|

市場調查報告書

商品編碼

2024208

全球汽車攝影機市場:按技術、燃油/電動車應用、車輛類型、視覺範圍、電動車類型、自動駕駛等級和地區分類-預測(至2033年)Automotive Camera Market by Technology (Digital, Infrared, Thermal), ICE and EV Application (ACC, BSD, AFL, IPA, OMS, NVS, & PA), Vehicle Type (PC, LCV, HCV), View (Front, Rear, Surround), EV Type, Level of Autonomy, Region - Global Forecast to 2033 |

||||||

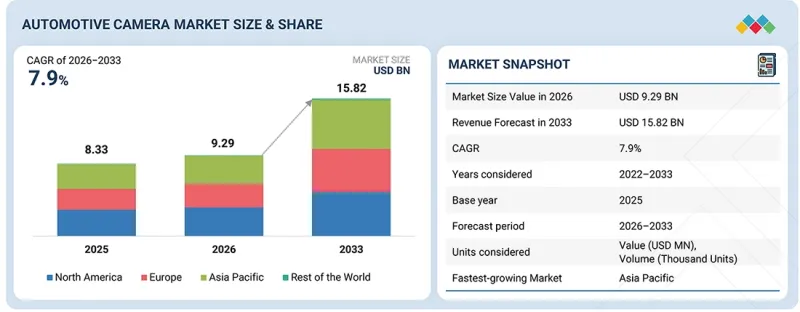

全球汽車攝影機市場預計將從 2026 年的 92.9 億美元成長到 2033 年的 158.2 億美元,複合年成長率為 7.9%。

| 調查範圍 | |

|---|---|

| 調查期 | 2026-2033 |

| 基準年 | 2025 |

| 預測期 | 2026-2033 |

| 單元 | 10億美元 |

| 部分 | 技術、內燃機/電動車應用、車輛類型、可見度、電動車類型、自動駕駛等級、區域 |

| 目標區域 | 亞太地區、歐洲、北美及其他地區 |

由於高階汽車需求不斷成長、消費者對更安全、更聰明的出行解決方案的需求日益增加,以及自動駕駛汽車技術的快速發展,全球市場正在擴張。這一趨勢表明,先進的攝影機系統正被應用於駕駛輔助功能中,例如主動車距控制巡航系統、夜視系統和車道維持系統,從而提升安全性和駕駛體驗。此外,人工智慧/機器學習等最尖端科技與汽車攝影機系統的融合,也正在加速市場成長。

“按視角類型分類,環景顯示攝影機預計將成為汽車攝影機市場中成長最快的細分市場。”

環景顯示攝影機可提供車輛周圍環境的360度全景影像,由於其在提升安全性和停車便利性方面的優勢,正日益普及於所有車型和細分市場。最初,環景系統僅限於高階和豪華車型,但如今,出於成本最佳化和消費者對安全功能日益成長的需求,許多汽車製造商正將環景顯示系統的應用範圍擴展到中階車型,包括掀背車和緊湊型SUV。這些系統整合了安裝在前、後和側視鏡上的多個高解析度攝影機,可產生即時拼接的車輛周圍環境俯視圖。汽車製造商正在新的汽車平臺上推廣多攝影機系統的應用,以提高安全性、滿足監管要求並增強便利性,尤其是在低速行駛和人口密集的城市環境中停車時。羅伯特·博世、大陸集團、法雷奧和麥格納等一級供應商正透過提供完全整合的360°感知系統來推動這一趨勢。這些系統能夠提供拼接式的俯視視圖,並支援自動停車和物件偵測等進階功能。因此,這些系統已成為現代ADAS系統的核心組件。隨著OEM廠商的持續整合和技術的進步,環景顯示攝影系統預計將在預測期內呈現最高的成長率。

“盲點偵測預計將成為車載攝影機的主要應用。”

由於在安靜駕駛環境下對安全性的需求日益成長,盲點監測(BSD)系統在內燃機(ICE)和電動乘用車的應用越來越廣泛。 BSD是中檔至豪華車型中最常見的ADAS(高級駕駛輔助系統)功能之一。該系統利用多個攝影機和感測器(通常每輛車配備兩個,豪華車型可達三到四個),並且能夠直接增加攝影機安裝數量,使其目前佔據了市場主導地位。隨著都市化進程的加速和大都會圈交通堵塞的加劇,視野受限和變換車道操作帶來的風險日益增加,加速了對BSD系統的需求。基於攝影機的ADAS功能主要採用安裝在側視鏡或後保險桿上的廣角後視攝影機,以覆蓋相鄰車道和車輛的盲點。此外,全球汽車製造商(OEM)正在朝著感測器融合的方向發展,即將車載攝影機、雷達和360°環景顯示系統結合,並與車道偏離警示系統和自動泊車等功能進行整合。因此,盲點偵測 (BSD) 的效用正從單一功能擴展到高階駕駛輔助系統 (ADAS) 的核心感知層。跨細分市場應用、每輛車攝影機數量的增加、強力的監管推動、原始設備製造商 (OEM) 的持續標準化以及在廣泛的 ADAS 架構中發揮的關鍵作用,預計在整個預測期內,盲點檢測仍將是汽車攝影機最大的應用領域。

本報告對全球汽車攝影機市場進行了深入分析,深入探討了關鍵促進因素和限制因素、產品開發和創新以及競爭格局。

目錄

第1章:引言

第2章執行摘要

第3章 主要發現

- 汽車攝影機市場對企業而言極具吸引力的機會

- 汽車攝影機市場(OE-ICE):按ICE應用分類

- 汽車攝影機市場(OE-ICE):按車輛類型分類

- 汽車攝影機市場(OE-ICE):依技術分類

- 電動汽車攝影機市場(OE):按電動汽車類型分類

- 汽車攝影機市場:依視角類型分類

- 電動汽車攝影機市場(OE):按電動汽車應用分類

- 汽車攝影機市場(OE):按自動駕駛等級分類

- 汽車攝影機市場:按地區分類

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求和閒置頻段

- 相互關聯的市場與跨產業機遇

- 一級/二級/三級公司的策略性舉措

第5章 產業趨勢

- 宏觀經濟展望

- GDP趨勢與預測

- 全球汽車和運輸業的趨勢

- 供應鏈分析

- 原物料供應商

- 零件製造商/技術供應商

- 雲端服務供應商

- OEM

- 最終用戶

- 汽車攝影機組件供應商列表

- 影像感測器供應商列表

- 相機模組供應商列表

- 一級ADAS供應商名單

- 軟體供應商列表

- 半導體供應商列表

- 定價分析

- 平均售價趨勢:依車型分類(2023-2025 年)

- 平均售價:按地區分類(2025 年)

- 貿易分析

- 進口方案(HS編碼900211)

- 出口方案(HS編碼900211)

- 重大會議和活動(2026-2027)

- 影響客戶業務的趨勢/干擾因素

- 投資和資金籌措場景

- 案例研究分析

- 電裝驅動器狀態監視器

- MOMENTA 的 MPILOT 自動停車和高速公路駕駛系統

- 瑞薩電子 R-CAR 軟體開發工具包

- 東京大學的迴避支持系統

- NIDEC ELESYS 感測器融合系統

- 生態系分析

第6章:技術進步、人工智慧的影響、專利與創新

- 主要技術

- 汽車平臺與電子電氣架構

- 集中式運算平台

- 區域建築

- 軟體定義車輛

- 高速網路

- 互補技術

- 雷達、LiDAR、超音波感測器

- ADAS ECU

- 技術/產品藍圖

- 短期:基礎建設和初步商業化(2026-2027 年)

- 中期計畫:擴大規模並最佳化效能(2028-2030 年)

- 長期願景:完全自主與智慧生態系(2030-2033)

- 人工智慧/生成式人工智慧的影響

- 專利分析

- 歐盟自由貿易協定對汽車和運輸業的影響

- 伊朗-以色列戰爭對汽車和運輸業的影響

第7章 監理環境與永續性舉措

- 當地法規和合規性

- 監管機構、政府機構和其他組織

- 業界標準

- 對永續性的承諾

- 碳排放和環境友善應用

- 監管政策對永續性努力的影響

- 認證、標籤檢視、環境標準

第8章:顧客趨勢與購買行為

- 決策流程

- 採購過程中的關鍵相關利益者及其評估標準

- 招募障礙和內部挑戰

- 終端用戶產業未滿足的需求

- 市場盈利

第9章 汽車攝影機市場(OE-ICE):依應用領域分類

- 主動車距控制巡航系統

- 主動車距控制巡航系統+前方碰撞警報

- 主動車距控制巡航系統+前方碰撞警報+交通標誌識別

- 盲點偵測

- 盲點偵測 + 車道維持輔助 + 車道偏離預警

- 自適應照明系統

- 智慧停車輔助

- 駕駛員監控系統

- 夜視系統

- 停車協助

- 重要見解

第10章 汽車攝影機市場(OE-ICE):依車輛類型分類

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 重要見解

第11章 汽車攝影機市場(OE-ICE):依技術分類

- 數位的

- 紅外線的

- 熱

第12章 汽車攝影機市場(OE-ICE):依視角類型分類

- 正面圖

- 後視圖

- 環景顯示

- 重要見解

第13章:電動車和混合動力汽車的攝影機市場(OE):按應用領域分類

- 主動車距控制巡航系統(ACC)

- 主動車距控制巡航系統+前方碰撞警報

- 主動車距控制巡航系統(ACC)+ 前方碰撞警報(FCW)+ 交通標誌辨識(TSR)

- 盲點偵測

- 盲點偵測 (BSD) + 車道維持輔助 (LKA) + 車道偏離警示 (LDW)

- 自適應照明系統(ALS)

- 智慧泊車輔助系統(IPA)

- 駕駛員監控系統(DMS)

- 夜視系統(NVS)

- 停車協助

- 重要見解

第14章:電動車與混合動力汽車(OE)相機市場:依電動車類型分類

- 電池電動車(BEV)

- 插電式混合動力車(PHEV)

- 燃料電池電動車(FCEV)

- 重要見解

第15章 汽車攝影機市場(ICE):依自動駕駛等級分類

- 0級/1級(L0/L1)

- 二級(L2)

- 3級(L3)

- 重要見解

第16章:汽車攝影機售後市場需求

- 正規企業的汽車攝影機售後市場

- 非正規企業的汽車攝影機售後市場

- 汽車攝影機售後市場需求的區域趨勢

- 區域層面各類相機售後市場價格分析

第17章 汽車攝影機(OE-ICE)市場:依地區分類

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 其他亞太地區

- 歐洲

- 德國

- 法國

- 西班牙

- 俄羅斯

- 英國

- 土耳其

- 其他歐洲國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他地區

- 巴西

- 伊朗

- 其他

第18章 競爭格局

- 主要參與企業的策略/優勢(2022-2025)

- 市佔率分析(2025 年)

- 收入分析(2021-2025)

- 企業評估與財務指標

- 品牌/產品對比

- 企業評估矩陣:主要企業(2025 年)

- 公司評估矩陣:Start-Ups/中小企業(2025 年)

- 競爭格局

第19章:公司簡介

- 主要企業

- ROBERT BOSCH GMBH

- MAGNA INTERNATIONAL INC.

- VALEO

- ZF FRIEDRICHSHAFEN AG

- DENSO CORPORATION

- FICOSA INTERNACIONAL SA

- APTIV

- AUMOVIO SE

- FORVIA

- RICOH

- KYOCERA CORPORATION

- 其他公司

- MOTHERSON

- AMBARELLA INTERNATIONAL LP

- OMNIVISION

- HITACHI ASTEMO, LTD.

- GENTEX CORPORATION

- SAMSUNG ELECTRO-MECHANICS

- TELEDYNE FLIR LLC

- HYUNDAI MOBIS

- MCNEX CO., LTD.

- STONKAM CO., LTD.

- BRIGADE ELECTRONICS GROUP PLC

- HPB OPTOELECTRONICS CO., LTD.

- SONY SEMICONDUCTOR SOLUTIONS CORPORATION

- LG ELECTRONICS

- GARMIN LTD.

第20章:調查方法

第21章附錄

The global automotive camera market size is projected to grow from USD 9.29 billion in 2026 to USD 15.82 billion by 2033, at a CAGR of 7.9%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | Automotive Camera Market by Technology, ICE and EV Application, Vehicle Type, View, EV Type, Level of Autonomy, Region - Global Forecast to 2033 |

| Regions covered | Asia Pacific, Europe, North America, and the Rest of the World |

The market is expanding globally due to the growing demand for premium vehicles, consumer preference for safer and smarter mobility solutions, and rapid advancements in autonomous vehicles. This trend highlights the use of advanced camera systems for driver assistance features such as adaptive cruise control, night vision system, and lane keep assist to enhance safety and driving experience. Additionally, the integration of cutting-edge technologies, such as AI/ML integration in automotive camera systems, accelerates market growth.

"Surround-view camera to be fastest-growing segment in automotive camera market, by view type"

Surround-view cameras offer a 360-degree view around the vehicle, which is increasingly gaining traction across vehicle segments due to their enhanced safety and parking convenience benefits. Initially limited to premium and luxury vehicles, currently many OEMs have expanded the availability of surround-view systems to mid-segment vehicles, including hatchbacks and compact SUVs, driven by cost optimization and rising consumer demand for safety features. These systems integrate multiple high-resolution cameras mounted at the front, rear, and side mirrors, generating a real-time stitched top-down view of the vehicle's surroundings. Automotive OEMs are increasingly installing multi-camera systems into new vehicle platforms to enhance safety, meet regulatory requirements, and improve user convenience, particularly for low-speed maneuvers and parking in dense urban environments. Major Tier 1 suppliers such as Robert Bosch, Continental, Valeo, and Magna are supporting this trend by delivering fully integrated 360° perception systems that provide a stitched top-down view and enable advanced functions like automated parking and object detection, making them a core part of modern ADAS stacks. Hence, with increasing OEM integration and technological advancements, surround-view camera systems are projected to grow at the fastest rate during the forecast period.

"Blind spot detection to be largest application of automotive cameras"

Blind spot detection (BSD) systems are witnessing increasing adoption in ICE and electric passenger vehicles, driven by the need for enhanced safety in silent vehicle operation. BSD is one of the most common ADAS features in mid- to premium-range cars. It utilizes multiple sets of cameras and sensors (usually 2 and can go up to 3-4 units per vehicle in higher-end cars), directly increasing the camera count, leading to its dominant share in the current scenario. With rising urbanization and increasing traffic congestion in metropolitan areas, the risk associated with limited visibility and lane-changing maneuvers is growing, thereby accelerating the demand for BSD systems. The integration of camera-based ADAS features, as they are primarily used in wide-angle rear-facing cameras mounted on side mirrors or rear bumpers, enables coverage of adjacent lanes and vehicle blind zones. Further, global OEMs are shifting toward sensor fusion, i.e., a combination of automotive cameras along with radars plus a 360° surround-view system, and integration with functions like lane assist and automated parking. This is expanding the BSD's utility beyond a single feature into a core perception ADAS layer. With its cross-segment penetration, higher camera-per-vehicle requirement, strong regulatory push, increasing OEM standardization, and integral role in broader ADAS architectures, blind spot detection is expected to remain the largest automotive camera application throughout the forecast period.

"Asia Pacific to be second-largest automotive camera market"

The Asia Pacific is the second-largest automotive camera market, driven by high vehicle production, rapid ADAS adoption in some economy-to-mid-level vehicles, and evolving safety regulations. China leads the market in the region due to its massive production base and increasing penetration of camera-based ADAS across both mass (A-C segment) and premium vehicles, where features such as rear-view cameras, lane departure warning, and 360-degree surround view are becoming standard. India is emerging as a high-growth market, supported by rising safety awareness, regulatory push, and increasing demand for affordable ADAS features in passenger vehicles. Meanwhile, Japan and South Korea are witnessing strong demand due to advanced safety standards and higher adoption of Level 2 and Level 2+ autonomous features, particularly in premium and electric vehicles. Growth is also notable in the commercial vehicle segment, where fleet operators are adopting cameras for blind spot detection, driver monitoring, and rear visibility to improve safety and efficiency.

The growth in the region is primarily driven by increasing safety regulations, electrification, and OEM-led technology integration. Automakers such as Hyundai Motor Company, Kia Corporation, Toyota Motor Corporation, and Honda Motor Co., Ltd. are aggressively integrating multi-camera systems across vehicle segments, focusing on applications such as ADAS, driver monitoring systems, and parking assistance. In addition, the shift toward EVs, especially in China, Japan, and South Korea, is accelerating camera adoption due to advanced electronic architectures. With strong policy support and rising investments in cost-effective camera modules, the demand for automotive cameras in the Asia Pacific is expected to remain high, with India and China acting as key growth engines due to volume expansion and increasing feature penetration.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in the automotive camera market. The break-up of the primaries is as follows:

- By Respondent Type: OEMs - 25%, Tier I -55%, and Tier II - 20%,

- By Designation: C-Level Director - 30%, Director-Level- 60%, and Others - 10%

- By Region: North America - 30%, Europe - 30%, and Asia Pacific - 40%,

The automotive camera market comprises major players such as Robert Bosch GmbH (Germany), Continental AG (Germany), Valeo (France), ZF Friedrichshafen AG (Germany), Denso Corporation (Japan), and Ficosa Internacional SA (Spain).

Research Coverage:

This research report categorizes the automotive camera market by technology (digital, infrared, thermal), EV application (adaptive cruise control, forward collision warning, traffic sign recognition, blind spot detection, lane keep assist, adaptive lighting system, intelligent park assist, driver monitoring system, night vision system, parking assist), vehicle type (passenger car, light commercial vehicle, heavy commercial vehicle), view type (front view, surround view, rear view), EV type (battery electric vehicle, plug-in hybrid electric vehicle, fuel cell electric vehicle), level of autonomy (Level 0/1, Level 2, Level 3), and region (Asia Pacific, Europe, North America, Rest of the World).

The report provides detailed information regarding key factors influencing market growth, including drivers, restraints, opportunities, and challenges. It also includes an in-depth competitive analysis of major industry players, covering their company profiles, product and service offerings, key strategies, partnerships, agreements, product launches, mergers & acquisitions, and recent developments. Additionally, the report covers analysis of SMEs/startups, the supplier ecosystem, and key developments across the automotive camera market.

Key Benefits of Buying the Report:

- The report will help market leaders and new entrants with information on the closest approximations of revenue numbers for the overall automotive camera market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain insights to position their businesses effectively and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market dynamics and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (shift toward camera-based perception systems replacing traditional sensors in entry- and mid-level vehicles, along with strong regulatory push for automotive safety features such as ADAS and rear-view cameras), restraints (high validation and calibration complexity of multi-camera systems and performance sensitivity under adverse environmental conditions such as low light and weather), opportunities (rapid adoption of camera-only or camera-dominant perception architectures in ADAS and growing demand for in-cabin sensing applications such as driver monitoring systems), and challenges (increasing bandwidth and data processing limitations with rising camera count and ensuring real-world performance reliability across diverse driving conditions)

- Product Development/Innovation: Insights into upcoming technologies, R&D activities, and advancements in camera systems, including AI-based image processing, high-resolution imaging, thermal sensing, and sensor fusion technologies

- Market Development: Comprehensive information about key markets, with analysis across major regions such as the Asia Pacific, Europe, North America, and the Rest of the World

- Market Diversification: Detailed insights into untapped markets, emerging applications, and recent investments in the automotive camera ecosystem

- Competitive Assessment: In-depth analysis of market share, growth strategies, and product offerings of leading players such as Robert Bosch GmbH, Continental AG, Valeo, ZF Friedrichshafen AG, and Denso Corporation

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SNAPSHOT

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN AUTOMOTIVE CAMERA MARKET

- 2.4 HIGH-GROWTH SEGMENTS IN AUTOMOTIVE CAMERA MARKET

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE CAMERA MARKET

- 3.2 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY ICE APPLICATION

- 3.3 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VEHICLE TYPE

- 3.4 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY TECHNOLOGY

- 3.5 ELECTRIC VEHICLE CAMERA MARKET (OE), BY EV TYPE

- 3.6 AUTOMOTIVE CAMERA MARKET, BY VIEW TYPE

- 3.7 ELECTRIC VEHICLE CAMERA MARKET (OE), BY EV APPLICATION

- 3.8 AUTOMOTIVE CAMERA MARKET (OE), BY LEVEL OF AUTONOMY

- 3.9 AUTOMOTIVE CAMERA MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Shift toward camera-based perception systems in entry and mid-level vehicles

- 4.2.1.2 Regulation-led "camera-per- vehicle inflation"

- 4.2.2 RESTRAINTS

- 4.2.2.1 Validation and calibration complexity for multi-camera systems

- 4.2.2.2 Susceptibility to environmental conditions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rapid adoption of camera-only or camera-dominant perception architectures in ADAS

- 4.2.3.2 Rise of in-cabin sensing applications

- 4.2.4 CHALLENGES

- 4.2.4.1 Bandwidth and data processing limitations with increasing camera count

- 4.2.4.2 Ensuring performance reliability in real-world environments

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 CROSS-INDUSTRY STRATEGIC THEMES

- 4.5.1.1 Shift from camera module -> perception system

- 4.5.1.2 Multi-camera architecture expansion

- 4.5.1.3 OEM co-development & platform lock-ins

- 4.5.1.4 Regional manufacturing & China /Emerging market focus

- 4.5.1.5 Transition to software-defined vehicles (SDVs)

- 4.5.1 CROSS-INDUSTRY STRATEGIC THEMES

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC OUTLOOK

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.2 SUPPLY CHAIN ANALYSIS

- 5.2.1 RAW MATERIAL SUPPLIERS

- 5.2.2 COMPONENT MANUFACTURERS/TECHNOLOGY PROVIDERS

- 5.2.3 CLOUD SERVICE PROVIDERS

- 5.2.4 OEMS

- 5.2.5 END USERS

- 5.3 SUPPLIER LIST OF AUTOMOTIVE CAMERA COMPONENTS

- 5.3.1 LIST OF IMAGE SENSOR SUPPLIERS

- 5.3.2 LIST OF CAMERA MODULE SUPPLIERS

- 5.3.3 LIST OF TIER 1 ADAS SUPPLIERS

- 5.3.4 LIST OF SOFTWARE SUPPLIERS

- 5.3.5 LIST OF SEMICONDUCTOR SUPPLIERS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2023-2025

- 5.4.2 AVERAGE SELLING PRICE, BY REGION, 2025

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 900211)

- 5.5.2 EXPORT SCENARIO (HS CODE 900211)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 DRIVER STATUS MONITOR BY DENSO

- 5.9.2 MPILOT AUTONOMOUS PARKING AND HIGHWAY DRIVING SYSTEM BY MOMENTA

- 5.9.3 R-CAR SOFTWARE DEVELOPMENT KIT BY RENESAS

- 5.9.4 EVASIVE MANEUVER ASSIST SYSTEM BY UNIVERSITY OF TOKYO

- 5.10 SENSOR FUSION SYSTEM BY NIDEC ELESYS

- 5.11 ECOSYSTEM ANALYSIS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 VEHICLE PLATFORM AND E/E ARCHITECTURE

- 6.1.2 CENTRALIZED COMPUTE PLATFORM

- 6.1.3 ZONAL ARCHITECTURE

- 6.1.4 SOFTWARE-DEFINED VEHICLE

- 6.1.5 HIGH-SPEED NETWORK

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 RADAR, LIDAR, AND ULTRASONIC SENSOR

- 6.2.2 ADAS ECU

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2026-2027): FOUNDATION AND EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2028-2030): SCALING AND PERFORMANCE OPTIMIZATION

- 6.3.3 LONG-TERM (2030-2033): FULL AUTONOMY AND INTELLIGENT ECOSYSTEMS

- 6.4 IMPACT OF AI/GENERATIVE AI

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF EU-FTA TRADE DEAL ON AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 6.7 IMPACT OF ISRAEL-IRAN WAR ON AUTOMOTIVE & TRANSPORTATION INDUSTRY

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS

- 7.2.2 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.2.2.1 European Union

- 7.2.2.2 US

- 7.2.2.3 China

- 7.2.2.4 India

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.2.3.1 Type I ecolabels

- 7.2.3.2 Product carbon footprint

- 7.2.3.3 Ecodesign and material standards

- 7.2.3.4 Hazardous substance restrictions

- 7.2.3.5 Circular economy and recycling certification

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.1.1 KEY BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 ADAPTIVE CRUISE CONTROL

- 9.2.1 ENHANCES OBJECT CLASSIFICATION, LANE CONTEXT, AND PERFORMANCE IN COMPLEX SCENARIOS

- 9.3 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING

- 9.3.1 INTEGRATION OF ADAPTIVE CRUISE CONTROL AND FORWARD COLLISION WARNING IN MID-RANGE VEHICLES TO DRIVE MARKET

- 9.4 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION

- 9.4.1 RELIANT ON FRONT-VIEW CAMERAS AND ON-BOARD IMAGE PROCESSING

- 9.5 BLIND SPOT DETECTION

- 9.5.1 STANDARDIZATION OF ADAS ACROSS MID AND HIGH SEGMENTS IN EMERGING MARKETS TO DRIVE GROWTH

- 9.6 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING

- 9.6.1 EFFECTIVE FOR HIGHWAY AND LONG-DISTANCE DRIVING

- 9.7 ADAPTIVE LIGHTING SYSTEM

- 9.7.1 EVOLVING TOWARD CAMERA-INTEGRATED MATRIX LED AND PIXEL LIGHTING

- 9.8 INTELLIGENT PARKING ASSIST

- 9.8.1 EMERGING AS PREMIUM CONVENIENCE FEATURE

- 9.9 DRIVER MONITORING SYSTEM

- 9.9.1 RISING CONCERNS ABOUT DRIVER FATIGUE AND DISTRACTION TO DRIVE GROWTH

- 9.10 NIGHT VISION SYSTEM

- 9.10.1 IMPROVED INFRARED AND THERMAL IMAGING TECHNOLOGIES TO DRIVE GROWTH

- 9.11 PARKING ASSIST

- 9.11.1 TRANSITION FROM COMPLIANCE-DRIVEN FEATURE TO MULTI-CAMERA, SOFTWARE-LED SYSTEM TO DRIVE GROWTH

- 9.12 KEY PRIMARY INSIGHTS

10 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VEHICLE TYPE

- 10.1 INTRODUCTION

- 10.2 PASSENGER CAR

- 10.2.1 GOVERNMENT REGULATIONS FOR MAKING ADAS MANDATORY IN PASSENGER CARS TO DRIVE GROWTH

- 10.3 LIGHT COMMERCIAL VEHICLE

- 10.3.1 INCREASING EMPHASIS ON LOGISTICS EFFICIENCY AND SAFETY TO DRIVE MARKET

- 10.4 HEAVY COMMERCIAL VEHICLE

- 10.4.1 GROWING NEED FOR IMPROVED DRIVER VISIBILITY TO DRIVE GROWTH

- 10.5 KEY PRIMARY INSIGHTS

11 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 DIGITAL

- 11.2.1 INCREASING ADOPTION OF ADAS TO DRIVE GROWTH

- 11.3 INFRARED

- 11.3.1 TRANSITION FROM OPTIONAL SAFETY FEATURE TO REGULATORY-MANDATED STANDARD TO DRIVE GROWTH

- 11.4 THERMAL

- 11.4.1 ADVANCEMENTS IN THERMAL IMAGING TECHNOLOGY FOR OBJECT DETECTION CAPABILITY ENHANCEMENT TO DRIVE GROWTH

12 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VIEW TYPE

- 12.1 INTRODUCTION

- 12.2 FRONT VIEW

- 12.2.1 NEED FOR COMPLIANCE WITH NCAP STANDARDS TO DRIVE GROWTH

- 12.3 REAR VIEW

- 12.3.1 SHIFT TOWARD HIGHER DYNAMIC RANGE TO DRIVE GROWTH

- 12.4 SURROUND VIEW

- 12.4.1 DEMAND FOR ENHANCED PARKING AND MANEUVERING ASSISTANCE IN CONGESTED URBAN AREAS TO DRIVE GROWTH

- 12.5 KEY PRIMARY INSIGHTS

13 ELECTRIC AND HYBRID VEHICLE (OE) CAMERA MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 ADAPTIVE CRUISE CONTROL (ACC)

- 13.2.1 SURGING ADOPTION OF ADAS IN MID-SEGMENT VEHICLES TO DRIVE GROWTH

- 13.3 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING

- 13.3.1 ENABLES AUTOMATIC SPEED, DISTANCE MANAGEMENT, AND TIMELY ALERTS IN CRITICAL SITUATIONS

- 13.4 ADAPTIVE CRUISE CONTROL (ACC) + FORWARD COLLISION WARNING (FCW) + TRAFFIC SIGN RECOGNITION (TSR)

- 13.4.1 REGULATORY BODIES PUSHING FOR ENHANCED ROAD SAFETY STANDARDS TO DRIVE GROWTH

- 13.5 BLIND SPOT DETECTION

- 13.5.1 GROWING COMPLEXITY OF URBAN DRIVING ENVIRONMENTS AND EV-SPECIFIC SAFETY CHALLENGES TO DRIVE GROWTH

- 13.6 BLIND SPOT DETECTION (BSD) + LANE KEEP ASSIST (LKA) + LANE DEPARTURE WARNING (LDW)

- 13.6.1 GROWING DEMAND FOR BUNDLED SAFETY FEATURES IN ASIA PACIFIC AND EUROPE TO DRIVE GROWTH

- 13.7 ADAPTIVE LIGHTING SYSTEM (ALS)

- 13.7.1 SHIFT FROM PREMIUM TO CRITICAL SAFETY FEATURE TO DRIVE GROWTH

- 13.8 INTELLIGENT PARKING ASSIST (IPA)

- 13.8.1 RISING ADOPTION IN PREMIUM ELECTRIC AND PLUG-IN HYBRID VEHICLES TO DRIVE GROWTH

- 13.9 DRIVER MONITORING SYSTEM (DMS)

- 13.9.1 GROWING ADOPTION IN DEVELOPED ECONOMIES TO DRIVE GROWTH

- 13.10 NIGHT VISION SYSTEM (NVS)

- 13.10.1 DEVELOPMENT OF SEMI AND FULLY AUTONOMOUS CARS NECESSITATING ADVANCED NIGHT VISION CAPABILITIES TO DRIVE MARKET

- 13.11 PARKING ASSIST

- 13.11.1 GROWING DEMAND FOR SAFETY FEATURES DURING VEHICLE REVERSALS TO PREVENT COLLISIONS TO DRIVE GROWTH

- 13.12 KEY PRIMARY INSIGHTS

14 ELECTRIC AND HYBRID VEHICLE (OE) CAMERA MARKET, BY EV TYPE

- 14.1 INTRODUCTION

- 14.2 BATTERY ELECTRIC VEHICLE (BEV)

- 14.2.1 DEPLOYMENT OF PEDESTRIAN AND CYCLIST DETECTION SYSTEMS TO DRIVE GROWTH

- 14.3 PLUG-IN HYBRID ELECTRIC VEHICLE (PHEV)

- 14.3.1 CONSUMER PREFERENCE FOR ADVANCED SAFETY TECHNOLOGIES TO DRIVE GROWTH

- 14.4 FUEL CELL ELECTRIC VEHICLE (FCEV)

- 14.4.1 INTEGRATION OF ADAPTIVE CRUISE CONTROL AND LANE KEEP ASSISTANCE TO DRIVE GROWTH

- 14.5 KEY PRIMARY INSIGHTS

15 AUTOMOTIVE CAMERA MARKET (ICE), BY LEVEL OF AUTONOMY

- 15.1 INTRODUCTION

- 15.2 LEVEL 0/LEVEL 1 (L0/L1)

- 15.2.1 WIDELY DEPLOYED ACROSS ENTRY AND MID-SEGMENT VEHICLES

- 15.3 LEVEL 2 (L2)

- 15.3.1 HIGH DEMAND FOR ADVANCED DRIVER ASSISTANCE IN PREMIUM VEHICLE SEGMENT TO DRIVE MARKET

- 15.4 LEVEL 3 (L3)

- 15.4.1 OEM PUSH FOR HIGHER LEVELS OF AUTONOMOUS VEHICLES TO DRIVE MARKET

- 15.5 KEY PRIMARY INSIGHTS

16 AUTOMOTIVE CAMERA AFTERMARKET DEMAND

- 16.1 INTRODUCTION

- 16.2 AUTOMOTIVE CAMERA AFTERMARKET FOR ORGANIZED PLAYERS

- 16.3 AUTOMOTIVE CAMERA AFTERMARKET FOR UNORGANIZED PLAYERS

- 16.4 REGIONAL TRENDS FOR AUTOMOTIVE CAMERA AFTERMARKET DEMAND

- 16.5 AFTERMARKET PRICING ANALYSIS FOR DIFFERENT TYPES OF CAMERAS AT REGIONAL LEVEL

17 AUTOMOTIVE CAMERA (OE-ICE) MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 ASIA PACIFIC

- 17.2.1 CHINA

- 17.2.1.1 Push toward commercialization of autonomous vehicles to drive market

- 17.2.2 INDIA

- 17.2.2.1 Rising safety awareness and regulatory push to drive market

- 17.2.3 JAPAN

- 17.2.3.1 Mandated safety features and innovation to drive market

- 17.2.4 SOUTH KOREA

- 17.2.4.1 Rising investment in autonomous driving solutions to drive market

- 17.2.5 THAILAND

- 17.2.5.1 Increasing vehicle manufacturing and exports to drive market

- 17.2.6 REST OF ASIA PACIFIC

- 17.2.1 CHINA

- 17.3 EUROPE

- 17.3.1 GERMANY

- 17.3.1.1 Advancements in automotive camera technology to drive market

- 17.3.2 FRANCE

- 17.3.2.1 Stringent government policies aimed at enhancing road safety to drive market

- 17.3.3 SPAIN

- 17.3.3.1 Initiatives for advanced automotive systems to drive market

- 17.3.4 RUSSIA

- 17.3.4.1 Government regulations mandating advanced safety systems to drive market

- 17.3.5 UK

- 17.3.5.1 Government's commitment to autonomy and safety to drive market

- 17.3.6 TURKEY

- 17.3.6.1 Surging adoption of driver assistance functions to drive market

- 17.3.7 REST OF EUROPE

- 17.3.1 GERMANY

- 17.4 NORTH AMERICA

- 17.4.1 US

- 17.4.1.1 Major automakers equipping premium vehicles with automotive cameras to drive market

- 17.4.2 CANADA

- 17.4.2.1 Growth of connected and autonomous vehicles to drive market

- 17.4.3 MEXICO

- 17.4.3.1 Emergence as key manufacturing hub for automakers and vehicle parts to drive market

- 17.4.1 US

- 17.5 REST OF THE WORLD (ROW)

- 17.5.1 BRAZIL

- 17.5.1.1 Government encouraging adoption of camera-enabled ADAS to drive market

- 17.5.2 IRAN

- 17.5.2.1 Consumer demand for safety features in vehicles to drive market

- 17.5.3 OTHERS

- 17.5.1 BRAZIL

18 COMPETITIVE LANDSCAPE

- 18.1 INTRODUCTION

- 18.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 18.3 MARKET SHARE ANALYSIS, 2025

- 18.4 REVENUE ANALYSIS, 2021-2025

- 18.5 COMPANY VALUATION AND FINANCIAL METRICS

- 18.6 BRAND/PRODUCT COMPARISON

- 18.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 18.7.1 STARS

- 18.7.2 EMERGING LEADERS

- 18.7.3 PERVASIVE PLAYERS

- 18.7.4 PARTICIPANTS

- 18.7.5 COMPANY FOOTPRINT

- 18.7.5.1 Company footprint

- 18.7.5.2 Region footprint

- 18.7.5.3 View type footprint

- 18.7.5.4 Level of autonomy footprint

- 18.7.5.5 Technology footprint

- 18.7.5.6 Vehicle type footprint

- 18.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 18.8.1 PROGRESSIVE COMPANIES

- 18.8.2 RESPONSIVE COMPANIES

- 18.8.3 DYNAMIC COMPANIES

- 18.8.4 STARTING BLOCKS

- 18.8.5 COMPETITIVE BENCHMARKING

- 18.8.5.1 List of start-ups/SMEs

- 18.8.5.2 Competitive benchmarking of start-ups/SMEs

- 18.9 COMPETITIVE SCENARIO

- 18.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 18.9.2 DEALS

- 18.9.3 EXPANSIONS

- 18.9.4 OTHERS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 ROBERT BOSCH GMBH

- 19.1.1.1 Business overview

- 19.1.1.2 Products offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches/developments

- 19.1.1.3.2 Deals

- 19.1.1.3.3 Others

- 19.1.1.4 MnM view

- 19.1.1.4.1 Key strengths

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses and competitive threats

- 19.1.2 MAGNA INTERNATIONAL INC.

- 19.1.2.1 Business overview

- 19.1.2.2 Products offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product launches/developments

- 19.1.2.3.2 Deals

- 19.1.2.3.3 Expansions

- 19.1.2.3.4 Others

- 19.1.2.4 MnM view

- 19.1.2.4.1 Key strengths

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses and competitive threats

- 19.1.3 VALEO

- 19.1.3.1 Business overview

- 19.1.3.2 Products offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Product launches/developments

- 19.1.3.3.2 Deals

- 19.1.3.3.3 Expansions

- 19.1.3.3.4 Others

- 19.1.3.4 MnM view

- 19.1.3.4.1 Key strengths

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses and competitive threats

- 19.1.4 ZF FRIEDRICHSHAFEN AG

- 19.1.4.1 Business overview

- 19.1.4.2 Products offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Product launches/developments

- 19.1.4.3.2 Deals

- 19.1.4.3.3 Expansions

- 19.1.4.3.4 Others

- 19.1.4.4 MnM view

- 19.1.4.4.1 Key strengths

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weaknesses and competitive threats

- 19.1.5 DENSO CORPORATION

- 19.1.5.1 Business overview

- 19.1.5.2 Products offered

- 19.1.5.3 Recent developments

- 19.1.5.3.1 Product launches/developments

- 19.1.5.3.2 Deals

- 19.1.5.3.3 Expansions

- 19.1.5.3.4 Others

- 19.1.5.4 MnM view

- 19.1.5.4.1 Key strengths

- 19.1.5.4.2 Strategic choices

- 19.1.5.4.3 Weaknesses and competitive threats

- 19.1.6 FICOSA INTERNACIONAL SA

- 19.1.6.1 Business overview

- 19.1.6.2 Products offered

- 19.1.6.3 Recent developments

- 19.1.6.3.1 Product launches/developments

- 19.1.6.3.2 Deals

- 19.1.6.3.3 Expansions

- 19.1.6.3.4 Others

- 19.1.7 APTIV

- 19.1.7.1 Business overview

- 19.1.7.2 Products offered

- 19.1.7.3 Recent developments

- 19.1.7.3.1 Product launches/developments

- 19.1.7.3.2 Deals

- 19.1.7.3.3 Expansions

- 19.1.7.3.4 Others

- 19.1.8 AUMOVIO SE

- 19.1.8.1 Business overview

- 19.1.8.2 Products offered

- 19.1.8.3 Recent developments

- 19.1.8.3.1 Product launches/developments

- 19.1.8.3.2 Deals

- 19.1.8.3.3 Expansions

- 19.1.9 FORVIA

- 19.1.9.1 Business overview

- 19.1.9.2 Products offered

- 19.1.9.3 Recent developments

- 19.1.9.3.1 Product launches/developments

- 19.1.9.3.2 Deals

- 19.1.9.3.3 Expansions

- 19.1.9.3.4 Others

- 19.1.10 RICOH

- 19.1.10.1 Business overview

- 19.1.10.2 Products offered

- 19.1.11 KYOCERA CORPORATION

- 19.1.11.1 Business overview

- 19.1.11.2 Products offered

- 19.1.11.3 Recent developments

- 19.1.11.3.1 Product launches/developments

- 19.1.11.3.2 Expansions

- 19.1.11.3.3 Others

- 19.1.1 ROBERT BOSCH GMBH

- 19.2 OTHER PLAYERS

- 19.2.1 MOTHERSON

- 19.2.2 AMBARELLA INTERNATIONAL LP

- 19.2.3 OMNIVISION

- 19.2.4 HITACHI ASTEMO, LTD.

- 19.2.5 GENTEX CORPORATION

- 19.2.6 SAMSUNG ELECTRO-MECHANICS

- 19.2.7 TELEDYNE FLIR LLC

- 19.2.8 HYUNDAI MOBIS

- 19.2.9 MCNEX CO., LTD.

- 19.2.10 STONKAM CO., LTD.

- 19.2.11 BRIGADE ELECTRONICS GROUP PLC

- 19.2.12 H.P.B. OPTOELECTRONICS CO., LTD.

- 19.2.13 SONY SEMICONDUCTOR SOLUTIONS CORPORATION

- 19.2.14 LG ELECTRONICS

- 19.2.15 GARMIN LTD.

20 RESEARCH METHODOLOGY

- 20.1 RESEARCH DATA

- 20.1.1 SECONDARY DATA

- 20.1.1.1 List of secondary sources

- 20.1.1.2 Key data from secondary sources

- 20.1.2 PRIMARY DATA

- 20.1.2.1 Breakdown of primaries

- 20.1.2.2 Primary participants

- 20.1.2.3 Objectives of primary research

- 20.1.2.4 Sampling techniques and data collection methods

- 20.1.1 SECONDARY DATA

- 20.2 MARKET SIZE ESTIMATION

- 20.2.1 BOTTOM-UP APPROACH

- 20.2.2 TOP-DOWN APPROACH

- 20.3 DATA TRIANGULATION

- 20.4 RESEARCH ASSUMPTIONS AND RISK ASSESSMENT

- 20.5 RESEARCH LIMITATIONS

21 APPENDIX

- 21.1 INSIGHTS FROM INDUSTRY EXPERTS

- 21.2 DISCUSSION GUIDE

- 21.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.4 CUSTOMIZATION OPTIONS

- 21.4.1 GLOBAL AUTOMOTIVE CAMERA MARKET, BY APPLICATION AND VEHICLE TYPE (ICE)

- 21.4.2 ELECTRIC & HYBRID VEHICLE CAMERA MARKET, BY APPLICATION AND ELECTRIC VEHICLE TYPE

- 21.4.3 COMPANY INFORMATION:

- 21.4.3.1 Profiling of additional market players (up to 5)

- 21.5 RELATED REPORTS

- 21.6 AUTHOR DETAILS

List of Tables

- TABLE 1 AUTOMOTIVE CAMERA MARKET DEFINITION, BY TECHNOLOGY

- TABLE 2 AUTOMOTIVE CAMERA MARKET DEFINITION, BY ICE AND ELECTRIC VEHICLE APPLICATION

- TABLE 3 AUTOMOTIVE CAMERA MARKET DEFINITION: BY ICE VEHICLE TYPE

- TABLE 4 AUTOMOTIVE CAMERA MARKET DEFINITION, BY VIEW TYPE

- TABLE 5 AUTOMOTIVE CAMERA MARKET DEFINITION, BY ELECTRIC VEHICLE TYPE

- TABLE 6 AUTOMOTIVE CAMERA MARKET DEFINITION, BY LEVEL OF AUTONOMY

- TABLE 7 INCLUSIONS AND EXCLUSIONS

- TABLE 8 CURRENCY EXCHANGE RATES, 2022-2025

- TABLE 9 BEST-SELLING ADAS-EQUIPPED CARS IN US, 2025

- TABLE 10 IMPACT ANALYSIS OF MARKET DYNAMICS

- TABLE 11 IMAGE SENSOR SUPPLIERS FOR TIER 1 COMPANIES

- TABLE 12 IMAGE SENSOR SUPPLIERS FOR TIER 2 COMPANIES

- TABLE 13 IMAGE SENSOR SUPPLIERS FOR TIER 3 COMPANIES

- TABLE 14 CAMERA MODULE SUPPLIERS

- TABLE 15 TIER 1 ADAS SUPPLIERS

- TABLE 16 SOFTWARE SUPPLIERS

- TABLE 17 SEMICONDUCTOR SUPPLIERS

- TABLE 18 ASIA PACIFIC: AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2023-2025 (USD)

- TABLE 19 EUROPE: AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2023-2025 (USD)

- TABLE 20 NORTH AMERICA: AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2023-2025 (USD)

- TABLE 21 GLOBAL: AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2023-2025 (USD)

- TABLE 22 AVERAGE SELLING PRICE TREND, BY REGION, 2025 (USD)

- TABLE 23 IMPORT DATA FOR HS CODE 900211-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 24 EXPORT DATA FOR HS CODE 900211-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 25 KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 26 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 27 PATENT ANALYSIS, AUGUST 2022-FEBRUARY 2026

- TABLE 28 DIRECT IMPACT EU-FTA TRADE DEAL ON AUTOMOTIVE CAMERA MARKET

- TABLE 29 DIRECT IMPACT OF ISRAEL-IRAN WAR ON AUTOMOTIVE CAMERA MARKET

- TABLE 30 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 31 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 32 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 33 INDUSTRY STANDARDS

- TABLE 34 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY VEHICLE TYPE (%)

- TABLE 35 KEY BUYING CRITERIA, BY VEHICLE TYPE

- TABLE 36 UNMET NEEDS OF END-USE INDUSTRIES

- TABLE 37 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 38 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 39 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 40 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 41 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 42 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 43 AUTOMOTIVE CAMERA INTEGRATION BY APPLICATION AND AUTONOMY LEVEL

- TABLE 44 OEM MODELS WITH ADAPTIVE CRUISE CONTROL, BY CAMERA SUPPLIER

- TABLE 45 ADAPTIVE CRUISE CONTROL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 46 ADAPTIVE CRUISE CONTROL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 47 ADAPTIVE CRUISE CONTROL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 48 ADAPTIVE CRUISE CONTROL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 49 ADAPTIVE CRUISE CONTROL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 50 ADAPTIVE CRUISE CONTROL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 51 OEM MODELS WITH ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING, BY CAMERA SUPPLIER

- TABLE 52 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 53 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 54 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 55 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 56 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 57 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 58 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 59 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 60 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 61 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 62 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 63 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 64 OEM MODELS WITH BLIND SPOT DETECTION, BY CAMERA SUPPLIER

- TABLE 65 BLIND SPOT DETECTION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 66 BLIND SPOT DETECTION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 67 BLIND SPOT DETECTION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 68 BLIND SPOT DETECTION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 69 BLIND SPOT DETECTION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 70 BLIND SPOT DETECTION: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 71 OEM MODELS WITH BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING, BY CAMERA SUPPLIER

- TABLE 72 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 73 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 74 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 75 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 76 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 77 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 78 OEM MODELS WITH ADAPTIVE LIGHTING SYSTEM, BY CAMERA SUPPLIER

- TABLE 79 ADAPTIVE LIGHTING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025(THOUSAND UNITS)

- TABLE 80 ADAPTIVE LIGHTING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 81 ADAPTIVE LIGHTING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 82 ADAPTIVE LIGHTING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 83 ADAPTIVE LIGHTING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 84 ADAPTIVE LIGHTING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 85 OEM MODELS WITH INTELLIGENT PARKING ASSIST, BY CAMERA SUPPLIER

- TABLE 86 INTELLIGENT PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 87 INTELLIGENT PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 88 INTELLIGENT PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 89 INTELLIGENT PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 90 INTELLIGENT PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 91 INTELLIGENT PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 92 OEM MODELS WITH DRIVER MONITORING SYSTEM, BY CAMERA SUPPLIER

- TABLE 93 DRIVER MONITORING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 94 DRIVER MONITORING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 95 DRIVER MONITORING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 96 DRIVER MONITORING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 97 DRIVER MONITORING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 98 DRIVER MONITORING SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 99 OEM MODELS WITH NIGHT VISION SYSTEM, BY CAMERA SUPPLIER

- TABLE 100 NIGHT VISION SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 101 NIGHT VISION SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 102 NIGHT VISION SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 103 NIGHT VISION SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 104 NIGHT VISION SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 105 NIGHT VISION SYSTEM: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 106 OEM MODELS WITH PARKING ASSIST, BY CAMERA SUPPLIER

- TABLE 107 PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 108 PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 109 PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 110 PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 111 PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 112 PARKING ASSIST: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 113 AUTOMOTIVE CAMERA MARKET, BY VEHICLE TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 114 AUTOMOTIVE CAMERA MARKET, BY VEHICLE TYPE, 2026-2029 (THOUSAND UNITS)

- TABLE 115 AUTOMOTIVE CAMERA MARKET, BY VEHICLE TYPE, 2030-2033 (THOUSAND UNITS)

- TABLE 116 AUTOMOTIVE CAMERA MARKET, BY VEHICLE TYPE, 2022-2025 (USD MILLION)

- TABLE 117 AUTOMOTIVE CAMERA MARKET, BY VEHICLE TYPE, 2026-2029 (USD MILLION)

- TABLE 118 AUTOMOTIVE CAMERA MARKET, BY VEHICLE TYPE, 2030-2033 (USD MILLION)

- TABLE 119 PASSENGER CAR: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 120 PASSENGER CAR: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 121 PASSENGER CARS AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 122 PASSENGER CAR: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 123 PASSENGER CAR: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 124 PASSENGER CAR: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 125 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 126 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 127 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 128 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 129 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 130 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 131 HEAVY COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 132 HEAVY COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 133 HEAVY COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 134 HEAVY COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 135 HEAVY COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 136 HEAVY COMMERCIAL VEHICLE: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 137 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY TECHNOLOGY, 2022-2025 (THOUSAND UNITS)

- TABLE 138 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY TECHNOLOGY, 2026-2029 (THOUSAND UNITS)

- TABLE 139 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY TECHNOLOGY, 2030-2033 (THOUSAND UNITS)

- TABLE 140 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 141 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY TECHNOLOGY, 2026-2029 (USD MILLION)

- TABLE 142 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY TECHNOLOGY, 2030-2033 (USD MILLION)

- TABLE 143 DIGITAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 144 DIGITAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 145 DIGITAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 146 DIGITAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 147 DIGITAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 148 DIGITAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 149 INFRARED: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 150 INFRARED: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 151 INFRARED: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 152 INFRARED: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 153 INFRARED: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 154 INFRARED: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 155 THERMAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 156 THERMAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 157 THERMAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 158 THERMAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 159 THERMAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 160 THERMAL: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 161 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VIEW TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 162 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VIEW TYPE, 2026-2029 (THOUSAND UNITS)

- TABLE 163 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VIEW TYPE, 2030-2033 (THOUSAND UNITS)

- TABLE 164 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VIEW TYPE, 2022-2025 (USD MILLION)

- TABLE 165 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VIEW TYPE, 2026-2029 (USD MILLION)

- TABLE 166 AUTOMOTIVE CAMERA MARKET (OE-ICE), BY VIEW TYPE, 2030-2033 (USD MILLION)

- TABLE 167 FRONT-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 168 FRONT-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 169 FRONT-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 170 FRONT-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 171 FRONT-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 172 FRONT-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 173 REAR-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 174 REAR-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 175 REAR-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 176 REAR-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 177 REAR-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 178 REAR-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 179 SURROUND-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 180 SURROUND-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 181 SURROUND-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 182 SURROUND-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 183 SURROUND-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 184 SURROUND-VIEW AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 185 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 186 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 187 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 188 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 189 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 190 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 191 OEM MODELS WITH ADAPTIVE CRUISE CONTROL, BY CAMERA SUPPLIER

- TABLE 192 ADAPTIVE CRUISE CONTROL: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 193 ADAPTIVE CRUISE CONTROL: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 194 ADAPTIVE CRUISE CONTROL: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 195 ADAPTIVE CRUISE CONTROL: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 196 ADAPTIVE CRUISE CONTROL: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 197 ADAPTIVE CRUISE CONTROL: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 198 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 199 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 200 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 201 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 202 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 203 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 204 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: ELECTRIC AND HYBRID VEHICLE AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 205 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 206 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 207 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 208 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 209 ADAPTIVE CRUISE CONTROL + FORWARD COLLISION WARNING + TRAFFIC SIGN RECOGNITION: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 210 OEM MODELS WITH BLIND SPOT DETECTION, BY CAMERA SUPPLIER

- TABLE 211 BLIND SPOT DETECTION: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 212 BLIND SPOT DETECTION: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 213 BLIND SPOT DETECTION: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 214 BLIND SPOT DETECTION: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 215 BLIND SPOT DETECTION ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 216 BLIND SPOT DETECTION: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 217 OEM MODELS WITH BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING, BY CAMERA SUPPLIER

- TABLE 218 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 219 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 220 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 221 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 222 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 223 BLIND SPOT DETECTION + LANE KEEP ASSIST + LANE DEPARTURE WARNING: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 224 ADAPTIVE LIGHTING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 225 ADAPTIVE LIGHTING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 226 ADAPTIVE LIGHTING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 227 ADAPTIVE LIGHTING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 228 ADAPTIVE LIGHTING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 229 ADAPTIVE LIGHTING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 230 OEM MODELS WITH INTELLIGENT PARKING ASSIST, BY CAMERA SUPPLIER

- TABLE 231 INTELLIGENT PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 232 INTELLIGENT PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 233 INTELLIGENT PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 234 INTELLIGENT PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 235 INTELLIGENT PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 236 INTELLIGENT PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 237 DRIVER MONITORING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 238 DRIVER MONITORING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 239 DRIVER MONITORING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 240 DRIVER MONITORING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 241 DRIVER MONITORING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 242 DRIVER MONITORING SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 243 OEM ELECTRIC MODELS WITH NIGHT VISION SYSTEM, BY CAMERA SUPPLIER

- TABLE 244 NIGHT VISION SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 245 NIGHT VISION SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 246 NIGHT VISION SYSTEM ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 247 NIGHT VISION SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 248 NIGHT VISION SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 249 NIGHT VISION SYSTEM: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 250 PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 251 PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 252 PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 253 PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 254 PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 255 PARKING ASSIST: ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 256 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY EV TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 257 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY EV TYPE, 2026-2029 (THOUSAND UNITS)

- TABLE 258 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY EV TYPE, 2030-2033 (THOUSAND UNITS)

- TABLE 259 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY EV TYPE, 2022-2025 (USD MILLION)

- TABLE 260 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY EV TYPE, 2026-2029 (USD MILLION)

- TABLE 261 ELECTRIC AND HYBRID VEHICLE CAMERA MARKET, BY EV TYPE, 2030-2033 (USD MILLION)

- TABLE 262 BATTERY ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 263 BATTERY ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 264 BATTERY ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 265 BATTERY ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 266 BATTERY ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 267 BATTERY ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 268 PLUG-IN HYBRID ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 269 PLUG-IN HYBRID ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 270 PLUG-IN HYBRID ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 271 PLUG-IN HYBRID ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 272 PLUG-IN HYBRID ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 273 PLUG-IN HYBRID ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 274 FUEL CELL ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 275 FUEL CELL ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 276 FUEL CELL ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 277 FUEL CELL ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 278 FUEL CELL ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 279 FUEL CELL ELECTRIC VEHICLE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 280 AUTOMOTIVE CAMERA MARKET (ICE), BY LEVEL OF AUTONOMY, 2022-2025 (THOUSAND UNITS)

- TABLE 281 AUTOMOTIVE CAMERA MARKET (ICE), BY LEVEL OF AUTONOMY, 2026-2029 (THOUSAND UNITS)

- TABLE 282 AUTOMOTIVE CAMERA MARKET (ICE), BY LEVEL OF AUTONOMY, 2030-2033 (THOUSAND UNITS)

- TABLE 283 AUTOMOTIVE CAMERA MARKET (ICE), BY LEVEL OF AUTONOMY, 2022-2025 (USD MILLION)

- TABLE 284 AUTOMOTIVE CAMERA MARKET (ICE), BY LEVEL OF AUTONOMY, 2026-2029 (USD MILLION)

- TABLE 285 AUTOMOTIVE CAMERA MARKET (ICE), BY LEVEL OF AUTONOMY, 2030-2033 (USD MILLION)

- TABLE 286 LEVEL 0/LEVEL 1: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 287 LEVEL 0/LEVEL 1: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 288 LEVEL 0/LEVEL 1: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 289 LEVEL 0/LEVEL 1: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 290 LEVEL 0/LEVEL 1: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 291 LEVEL 0/LEVEL 1: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 292 LEVEL 2: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 293 LEVEL 2: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 294 LEVEL 2: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 295 LEVEL 2: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 296 LEVEL 2: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 297 LEVEL 2: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 298 LEVEL 3: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 299 LEVEL 3: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 300 LEVEL 3: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 301 LEVEL 3: AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 302 LEVEL 3: AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 303 LEVEL 3: AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 304 AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 305 AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (THOUSAND UNITS)

- TABLE 306 AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (THOUSAND UNITS)

- TABLE 307 AUTOMOTIVE CAMERA MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 308 AUTOMOTIVE CAMERA MARKET, BY REGION, 2026-2029 (USD MILLION)

- TABLE 309 AUTOMOTIVE CAMERA MARKET, BY REGION, 2030-2033 (USD MILLION)

- TABLE 310 ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 311 ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2026-2029 (THOUSAND UNITS)

- TABLE 312 ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2030-2033 (THOUSAND UNITS)

- TABLE 313 ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 314 ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2026-2029 (USD MILLION)

- TABLE 315 ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2030-2033 (USD MILLION)

- TABLE 316 CHINA: L3 AND L4 TESTING LICENSES BY OEMS

- TABLE 317 CHINA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 318 CHINA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 319 CHINA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 320 CHINA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 321 CHINA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 322 CHINA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 323 INDIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 324 INDIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 325 INDIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 326 INDIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 327 INDIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 328 INDIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 329 JAPAN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 330 JAPAN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 331 JAPAN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 332 JAPAN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 333 JAPAN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 334 JAPAN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 335 SOUTH KOREA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 336 SOUTH KOREA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 337 SOUTH KOREA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 338 SOUTH KOREA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 339 SOUTH KOREA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 340 SOUTH KOREA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 341 THAILAND: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 342 THAILAND: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 343 THAILAND: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 344 THAILAND: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 345 THAILAND: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 346 THAILAND: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 347 REST OF ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 348 REST OF ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 349 REST OF ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 350 REST OF ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 351 REST OF ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 352 REST OF ASIA PACIFIC: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 353 EUROPE: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 354 EUROPE: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2026-2029 (THOUSAND UNITS)

- TABLE 355 EUROPE: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2030-2033 (THOUSAND UNITS)

- TABLE 356 EUROPE: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 357 EUROPE: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2026-2029 (USD MILLION)

- TABLE 358 EUROPE: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2030-2033 (USD MILLION)

- TABLE 359 GERMANY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 360 GERMANY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 361 GERMANY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 362 GERMANY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 363 GERMANY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 364 GERMANY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 365 FRANCE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 366 FRANCE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 367 FRANCE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 368 FRANCE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 369 FRANCE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 370 FRANCE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 371 SPAIN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 372 SPAIN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 373 SPAIN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 374 SPAIN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 375 SPAIN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 376 SPAIN: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 377 RUSSIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 378 RUSSIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 379 RUSSIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 380 RUSSIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 381 RUSSIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 382 RUSSIA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 383 UK: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 384 UK: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 385 UK: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 386 UK: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 387 UK: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 388 UK: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 389 TURKEY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 390 TURKEY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 391 TURKEY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 392 TURKEY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 393 TURKEY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 394 TURKEY: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 395 REST OF EUROPE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 396 REST OF EUROPE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 397 REST OF EUROPE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 398 REST OF EUROPE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 399 REST OF EUROPE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 400 REST OF EUROPE: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 401 NORTH AMERICA: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 402 NORTH AMERICA: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2026-2029 (THOUSAND UNITS)

- TABLE 403 NORTH AMERICA: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2030-2033 (THOUSAND UNITS)

- TABLE 404 NORTH AMERICA: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 405 NORTH AMERICA: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2026-2029 (USD MILLION)

- TABLE 406 NORTH AMERICA: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2030-2033 (USD MILLION)

- TABLE 407 US: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 408 US: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 409 US: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 410 US: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 411 US: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 412 US: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 413 CANADA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 414 CANADA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 415 CANADA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 416 CANADA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 417 CANADA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 418 CANADA: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 419 MEXICO: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 420 MEXICO: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (THOUSAND UNITS)

- TABLE 421 MEXICO: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (THOUSAND UNITS)

- TABLE 422 MEXICO: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 423 MEXICO: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2026-2029 (USD MILLION)

- TABLE 424 MEXICO: AUTOMOTIVE CAMERA MARKET, BY APPLICATION, 2030-2033 (USD MILLION)

- TABLE 425 REST OF THE WORLD: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 426 REST OF THE WORLD: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2026-2029 (THOUSAND UNITS)

- TABLE 427 REST OF THE WORLD: AUTOMOTIVE CAMERA MARKET, BY COUNTRY, 2030-2033 (THOUSAND UNITS)