|

市場調查報告書

商品編碼

2021042

全球多層薄膜市場報告:按類型、應用、組件和地區分類 - 預測(至 2031 年)Mulch Films Market Report by Type (Clear/Transparent, Black Mulch, Colored Mulch, Photo-selective Mulch, Degradable Mulch), Application (Agricultural and Horticulture), Element (LLDPE, LDPE, HDPE, EVA, PLA, PHA), and Region - Global Forecast to 2031 |

||||||

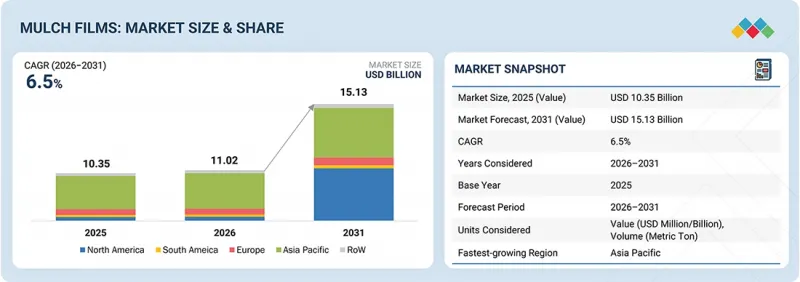

2026 年全球多膜市場規模預計為 110.2 億美元,預計到 2031 年將達到 151.3 億美元,複合年成長率為 6.5%。

| 調查範圍 | |

|---|---|

| 調查期 | 2026-2031 |

| 基準年 | 2025 |

| 預測期 | 2026-2031 |

| 單元 | 美元,噸 |

| 部分 | 類型、成分、用途、地區 |

| 目標區域 | 北美、歐洲、亞太地區、南美及其他地區 |

由於精密農業、保護性耕作和先進土壤管理技術的日益普及,市場正經歷顯著變化。智慧農業技術的引入,例如基於感測器的灌溉系統、自動地膜鋪設機和氣候響應型薄膜,進一步提升了產品的功能性。產業主要企業正積極研發高性能可生物分解和紫外線穩定型薄膜,以改善土壤健康、最大限度地減少對環境的不利影響,並促進環境友善農業的發展。地膜產業的最新產品研發表明,產品耐久性、保水性和針對特定作物的功能性日益受到重視,這預示著產品成長的上升趨勢。

地膜產業的機會與變革主要與農業向永續農業和資源高效型耕作方式的快速轉型密切相關。隨著人們對更高作物產量、更優質農產品和更高效用水的需求日益成長,地膜被視為對農民和生產者而言具有巨大的商業性潛力。農民使用地膜有助於提高用水效率、控制雜草、調節土壤溫度並減少除草劑的使用,從而提高農業,特別是園藝和高價值作物的盈利。該行業的變化被認為源於更嚴格的塑膠使用環境法規、環保替代品的出現以及向永續材料的過渡。這些因素正在為該行業帶來重大變化,並給整個行業的成長帶來挑戰。

人工智慧驅動的養分最佳化:人工智慧和機器學習在地膜市場也扮演著重要角色。這使得企業能夠在生產地膜之前了解土壤、天氣和作物狀況。因此,他們可以準確地確定地膜的厚度、顏色和類型。例如,黑色地膜可用於雜草控制,而透明地膜可用於土壤增溫。人工智慧還可以用於了解地膜的耐久性和分解時間,從而避免缺陷和成本。農民也能從數據工具中受益,了解何時以及使用何種類型的地膜。因此,他們可以製定更好的計劃並減少浪費,從而提高農作物產量。

先進的複合技術:地膜產業的主要關注點之一是材料研發。各公司不僅致力於研發傳統材料,也著力開發環保材料。然而,由於聚乙烯薄膜具有高強度和成本績效,因此仍被廣泛應用。另一方面,隨著環境保護法規的日益嚴格,對可生物分解薄膜的需求也不斷成長。此外,該行業的新產品具有優異的紫外線防護性能,能夠承受強烈的陽光照射。其中一些產品能夠有效調節土壤溫度,從而促進作物生長。另一些產品則具有卓越的保水性,從而減少用水量。部分產品在安裝和使用過程中也具有良好的抗撕裂性。該行業還提供專為作物設計的薄膜,旨在滿足水果、蔬菜和花卉等作物的需求。

精準施肥系統:地膜鋪設技術也透過合理應用現代技術而不斷改進。現代技術使農民能夠有效利用自動化地膜鋪設機,從而實現地膜的均勻鋪設,節省時間和人力。土壤濕度感測器有助於獲取灌溉方面的準確資訊。透過物聯網技術,可以獲得田間目前狀況的精確資訊。利用GPS的農場管理技術有助於規劃地膜鋪設時的合理間距,避免鋪設錯誤造成資源浪費。合理使用地膜有助於提高土地利用效率和產量。

本報告對全球多層薄膜市場進行了深入分析,深入探討了關鍵促進因素和限制因素、產品開發和創新以及競爭格局。

目錄

第1章:引言

第2章執行摘要

第3章 主要發現

- 多膜市場對企業而言極具吸引力的機會

- 多膜市場:按類型和地區分類

- 多膜市場:按組件分類

- 多膜市場:按組件分類

- 多膜市場:按應用領域分類

- 多膜市場:按國家分類

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求和閒置頻段

- 多膜市場中尚未滿足的需求

- 閒置頻段的機遇

- 相互關聯的市場與跨產業機遇

- 互聯市場

- 跨部門機會

- 新的經營模式和生態系統的變化

- 新經營模式

- 生態系變化

- 一級/二級/三級公司的策略性舉措

第5章 產業趨勢

- 波特五力分析

- 總體經濟指標

- 人口成長和耕地短缺

- 全球農業用水趨勢對地膜市場的影響

- 價值鏈分析

- 原物料採購

- 聚合物加工和配方

- 薄膜製造(擠出成型)

- 產品客製化和包裝

- 分銷和銷售網路

- 最終用途、售後支援和廢棄物管理

- 生態系分析

- 需求端

- 供應端

- 定價分析

- 主要企業平均售價:按類型

- 平均售價趨勢:按地區分類

- 平均售價趨勢:依應用領域分類

- 貿易分析

- HS編碼392010的進口方案

- HS編碼392010的出口場景

- 重大會議和活動(2024-2026)

- 影響客戶業務的趨勢/干擾因素

- 案例研究分析

- BASF公司利用人工智慧技術進行現場分析,提升了可生物分解地膜的效能。

- NOVAMONT 開發基於人工智慧的綜合農業資料分析,用於最佳化可生物分解的地膜。

- RKW集團推出用於精準園藝的AI智慧覆蓋系統。

- 2025年美國關稅的影響 - 多膜市場

- 主要關稅表

- 價格影響分析

- 國家/地區

- 對終端用戶產業的影響

第6章:透過採用技術、專利、數位技術和人工智慧實現策略顛覆

- 主要新技術

- 可生物分解的生物基地膜

- 奈米科技增強多層膜

- 智慧/感測器整合多層膜

- 互補技術

- 滴灌系統

- 精密農業和土壤監測感測器

- 機械式地膜鋪設與回收機

- 鄰近技術

- 生質塑膠和生物聚合物技術

- 農業薄膜鋪設與回收機

- 土壤生物分解監測與環境檢測技術

- 專利分析

- 未來用途

- 可生物分解和可土壤分解的地膜材料

- 具有整合感測器監測功能的智慧多層薄膜

- 光選擇性與氣候適應多層膜

- 高性能多層薄膜

- 基於可回收循環經濟的農業薄膜

- 生成式人工智慧對多片電影市場的影響

- 生成式人工智慧在多片電影市場的應用

- 主要應用案例和市場展望

- 多片電影產業的最佳實踐

- 人工智慧在多片電影市場的應用案例研究研究

- 相互關聯的鄰近生態系及其對市場參與企業的影響

- 多片市場中客戶對採用生成式人工智慧的準備情況

- 成功案例和實際應用

第7章 監理情勢

- 當地法規和合規性

- 對永續性的承諾

- 對永續性和監管政策措施的影響

- 認證、標籤檢視、環境標準

第8章:顧客趨勢與購買行為

- 決策流程

- 買方相關利益者和採購評估標準

- 採購過程中的關鍵相關利益者

- 購買標準

- 招募中的障礙和內部挑戰

- 各終端使用者/終端用途產業中未被滿足的需求

- 市場盈利

第9章:多膜市場:依組件分類

- 傳統聚烯基多層膜

- LLDPE

- LDPE

- HDPE

- EVA

- 可生物分解和可堆肥的地膜

- PLA

- PHA

- PBAT

- 其他成分

- PBS(聚丁二酸丁二醇酯)

- TPS(熱塑性澱粉)

- OXO-PE,特殊共聚物,少量混合物

第10章:多片電影市場:按類型分類

- 透明的

- 黑色多色

- 多種顏色

- 光選擇性多

- 可生物分解的覆蓋物

- 其他類型

第11章:多膜市場:依應用領域分類

- 田間作物

- 園藝作物

第12章:多片電影市場:按地區分類

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲和紐西蘭

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 其他地區

- 非洲

- 中東

第13章 競爭格局

- 概述

- 主要企業的競爭策略/優勢(2020-2025)

- 收入分析(2020-2025)

- 市佔率分析(2025 年)

- 產品對比

- 企業評估矩陣:主要企業(2025 年)

- 公司評估矩陣:Start-Ups/中小企業(2025 年)

- 競爭格局

第14章:公司簡介

- 主要企業

- BASF SE

- AMCOR PLC

- DOW

- KURARAY

- EXXON MOBIL CORPORATION

- RKW GROUP

- INTERGRO, INC.

- GREEN MANEUVER INDUSTRIES LLP

- PLASTIKA KRITIS SA

- KOTHARI GROUP

- ORGANIX SOLUTIONS

- CAPTAIN POLYPLAST LTD.

- SUNSHINE PAPER COMPANY

- TILAK POLYPACK PVT. LTD

- IRIS POLYMERS

- 可生物分解地膜製造商

- EPI(EUROPE)LTD

- NOVAMONT SPA

- ARMANDO ALVAREZ GROUP

- ACHILLES CORPORATION

- WALKI GROUP OY

- UKHI

- TURFQUICK AB SWEDEN

- FILMORGANIC

- KINGFA SCIENCE & TECHNOLOGY(INDIA)LIMITED

- GROWIT INDIA PRIVATE LIMITED

第15章:調查方法

第16章:鄰近市場與相關市場

- 限制

- 多膜市場

- 市場定義

- 市場概覽

第17章附錄

The global mulch films market is estimated at USD 11.02 billion in 2026 and is projected to reach USD 15.13 billion by 2031, at a CAGR of 6.5%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD) and Volume (Metric Tons) |

| Segments | By Type, Element, and Application, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

The market is experiencing significant changes due to the increased adoption of precision agriculture, protected cultivation, and advanced soil management. The incorporation of smart farming technology, such as sensor-based irrigation systems, automatic mulch laying equipment, and climate-responsive films, is further enhancing product capabilities. Major players in the industry are actively working towards developing high-performance biodegradable and UV-stabilized films to improve soil health, minimize environmental damage, and encourage green farming. Recent product developments in the mulch films industry indicate an increased focus on product longevity, moisture retention, and crop-specific capabilities, indicating an upward trend in product growth.

Opportunities and disruption in the mulch films market. The opportunities and disruption in the mulch films industry are largely associated with the rapid shift to sustainable agriculture and resource-efficient farming practices. Mulch films are seen to have tremendous commercial potential for farmers and manufacturers, as the industry is witnessing increased demand for crop yield, better produce quality, and efficient water usage. The use of mulch films by farmers can help in the efficient use of water, reduce weeds, control soil temperature, and reduce the use of herbicides, thereby increasing the profitability of the farming industry, especially in horticulture and high-value crops. The disruption in the industry can be attributed to the increasing environmental regulations on the use of plastic, the rise of eco-friendly alternatives, and the shift to sustainable materials, which are disrupting the industry, thereby creating a challenge for the overall industry to grow.

AI-driven nutrient optimization: Artificial intelligence and machine learning are also useful in the mulch films market. This will help the company understand the soil, the weather, and the crops before they start making the films. They will, therefore, be aware of the thickness, the color, and the type of film to make. For example, the films may be black to control weeds. On the other hand, the transparent ones may be used for warming the soil. The durability of the films and the time taken for them to decompose may also be ascertained using artificial intelligence. This will help prevent failures and costs. The farmers will also benefit from the data tools. This will help them understand when to use the films and the type of film to use. They will, therefore, plan well, and there will be no form of waste. This will result in increased yield from the farms.

Advanced formulation technologies: One of the major areas of focus in the mulch films industry is material development. Companies are developing conventional as well as eco-friendly materials. However, polyethylene films are still in use due to their high strength and cost-effectiveness. At the same time, biodegradable films are also in high demand due to the implementation of stricter rules regarding environmental protection. Additionally, new products in the industry come equipped with better UV protection, allowing them to withstand harsh sun conditions. Some of these products are also better at controlling soil temperature, thereby allowing crops to develop faster. Some of them also provide better moisture retention capabilities, thereby reducing water usage. Some of these products are also tear-resistant during installation as well as usage. Films for crops are also available in the industry, where products are designed according to the needs of crops such as fruits, vegetables, or flowers.

Precision fertigation systems: The techniques that have been adopted for the application of mulch films are also being modernized by making proper use of modern technology. Modern technology has helped farmers in making proper use of automatic mulch laying machines. This helps in the proper and uniform application of mulch films. This has helped in saving time and labor. Soil moisture sensors have helped in acquiring proper knowledge regarding irrigation. With the help of IoT technology, proper knowledge can be obtained regarding the prevailing conditions in the field. GPS-based farm management techniques have helped in proper planning for proper spacing in the application of mulch films. This has helped in avoiding errors in the application of mulch films. Such errors lead to the wastage of resources. Proper techniques for the application of mulch films have helped in increasing efficiency and productivity from the same land.

"Conventional polyolefin-based mulch films stood as the major segment within the form segment of the mulch films market."

The mulch films market indicates that the conventional polyolefin films have the largest market share in the form segment. They include films such as polyethylene, which are commonly used in all farming regions. The films are leading the market due to the ease of production, low cost, and simplicity of use. They are also the preference of the farmers, as they provide good performance in terms of weeds, moisture, and soil temperature. The films are also strong enough to withstand various kinds of weather, making them suitable for repeated use.

These films are easy to store, transport, and apply with the help of standard mulch laying machines. Also, they are available in various colors and thickness levels, making it easy for the farmer to select the product based on the needs of the crop and the climatic conditions. If compared with the other products, the performance of these films is guaranteed, and they are easy to handle. Also, the availability of these films in the market, both in developed and emerging countries, supports the high demand for the product. Furthermore, the low cost and easy supply of the product make it an easy choice for the farmer. Thus, the conventional polyolefin-based mulch films are the market leaders, despite the increasing trend towards biodegradable films.

"Within the application segment, horticulture crops accounted for the largest share."

The mulch films segment indicates that horticulture crops represent the highest share in the application segment. This includes crops such as fruits, vegetables, and flowers, among others. The high share is attributed to factors such as yield, quality, and appearance of crops. Mulch films help in controlling weeds, retaining moisture in the soil, and controlling soil temperature. These factors are crucial in crops that require stable climatic conditions. Mulch films also assist in controlling soil contact, thus making crops clean. Mulch films are used in both greenhouse and field horticulture. They are also helpful in the efficient use of water with the aid of drip irrigation systems. Water loss, herbicides, and labor costs are reduced with the use of these films. They are also helpful in the uniform growth of crops and the yield of crops during different seasons. With the increase in the demand for quality fruits and vegetables, the use of these films is also increasing. This maintains the leading position of the horticulture segment in the market for mulch films. In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the mulch films market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World (Middle East and Africa) - 10%

Prominent companies in the market include BASF SE (Germany), Amcor Plc (Switzerland), Dow Inc. (US), Kuraray Co., Ltd. (Japan), and Exxon Mobil Corporation (US). Other important companies include RKW Group (Germany), Intergro, Inc. (United States), Green Maneuver Industries LLP (India), Plastika Kritis S.A. (Greece), and Kothari Group (India). The market also includes Organix Solutions (India), Captain Polyplast Ltd. (India), Sunshine Paper Company (China), Tilak Polypack Pvt. Ltd. (India), and Iris Polymers (India).

Research Coverage:

This research report categorizes the mulch films market by type ( clear/transparent mulch, black mulch, colored mulch, photoselective mulch, degradable mulch, biodegradable mulch, photodegradable mulch, others), element (conventional polyolefin-based mulch films [LLDPE, LDPE, HDPE, EVA], biodegradable & compostable mulch films [PLA, PHA, PBAT], other elements), application (field crop, horticulture crop), and region. The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the global mulch films market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions and services, key strategies, contracts, partnerships, and agreements. New product & service launches, mergers and acquisitions, and recent developments associated with the global mulch films market. Competitive analysis of upcoming startups in the market ecosystem is covered in this report.

Reasons to buy this report:

The report will help the market leader/new entrants in this market with information on the closest approximations of the revenue numbers for the overall mulch films market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

1. In-depth Segmentation Based On Type, Element, and Application: Comprehensive analysis across clear/transparent mulch, black mulch, colored mulch, photoselective mulch, degradable mulch, biodegradable mulch, photodegradable mulch, others, conventional polyolefin-based mulch films (LLDPE, LDPE, HDPE, EVA), biodegradable & compostable mulch films (PLA, PHA, PBAT), other elements, application (field crops, horticulture crops). The study examines key drivers (enhancing crop productivity through microclimate management., improving water-use efficiency in irrigated agriculture, promoting protected cultivation via government subsidies, reducing weed pressure and chemical dependency), restraints (addressing agricultural plastic waste accumulation, managing higher costs of biodegradable alternatives, overcoming limited recycling infrastructure in rural areas, improving farmer awareness and technical training), opportunities (increasing adoption of precision irrigation and water management practices, accelerating transition toward sustainable and bio-based films, integrating mulch films with precision irrigation systems), and challenges (navigating regulatory restrictions on plastic usage, mitigating raw material price volatility. ensuring field performance consistency of biodegradable films).

2. Region-specific Insights with Focus on Emerging Markets: The report provides detailed country- and region-level analysis, highlighting growth opportunities across Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa. It evaluates regional demand patterns, irrigation penetration, regulatory policies related to nutrient management, and investment trends in precision agriculture, offering strategic guidance for expansion and localization initiatives.

3. Competitive Intelligence and Innovation Landscape: Leading market participants, BASF SE (Germany), Amcor Plc (Switzerland), Dow Inc. (US), Kuraray Co., Ltd. (Japan), and Exxon Mobil Corporation (US), are profiled in detail. The report covers recent product launches, capacity expansions, strategic partnerships, and investments in specialty nutrient technologies shaping the competitive dynamics of the global mulch market.

4. Demand Forecasts Backed by Data-driven Methodologies: Market sizing and growth projections through 2031 are developed using a combination of top-down and bottom-up approaches, validated by industry experts, trade associations, and official government data. These insights provide reliable guidance for planning investment and market opportunity assessment in the global mulch films sector.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MULCH FILMS MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MULCH FILMS MARKET

- 3.2 MULCH FILMS MARKET, BY TYPE AND REGION

- 3.3 MULCH FILMS MARKET, BY ELEMENT

- 3.4 MULCH FILMS MARKET, BY ELEMENT

- 3.5 MULCH FILMS MARKET, BY APPLICATION

- 3.6 MULCH FILMS MARKET, BY COUNTRY/REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Enhancing Crop Productivity Through Microclimate Management

- 4.2.1.2 Improving Water-use Efficiency in Irrigated Agriculture

- 4.2.1.3 Promoting Protected Cultivation via Government Subsidies

- 4.2.1.4 Reducing Weed Pressure and Chemical Dependency

- 4.2.2 RESTRAINTS

- 4.2.2.1 Addressing Agricultural Plastic Waste Accumulation

- 4.2.2.2 Managing Higher Costs of Biodegradable Alternatives

- 4.2.2.3 Limited Recycling Infrastructure in Rural Areas

- 4.2.2.4 Improving Farmer Awareness and Technical Training

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing Adoption of Precision Irrigation and Water Management Practices

- 4.2.3.2 Accelerating Transition Toward Sustainable and Bio-based Films

- 4.2.3.3 Environmental Concerns Related to Plastic Residue Accumulation

- 4.2.4 CHALLENGES

- 4.2.4.1 Navigating Regulatory Restrictions on Plastic Usage

- 4.2.4.2 Mitigating Raw Material Price Volatility

- 4.2.4.3 Ensuring Field Performance Consistency of Biodegradable Films

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MULCH FILMS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 RISE IN POPULATION AND SCARCITY OF ARABLE LAND

- 5.2.2 GLOBAL AGRICULTURAL WATER USE TRENDS IMPACTING MULCH FILMS MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL PROCUREMENT

- 5.3.2 POLYMER PROCESSING AND COMPOUNDING

- 5.3.3 FILM MANUFACTURING (EXTRUSION)

- 5.3.4 PRODUCT CUSTOMIZATION AND PACKAGING

- 5.3.5 DISTRIBUTION AND SALES NETWORK

- 5.3.6 END USE, POST-SALES SUPPORT, AND WASTE MANAGEMENT

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 DEMAND SIDE

- 5.4.2 SUPPLY SIDE

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.3 AVERAGE SELLING PRICE TREND, BY APPLICATION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO OF HS CODE 392010

- 5.6.2 EXPORT SCENARIO OF HS CODE 392010

- 5.7 KEY CONFERENCES AND EVENTS, 2024-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 BASF SE ADVANCED BIODEGRADABLE MULCH FILM PERFORMANCE WITH AI-DRIVEN FIELD ANALYTICS

- 5.9.2 NOVAMONT INTEGRATED AI-BASED AGRONOMIC DATA ANALYTICS FOR BIODEGRADABLE MULCH FILM OPTIMIZATION

- 5.9.3 RKW GROUP IMPLEMENTED AI-ENABLED SMART MULCHING SYSTEM FOR PRECISION HORTICULTURE

- 5.10 IMPACT OF 2025 US TARIFF - MULCH FILMS MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 China (Asia Pacific)

- 5.10.4.2 Canada (North America)

- 5.10.4.3 European Union (Europe)

- 5.10.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 BIODEGRADABLE AND BIO-BASED MULCH FILMS

- 6.1.2 NANOTECHNOLOGY-ENHANCED MULCH FILMS

- 6.1.3 SMART/SENSOR-INTEGRATED MULCH FILMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 DRIP IRRIGATION SYSTEMS

- 6.2.2 PRECISION AGRICULTURE & SOIL MONITORING SENSORS

- 6.2.3 MECHANICAL MULCH FILM LAYING AND RETRIEVAL EQUIPMENT

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 BIOPLASTICS AND BIOPOLYMER TECHNOLOGY

- 6.3.2 AGRICULTURAL FILM LAYING AND RETRIEVAL MACHINERY

- 6.3.3 SOIL BIODEGRADATION MONITORING & ENVIRONMENTAL TESTING TECHNOLOGIES

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 BIODEGRADABLE AND SOIL-DEGRADABLE MULCH FILM MATERIALS

- 6.5.2 SMART MULCH FILMS WITH SENSOR-INTEGRATED MONITORING

- 6.5.3 PHOTOSELECTIVE AND CLIMATE-ADAPTIVE MULCH FILMS

- 6.5.4 MULTI-LAYER HIGH-PERFORMANCE MULCH FILM STRUCTURES

- 6.5.5 RECYCLABLE AND CIRCULAR ECONOMY-BASED AGRICULTURAL FILMS

- 6.6 IMPACT OF GENERATIVE AI ON MULCH FILMS MARKET

- 6.6.1 INTRODUCTION

- 6.6.2 USE OF GENERATIVE AI ON MULCH FILMS MARKET

- 6.6.3 TOP USE CASES AND MARKET POTENTIAL

- 6.6.4 BEST PRACTICES IN MULCH FILMS INDUSTRY

- 6.6.5 CASE STUDIES OF AI IMPLEMENTATION IN MULCH FILMS MARKET

- 6.6.6 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.7 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN MULCH FILMS MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.2.3 ADOPTION BARRIER & INTERNAL CHALLENGES

- 8.2.4 UNMET NEEDS OF VARIOUS END USERS/END-USE INDUSTRIES

- 8.2.4.1 Open-field Crop Farmers (Vegetables, Fruits, Row Crops)

- 8.2.4.2 Greenhouse & Protected Cultivation Operators

- 8.2.4.3 Large Commercial Farms & Contract Farming Operations

- 8.2.4.4 Sustainable & Organic Farming Sector

- 8.2.5 MARKET PROFITABILITY

9 MULCH FILMS MARKET, BY ELEMENT

- 9.1 INTRODUCTION

- 9.2 CONVENTIONAL POLYOLEFIN-BASED MULCH FILMS

- 9.2.1 LLDPE

- 9.2.1.1 Soil temperature regulation to improve crop yields

- 9.2.2 LDPE

- 9.2.2.1 Growth in awareness among farmers led to increased use of LDPE mulch films

- 9.2.3 HDPE

- 9.2.3.1 Extensive use with variegated applications in agriculture

- 9.2.4 EVA

- 9.2.4.1 Increase in awareness of environmental benefits of EVA mulch films

- 9.2.1 LLDPE

- 9.3 BIODEGRADABLE & COMPOSTABLE MULCH FILMS

- 9.3.1 PLA

- 9.3.1.1 Technologically advanced PLA mulch films offer performance with sustainability

- 9.3.2 PHA

- 9.3.2.1 Rise in adoption of sustainable agriculture among farmers

- 9.3.3 PBAT

- 9.3.3.1 Rising adoption of PBAT for high-performance biodegradable mulch films

- 9.3.1 PLA

- 9.4 OTHER ELEMENTS

- 9.4.1 PBS (POLYBUTYLENE SUCCINATE)

- 9.4.1.1 Increasing demand for biodegradable polymers driving adoption of PBS mulch films

- 9.4.2 TPS (THERMOPLASTIC STARCH)

- 9.4.2.1 Expanding use of bio-based materials supporting development of TPS mulch films

- 9.4.3 OXO-PE, SPECIALTY COPOLYMERS, MINOR BLENDS

- 9.4.3.1 Expanding use of bio-based blends

- 9.4.1 PBS (POLYBUTYLENE SUCCINATE)

10 MULCH FILMS MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 CLEAR/TRANSPARENT

- 10.2.1 USE OF CLEAR PLASTIC MULCHES IN COOLER REGIONS

- 10.3 BLACK MULCH

- 10.3.1 INCREASED PRODUCTION OF LEAFY VEGETABLES THAT USE INEXPENSIVE BLACK MULCHES

- 10.4 COLORED MULCH

- 10.4.1 COLORED MULCHES FOR IMPROVED CROP PRODUCTION

- 10.5 PHOTOSELECTIVE MULCH

- 10.5.1 ADOPTION OF PHOTOSELECTIVE MULCH FILMS FOR SUSTAINABLE AGRICULTURE

- 10.6 DEGRADABLE MULCH

- 10.6.1 INCREASE IN USE OF DEGRADABLE MULCH FILMS

- 10.6.2 BIODEGRADABLE MULCH

- 10.6.3 PHOTODEGRADABLE MULCH

- 10.7 OTHER TYPES

11 MULCH FILMS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 FIELD CROPS

- 11.2.1 DEMAND FOR IMPROVED YIELDS OF HIGH-VALUE CROPS

- 11.2.2 CEREALS & GRAINS

- 11.2.3 OILSEEDS & PULSES

- 11.2.4 OTHER FIELD CROPS

- 11.3 HORTICULTURAL CROPS

- 11.3.1 HIGH PREFERENCE FOR COLORED MULCH IN COMMERCIAL HORTICULTURE

- 11.3.2 FRUIT & VEGETABLES

- 11.3.3 FLOWERS & ORNAMENTALS

- 11.3.4 OTHER HORTICULTURE CROPS

12 MULCH FILMS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Rise in demand for mulch films from food and dairy industries

- 12.2.2 CANADA

- 12.2.2.1 Need to reduce water usage, control weed growth, and improve soil quality

- 12.2.3 MEXICO

- 12.2.3.1 Skilled and cost-effective labor force and free trade agreements

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Favorable EU regulations for selecting plastics and new recycling initiatives for mulch films

- 12.3.2 FRANCE

- 12.3.2.1 Over 1 million hectares covered in mulch films, especially black

- 12.3.3 UK

- 12.3.3.1 Need to enhance crop yields, improve crop quality, and reduce weed control costs

- 12.3.4 ITALY

- 12.3.4.1 Adoption of eco-friendly films and various government initiatives to promote mulch films

- 12.3.5 SPAIN

- 12.3.5.1 Implementation of plastic waste recycling, reduction of plastic usage, and landfilling in cooperation

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Massive industrial growth & urbanization, and growth in focus on increasing agricultural output

- 12.4.2 INDIA

- 12.4.2.1 Promotion of agro-textile sector by government and increase in food demand

- 12.4.3 JAPAN

- 12.4.3.1 Advanced crop technologies and need to save labor and time

- 12.4.4 AUSTRALIA & NEW ZEALAND

- 12.4.4.1 Effectiveness of mulch films in promoting growth of avocado trees

- 12.4.5 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 SOUTH AMERICA

- 12.5.1 BRAZIL

- 12.5.1.1 High adoption of intensive agricultural practices, expansion of irrigated agriculture, and greater demand for high-quality fruits and vegetables

- 12.5.2 ARGENTINA

- 12.5.2.1 Expansion of mulch film adoption driven by export-oriented agriculture

- 12.5.3 REST OF SOUTH AMERICA

- 12.5.1 BRAZIL

- 12.6 REST OF THE WORLD (ROW)

- 12.6.1 AFRICA

- 12.6.1.1 Availability of affordable and versatile mulch films

- 12.6.2 MIDDLE EAST

- 12.6.2.1 Need to conserve soil moisture, reduce weed growth, enhance soil fertility, and improve crop yields

- 12.6.1 AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2020-2025

- 13.3 REVENUE ANALYSIS, 2020-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 PRODUCT COMPARISON

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.6.5.1 Company footprint

- 13.6.5.2 Type footprint

- 13.6.5.3 Application footprint

- 13.6.5.4 Type footprint

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- 13.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.7.5.1 Detailed list of key startups/SMEs

- 13.7.5.2 Competitive benchmarking of key startups/SMEs

- 13.8 COMPETITIVE SCENARIO

- 13.8.1 PRODUCT LAUNCHES

- 13.8.2 DEALS

- 13.8.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 BASF SE

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 AMCOR PLC

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 DOW

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 KURARAY

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses and competitive threats

- 14.1.5 EXXON MOBIL CORPORATION

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 RKW GROUP

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 MnM view

- 14.1.7 INTERGRO, INC.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 MnM view

- 14.1.8 GREEN MANEUVER INDUSTRIES LLP

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 MnM view

- 14.1.9 PLASTIKA KRITIS S.A.

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 MnM view

- 14.1.10 KOTHARI GROUP

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 MnM view

- 14.1.11 ORGANIX SOLUTIONS

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 MnM view

- 14.1.12 CAPTAIN POLYPLAST LTD.

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 MnM view

- 14.1.13 SUNSHINE PAPER COMPANY

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 MnM view

- 14.1.14 TILAK POLYPACK PVT. LTD

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 MnM view

- 14.1.15 IRIS POLYMERS

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.15.3 MnM view

- 14.1.1 BASF SE

- 14.2 BIODEGRADABLE MULCH FILM MANUFACTURERS

- 14.2.1 EPI (EUROPE) LTD

- 14.2.1.1 Business overview

- 14.2.1.2 Products offered

- 14.2.1.3 MnM view

- 14.2.2 NOVAMONT S.P.A.

- 14.2.2.1 Business overview

- 14.2.2.2 Products offered

- 14.2.2.3 Recent developments

- 14.2.2.4 MnM view

- 14.2.3 ARMANDO ALVAREZ GROUP

- 14.2.3.1 Business overview

- 14.2.3.2 Products offered

- 14.2.3.3 Recent developments

- 14.2.3.4 MnM view

- 14.2.4 ACHILLES CORPORATION

- 14.2.4.1 Business overview

- 14.2.4.2 Products offered

- 14.2.4.3 MnM view

- 14.2.5 WALKI GROUP OY

- 14.2.5.1 Business overview

- 14.2.5.2 Products offered

- 14.2.5.3 MnM view

- 14.2.6 UKHI

- 14.2.7 TURFQUICK AB SWEDEN

- 14.2.8 FILMORGANIC

- 14.2.9 KINGFA SCIENCE & TECHNOLOGY (INDIA) LIMITED

- 14.2.10 GROWIT INDIA PRIVATE LIMITED

- 14.2.1 EPI (EUROPE) LTD

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 List of major secondary sources

- 15.1.1.2 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key industry insights

- 15.1.2.3 Breakdown of primaries

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.2.2.1 Approach to estimate market size using top-down analysis

- 15.3 DATA TRIANGULATION

- 15.4 RESEARCH ASSUMPTIONS

- 15.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 ADJACENT AND RELATED MARKETS

- 16.1 INTRODUCTION

- 16.2 LIMITATIONS

- 16.3 MULCH FILMS MARKET

- 16.3.1 MARKET DEFINITION

- 16.3.2 MARKET OVERVIEW

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS

List of Tables

- TABLE 1 INCLUSIONS & EXCLUSIONS

- TABLE 2 USD EXCHANGE RATES, 2021-2025

- TABLE 3 MULCH FILMS MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 MULCH FILMS ECOSYSTEM

- TABLE 5 AVERAGE SELLING PRICE OF MULCH FILMS OF KEY PLAYERS, BY TYPE, 2025 (USD/KG)

- TABLE 6 AVERAGE SELLING PRICE TREND OF MULCH FILMS, BY REGION, 2023-2025 (USD/KG)

- TABLE 7 AVERAGE SELLING PRICE TREND OF MULCH FILMS, BY APPLICATION, 2023-2025 (USD/KG)

- TABLE 8 IMPORT VALUE OF HS CODE 392010, BY KEY COUNTRY, 2021-2025 (USD THOUSAND)

- TABLE 9 EXPORT VALUE OF HS CODE 392010, BY KEY COUNTRY, 2021-2025 (USD THOUSAND)

- TABLE 10 MULCH FILMS MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2024-2026

- TABLE 11 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 12 REGIONAL TARIFF IMPACT ON MULCH FILMS EXPORTS TO US

- TABLE 13 KEY PATENTS PERTAINING TO MULCH FILMS, 2015-2025

- TABLE 14 TOP USE CASES AND MARKET POTENTIAL

- TABLE 17 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- TABLE 18 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES AND OTHER ORGANIZATIONS

- TABLE 21 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 22 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 23 GLOBAL INDUSTRY STANDARDS IN MULCH FILMS MARKET

- TABLE 24 KEY INDUSTRY STANDARDS FOR MULCH FILMS MARKET

- TABLE 25 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY ELEMENT

- TABLE 26 KEY BUYING CRITERIA FOR ELEMENT

- TABLE 27 MULCH FILMS MARKET, BY ELEMENT, 2021-2025 (USD MILLION)

- TABLE 28 MULCH FILMS MARKET, BY ELEMENT, 2026-2031 (USD MILLION)

- TABLE 29 CONVENTIONAL POLYOLEFIN-BASED MULCH FILMS: MULCH FILMS MARKET, BY ELEMENT, 2021-2025 (USD MILLION)

- TABLE 30 CONVENTIONAL POLYOLEFIN-BASED MULCH FILMS: MULCH FILMS MARKET, BY ELEMENT, 2026-2031 (USD MILLION)

- TABLE 31 CONVENTIONAL POLYOLEFIN-BASED MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 32 CONVENTIONAL POLYOLEFIN-BASED MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 33 LLDPE-BASED MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 34 LLDPE-BASED MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 35 LDPE: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 36 LDPE: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 37 HDPE: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 38 HDPE: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 39 EVA-BASED MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 40 EVA-BASED MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 41 BIODEGRADABLE & COMPOSTABLE MULCH FILMS: MULCH FILMS MARKET, BY ELEMENT, 2021-2025 (USD MILLION)

- TABLE 42 BIODEGRADABLE & COMPOSTABLE MULCH FILMS: MULCH FILMS MARKET, BY ELEMENT, 2026-2031 (USD MILLION)

- TABLE 43 BIODEGRADABLE & COMPOSTABLE MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 44 BIODEGRADABLE & COMPOSTABLE MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 45 PLA-BASED MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 46 PLA-BASED MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 47 PHA: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 48 PHA: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 49 PBAT-BASED MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 50 PBAT-BASED MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 51 OTHER MULCH FILM ELEMENTS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 52 OTHER MULCH FILM ELEMENTS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 53 MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 54 MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 55 MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 56 MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 57 CLEAR/TRANSPARENT: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 58 CLEAR/TRANSPARENT: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 59 CLEAR/TRANSPARENT: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 60 CLEAR/TRANSPARENT: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 61 BLACK MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 62 BLACK MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 63 BLACK MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 64 BLACK MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 65 COLORED MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 66 COLORED MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 67 COLORED MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 68 COLORED MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 69 PHOTOSELECTIVE MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 70 PHOTOSELECTIVE MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 71 PHOTOSELECTIVE MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 72 PHOTOSELECTIVE MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 73 DEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 74 DEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 75 DEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 76 DEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 77 BIODEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 78 BIODEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 79 BIODEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 80 BIODEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 81 PHOTODEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 82 PHOTODEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 83 PHOTODEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 84 PHOTODEGRADABLE MULCH: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 85 OTHER TYPES: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 86 OTHER TYPES: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 87 OTHER TYPES: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 88 OTHER TYPES: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 89 MULCH FILMS MARKET, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 90 MULCH FILMS MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 91 FIELD CROPS: MULCH FILMS MARKET, BY CROP TYPE, 2021-2025 (USD MILLION)

- TABLE 92 FIELD CROPS: MULCH FILMS MARKET, BY CROP TYPE, 2026-2031 (USD MILLION))

- TABLE 93 FIELD CROPS: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 94 FIELD CROPS: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 95 FIELD CROPS: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 96 FIELD CROPS: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 97 HORTICULTURAL CROPS: MULCH FILMS MARKET, BY CROP TYPE, 2021-2025 (USD MILLION)

- TABLE 98 HORTICULTURAL CROPS: MULCH FILMS MARKET, BY CROP TYPE, 2026-2031 (USD MILLION)

- TABLE 99 HORTICULTURAL CROPS: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 100 HORTICULTURAL CROPS: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 101 HORTICULTURAL CROPS: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 102 HORTICULTURAL CROPS: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 103 MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 104 MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 105 MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 106 MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 107 NORTH AMERICA: MULCH FILMS MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 108 NORTH AMERICA: MULCH FILMS MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 109 NORTH AMERICA: MULCH FILMS MARKET, BY COUNTRY, 2021-2025 (KT)

- TABLE 110 NORTH AMERICA: MULCH FILMS MARKET, BY COUNTRY, 2026-2031 (KT)

- TABLE 111 NORTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 112 NORTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 113 NORTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 114 NORTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 115 NORTH AMERICA: MULCH FILMS MARKET, BY ELEMENT, 2021-2025 (USD MILLION)

- TABLE 116 NORTH AMERICA: MULCH FILMS MARKET, BY ELEMENT, 2026-2031 (USD MILLION)

- TABLE 117 NORTH AMERICA: MULCH FILMS MARKET, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 118 NORTH AMERICA: MULCH FILMS MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 119 NORTH AMERICA: MULCH FILMS MARKET FOR FIELD CROPS, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 120 NORTH AMERICA: MULCH FILMS MARKET FOR FIELD CROPS, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 121 NORTH AMERICA: MULCH FILMS MARKET FOR HORTICULTURAL CROPS, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 122 NORTH AMERICA: MULCH FILMS MARKET FOR HORTICULTURAL CROPS, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 123 US: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 124 US: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 125 US: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 126 US: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 127 CANADA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 128 CANADA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 129 CANADA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 130 CANADA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 131 MEXICO: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 132 MEXICO: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 133 MEXICO: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 134 MEXICO: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 135 EUROPE: MULCH FILMS MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 136 EUROPE: MULCH FILMS MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 137 EUROPE: MULCH FILMS MARKET, BY COUNTRY, 2021-2025 (KT)

- TABLE 138 EUROPE: MULCH FILMS MARKET, BY COUNTRY, 2026-2031 (KT)

- TABLE 139 EUROPE: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 140 EUROPE: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 141 EUROPE: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 142 EUROPE: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 143 EUROPE: MULCH FILMS MARKET, BY ELEMENT, 2021-2025 (USD MILLION)

- TABLE 144 EUROPE: MULCH FILMS MARKET, BY ELEMENT, 2026-2031 (USD MILLION)

- TABLE 145 EUROPE: MULCH FILMS MARKET, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 146 EUROPE: MULCH FILMS MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 147 EUROPE: MULCH FILMS MARKET, BY APPLICATION, 2021-2025 (KT)

- TABLE 148 EUROPE: MULCH FILMS MARKET, BY APPLICATION, 2026-2031 (KT)

- TABLE 149 FIELD CROPS: MULCH FILMS MARKET IN EUROPE, BY CROP TYPE, 2021-2025 (USD MILLION)

- TABLE 150 FIELD CROPS: MULCH FILMS MARKET IN EUROPE, BY CROP TYPE, 2026-2031 (USD MILLION)

- TABLE 151 HORTICULTURAL CROPS: MULCH FILMS MARKET IN EUROPE, BY CROP TYPE, 2021-2025 (USD MILLION)

- TABLE 152 HORTICULTURAL CROPS: MULCH FILMS MARKET IN EUROPE, BY CROP TYPE, 2026-2031 (USD MILLION)

- TABLE 153 GERMANY: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 154 GERMANY: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 155 GERMANY: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 156 GERMANY: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 157 FRANCE: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 158 FRANCE: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 159 FRANCE: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 160 FRANCE: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 161 UK: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 162 UK: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 163 UK: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 164 UK: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 165 ITALY: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 166 ITALY: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 167 ITALY: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 168 ITALY: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 169 SPAIN: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 170 SPAIN: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 171 SPAIN: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 172 SPAIN: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 173 REST OF EUROPE: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 174 REST OF EUROPE: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 175 REST OF EUROPE: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 176 REST OF EUROPE: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 177 ASIA PACIFIC: MULCH FILMS MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 178 ASIA PACIFIC: MULCH FILMS MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 179 ASIA PACIFIC: MULCH FILMS MARKET, BY COUNTRY, 2021-2025 (KT)

- TABLE 180 ASIA PACIFIC: MULCH FILMS MARKET, BY COUNTRY, 2026-2031 (KT)

- TABLE 181 ASIA PACIFIC: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 182 ASIA PACIFIC: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 183 ASIA PACIFIC: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 184 ASIA PACIFIC: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 185 ASIA PACIFIC: MULCH FILMS MARKET, BY ELEMENT, 2021-2025 (USD MILLION)

- TABLE 186 ASIA PACIFIC: MULCH FILMS MARKET, BY ELEMENT, 2026-2031 (USD MILLION)

- TABLE 187 ASIA PACIFIC: MULCH FILMS MARKET, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 188 ASIA PACIFIC: MULCH FILMS MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 189 ASIA PACIFIC: MULCH FILMS MARKET, BY APPLICATION, 2021-2025 (KT)

- TABLE 190 ASIA PACIFIC: MULCH FILMS MARKET, BY APPLICATION, 2026-2031 (KT)

- TABLE 191 ASIA PACIFIC: MULCH FILMS MARKET FOR FIELD CROPS, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 192 ASIA PACIFIC: MULCH FILMS MARKET FOR FIELD CROPS, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 193 ASIA PACIFIC: MULCH FILMS MARKET FOR HORTICULTURAL CROPS, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 194 ASIA PACIFIC: MULCH FILMS MARKET FOR HORTICULTURAL CROPS, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 195 CHINA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 196 CHINA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 197 CHINA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 198 CHINA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 199 INDIA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 200 INDIA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 201 INDIA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 202 INDIA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 203 JAPAN: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 204 JAPAN: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 205 JAPAN: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 206 JAPAN: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 207 AUSTRALIA & NEW ZEALAND: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 208 AUSTRALIA & NEW ZEALAND: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 209 AUSTRALIA & NEW ZEALAND: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 210 AUSTRALIA & NEW ZEALAND: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 211 REST OF ASIA PACIFIC: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 212 REST OF ASIA PACIFIC: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 213 REST OF ASIA PACIFIC: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 214 REST OF ASIA PACIFIC: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 215 SOUTH AMERICA: MULCH FILMS MARKET, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 216 SOUTH AMERICA: MULCH FILMS MARKET, BY COUNTRY, 2026-2031 (USD MILLION)

- TABLE 217 SOUTH AMERICA: MULCH FILMS MARKET, BY COUNTRY, 2021-2025 (KT)

- TABLE 218 SOUTH AMERICA: MULCH FILMS MARKET, BY COUNTRY, 2026-2031 (KT)

- TABLE 219 SOUTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 220 SOUTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 221 SOUTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 222 SOUTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 223 SOUTH AMERICA: MULCH FILMS MARKET, BY ELEMENT, 2021-2025 (USD MILLION)

- TABLE 224 SOUTH AMERICA: MULCH FILMS MARKET, BY ELEMENT, 2026-2031 (USD MILLION)

- TABLE 225 SOUTH AMERICA: MULCH FILMS MARKET, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 226 SOUTH AMERICA: MULCH FILMS MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 227 SOUTH AMERICA: MULCH FILMS MARKET, BY APPLICATION, 2021-2025 (KT)

- TABLE 228 SOUTH AMERICA: MULCH FILMS MARKET, BY APPLICATION, 2026-2031 (KT)

- TABLE 229 FIELD CROPS: MULCH FILMS MARKET IN SOUTH AMERICA, BY CROP TYPE, 2021-2025 (USD MILLION)

- TABLE 230 FIELD CROPS: MULCH FILMS MARKET IN SOUTH AMERICA, BY CROP TYPE, 2026-2031 (USD MILLION)

- TABLE 231 HORTICULTURAL CROPS: MULCH FILMS MARKET IN SOUTH AMERICA, BY CROP TYPE, 2021-2025 (USD MILLION)

- TABLE 232 HORTICULTURAL CROPS: MULCH FILMS MARKET IN SOUTH AMERICA, BY CROP TYPE, 2026-2031 (USD MILLION)

- TABLE 233 BRAZIL: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 234 BRAZIL: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 235 BRAZIL: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 236 BRAZIL: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 237 ARGENTINA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 238 ARGENTINA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 239 ARGENTINA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 240 ARGENTINA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 241 REST OF SOUTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 242 REST OF SOUTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 243 REST OF SOUTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 244 REST OF SOUTH AMERICA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 245 ROW: MULCH FILMS MARKET, BY REGION, 2021-2025 (USD MILLION)

- TABLE 246 ROW: MULCH FILMS MARKET, BY REGION, 2026-2031 (USD MILLION)

- TABLE 247 ROW: MULCH FILMS MARKET, BY REGION, 2021-2025 (KT)

- TABLE 248 ROW: MULCH FILMS MARKET, BY REGION, 2026-2031 (KT)

- TABLE 249 ROW: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 250 ROW: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 251 ROW: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 252 ROW: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 253 ROW: MULCH FILMS MARKET, BY ELEMENT, 2021-2025 (USD MILLION)

- TABLE 254 ROW: MULCH FILMS MARKET, BY ELEMENT, 2026-2031 (USD MILLION)

- TABLE 255 ROW: MULCH FILMS MARKET, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 256 ROW: MULCH FILMS MARKET, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 257 ROW: MULCH FILMS MARKET, BY APPLICATION, 2021-2025 (KT)

- TABLE 258 ROW: MULCH FILMS MARKET, BY APPLICATION, 2026-2031 (KT)

- TABLE 259 ROW: MULCH FILMS MARKET FOR FIELD CROPS, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 260 ROW: MULCH FILMS MARKET FOR FIELD CROPS, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 261 ROW: MULCH FILMS MARKET FOR HORTICULTURAL CROPS, BY APPLICATION, 2021-2025 (USD MILLION)

- TABLE 262 ROW: MULCH FILMS MARKET FOR HORTICULTURAL CROPS, BY APPLICATION, 2026-2031 (USD MILLION)

- TABLE 263 AFRICA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 264 AFRICA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 265 AFRICA: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 266 AFRICA: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 267 MIDDLE EAST: MULCH FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 268 MIDDLE EAST: MULCH FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

- TABLE 269 MIDDLE EAST: MULCH FILMS MARKET, BY TYPE, 2021-2025 (KT)

- TABLE 270 MIDDLE EAST: MULCH FILMS MARKET, BY TYPE, 2026-2031 (KT)

- TABLE 271 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN MULCH FILMS MARKET, 2020-2025

- TABLE 272 MULCH FILMS MARKET: DEGREE OF COMPETITION

- TABLE 273 MULCH FILMS MARKET: ELEMENT FOOTPRINT

- TABLE 274 MULCH FILMS MARKET: APPLICATION FOOTPRINT

- TABLE 275 MULCH FILMS MARKET: TYPE FOOTPRINT

- TABLE 276 MULCH FILMS MARKET: KEY STARTUPS/SMES

- TABLE 277 MULCH FILMS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2025

- TABLE 278 MULCH FILMS MARKET: PRODUCT LAUNCHES, JANUARY 2021-SEPTEMBER 2025

- TABLE 279 MULCH FILMS MARKET: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 280 MULCH FILMS MARKET: EXPANSIONS, JANUARY 2020-DECEMBER 2025

- TABLE 281 BASF SE: COMPANY OVERVIEW

- TABLE 282 BASF SE: PRODUCTS OFFERED

- TABLE 283 BASF SE: PRODUCT LAUNCHES

- TABLE 284 BASF SE: DEALS

- TABLE 285 BASF SE: EXPANSIONS

- TABLE 286 AMCOR PLC: COMPANY OVERVIEW

- TABLE 287 AMCOR PLC: PRODUCTS OFFERED

- TABLE 288 AMCOR PLC: DEALS

- TABLE 289 DOW: COMPANY OVERVIEW

- TABLE 290 DOW: PRODUCTS OFFERED

- TABLE 291 DOW: PRODUCT LAUNCHES

- TABLE 292 DOW: DEALS

- TABLE 293 KURARAY: COMPANY OVERVIEW

- TABLE 294 KURARAY: PRODUCTS OFFERED

- TABLE 295 EXXON MOBIL CORPORATION: BUSINESS OVERVIEW

- TABLE 296 EXXON MOBIL CORPORATION: PRODUCTS OFFERED

- TABLE 297 EXXON MOBIL CORPORATION: DEALS

- TABLE 298 EXXON MOBIL CORPORATION: EXPANSIONS

- TABLE 299 RKW GROUP: COMPANY OVERVIEW

- TABLE 300 RKW GROUP: PRODUCTS OFFERED

- TABLE 301 INTERGRO, INC.: COMPANY OVERVIEW

- TABLE 302 INTERGRO, INC.: PRODUCTS OFFERED

- TABLE 303 GREEN MANEUVER INDUSTRIES LLP: COMPANY OVERVIEW

- TABLE 304 GREEN MANEUVER INDUSTRIES LLP: PRODUCTS OFFERED

- TABLE 305 PLASTIKA KRITIS S.A.: COMPANY OVERVIEW

- TABLE 306 PLASTIKA KRITIS S.A.: OFFERED

- TABLE 307 KOTHARI GROUP: COMPANY OVERVIEW

- TABLE 308 KOTHARI GROUP: PRODUCTS OFFERED

- TABLE 309 ORGANIX SOLUTIONS: COMPANY OVERVIEW

- TABLE 310 ORGANIX SOLUTIONS: PRODUCTS OFFERED

- TABLE 311 CAPTAIN POLYPLAST LTD.: COMPANY OVERVIEW

- TABLE 312 CAPTAIN POLYPLAST LTD.: PRODUCTS OFFERED

- TABLE 313 SUNSHINE PAPER COMPANY: COMPANY OVERVIEW

- TABLE 314 SUNSHINE PAPER COMPANY: PRODUCTS OFFERED

- TABLE 315 TILAK POLYPACK PVT. LTD: COMPANY OVERVIEW

- TABLE 316 TILAK POLYPACK PVT. LTD: PRODUCTS OFFERED

- TABLE 317 IRIS POLYMERS: COMPANY OVERVIEW

- TABLE 318 IRIS POLYMERS: PRODUCTS OFFERED

- TABLE 319 EPI (EUROPE) LTD: COMPANY OVERVIEW

- TABLE 320 EPI (EUROPE) LTD: PRODUCTS OFFERED

- TABLE 321 NOVAMONT S.P.A.: COMPANY OVERVIEW

- TABLE 322 NOVAMONT S.P.A.: PRODUCTS OFFERED

- TABLE 323 NOVAMONT S.P.A: PRODUCT LAUNCHES

- TABLE 324 NOVAMONT S.P.A.: DEALS

- TABLE 325 ARMANDO ALVAREZ GROUP: COMPANY OVERVIEW

- TABLE 326 ARMANDO ALVAREZ GROUP: PRODUCTS OFFERED

- TABLE 327 ARMANDO ALVAREZ GROUP: PRODUCT LAUNCHES

- TABLE 328 ARMANDO ALVAREZ GROUP: DEALS

- TABLE 329 ACHILLES CORPORATION: COMPANY OVERVIEW

- TABLE 330 ACHILLES CORPORATION: PRODUCTS OFFERED

- TABLE 331 WAKI GROUP OY: COMPANY OVERVIEW

- TABLE 332 WALKI GROUP OY: PRODUCTS OFFERED

- TABLE 333 ADJACENT MARKET

- TABLE 334 AGRICULTURAL FILMS MARKET, BY TYPE, 2021-2025 (USD MILLION)

- TABLE 335 AGRICULTURAL FILMS MARKET, BY TYPE, 2026-2031 (USD MILLION)

List of Figures

- FIGURE 1 MARKET SEGMENTATION

- FIGURE 1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 2 MULCH FILMS MARKET, BY TYPE, 2026 - 2031

- FIGURE 3 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN MULCH FILMS MARKET, 2021-2025

- FIGURE 4 DISRUPTIVE TRENDS IMPACTING GROWTH OF MULCH FILMS MARKET

- FIGURE 5 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS IN MULCH FILMS MARKET, 2026

- FIGURE 6 ASIA PACIFIC TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 7 GROWING USE OF PRECISION NUTRIENT MANAGEMENT AND FERTIGATION IN MULCH FILMS MARKET

- FIGURE 8 BLACK MULCH AND ASIA PACIFIC ACCOUNTED FOR LARGEST MARKET SHARES IN 2026

- FIGURE 9 LLDPE SEGMENT DOMINATED MULCH FILMS MARKET IN 2026

- FIGURE 10 CONVENTIONAL POLYOLEFIN-BASED MULCH FILMS SEGMENT TO LEAD MARKET IN 2026

- FIGURE 11 HORTICULTURAL CROPS SEGMENT TO DOMINATE MARKET IN 2026

- FIGURE 12 CHINA TO REGISTER LARGEST MARKET SHARE DURING 2026

- FIGURE 13 MARKET DYNAMICS: MULCH FILMS MARKET

- FIGURE 14 US IRRIGATED HARVESTED ACRES (MILLION ACRES)

- FIGURE 15 MULCH FILMS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 16 TRENDS IN GLOBAL AGRICULTURAL LAND AREA, 2010-2023 (MILLION SQUARE KILOMETERS)

- FIGURE 17 AGRICULTURAL WATER WITHDRAWAL SHARE, BY REGION (%)

- FIGURE 18 MULCH FILMS MARKET: VALUE CHAIN ANALYSIS

- FIGURE 19 KEY PARTICIPANTS IN MULCH FILMS ECOSYSTEM

- FIGURE 20 MULCH FILMS MARKET: ECOSYSTEM ANALYSIS

- FIGURE 21 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD/KG)

- FIGURE 22 AVERAGE SELLING PRICE TREND, BY APPLICATION, 2023-2025 (USD/KG)

- FIGURE 23 IMPORT VALUE OF HS CODE 392010, BY KEY COUNTRY, 2021-2025 (USD THOUSAND)

- FIGURE 24 EXPORT VALUE OF HS CODE 392010, BY KEY COUNTRY, 2021-2025 (USD THOUSAND)

- FIGURE 25 MULCH FILMS MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 26 NUMBER OF PATENTS GRANTED FOR MULCH FILMS MARKET, 2016-2026

- FIGURE 27 FUTURE APPLICATIONS

- FIGURE 28 MULCH FILMS MARKET: DECISION-MAKING FACTORS

- FIGURE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY ELEMENT

- FIGURE 30 KEY INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR ELEMENTS

- FIGURE 31 MULCH FILMS MARKET, BY ELEMENT, 2026-2031 (USD MILLION)

- FIGURE 32 BLACK MULCH SEGMENT TO DOMINATE MULCH FILMS MARKET (USD MILLION)

- FIGURE 33 HORTICULTURAL CROPS SET TO DOMINATE MULCH FILMS MARKET, 2026 VS. 2031 (USD MILLION)

- FIGURE 34 INDIA TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- FIGURE 35 ASIA PACIFIC: MARKET SNAPSHOT

- FIGURE 36 SEGMENTAL REVENUE ANALYSIS OF KEY PLAYERS, 2022-2025 (USD BILLION)

- FIGURE 37 SHARE ANALYSIS OF KEY PLAYERS IN MULCH FILMS MARKET, 2025

- FIGURE 38 PRODUCT ANALYSIS, BY KEY PLAYER

- FIGURE 39 MULCH FILMS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 40 MULCH FILMS MARKET: COMPANY FOOTPRINT

- FIGURE 41 MULCH FILMS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 42 BASF SE: COMPANY SNAPSHOT

- FIGURE 43 AMCOR PLC: COMPANY SNAPSHOT

- FIGURE 44 DOW: COMPANY SNAPSHOT

- FIGURE 45 KURARAY: COMPANY SNAPSHOT

- FIGURE 46 EXXON MOBIL CORPORATION: COMPANY SNAPSHOT

- FIGURE 47 CAPTAIN POLYPLAST LTD.: COMPANY SNAPSHOT

- FIGURE 48 ACHILLES CORPORATION: COMPANY SNAPSHOT

- FIGURE 49 MULCH FILMS MARKET: RESEARCH DESIGN

- FIGURE 50 KEY DATA FROM SECONDARY SOURCES

- FIGURE 51 KEY DATA FROM PRIMARY SOURCES

- FIGURE 52 INSIGHTS FROM INDUSTRY EXPERTS

- FIGURE 53 BREAKDOWN OF PRIMARIES, BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 54 MULCH FILMS MARKET: DEMAND-SIDE CALCULATION

- FIGURE 55 MULCH FILMS MARKET SIZE ESTIMATION STEPS AND RESPECTIVE SOURCES: SUPPLY SIDE

- FIGURE 56 MULCH FILMS MARKET: SUPPLY-SIDE ANALYSIS

- FIGURE 57 DATA TRIANGULATION METHODOLOGY

多層膜市場:按類型、材料、技術、厚度和來源分類-2026-2032年全球市場預測

多層膜市場:按類型、材料、技術、厚度和來源分類-2026-2032年全球市場預測 地膜市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

地膜市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 2026年全球多層薄膜市場報告

2026年全球多層薄膜市場報告 地膜市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、要素、地區和競爭細分,2020-2030 年

地膜市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、要素、地區和競爭細分,2020-2030 年 地膜市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

地膜市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 2030 年多層薄膜市場預測:按類型、材料、應用、最終用戶和地區進行的全球分析

2030 年多層薄膜市場預測:按類型、材料、應用、最終用戶和地區進行的全球分析 複合薄膜市場規模、佔有率、趨勢分析報告:按原料、作物、地區、細分市場預測,2025-2030

複合薄膜市場規模、佔有率、趨勢分析報告:按原料、作物、地區、細分市場預測,2025-2030 複合膜市場評估:依產品類型、應用、要素和地區劃分的機會和預測(2017-2031)

複合膜市場評估:依產品類型、應用、要素和地區劃分的機會和預測(2017-2031) 全球地膜市場規模研究,按類型、應用、要素和區域預測 2022-2032

全球地膜市場規模研究,按類型、應用、要素和區域預測 2022-2032