|

市場調查報告書

商品編碼

1936068

全球電動車充電器用電子灌封膠市場(至2032年),按充電器類型(交流/直流)、安裝類型(壁掛式/固定式)、材料類型(聚氨酯/矽酮/環氧樹脂)、固化技術、應用、電動車組件和地區分類Electronic Potting Compound Market for EV charger, By Charger Type (AC, DC), Setup Type (Wall Mount, Stationary), Material Type (Polyurethane, Silicone, Epoxy), Curing Technology, Application, EV Component, and Region - Global Forecast to 2032 |

||||||

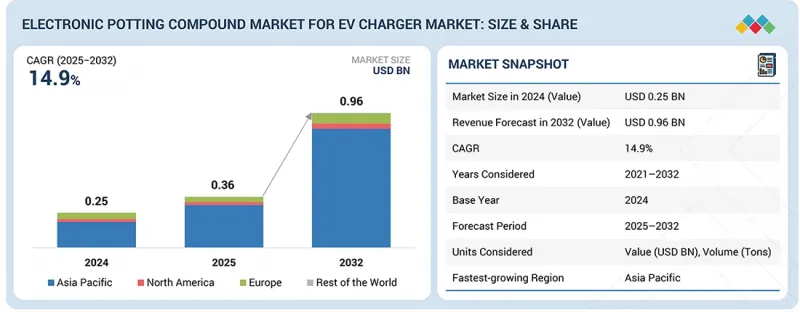

預計電動車充電器用電子灌封化合物的市場規模將從 2025 年的 3.6 億美元成長到 2032 年的 9.6 億美元,複合年成長率為 14.9%。

交流充電器中緊湊型整合電源和基板的日益普及,推動了對低黏度灌封化合物的需求,這種化合物能夠確保完全覆蓋,同時又不影響散熱性能。

| 調查範圍 | |

|---|---|

| 調查期 | 2021-2032 |

| 基準年 | 2024 |

| 預測期 | 2025-2032 |

| 單元 | 金額(美元),數量(噸) |

| 部分 | 充電器類型、安裝類型、材料類型、固化技術、電動汽車零件、應用 |

| 目標區域 | 亞太地區、歐洲、北美和世界其他地區 |

在直流充電器領域,超快速充電技術的普及推動了對高導熱性和高局部放電電阻灌封材料的需求。此外,直流充電器的設計正朝著液冷和密封式功率模組的方向發展,這增加了灌封層的厚度和材料消耗。對於這兩種類型的充電器而言,與自動化點膠製程的兼容性和快速熱固化性能正成為關鍵的材料要求。此外,戶外充電器安裝量的增加也凸顯了具有長期防潮性和抗電痕性能的材料的重要性。

根據充電器類型分類,預計直流充電器將在預測期內引領市場。

由於直流充電器相比交流充電器和車載充電器具有更高的功率密度和更高的運行壓力,預計在預測期內,直流充電器將成為市場的主要驅動力。公共直流充電設施和車隊停車場運作環境惡劣,常年潮濕、振動,且需連續運行,因此對能夠確保電氣絕緣、環境保護和減震性能的堅固耐用的封裝的需求日益成長。原始設備製造商 (OEM) 和充電網路營運商的大規模基礎設施建設優先考慮在高速公路、商業設施和車隊停車場安裝高功率直流設備,這導致對使用大量灌封材料的充電平台的需求激增。

派克漢尼汾等材料供應商正積極響應,推出低黏度、快速流動的導熱灌封膠,這種灌封膠能夠填充高功率直流模組內部的狹小縫隙,並將熱量高效地傳遞至機殼或散熱器。直接注射和澆注系統具有固化速度更快、可進行在線連續品管等優勢,正日益普及,以支持高產量生產。

同時,政府主導的項目,例如美國的「國家電動車基礎設施」(NEVI)舉措和中國超快速公共充電走廊的持續擴張,正在加速高功率直流充電樁的部署。例如,2025年8月,加州能源委員會啟動了5,500萬美元的“加州快速充電計畫”,旨在津貼在企業和公共設施安裝公共快速充電樁,包括高功率直流充電站。這些投資推動了對兼具耐熱性和電氣可靠性的灌封膠的需求,因為新的高功率直流充電樁需要大量的封裝材料來確保長期運作穩定性和符合相關法規。

“按材料類型,預計環氧樹脂材料在預測期內將呈現最高的成長率。”

環氧樹脂憑藉其高機械強度和結構剛性,在電動車充電器灌封應用中發揮關鍵作用,為暴露於熱循環、振動和機械衝擊的敏感電子和功率元件提供持久保護。其優異的電絕緣性和耐化學性使其成為車載和非車載充電系統中高壓交流/直流轉換和安全關鍵功能的理想選擇。環氧樹脂灌封化合物還具有強大的防潮和防污染性能,可延長電動車充電器電子元件在各種環境條件下的運作。配方的柔軟性允許添加導熱填料,從而改善高功率模組和高密度功率電子裝置的散熱性能。此外,成熟的全球製造基地和完善的環氧樹脂系統供應商生態系統支援電動車充電器的可擴展且經濟高效的生產。人們也越來越重視低VOC排放且符合REACH等不斷更新的法規的環保環氧樹脂配方,同時又不影響其絕緣性能或耐久性。例如,2025年11月,Wevo Chemie推出了阻燃導熱環氧灌封樹脂,符合EN 45545-2和UL 94 V-0等嚴格的安全標準。這些材料具有很高的抗局部放電能力和改進的流動性能,使其適用於高壓、高性能應用,包括先進電動車充電器的封裝。

按地區分類,預計歐洲在預測期內將佔據主要佔有率。

歐洲的電動車充電基礎設施正在快速擴張,預計到2025年底,公共充電樁的數量將超過120萬個,快速充電和超快速充電也將持續強勁成長。這推動了對充電樁電子元件的需求,而這些電子元件需要灌封和封裝。強而有力的監管和政策支持,特別是歐盟的《替代燃料基礎設施法規》和廣泛的排放目標,促使各成員國廣泛採用高功率充電樁,從而推動了對耐用且符合規範的灌封材料的需求。歐洲的充電樁製造商和充電服務供應商(例如壁掛式充電樁)正在大力投資智慧、高密度超快速充電樞紐,這些樞紐整合了複雜的電源和控制電子元件,並受益於用於絕緣、溫度控管和環境保護的灌封技術。該地區對互通性和安全標準的重視,包括採用ISO 15118標準實施CCS(充電樁認證),進一步提高了對電子保護材料的性能和可靠性要求。這推動了先進灌封化合物在充電樁設計上的應用。公共電網中直流和超快速充電樁的快速普及,推動了對具有優異導熱性和機械強度的灌封膠的需求,以確保溫度控管和長期可靠性。同時,歐盟範圍內統一的介面、通訊協定和安全框架簡化了充電樁平台,並促進了灌封材料規格的一致性。歐盟也是漢高、Electrolube、Demak集團和ELANTAS等主要灌封膠生產商的所在地。

本報告調查了電動車充電器電子灌封化合物的全球市場,並提供了市場概況、影響市場成長的各種因素分析、技術和專利趨勢、法律制度、案例研究、市場規模趨勢和預測、按各個細分市場、地區/主要國家進行的詳細分析、競爭格局以及主要企業的概況。

目錄

第1章 引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進要素

- 抑制因素

- 機會

- 任務

- 未滿足的需求和閒置頻段

- 與相關市場和不同產業相關的跨領域機遇

- 一級/二級/三級公司的策略性舉措

第5章 產業趨勢

- 總體經濟指標

- 影響您業務的趨勢和顛覆性因素

- 定價分析

- 生態系分析

- 供應鏈分析

- 案例研究分析

- 投資和資金籌措方案

- 貿易分析

- 2026年重大會議和活動

- 電動車充電器材料消耗量分析

- 電動車充電器灌封化合物材料的未來發展藍圖

- 主要市場公共電動車充電樁安裝分析

第6章:技術進步、人工智慧的影響、專利、創新與未來應用

- 專利分析

- 生成式人工智慧對電動車充電器電子灌封化合物市場的影響

- 關鍵新興技術

- 互補技術

- 鄰近技術

- 技術/產品藍圖

第7章 監理環境與永續性舉措

- 地方法規和合規性

- 監管機構、政府機構和其他組織

- 對永續性的承諾

第8章:顧客狀況與購買行為

- 決策流程

- 買方相關利益者和採購評估標準

- 採用障礙和內部挑戰

9. 按充電器類型分類的電動車充電器用電子灌封膠市場

- 交流充電器

- 直流充電器

- 關鍵見解

第10章 依安裝類型分類的電動車充電器電子灌封膠市場

- 壁掛式(單一)

- 固定類型(公共)

- 關鍵見解

第11章:電動車充電器用電子灌封膠市場(依材料分類)

- 聚氨酯

- 矽酮

- 環氧樹脂

- 關鍵見解

12. 依固化技術分類的電動車充電器電子灌封膠市場

- 室溫固化

- 熱固化

- 紫外線固化

- 關鍵見解

第13章 電動車充電器用電子灌封膠市場(以電動車組件分類)

- 電動機定子

- 電動汽車電池

- 電動車電池冷卻系統

- 車用充電器(OBC)

- 車用充電連接器

- 汽車電源轉換器

- 其他

- 關鍵見解

第14章 電動車充電器用電子灌封膠市場(依應用領域分類)

- 電力電子

- 高壓元件、匯流排、感測器繼電器

- PCB和控制模組

- 連接器電纜 IP 區

- 充能槍

- 其他

第15章 電動車充電器用電子灌封化合物市場(按地區分類)

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 印尼

- 新加坡

- 歐洲

- 奧地利

- 丹麥

- 法國

- 德國

- 荷蘭

- 挪威

- 西班牙

- 瑞典

- 瑞士

- 英國

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 世界其他地區

- 巴西

- 阿拉伯聯合大公國

第16章 競爭格局

- 概述

- 主要企業/主要企業的策略

- 電動車充電器用電子灌封膠製造商市場佔有率分析

- 上市公司和公眾公司的獲利分析

- 估值和財務指標

- 品牌/產品對比

- 公司評估矩陣:主要企業

- 公司估值矩陣:Start-Ups/中小企業

- 競爭場景

第17章:公司簡介

- 主要企業

- HENKEL CORPORATION

- PARKER HANNIFIN CORP

- ELANTAS

- DOW

- MOMENTIVE

- ELECTROLUBE

- DEMAK GROUP

- WEVO-CHEMIE GMBH

- EPOXIES, ETC.

- RAMPF

- KISLING

- SIKA AUTOMOTIVE

- 其他公司

- MASTER BOND

- PERMABOND

- DOPAG

- FINEFINISH

- MG CHEMICALS

- 3M

- VEEYOR POLYMERS

- NAGASE & CO., LTD.

- WACKER CHEMIE AG

- PROSTECH

- MB ENTERPRISES

- ELKEM ASA

- ITW PERFORMANCE POLYMERS

第18章調查方法

第19章附錄

The electronic potting compound market for EV charger is projected to reach USD 0.96 billion by 2032 from USD 0.36 billion in 2025 at a CAGR of 14.9%. AC chargers are increasingly adopting compact, integrated power and control boards, driving demand for low-viscosity potting compounds that ensure complete coverage without affecting heat dissipation.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million), Volume (Tons) |

| Segments | By Charger Type, Setup Type, Material Type, Curing Technology, EV Component, Application |

| Regions covered | Asia Pacific, Europe, North America, Rest of the World |

In DC chargers, the transition toward ultra-fast charging is intensifying the need for high-thermal-conductivity and high-partial-discharge-resistant potting materials. DC charger designs are also moving toward liquid-cooled and sealed power modules, increasing potting thickness and material consumption. Across both charger types, compatibility with automated dispensing and fast thermal curing is becoming a key material requirement. Additionally, materials with long-term resistance to moisture ingress and electrical tracking are gaining importance as outdoor charger deployments expand.

"DC charger is projected to lead the electronic potting compound market for EV charger during the forecast period."

DC chargers are expected to lead the electronic potting compound market for EV chargers during the forecast period due to their significantly higher power density and operating stress compared with AC or onboard chargers. Public DC charging sites and fleet depots operate in harsher environments exposed to moisture, vibration, and continuous duty cycles, which increase demand for robust encapsulation to ensure electrical insulation, environmental protection, and vibration damping. Large-scale infrastructure rollouts by OEMs and charge network operators are prioritizing high-power DC installations along highways, at commercial sites, and within fleet depots, concentrating unit volumes in charger platforms that require heavy and consistent potting usage. Material suppliers such as Parker Hannifin Corp are responding with low viscosity, fast flow thermally conductive potting compounds that can fill narrow gaps and efficiently transfer heat to housings and heat sinks in high power DC modules, while direct injection and pourable systems with faster curing and in-line quality control are gaining traction to support high throughput manufacturing. In parallel, ongoing government backed programs such as the US NEVI (National Electric Vehicle Infrastructure) initiative and China's continued expansion of ultra fast public charging corridors are accelerating the deployment of high power DC chargers. For instance, in August 2025, the California Energy Commission launched a USD 55 million Fast Charge California Program to subsidize public fast charger installations, including high-power DC stations at businesses and public sites. These investments increase demand for thermally robust and electrically reliable potting compounds, as each new high-power DC installation requires substantial encapsulation material to ensure long-term operational stability and regulatory compliance.

"The epoxy material is projected to register the highest growth in the electronic potting compound market for EV charger during the forecast period."

The epoxy segment is projected to register the highest growth in the electronic potting compound market for EV charger during the forecast period. Epoxy resins play a critical role in EV charger potting applications due to their high mechanical strength and structural rigidity, which provide durable protection for sensitive electronic and power components exposed to thermal cycling, vibration, and mechanical shock. They offer excellent electrical insulation and chemical resistance, making them well-suited for high voltage AC/DC conversion and safety-critical functions in both onboard and offboard charging systems. Epoxy potting compounds also deliver strong moisture and contaminant barrier performance, extending the operational life of EV charger electronics across diverse environmental conditions. Their formulation flexibility allows the incorporation of thermally conductive fillers, enabling improved heat dissipation in high-power modules and dense power electronics. In addition, the mature global manufacturing base and well-established supplier ecosystem for epoxy systems support scalability and cost efficiency in EV charger production. There is also growing emphasis on environmentally compliant epoxy formulations with lower VOC emissions and alignment with evolving regulations such as REACH, without sacrificing insulation or durability. For instance, in November 2025, Wevo Chemie introduced flame-retardant, thermally conductive epoxy potting resins designed to meet strict safety standards, such as EN 45545-2 and UL 94 V-0. These materials offer strong resistance to partial discharge and improved flow characteristics, making them suitable for high-voltage and high-performance applications, including advanced EV charger encapsulation.

"Europe is projected to hold a significant share in the electronic potting compound market for EV charger during the forecast period."

Europe is rapidly expanding its EV charging infrastructure with public charger installations exceeding 1.2 million units by the end of 2025 and continued strong growth in fast and ultra-fast charging, driving higher volumes of charger electronics that require potting and encapsulation. Strong regulatory and policy support, most notably the EU's Alternative Fuels Infrastructure Regulation and broader emission reduction targets, mandate widespread deployment of high-power chargers across member states, increasing demand for durable and compliant potting materials. European charger OEMs and charging service providers such as Wallbox are investing heavily in smart, high-density, and ultra-fast charging hubs that integrate complex power and control electronics, benefiting from potting for insulation, thermal management, and environmental protection. The region's strong emphasis on interoperability and safety standards, including CCS implementations with ISO 15118 features, further raises performance and reliability requirements for electronic protection materials, encouraging the use of advanced potting compounds in charger designs. The rapidly increasing share of DC and ultra-fast chargers in public networks is also elevating the need for thermally conductive and mechanically robust potting compounds to manage heat and ensure long-term reliability. At the same time, harmonized interfaces, communication protocols, and safety frameworks across the EU simplify charger platforms and promote consistency in potting material specifications. The region is also home to leading potting compound manufacturers, including Henkel, Electrolube, Demak Group, and ELANTAS.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEM - 20 %, Tier 1 - 70%, and Tier 2 - 10%

- By Designation: C-level - 40%, Directors - 35%, and Others - 25%

- By Region: Asia Pacific - 35%, North America - 35%, Europe - 25%, and Rest of the World - 5%

The electronic potting compound market for EV charger is dominated by major players, including Henkel Corporation (Germany), Dow (US), Parker Hannifin Corp (US), ELANTAS (Germany), and Momentive (US). These companies are expanding their portfolios to strengthen their position in the electronic potting compound market for EV charger.

Research Coverage:

The report covers the electronic potting compound market for EV charger in terms of setup type (wall mount, stationary), charger type (AC charger, DC charger), application (power electronics, HV components, busbars, and sensor relays, PCB and control modules, connector cable IP zones, charging gun, others), material type (polyurethane, epoxy, silicone), curing technology (room temperature cured, thermal cured, UV cured), EV component (electric motor stator, EV battery cells, EV battery cooling system, on-board charger, in-vehicle charging connector, in-vehicle power converter, others), and region. It covers the competitive landscape and company profiles of the significant players in the electronic potting compound market for EV charger.

The study also includes an in-depth competitive analysis of the key market players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the electronic potting compound market for EV charger and their subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

- The report will help market leaders/new entrants with information on various trends in the electronic potting compound market for EV charger based on setup type, charger type, application, material type, curing technology, EV component, and region.

The report provides insight into the following points:

- Analysis of key drivers (rising power density in charger electronics driving demand for high-thermal-conductivity potting materials, tightening electrical safety, insulation, and high-voltage testing standards, expansion of high-power DC fast charging drives advanced thermal cycling and stress-resistant potting requirements), restraints (regulatory tightening on flame-retardant chemistries and additive bans, restrictions on SVHCs under REACH and tightening RoHS scrutiny), opportunities (commercialization of high-thermal-conductivity silicone potting for WBG-enabled power modules, turnkey integration of automated dispensing and advanced potting materials for high-volume EV charger production), and challenges (SiC/GaN high-stress behavior creating new reliability failure modes for existing potting systems, circularity and end-of-life issues limiting high-performance polymer choices)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the electronic potting compound market for EV charger

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the electronic potting compound market for EV charger

- Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players, such as Henkel Corporation (Germany), Dow (US), Parker Hannifin Corp (US), ELANTAS (Germany), and Momentive (US), in the electronic potting compound market for EV charger

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE AND SEGMENTATION

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNITS CONSIDERED

- 1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING ELECTRONIC POTTING COMPOUND MARKET FOR ELECTRIC VEHICLE (EV) CHARGER

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER

- 3.2 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION

- 3.3 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY SETUP TYPE

- 3.4 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE

- 3.5 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY MATERIAL TYPE

- 3.6 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CURING TECHNOLOGY

- 3.7 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY EV COMPONENT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising power density driving demand for high-thermal-conductivity potting materials

- 4.2.1.1.1 Ev charger types and utilization trends, 2026-2032

- 4.2.1.2 Tightening electrical safety, insulation, and high-voltage testing standards

- 4.2.1.3 Expansion of high-power DC fast charging increasing need for stress-resistant and thermal-cycling-stable potting materials

- 4.2.1.1 Rising power density driving demand for high-thermal-conductivity potting materials

- 4.2.2 RESTRAINTS

- 4.2.2.1 Regulatory pressure on flame-retardant chemistries and additive bans

- 4.2.2.2 Restrictions on substances of very high concern (SVHC)

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Commercialization of high-thermal-conductivity silicone potting for WBG-enabled power modules

- 4.2.3.2 Turnkey integration of automated dispensing and advanced potting materials for high-volume electric vehicle charger production

- 4.2.4 CHALLENGES

- 4.2.4.1 High-stress behavior of silicon carbide (SiC)/gallium nitride (GaN) creating new reliability failure modes for existing potting systems

- 4.2.4.2 Circularity and end-of-life issues limiting high-performance polymer choices

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL ELECTRIC VEHICLE CHARGING STATION MARKET

- 5.1.4 TRENDS IN GLOBAL ELECTRIC VEHICLE INDUSTRY

- 5.2 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.3 PRICING ANALYSIS

- 5.3.1 INDICATIVE PRICING ANALYSIS, BY CHARGER TYPE, 2024-2026 (USD/TON)

- 5.3.2 AVERAGE SELLING PRICE TREND FOR CHARGER TYPES, BY REGION, 2024-2026

- 5.3.2.1 Average selling price trend for AC chargers, by region, 2024-2026

- 5.3.2.2 Average selling price trend for DC chargers, by region, 2024-2026

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 CASE STUDY ANALYSIS

- 5.6.1 IMPROVING THERMAL PERFORMANCE AND RELIABILITY OF ELECTRIC VEHICLE ON-BOARD CHARGERS USING LOW-VISCOSITY POLYURETHANE POTTING COMPOUNDS

- 5.6.2 ENHANCING DURABILITY AND RELIABILITY OF ELECTRIC VEHICLE CHARGING CONNECTORS USING ADVANCED POTTING COMPOUNDS

- 5.6.3 MITIGATING THERMAL RUNAWAY IN CYLINDRICAL BATTERY SYSTEMS USING ADVANCED POLYURETHANE POTTING COMPOUNDS

- 5.7 INVESTMENT AND FUNDING SCENARIO

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO (HS CODE 3910)

- 5.8.2 EXPORT SCENARIO (HS CODE 3910)

- 5.8.3 IMPORT SCENARIO (HS CODE 390730)

- 5.8.4 EXPORT SCENARIO (HS CODE 390730)

- 5.9 KEY CONFERENCES AND EVENTS, 2026

- 5.10 INSIGHTS INTO MATERIAL CONSUMPTION PER EV CHARGER

- 5.10.1 POTTING COMPOUND CONSUMPTION PER CHARGER ARCHITECTURE

- 5.11 FUTURE ROADMAP FOR POTTING COMPOUND MATERIALS IN EV CHARGING STATIONS

- 5.11.1 MATERIALS ENABLING HIGHER POWER DENSITY AND ULTRA-FAST CHARGING

- 5.11.2 THERMAL AND ELECTRICAL PERFORMANCE UPGRADES FOR CONTINUOUS OPERATION

- 5.11.3 MANUFACTURING-OPTIMIZED POTTING FOR SCALABLE CHARGER DEPLOYMENT

- 5.11.4 SUSTAINABILITY, REWORKABILITY, AND END-OF-LIFE COMPLIANCE

- 5.12 INSIGHTS INTO PUBLIC ELECTRIC VEHICLE CHARGER SETUP FOR MAJOR MARKETS

- 5.12.1 AC CHARGER

- 5.12.2 DC CHARGER

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 PATENT ANALYSIS

- 6.2 IMPACT OF GENERATIVE AI ON ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER

- 6.2.1 TOP USE CASES AND MARKET POTENTIAL

- 6.2.1.1 High-performance power electronics

- 6.2.1.2 Connector and harness reliability

- 6.2.1.3 Custom compound design

- 6.2.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS

- 6.2.2.1 Generative design in formulation

- 6.2.2.2 AI-driven manufacturing and quality

- 6.2.3 CASE STUDIES RELATED TO AI IMPLEMENTATION

- 6.2.3.1 Accelerating potting compound innovation using AI-driven R&D platforms

- 6.2.3.2 Generative AI for advanced polymer and materials design

- 6.2.3.3 Customized potting compounds for EV power electronics

- 6.2.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT OF MARKET PLAYERS

- 6.2.4.1 Supply chain and services

- 6.2.4.2 Adjacent technologies

- 6.2.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED PROCESS IN ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER

- 6.2.1 TOP USE CASES AND MARKET POTENTIAL

- 6.3 KEY EMERGING TECHNOLOGIES

- 6.3.1 ADVANCED THERMALLY CONDUCTIVE SILICONE TECHNOLOGIES FOR EV CHARGER POWER ELECTRONICS

- 6.3.2 WIDE BANDGAP (WBG) POWER SEMICONDUCTORS

- 6.3.3 LOW-VISCOSITY, VOID-FREE POTTING CHEMISTRIES

- 6.3.4 FAST-CURE AND SNAP-CURE POTTING FORMULATIONS

- 6.4 COMPLEMENTARY TECHNOLOGIES

- 6.4.1 AUTOMATED DISPENSING AND METERING SYSTEMS

- 6.4.2 AL-ENABLED PROCESS MONITORING AND CONTROL

- 6.5 ADJACENT TECHNOLOGIES

- 6.5.1 CONFORMAL COATINGS AND SELECTIVE ENCAPSULATION

- 6.5.2 ADVANCED ADHESIVES AND STRUCTURAL BONDING MATERIALS

- 6.5.3 RECYCLABLE AND DEBONDABLE POLYMER SYSTEMS

- 6.6 TECHNOLOGY/PRODUCT ROADMAP

- 6.6.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.6.2 MID-TERM (2028-2030) | EXPANSION & STANDARDIZATION

- 6.6.3 LONG-TERM (2031-2035+) | MASS COMMERCIALIZATION & DISRUPTION

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2.1 INDUSTRY STANDARDS

- 7.3 SUSTAINABILITY INITIATIVES

- 7.3.1 CARBON IMPACT AND ECO-APPLICATIONS

- 7.3.1.1 Bio-based resins

- 7.3.1.2 Low-VOC, solventless formulations

- 7.3.1.3 Removable (debondable) potting

- 7.3.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.3.1 CARBON IMPACT AND ECO-APPLICATIONS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

9 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE

- 9.1 INTRODUCTION

- 9.2 AC CHARGER

- 9.2.1 INCREASING POWER DENSITY IN COMPACT AC CHARGER DESIGNS TO FUEL GROWTH

- 9.3 DC CHARGER

- 9.3.1 GOVERNMENT-BACKED EXPANSION OF ULTRA-FAST DC CHARGING NETWORKS TO FUEL GROWTH

- 9.4 KEY PRIMARY INSIGHTS

10 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY SETUP TYPE

- 10.1 INTRODUCTION

- 10.2 WALL MOUNT (PRIVATE)

- 10.2.1 EXPANSION OF RESIDENTIAL LEVEL 2 CHARGING INFRASTRUCTURE TO FUEL GROWTH

- 10.3 STATIONARY (PUBLIC)

- 10.3.1 SCALING DEPLOYMENT OF ULTRA-FAST PUBLIC CHARGING HUBS TO FUEL GROWTH

- 10.4 KEY PRIMARY INSIGHTS

11 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY MATERIAL TYPE

- 11.1 INTRODUCTION

- 11.2 POLYURETHANE

- 11.2.1 ADVANCEMENTS IN TWO-COMPONENT POLYURETHANE SYSTEMS FOR EV CHARGER ENCAPSULATION TO FUEL GROWTH

- 11.3 SILICONE

- 11.3.1 SHIFT TOWARD HIGH THERMALLY CONDUCTIVE SILICONE MATERIALS IN ULTRA-FAST CHARGING PLATFORMS TO DRIVE MARKET

- 11.4 EPOXY

- 11.4.1 EXPANSION OF LOW-VOC, REGULATION-COMPLIANT EPOXY FORMULATIONS IN ELECTRIC VEHICLE CHARGING APPLICATIONS TO FUEL GROWTH

- 11.5 KEY PRIMARY INSIGHTS

12 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CURING TECHNOLOGY

- 12.1 INTRODUCTION

- 12.2 ROOM TEMPERATURE CURED

- 12.2.1 EXPANSION OF TWO-COMPONENT ROOM-TEMPERATURE-CURED SYSTEMS IN AC AND DC CHARGERS TO FUEL GROWTH

- 12.3 THERMAL CURED

- 12.3.1 HIGHER POWER RATINGS AND SIC INTEGRATION ACCELERATING USE OF THERMALLY CURED POTTING COMPOUNDS

- 12.4 UV CURED

- 12.4.1 EXPANSION OF HYBRID UV CURING SYSTEMS IN COMPACT AND SMART CHARGER DESIGNS TO FUEL GROWTH

- 12.5 KEY PRIMARY INSIGHTS

13 ELECTRONIC POTTING COMPOUND MARKET, BY EV COMPONENT

- 13.1 INTRODUCTION

- 13.2 ELECTRIC MOTOR STATOR

- 13.2.1 SHIFT TOWARD HIGH-DENSITY DRIVE UNITS STRENGTHENING NEED FOR RELIABLE STATOR ENCAPSULATION

- 13.3 EV BATTERY CELL

- 13.3.1 INCREASING FOCUS ON THERMAL RUNAWAY MITIGATION IN ELECTRIC VEHICLE BATTERIES TO DRIVE MARKET

- 13.4 EV BATTERY COOLING SYSTEM

- 13.4.1 RISING ADOPTION OF CELL-TO-PACK AND CELL-TO-CHASSIS ARCHITECTURES TO BOOST ENCAPSULATION DEMAND

- 13.5 ON-BOARD CHARGER

- 13.5.1 GROWING INTEGRATION OF MULTI-FUNCTIONAL OBC AND DC-DC UNITS TO DRIVE DEMAND

- 13.6 IN-VEHICLE CHARGING CONNECTOR

- 13.6.1 RISING ADOPTION OF HIGH-CURRENT, COMPACT EV CHARGING CONNECTORS TO FUEL GROWTH

- 13.7 IN-VEHICLE POWER CONVERTER

- 13.7.1 RISING INTEGRATION OF MULTIPLE POWER-ELECTRONICS FUNCTIONS TO FUEL GROWTH

- 13.8 OTHERS

- 13.9 KEY PRIMARY INSIGHTS

14 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY APPLICATION

- 14.1 INTRODUCTION

- 14.2 POWER ELECTRONICS

- 14.3 HV COMPONENTS, BUSBARS, AND SENSOR RELAYS

- 14.4 PCB AND CONTROL MODULES

- 14.5 CONNECTOR CABLE IP ZONES

- 14.6 CHARGING GUNS

- 14.7 OTHERS

15 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION

- 15.1 INTRODUCTION

- 15.2 ASIA PACIFIC

- 15.2.1 CHINA

- 15.2.1.1 Presence of well-established domestic manufacturing ecosystem for chargers, power electronics, and materials to drive market

- 15.2.2 INDIA

- 15.2.2.1 Growing localization of EV charger manufacturing under "Make in India" initiative to fuel growth

- 15.2.3 JAPAN

- 15.2.3.1 Increasing installation of high-output EV chargers under Japan's 2030 targets to drive market

- 15.2.4 SOUTH KOREA

- 15.2.4.1 Government-backed deployment of ultra-fast charging networks to fuel growth

- 15.2.5 THAILAND

- 15.2.5.1 Rapid deployment of high-power DC fast chargers to drive market

- 15.2.6 INDONESIA

- 15.2.6.1 Rapid deployment of public EV charging stations and local manufacturing to drive market

- 15.2.7 SINGAPORE

- 15.2.7.1 Deployment of compact, high-density public EV charging systems to drive market

- 15.2.1 CHINA

- 15.3 EUROPE

- 15.3.1 AUSTRIA

- 15.3.1.1 Strategic investment in high-power EV charging under eMove Austria to fuel growth

- 15.3.2 DENMARK

- 15.3.2.1 Acceleration of residential and public EV charger installations under regulatory reforms to drive market

- 15.3.3 FRANCE

- 15.3.3.1 Fleet-focused charging rollouts and OEM-led infrastructure expansion to drive market

- 15.3.4 GERMANY

- 15.3.4.1 Expansion of multi-family residential and corridor charging infrastructure to drive market

- 15.3.5 NETHERLANDS

- 15.3.5.1 High per-capita EV charger installations to drive market

- 15.3.6 NORWAY

- 15.3.6.1 Expansion of highway DC fast-charging corridors to drive market

- 15.3.7 SPAIN

- 15.3.7.1 Government-backed expansion of corridor and rural EV charging networks to fuel growth

- 15.3.8 SWEDEN

- 15.3.8.1 Megawatt charging corridor development to drive high-power charger installations

- 15.3.9 SWITZERLAND

- 15.3.9.1 Subsidized deployment of high-power fleet charging systems to drive market

- 15.3.10 UK

- 15.3.10.1 Government-backed expansion of motorway super hubs and depot charging to fuel growth

- 15.3.1 AUSTRIA

- 15.4 NORTH AMERICA

- 15.4.1 US

- 15.4.1.1 Strategic OEM partnerships and high-voltage charger rollouts to drive market

- 15.4.2 CANADA

- 15.4.2.1 Government-backed rollout of EV chargers to drive market

- 15.4.3 MEXICO

- 15.4.3.1 Strategic rollout of retail and commercial charging sites to fuel growth

- 15.4.1 US

- 15.5 REST OF THE WORLD

- 15.5.1 BRAZIL

- 15.5.1.1 Policy-backed residential charging access expansion in multi-unit buildings to fuel growth

- 15.5.2 UAE

- 15.5.2.1 Scaling fleet-focused and destination DC fast charging networks to drive market

- 15.5.1 BRAZIL

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 16.3 MARKET SHARE ANALYSIS OF EV CHARGER POTTING COMPOUND MANUFACTURERS, 2025

- 16.4 REVENUE ANALYSIS OF TOP LISTED/PUBLIC PLAYERS, 2020-2024

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS, 2026

- 16.5.1 COMPANY VALUATION

- 16.5.2 FINANCIAL METRICS

- 16.6 BRAND/ PRODUCT COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2026

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2026

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Charger type footprint

- 16.7.5.4 Material type footprint

- 16.7.5.5 Setup type footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2026

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2026

- 16.8.5.1 List of startups/SMEs

- 16.8.5.2 Competitive benchmarking of startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 HENKEL CORPORATION

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 PARKER HANNIFIN CORP

- 17.1.2.1 Business overview

- 17.1.2.2 Product offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Other developments

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 ELANTAS

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 MnM view

- 17.1.3.3.1 Key strengths

- 17.1.3.3.2 Strategic choices

- 17.1.3.3.3 Weaknesses and competitive threats

- 17.1.4 DOW

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Other developments

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 MOMENTIVE

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 MnM view

- 17.1.5.3.1 Key strengths

- 17.1.5.3.2 Strategic choices

- 17.1.5.3.3 Weaknesses and competitive threats

- 17.1.6 ELECTROLUBE

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Other developments

- 17.1.7 DEMAK GROUP

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.8 WEVO-CHEMIE GMBH

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.9 EPOXIES, ETC.

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.10 RAMPF

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Expansions

- 17.1.10.3.2 Other developments

- 17.1.11 KISLING

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Deals

- 17.1.12 SIKA AUTOMOTIVE

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.1 HENKEL CORPORATION

- 17.2 OTHER PLAYERS

- 17.2.1 MASTER BOND

- 17.2.2 PERMABOND

- 17.2.3 DOPAG

- 17.2.4 FINEFINISH

- 17.2.5 MG CHEMICALS

- 17.2.6 3M

- 17.2.7 VEEYOR POLYMERS

- 17.2.8 NAGASE & CO., LTD.

- 17.2.9 WACKER CHEMIE AG

- 17.2.10 PROSTECH

- 17.2.11 MB ENTERPRISES

- 17.2.12 ELKEM ASA

- 17.2.13 ITW PERFORMANCE POLYMERS

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of key secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Primary interview participants

- 18.1.2.2 Key industry insights and breakdown of primary interviews

- 18.1.2.3 List of primary interview participants

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.2 TOP-DOWN APPROACH

- 18.3 DATA TRIANGULATION

- 18.4 FACTOR ANALYSIS

- 18.4.1 DEMAND- AND SUPPLY-SIDE FACTOR ANALYSIS

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RESEARCH LIMITATIONS

- 18.7 RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.3.1 BREAKDOWN OF ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY SETUP TYPE, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 19.3.2 COMPANY INFORMATION:

- 19.3.2.1 Profiling of additional market players (up to 5)

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS

List of Tables

- TABLE 1 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: DEFINITION OF CHARGER TYPES

- TABLE 2 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: DEFINITION OF SETUP TYPES

- TABLE 3 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: DEFINITION OF MATERIAL TYPES

- TABLE 4 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: DEFINITION OF CURING TECHNOLOGIES

- TABLE 5 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: DEFINITION OF EV COMPONENTS

- TABLE 6 USD EXCHANGE RATES, 2021-2025

- TABLE 7 EV CHARGER TYPES AND UTILIZATION TRENDS, 2026-2032

- TABLE 8 ELECTRIC VEHICLE CHARGING INCENTIVES, BY COUNTRY

- TABLE 9 IMPACT OF MARKET DYNAMICS ON ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER

- TABLE 10 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2030

- TABLE 11 INDICATIVE PRICING ANALYSIS, BY CHARGER TYPE, 2024-2026 (USD/TON)

- TABLE 12 AVERAGE SELLING PRICE TREND FOR AC CHARGERS, BY REGION, 2024-2026 (USD/TON)

- TABLE 13 AVERAGE SELLING PRICE TREND FOR DC CHARGERS, BY REGION, 2024-2026 (USD/TON)

- TABLE 14 ELECTRONIC COMPOUND MARKET FOR EV CHARGER: ROLE OF COMPANIES IN MARKET ECOSYSTEM

- TABLE 15 IMPORT DATA FOR HS CODE 3910, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 16 EXPORT DATA FOR HS CODE 3910, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 17 IMPORT DATA FOR HS CODE 390730, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 18 EXPORT DATA FOR HS CODE 390730, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 19 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: KEY CONFERENCES AND EVENTS, 2026

- TABLE 20 POTTING COMPOUND CONSUMPTION PER CHARGER ARCHITECTURE (IN GRAMS)

- TABLE 21 AC CHARGER SETUP, BY KEY COUNTRIES, 2025

- TABLE 22 DC CHARGER SETUP, BY KEY COUNTRIES, 2025

- TABLE 23 PATENT ANALYSIS, 2025

- TABLE 24 POTTING MATERIAL COMPARISON

- TABLE 25 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 26 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 27 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 28 GLOBAL INDUSTRY STANDARDS, BY COUNTRY/REGION

- TABLE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF POTTING COMPOUND IN EV CHARGERS, BY CHARGER TYPE (%)

- TABLE 30 KEY BUYING CRITERIA FOR POTTING COMPOUND IN EV CHARGERS, BY CHARGER TYPE

- TABLE 31 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 32 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 33 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 34 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 35 AC CHARGER: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 36 AC CHARGER: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 37 AC CHARGER: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (USD MILLION)

- TABLE 38 AC CHARGER: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (USD MILLION)

- TABLE 39 DC CHARGER: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 40 DC CHARGER: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 41 DC CHARGER: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (USD MILLION)

- TABLE 42 DC CHARGER: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (USD MILLION)

- TABLE 43 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY SETUP TYPE, 2021-2024 (TONS)

- TABLE 44 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY SETUP TYPE, 2025-2032 (TONS)

- TABLE 45 WALL MOUNT (PRIVATE): ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 46 WALL MOUNT (PRIVATE): ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 47 STATIONARY (PUBLIC): ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 48 STATIONARY (PUBLIC): ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 49 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY MATERIAL TYPE, 2021-2024 (TONS)

- TABLE 50 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY MATERIAL TYPE, 2025-2032 (TONS)

- TABLE 51 POLYURETHANE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 52 POLYURETHANE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 53 SILICONE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 54 SILICONE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 55 EPOXY: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 56 EPOXY: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 57 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CURING TECHNOLOGY, 2021-2024 (TONS)

- TABLE 58 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CURING TECHNOLOGY, 2025-2032 (TONS)

- TABLE 59 ROOM TEMPERATURE CURED: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 60 ROOM TEMPERATURE CURED: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 61 THERMAL CURED: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 62 THERMAL CURED: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 63 UV CURED: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 64 UV CURED: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 65 ELECTRONIC POTTING COMPOUND MARKET, BY EV COMPONENT, 2021-2024 (TONS)

- TABLE 66 ELECTRONIC POTTING COMPOUND MARKET, BY EV COMPONENT, 2025-2032 (TONS)

- TABLE 67 ELECTRIC MOTOR STATOR: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2021-2024 (KILOS)

- TABLE 68 ELECTRIC MOTOR STATOR: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2025-2032 (KILOS)

- TABLE 69 EV BATTERY CELL: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2021-2024 (KILOS)

- TABLE 70 EV BATTERY CELL: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2025-2032 (KILOS)

- TABLE 71 EV BATTERY COOLING SYSTEM: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2021-2024 (KILOS)

- TABLE 72 EV BATTERY COOLING SYSTEM: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2025-2032 (KILOS)

- TABLE 73 ON-BOARD CHARGER: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2021-2024 (KILOS)

- TABLE 74 ON-BOARD CHARGER: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2025-2032 (KILOS)

- TABLE 75 IN-VEHICLE CHARGING CONNECTOR: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2021-2024 (KILOS)

- TABLE 76 IN-VEHICLE CHARGING CONNECTOR: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2025-2032 (KILOS)

- TABLE 77 IN-VEHICLE POWER CONVERTER: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2021-2024 (KILOS)

- TABLE 78 IN-VEHICLE POWER CONVERTER: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2025-2032 (KILOS)

- TABLE 79 OTHERS: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2021-2024 (KILOS)

- TABLE 80 OTHERS: ELECTRONIC POTTING COMPOUND MARKET, BY REGION, 2025-2032 (KILOS)

- TABLE 81 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (TONS)

- TABLE 82 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (TONS)

- TABLE 83 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2021-2024 (USD MILLION)

- TABLE 84 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025-2032 (USD MILLION)

- TABLE 85 ASIA PACIFIC: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2021-2024 (TONS)

- TABLE 86 ASIA PACIFIC: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2025-2032 (TONS)

- TABLE 87 ASIA PACIFIC: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 88 ASIA PACIFIC: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 89 CHINA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 90 CHINA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 91 CHINA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 92 CHINA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 93 INDIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 94 INDIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 95 INDIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 96 INDIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 97 JAPAN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 98 JAPAN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 99 JAPAN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 100 JAPAN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 101 SOUTH KOREA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 102 SOUTH KOREA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 103 SOUTH KOREA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 104 SOUTH KOREA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 105 THAILAND: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 106 THAILAND: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 107 THAILAND: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 108 THAILAND: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 109 INDONESIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 110 INDONESIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 111 INDONESIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 112 INDONESIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 113 SINGAPORE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 114 SINGAPORE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 115 SINGAPORE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 116 SINGAPORE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 117 EUROPE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2021-2024 (TONS)

- TABLE 118 EUROPE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2025-2032 (TONS)

- TABLE 119 EUROPE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 120 EUROPE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 121 AUSTRIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 122 AUSTRIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 123 AUSTRIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 124 AUSTRIA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 125 DENMARK: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 126 DENMARK: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 127 DENMARK: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 128 DENMARK: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 129 FRANCE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 130 FRANCE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 131 FRANCE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 132 FRANCE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 133 GERMANY: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 134 GERMANY: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 135 GERMANY: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 136 GERMANY: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 137 NETHERLANDS: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 138 NETHERLANDS: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 139 NETHERLANDS: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 140 NETHERLANDS: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 141 NORWAY: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 142 NORWAY: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 143 NORWAY: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 144 NORWAY: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 145 SPAIN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 146 SPAIN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 147 SPAIN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 148 SPAIN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 149 SWEDEN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 150 SWEDEN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 151 SWEDEN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 152 SWEDEN: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 153 SWITZERLAND: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 154 SWITZERLAND: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 155 SWITZERLAND: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 156 SWITZERLAND: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 157 UK: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 158 UK: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 159 UK: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 160 UK: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 161 NORTH AMERICA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2021-2024 (TONS)

- TABLE 162 NORTH AMERICA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2025-2032 (TONS)

- TABLE 163 NORTH AMERICA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 164 NORTH AMERICA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 165 US: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 166 US: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 167 US: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 168 US: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 169 CANADA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 170 CANADA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 171 CANADA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 172 CANADA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 173 MEXICO: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 174 MEXICO: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 175 MEXICO: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 176 MEXICO: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 177 REST OF THE WORLD: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2021-2024 (TONS)

- TABLE 178 REST OF THE WORLD: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2025-2032 (TONS)

- TABLE 179 REST OF THE WORLD: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 180 REST OF THE WORLD: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 181 BRAZIL: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 182 BRAZIL: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 183 BRAZIL: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 184 BRAZIL: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 185 UAE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (TONS)

- TABLE 186 UAE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (TONS)

- TABLE 187 UAE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2021-2024 (USD MILLION)

- TABLE 188 UAE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025-2032 (USD MILLION)

- TABLE 189 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2026

- TABLE 190 MARKET SHARE ANALYSIS OF TOP 5 PLAYERS, 2025

- TABLE 191 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: REGION FOOTPRINT, 2026

- TABLE 192 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: CHARGER TYPE FOOTPRINT, 2026

- TABLE 193 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: MATERIAL TYPE FOOTPRINT, 2026

- TABLE 194 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: SETUP TYPE FOOTPRINT, 2026

- TABLE 195 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: LIST OF KEY STARTUPS/SMES

- TABLE 196 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 197 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: PRODUCT LAUNCHES, JANUARY 2021-FEBRUARY 2026

- TABLE 198 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: DEALS, JANUARY 2021-FEBRUARY 2026

- TABLE 199 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: EXPANSIONS, JANUARY 2021-FEBRUARY 2026

- TABLE 200 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: OTHER DEVELOPMENTS, JANUARY 2021- FEBRUARY 2026

- TABLE 201 HENKEL CORPORATION: COMPANY OVERVIEW

- TABLE 202 HENKEL CORPORATION: PRODUCTS OFFERED

- TABLE 203 HENKEL CORPORATION: POTTING PRODUCT PORTFOLIO

- TABLE 204 HENKEL CORPORATION: PRODUCT LAUNCHES

- TABLE 205 PARKER HANNIFIN CORP: COMPANY OVERVIEW

- TABLE 206 PARKER HANNIFIN CORP: PRODUCTS OFFERED

- TABLE 207 PARKER HANNIFIN CORP: POTTING & ENCAPSULANTS PORTFOLIO

- TABLE 208 PARKER HANNIFIN CORP: OTHER DEVELOPMENTS

- TABLE 209 ELANTAS: COMPANY OVERVIEW

- TABLE 210 ELANTAS: PRODUCTS OFFERED

- TABLE 211 DOW: COMPANY OVERVIEW

- TABLE 212 DOW: PRODUCTS OFFERED

- TABLE 213 DOW: PRODUCT LAUNCHES

- TABLE 214 DOW: OTHER DEVELOPMENTS

- TABLE 215 MOMENTIVE: COMPANY OVERVIEW

- TABLE 216 MOMENTIVE: PRODUCTS OFFERED

- TABLE 217 ELECTROLUBE: COMPANY OVERVIEW

- TABLE 218 ELECTROLUBE: PRODUCTS OFFERED

- TABLE 219 ELECTROLUBE: OTHER DEVELOPMENTS

- TABLE 220 DEMAK GROUP: COMPANY OVERVIEW

- TABLE 221 DEMAK GROUP: PRODUCTS OFFERED

- TABLE 222 WEVO-CHEMIE GMBH: COMPANY OVERVIEW

- TABLE 223 WEVO-CHEMIE GMBH: PRODUCTS OFFERED

- TABLE 224 WEVO-CHEMIE GMBH: SOLUTIONS FOR EV CHARGING

- TABLE 225 WEVO-CHEMIE GMBH: PRODUCT LAUNCHES

- TABLE 226 EPOXIES, ETC.: COMPANY OVERVIEW

- TABLE 227 EPOXIES, ETC.: PRODUCTS OFFERED

- TABLE 228 RAMPF: COMPANY OVERVIEW

- TABLE 229 RAMPF: PRODUCTS OFFERED

- TABLE 230 RAMPF: EXPANSIONS

- TABLE 231 RAMPF: OTHER DEVELOPMENTS

- TABLE 232 KISLING: COMPANY OVERVIEW

- TABLE 233 KISLING: PRODUCTS OFFERED

- TABLE 234 KISLING: DEALS

- TABLE 235 SIKA AUTOMOTIVE: COMPANY OVERVIEW

- TABLE 236 SIKA AUTOMOTIVE: PRODUCTS OFFERED

List of Figures

- FIGURE 1 MARKET SCENARIO

- FIGURE 2 GLOBAL ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, 2021-2032

- FIGURE 3 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, 2021-2025

- FIGURE 4 DISRUPTIONS INFLUENCING GROWTH OF ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER

- FIGURE 5 HIGH-GROWTH SEGMENTS IN ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, 2025-2032

- FIGURE 6 ASIA PACIFIC TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 7 GROWTH IN HIGH-POWER EV CHARGER INSTALLATIONS REQUIRING INSULATION AND THERMAL PROTECTION TO DRIVE MARKET

- FIGURE 8 ASIA PACIFIC ACCOUNTED FOR LARGEST MARKET SHARE IN 2025

- FIGURE 9 STATIONARY TO BE FASTER-GROWING SEGMENT THAN WALL MOUNT DURING FORECAST PERIOD

- FIGURE 10 DC CHARGER SEGMENT TO LEAD MARKET IN 2032

- FIGURE 11 EPOXY SEGMENT TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 12 THERMAL CURED SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2032

- FIGURE 13 EV BATTERY CELL SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2032

- FIGURE 14 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 15 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 16 INDICATIVE PRICING ANALYSIS, BY CHARGER TYPE, 2024-2026 (USD/TON)

- FIGURE 17 AVERAGE SELLING PRICE TREND FOR AC CHARGERS, BY REGION, 2024-2026 (USD/TON)

- FIGURE 18 AVERAGE SELLING PRICE TREND FOR DC CHARGERS, BY REGION, 2024-2026 (USD/TON)

- FIGURE 19 ELECTRONIC COMPOUND MARKET FOR EV CHARGER ECOSYSTEM

- FIGURE 20 SUPPLY CHAIN ANALYSIS

- FIGURE 21 INVESTMENT AND FUNDING SCENARIO, 2022-2025

- FIGURE 22 IMPORT DATA FOR HS CODE 3910, BY COUNTRY, 2021-2024 (USD MILLION)

- FIGURE 23 EXPORT DATA FOR HS CODE 3910, BY COUNTRY, 2021-2024 (USD MILLION)

- FIGURE 24 IMPORT DATA FOR HS CODE 390730, BY COUNTRY, 2021-2024 (USD MILLION)

- FIGURE 25 EXPORT DATA FOR HS CODE 390730, BY COUNTRY, 2021-2024 (USD MILLION)

- FIGURE 26 PATENT ANALYSIS, 2016-2025

- FIGURE 27 LEGAL STATUS OF PATENTS, 2016-2025

- FIGURE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF POTTING COMPOUND IN EV CHARGER, BY CHARGER TYPE

- FIGURE 29 KEY BUYING CRITERIA FOR POTTING COMPOUND IN EV CHARGER, BY CHARGER TYPE

- FIGURE 30 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CHARGER TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 31 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY SETUP TYPE, 2025 VS. 2032 (TONS)

- FIGURE 32 EV POTTING COMPOUND MATERIAL, BY TEMPERATURE RESISTANCE

- FIGURE 33 EV POTTING COMPOUND MATERIAL, BY FLEXIBILITY AND MECHANICAL STRENGTH

- FIGURE 34 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY MATERIAL TYPE, 2025 VS. 2032 (TONS)

- FIGURE 35 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY CURING TECHNOLOGY, 2025 VS. 2032 (TONS)

- FIGURE 36 ELECTRONIC POTTING COMPOUND MARKET, BY EV COMPONENT, 2025 VS. 2032 (TONS)

- FIGURE 37 EV MOTOR POTTING COMPOUND, THERMALLY CONDUCTIVE

- FIGURE 38 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY REGION, 2025 VS. 2032 (USD MILLION)

- FIGURE 39 ASIA PACIFIC: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER SNAPSHOT

- FIGURE 40 EUROPE: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2025 VS. 2032 (USD MILLION)

- FIGURE 41 NORTH AMERICA: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER SNAPSHOT

- FIGURE 42 REST OF THE WORLD: ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER, BY COUNTRY, 2025 VS. 2032 (USD MILLION)

- FIGURE 43 MARKET SHARE ANALYSIS OF TOP EV CHARGER POTTING COMPOUND MANUFACTURERS, 2025

- FIGURE 44 REVENUE ANALYSIS OF TOP LISTED MARKET PLAYERS, 2020-2024

- FIGURE 45 COMPANY VALUATION OF TOP LISTED PLAYERS, 2026 (USD BILLION)

- FIGURE 46 FINANCIAL METRICS OF TOP-LISTED PLAYERS, 2026

- FIGURE 47 BRAND COMPARISON OF TOP 5 PLAYERS

- FIGURE 48 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2026

- FIGURE 49 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: COMPANY FOOTPRINT, 2026

- FIGURE 50 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: STARTUP/SME EVALUATION MATRIX, 2026

- FIGURE 51 HENKEL CORPORATION: COMPANY SNAPSHOT

- FIGURE 52 HENKEL CORPORATION: APPLICATION OF POTTING IN CHARGING CONNECTORS

- FIGURE 53 PARKER HANNIFIN CORP: COMPANY SNAPSHOT

- FIGURE 54 ELANTAS: COMPANY SNAPSHOT

- FIGURE 55 DOW: COMPANY SNAPSHOT

- FIGURE 56 RESEARCH DESIGN

- FIGURE 57 RESEARCH PROCESS FLOW

- FIGURE 58 KEY INSIGHTS FROM INDUSTRY EXPERTS

- FIGURE 59 BREAKDOWN OF PRIMARY INTERVIEWS

- FIGURE 60 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 61 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: BOTTOM-UP APPROACH

- FIGURE 62 ELECTRONIC POTTING COMPOUND MARKET FOR EV CHARGER: TOP-DOWN APPROACH

- FIGURE 63 DATA TRIANGULATION

- FIGURE 64 MARKET GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS AND OPPORTUNITIES

灌封膠市場-全球產業規模、佔有率、趨勢、機會與預測,依產品、技術、應用、最終用途、地區和競爭細分,2020-2030 年預測

灌封膠市場-全球產業規模、佔有率、趨勢、機會與預測,依產品、技術、應用、最終用途、地區和競爭細分,2020-2030 年預測 灌封膠市場規模、佔有率和趨勢分析報告:按產品、按技術、按最終用途、按地區、細分市場預測,2024-2030 年

灌封膠市場規模、佔有率和趨勢分析報告:按產品、按技術、按最終用途、按地區、細分市場預測,2024-2030 年