP COMPONENTS - CHINA FORKLIFT PRODUCT MIX, 2024 VS. 2030

- FIGURE 22 REST OF ASIA PACIFIC FTP PRODUCT MARKET FOR OFF-HIGHWAY EQUIPMENT, 2024 VS. 2030

- FIGURE 23 FTP COMPONENTS - REST OF APAC CONSTRUCTION & MINING EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- FIGURE 24 FTP COMPONENTS - REST OF APAC AGRICULTURAL EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- FIGURE 25 FTP COMPONENTS - REST OF APAC FORKLIFT PRODUCT MIX, 2024 VS. 2030

- FIGURE 26 EUROPE CONSTRUCTION & MINING EQUIPMENT SALES - 2024 VS. 2030

- FIGURE 27 EUROPE AGRICULTURAL EQUIPMENT-WISE SALES - 2024 VS. 2030

- FIGURE 28 EUROPE FORKLIFT-WISE SALES - 2024 VS. 2030

- FIGURE 29 EUROPE OFF-HIGHWAY EQUIPMENT FTP MARKET, BY EQUIPMENT CATEGORY, 2024 VS. 2030

- FIGURE 30 FTP COMPONENTS - EUROPE CONSTRUCTION & MINING EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- FIGURE 31 FTP COMPONENTS - EUROPE AGRICULTURAL EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- FIGURE 32 FTP COMPONENTS - EUROPE FORKLIFT PRODUCT MIX, 2024 VS. 2030

- FIGURE 33 CONSTRUCTION & MINING EQUIPMENT SALES - NORTH AMERICA

- FIGURE 34 AGRICULTURAL EQUIPMENT & FORKLIFT SALES - NORTH AMERICA

- FIGURE 35 NORTH AMERICA OFF-HIGHWAY EQUIPMENT FTP MARKET, BY EQUIPMENT CATEGORY, 2024 VS. 2030

- FIGURE 36 FTP COMPONENTS - NORTH AMERICA CONSTRUCTION & MINING EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- FIGURE 37 FTP COMPONENTS - NORTH AMERICA AGRICULTURAL EQUIPMENT PRODUCT MIX, 2024 VS. 2030

- FIGURE 38 FTP COMPONENTS - NORTH AMERICA FORKLIFT PRODUCT MIX, 2024 VS. 2030

- FIGURE 39 KIT SIZE PRICE BREAKDOWN FOR BACKHOE LOADERS

- FIGURE 40 KIT SIZE PRICE BREAKDOWN FOR CRAWLER EXCAVATORS

- FIGURE 41 KIT SIZE PRICE BREAKDOWN FOR MOTOR GRADERS

- FIGURE 42 KIT SIZE PRICE BREAKDOWN FOR CRAWLER DOZER

- FIGURE 43 KIT SIZE PRICE BREAKDOWN FOR AGRICULTURE TRACTORS

- FIGURE 44 KIT SIZE PRICE BREAKDOWN FOR FORKLIFTS CLASS 1-3

- FIGURE 45 KIT SIZE PRICE BREAKDOWN FOR FORKLIFTS CLASS 4 & 5

- FIGURE 46 FLUID TRANSFER PRODUCT KEY SUPPLIERS

- FIGURE 47 PARKER HANNIFIN - FINANCIAL ANALYSIS

- FIGURE 48 EATON CORPORATION - FINANCIAL ANALYSIS

- FIGURE 49 GATES INDUSTRIAL CORPORATION - FINANCIAL ANALYSIS

- FIGURE 50 CONTINENTAL AG - FINANCIAL ANALYSIS

- FIGURE 51 GATES INDUSTRIAL CORPORATION - REVENUE CHARTS

- FIGURE 52 CONTINENTAL AG - REVENUE CHARTS

- FIGURE 53 DANFOSS - FINANCIAL ANALYSIS

- FIGURE 54 BOSCH REXROTH - FINANCIAL ANALYSIS

- FIGURE 55 SEMPERIT AG - FINANCIAL ANALYSIS

- FIGURE 56 MANULI HYDRAULICS - FINANCIAL ANALYSIS

- FIGURE 57 POLYHOSE - FINANCIAL ANALYSIS

流體管理和視覺化系統市場:2026-2032年全球市場預測(按產品、交付方式、技術、部署方式、應用和最終用途產業分類)流體管理系統市場:2026-2032年全球市場預測(依產品類型、技術、流體類型、壓力範圍、安裝類型、應用、最終用戶和分銷管道分類)

流體管理和視覺化系統市場:2026-2032年全球市場預測(按產品、交付方式、技術、部署方式、應用和最終用途產業分類)流體管理系統市場:2026-2032年全球市場預測(依產品類型、技術、流體類型、壓力範圍、安裝類型、應用、最終用戶和分銷管道分類) 2026年全球流體管理系統市場報告2026年全球液體抽吸系統市場報告

2026年全球流體管理系統市場報告2026年全球液體抽吸系統市場報告 流體管理系統市場:全球按產品、應用、最終用戶和地區分類 - 預測至 2030 年

流體管理系統市場:全球按產品、應用、最終用戶和地區分類 - 預測至 2030 年 流體管理系統市場(按產品、應用、最終用戶、國家和地區)-2024 年至 2032 年產業分析、市場規模、市場佔有率及預測

流體管理系統市場(按產品、應用、最終用戶、國家和地區)-2024 年至 2032 年產業分析、市場規模、市場佔有率及預測 流體管理系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

流體管理系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 流體管理系統:市場洞察·競爭環境·市場預測 (~2030年)

流體管理系統:市場洞察·競爭環境·市場預測 (~2030年) 輸液管理和視覺化系統市場至2030年的預測:按產品、模式、應用、最終用戶和地區的全球分析

輸液管理和視覺化系統市場至2030年的預測:按產品、模式、應用、最終用戶和地區的全球分析