|

市場調查報告書

商品編碼

1893727

全球文件人工智慧市場(至 2030 年):按產品(身分提供者、文件工作流程自動化、生成式人工智慧文件產生、企業內容管理、管治工具)和用例(合規報告、客戶回饋、KYC 文件、RFP 回應、採購訂單)分類Document AI Market by Offering (IDP, Document Workflow Automation, Generative AI Document Generation, ECM, and Governance Tools), Use Case (Compliance Reports, Customer Feedback, KYC Document, RFP Responses, Purchase Orders) - Global Forecast to 2030 |

||||||

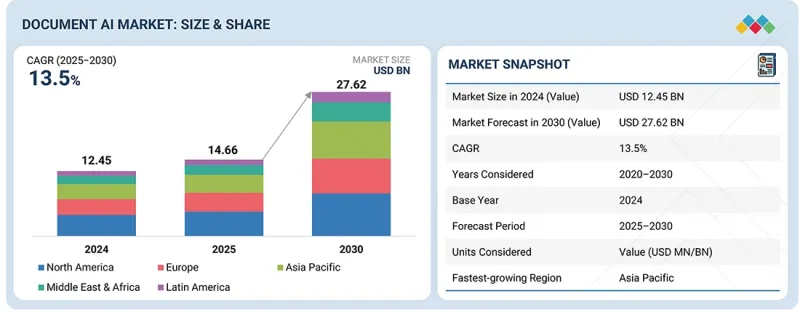

全球文檔人工智慧市場預計將從 2025 年的 146.6 億美元成長到 2030 年的 276.2 億美元,預測期內複合年成長率為 13.5%。

| 調查範圍 | |

|---|---|

| 調查期 | 2020-2030 |

| 基準年 | 2024 |

| 預測期 | 2025-2030 |

| 單元 | 美元 |

| 部分 | 產品類別、文件類型、使用案例、產業、地區 |

| 目標區域 | 北美洲、歐洲、亞太地區、中東和非洲、拉丁美洲 |

隨著自適應文件學習模型能夠使系統透過即時使用者回饋進行自我改進,從而減少人工重新訓練的需求並提高對各種文件格式的識別準確率,市場正在蓬勃發展。基於圖的文檔智慧還能透過連結多頁文件中的實體和關係來增強上下文理解,這在法律、保險和合規營運中尤其重要。然而,各行業文件資料格式標準化程度有限,阻礙了互通性,也妨礙了模型的大規模大規模部署。

“透過提供 IDP 解決方案,隨著企業優先考慮端到端自動化和合規資料處理,IDP 解決方案在市場主導。”

智慧型文件處理 (IDP) 解決方案有望佔據最大的市場佔有率,因為它們能夠實現非結構化和半結構化文件工作流程的完全自動化。 IDP 平台整合了 OCR、NLP 和機器學習技術,能夠高精度地從發票、表單、合約和合規文件中提取、分類和檢驗資料。銀行、保險和醫療保健等行業的企業正在採用 IDP 來加快文件處理速度、減少手動資料輸入並維護符合審核要求的數位化記錄。遠距辦公的快速發展和無紙化流程的推進進一步推動了對雲端基礎的IDP 平台的需求。 UiPath、ABBYY 和 Kofax 等供應商正在透過生成式人工智慧、RPA 整合和特定領域的預訓練模型來增強其 IDP 解決方案,從而實現快速部署和高投資回報率。此外,對可解釋人工智慧和資料沿襲功能日益成長的需求,以及與監管合規性要求一致的需求,正在鞏固 IDP 作為企業級文件自動化基礎的地位。

“隨著企業擴大實現複雜、海量內容處理的自動化,非結構化文件正在推動文件類型市場的發展。”

按文檔類型分類,非結構化文件預計將佔據最大的市場佔有率。這反映出處理電子郵件、合約、報告、手寫筆記和多媒體記錄等沒有固定範本的文件的需求日益成長。在銀行、醫療保健和政府等行業,大量企業資料仍然是非結構化的,這催生了對能夠理解各種文件格式的高級人工智慧模型的巨大需求。佈局感知變壓器、多模態人工智慧和自然語言理解的最新進展,使得文件人工智慧系統能夠同時從文字、表格和圖像中準確提取上下文資訊。 Google、微軟和AWS等供應商正在擴展其處理多格式文件的解決方案,利用針對特定產業進行微調的預訓練模型。合規主導的自動化和資料管治要求,尤其是在審核追蹤和客戶溝通領域,也在加速非結構化文件處理技術的應用。隨著各組織致力於將傳統檔案數位化並建立搜尋的文件庫,非結構化文件智慧已成為推動大規模數位生態系統效率提升、決策改進和監管透明度的核心技術。

“亞太地區在創新和不斷發展的戰略驅動下經歷了快速成長,而北美則保持了主導地位。”

文件人工智慧市場在不同地區差異顯著,亞太地區預計將實現最高成長率,這主要得益於印度、印尼和越南等國家在「數位印度」和日本「社會5.0」等國家舉措的支持下,正經歷著快速的數位轉型。對多語言OCR和自然語言處理能力的需求,正推動企業加強對雲端基礎人工智慧和識別解決方案的投資,以實現銀行、金融和保險(BFSI)、醫療保健、物流和政府部門的工作流程自動化。金融科技、數位支付和電子化管治的興起,也推動了合規、客戶註冊和身份驗證等方面的文件自動化需求。

同時,由於北美擁有先進的基礎設施、早期應用以及Google、微軟、AWS、IBM 和 Adobe 等廠商的存在,預計到 2025 年,北美將引領市場。 HIPAA、SOX 和 GDPR 等嚴格的法規正在推動人工智慧驅動的合規和審核解決方案的普及,這些解決方案利用人工智慧進行分類、合約分析和理賠處理,尤其是在金融、保險和醫療保健行業。生成式人工智慧、紅黃綠 (RAG) 和可解釋性模型的整合正在提高文件的準確性和可理解性。因此,北美的創新與亞太地區的數位成長正在塑造全球文檔人工智慧格局,並推動市場擴張。

本報告調查了全球文件人工智慧市場,並提供了市場概覽、影響市場成長的各種因素分析、技術和專利趨勢、法律制度、案例研究、市場規模趨勢和預測、按各個細分市場、地區/主要國家/地區進行的詳細分析、競爭格局以及主要企業的概況。

目錄

第1章 引言

第2章調查方法

第3章執行摘要

第4章重要考察

第5章 市場概覽

- 市場動態

- 促進要素

- 抑制因素

- 機會

- 任務

- 未滿足的需求和閒置頻段

- 與相關市場和不同產業相關的跨領域機遇

- 一級/二級/三級公司的策略性舉措

- 從文件處理到企業知識智慧

- 向自主文件工作流程過渡

- 人工智慧管治與倫理考量文件 人工智慧實施

第6章 產業趨勢

- 波特五力分析

- 供應鏈分析

- 文檔人工智慧的演變

- 生態系分析

- 定價分析

- 投資和資金籌措方案

- 案例研究分析

- 2025-2026 年重要會議與活動

- 影響您業務的趨勢/顛覆性因素

第7章:技術進步、人工智慧影響、專利、創新與未來應用

- 關鍵新興技術

- OCR

- NLP

- 電腦視覺

- 神經網路

- LLM(大規模語言模型)

- 知識圖譜

- 互補技術

- RPA

- 雲端運算

- 數據標註和標記

- 網路安全

- 資料庫和資料湖技術

- 鄰近技術

- 語音轉文字和語音辨識

- 數位身份檢驗

- 區塊鏈

- IoT

- 擴增實境和虛擬實境(AR/VR)

- 專利分析

- 未來應用

第8章:監理環境

- 地方法規和合規性

第9章:顧客狀況與購買行為

- 決策流程

- 採購相關利益者和採購評估標準

- 招募障礙和內部挑戰

- 各個終端用戶產業中尚未滿足的需求

- 市場盈利

第10章 依服務類別分類的文檔人工智慧市場

- 解決方案

- IDP

- 文件工作流程自動化

- 生成式人工智慧文件生成

- 企業內容管理 (ECM) 與管治工具

- 服務

- 專業服務

- 託管服務

- 部署模式

- 雲

- 本地部署

第11章 依文檔類型分類的文檔人工智慧市場

- 結構化

- 非結構化

- 半結構化

- 多模態/混合內容

第12章:按用例分類的文檔人工智慧市場

- 財會

- 發票和稅務文件

- 收據和退款申請

- 銀行對帳單

- 財務報告和監管文件

- 費用報告

- 其他

- 人力資源

- 履歷/CVS

- 入職文件

- 薪資核算

- 政策文件

- 其他

- 法律與合規

- 合約

- 協定

- NDA

- 監管文件

- 合規報告

- 其他

- 客戶服務

- KYC文件

- 發票

- 客戶回饋

- 服務請求

- 其他

- 行銷與銷售

- 提案

- RFP回覆表

- 調查結果

- 宣傳活動資料

- 其他

- 供應鏈與物流

- 採購訂單

- 交貨

- 載貨證券

- 出貨單

- 其他

第13章 按產業分類的文檔人工智慧市場

- BFSI

- 運輸/物流

- 醫療保健與生命科學

- 政府和公共部門

- 零售與電子商務

- 製造業

- 能源與公共產業

- 電訊

- 教育

- 其他

第14章 各地區人工智慧市場文檔

- 北美洲

- 市場促進因素

- 宏觀經濟展望

- 美國

- 加拿大

- 歐洲

- 市場促進因素

- 宏觀經濟展望

- 英國

- 德國

- 法國

- 義大利

- 其他

- 亞太地區

- 市場促進因素

- 宏觀經濟展望

- 中國

- 印度

- 日本

- 韓國

- 新加坡

- 其他

- 中東和非洲

- 市場促進因素

- 宏觀經濟展望

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 卡達

- 其他

- 拉丁美洲

- 市場促進因素

- 宏觀經濟展望

- 巴西

- 墨西哥

- 其他

第15章 競爭格局

- 概述

- 主要參與企業的策略/優勢

- 收入分析

- 市佔率分析

- 產品對比

- 估值和財務指標

- 公司評估矩陣:主要企業

- 公司估值矩陣:Start-Ups/中小企業

- 競爭場景

第16章:公司簡介

- 智慧型文檔處理

- 主要企業

- 其他公司

- 生成式人工智慧文件生成

- 主要企業

第17章:鄰近及相關市場

第18章附錄

The global Document AI market is anticipated to grow at a compound annual growth rate (CAGR) of 13.5% over the forecast period, from an estimated USD 14.66 billion in 2025 to USD 27.62 billion by 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD (Million) |

| Segments | Offering, document type, use case, vertical, and region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America |

The market is growing as adaptive document learning models enable systems to self-improve through real-time user feedback, reducing the need for manual retraining and improving accuracy across diverse document formats. Also, graph-based document intelligence is enhancing contextual understanding by linking entities and relationships within multi-page documents, which is particularly valuable for legal, insurance, and compliance workflows. However, limited standardization of document data formats across industries continues to restrain interoperability and hinders seamless model deployment at scale.

"IDP solutions dominate the Document AI market as enterprises prioritize end-to-end automation and compliance-ready data processing"

Intelligent Document Processing (IDP) solutions are projected to hold the largest market share in the Document AI market, driven by their ability to deliver complete automation across unstructured and semi-structured document workflows. IDP platforms integrate OCR, NLP, and machine learning to extract, classify, and validate data from invoices, forms, contracts, and compliance documents with high accuracy. Enterprises in sectors such as banking, insurance, and healthcare are adopting IDP to accelerate document turnaround times, reduce manual data entry, and maintain audit-ready digital records. The rapid expansion of remote operations and paperless initiatives has further increased demand for cloud-based IDP platforms. Vendors like UiPath, ABBYY, and Kofax are enhancing IDP solutions with generative AI, RPA integration, and pre-trained models for specific domains, enabling faster deployments and higher ROI. Additionally, the growing need for explainable AI and data lineage capabilities aligns with regulatory compliance requirements, reinforcing IDP's position as the preferred foundation for enterprise-scale document automation.

"Unstructured documents lead the Document AI market as enterprises automate complex, high-volume content processing"

Unstructured document types are expected to hold the largest market share in the Document AI market, reflecting the growing need to process emails, contracts, reports, handwritten notes, and multimedia-rich records that lack fixed templates. Across industries such as banking, healthcare, and government, most enterprise data remains unstructured, creating a significant demand for advanced AI models capable of understanding variable document formats. Recent advancements in layout-aware transformers, multimodal AI, and natural language understanding are allowing Document AI systems to accurately extract contextual information from text, tables, and images simultaneously. Vendors like Google, Microsoft, and AWS have expanded their solutions to handle multi-format documents using pre-trained models fine-tuned for specific industries. The adoption of unstructured document processing is also being accelerated by compliance-driven automation and data governance requirements, particularly for audit trails and customer communications. As enterprises focus on digitizing legacy archives and enabling searchable document repositories, unstructured document intelligence has become central to driving efficiency, improving decision-making, and ensuring regulatory transparency across large-scale digital ecosystems.

"Asia Pacific to witness rapid growth fueled by innovation and evolving strategies, while North America leads in market size"

The Document AI market exhibits strong regional differences, with the Asia Pacific region predicted to grow the fastest due to the rapid digital transformation in countries such as India, Indonesia, and Vietnam, supported by initiatives like Digital India and Japan's Society 5.0. Businesses are increasingly investing in cloud-based Document AI and IDP solutions to automate workflows in BFSI, healthcare, logistics, and government, driven by the need for multilingual OCR and natural language processing capabilities. The rise of fintech, digital payments, and e-governance is also driving the need for document automation in compliance, onboarding, and identity verification. Meanwhile, North America is expected to lead in 2025, thanks to its advanced infrastructure, early adoption, and vendors such as Google, Microsoft, AWS, IBM, and Adobe. Strict regulations, such as HIPAA, SOX, and GDPR, are driving the adoption of AI-driven compliance and audit solutions, particularly in the finance, insurance, and healthcare sectors, which utilize AI for classification, contract analysis, and claims processing. The integration of generative AI, RAG, and explainability models enhances document accuracy and understanding. Thus, North America's innovation and Asia Pacific's digital growth are jointly shaping the global Document AI landscape, driving market expansion.

Breakdown of primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the market.

- By Company: Tier I - 33%, Tier II - 44%, and Tier III - 23%

- By Designation: Directors - 36%, Managers - 41%, and others - 23%

- By Region: North America - 39%, Europe - 18%, Asia Pacific - 32%, Middle East & Africa - 4%, and Latin America - 7%

The report includes the study of key players offering solutions and services. It profiles major vendors in the Document AI market. The major players in the Document AI market include Google (US), Microsoft (US), SAP (Germany), IBM (US), AWS (US), Oracle (US), Adobe (US), ABBYY (US), Automation Anywhere (US), UiPath (US), Appian (US), H2O.ai (US), EdgeVerve (India), Super.ai (US), Rossum (UK), Tungsten Automation (US), OpenText (Canada), Hyland (US), Hyperscience (US), EXL (US), Snowflake (US), Salesforce (US), Grooper (US), DocDigitizer (US), Cinnamon (Japan), Docugami (US), Mistral AI (France), Upstage (US), DocByte (Belgium), Infrrd (US), Docketry (US), OpenAI (US), Gamma (US), AidocMaker (US), Anthropic (US), Checkbox (US), Docubee (US), DocuPilot (US), Docsumo (US), Formstack (US), HyperWrite (US), Lindy (US), QuillBot (US), and Scribe (US).

Research coverage

This research report covers the Document AI market, which has been segmented by offering, document type, use cases, and vertical. The offering segment is split into solutions and services. The solutions segment is further split into IDP, Document Workflow Automation, Generative AI Document Generation, and ECM & Governance Tools. Services are segmented into professional and managed services. The market, by document type, includes structured, unstructured, semi-structured, and multimodal/mixed content. Use cases include finance & accounting, legal & compliance, customer service, marketing & sales, HR, and supply chain & logistics. The verticals covered are BFSI, healthcare & life sciences, government & public sector, retail & e-commerce, manufacturing, energy & utilities, telecommunications, transportation & logistics, education, and other verticals. The regional analysis covers North America, Europe, Asia Pacific, the Middle East & Africa (MEA), and Latin America.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (advancements in OCR+NER fusion pipelines delivering higher precision, growth of e-signature and e-workflow ecosystems tying documents to transactions, marketplace bundling of capture tools with analytics and BI tools), restraints (cross-border data residency limits for model training and telemetry, high annotation cost for rare and long-tail templates), opportunities (synthetic-document marketplaces for niche training datasets, generative-assisted contract drafting integrated with clause libraries, auto-remediation engines that self-heal extraction errors through feedback loops), and challenges (maintaining extraction stability as templates and forms evolve, securing annotation supply chains against malicious or low-quality labels)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches

- Market Development: Comprehensive information about lucrative markets-the report analyses the Document AI market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments

- Competitive Assessment: In-depth assessment of market shares, growth strategies and offerings of leading players like Google (US), Microsoft (US), SAP (Germany), IBM (US), AWS (US), Oracle (US), Adobe (US), ABBYY (US), Automation Anywhere (US), UiPath (US), Appian (US), H2O.ai (US), EdgeVerve (India), Super.ai (US), Rossum (UK), Tungsten Automation (US), OpenText (Canada), Hyland (US), Hyperscience (US), EXL (US), Snowflake (US), Salesforce (US), Grooper (US), DocDigitizer (US), Cinnamon (Japan), Docugami (US), Mistral AI (France), Upstage (US), DocByte (Belgium), Infrrd (US), Docketry (US), OpenAI (US), Gamma (US), AidocMaker (US), Anthropic (US), Checkbox (US), Docubee (US), DocuPilot (US), Docsumo (US), Formstack (US), HyperWrite (US), Lindy (US), QuillBot (US), and Scribe (US)

The report also helps stakeholders understand the pulse of the Document AI market, providing them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DOCUMENT AI MARKET

- 4.2 DOCUMENT AI MARKET, BY SOLUTION

- 4.3 NORTH AMERICA: DOCUMENT AI MARKET, BY TOP SOLUTIONS AND DOCUMENT TYPES

- 4.4 DOCUMENT AI MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Advancements in OCR+NER fusion pipelines delivering higher precision

- 5.2.1.2 Growth of e-signature and e-workflow ecosystems tying documents to transactions

- 5.2.1.3 Marketplace bundling of capture tools with analytics and BI tools

- 5.2.2 RESTRAINTS

- 5.2.2.1 Cross-border data residency limits for model training and telemetry

- 5.2.2.2 High annotation cost for rare and long-tail templates

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Synthetic-document marketplaces for niche training datasets

- 5.2.3.2 Generative-assisted contract drafting integrated with clause libraries

- 5.2.3.3 Auto-remediation engines that self-heal extraction errors through feedback loops

- 5.2.4 CHALLENGES

- 5.2.4.1 Maintaining extraction stability as templates and forms evolve

- 5.2.4.2 Securing annotation supply chains against malicious or low-quality labels

- 5.2.1 DRIVERS

- 5.3 UNMET NEEDS AND WHITE SPACES

- 5.3.1 UNMET NEEDS IN DOCUMENT AI MARKET

- 5.3.2 WHITE-SPACE OPPORTUNITIES IN DOCUMENT AI MARKET

- 5.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 5.4.1 INTERCONNECTED MARKETS

- 5.4.2 CROSS-SECTOR OPPORTUNITIES

- 5.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 5.5.1 KEY MOVES AND STRATEGIC FOCUS

- 5.6 TRANSITION FROM DOCUMENT PROCESSING TO ENTERPRISE KNOWLEDGE INTELLIGENCE

- 5.7 MOVEMENT TOWARD AUTONOMOUS DOCUMENT WORKFLOWS

- 5.8 AI GOVERNANCE AND ETHICAL CONSIDERATIONS IN DOCUMENT AI ADOPTION

6 INDUSTRY TRENDS

- 6.1 PORTER'S FIVE FORCES ANALYSIS

- 6.1.1 THREAT OF NEW ENTRANTS

- 6.1.2 THREAT OF SUBSTITUTES

- 6.1.3 BARGAINING POWER OF SUPPLIERS

- 6.1.4 BARGAINING POWER OF BUYERS

- 6.1.5 INTENSITY OF COMPETITION RIVALRY

- 6.2 SUPPLY CHAIN ANALYSIS

- 6.3 EVOLUTION OF DOCUMENT AI

- 6.4 ECOSYSTEM ANALYSIS

- 6.4.1 INTELLIGENT DOCUMENT PROCESSING PROVIDERS

- 6.4.2 GEN AI DOCUMENT GENERATION PROVIDERS

- 6.4.3 DOCUMENT WORKFLOW AUTOMATION PROVIDERS

- 6.4.4 ECM & GOVERNANCE PROVIDERS

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE OF OFFERINGS, BY KEY PLAYER, 2025

- 6.5.2 AVERAGE SELLING PRICE, BY USE CASE, 2025

- 6.6 INVESTMENT AND FUNDING SCENARIO

- 6.7 CASE STUDY ANALYSIS

- 6.7.1 VERYFI ENABLES KOLLWITZOWEN TO PROVIDE FAIR PROMOTIONS WITH INSTANT RECEIPT VALIDATIONS

- 6.7.2 INFRRD AI TRANSFORMS MEDTECH LEADER'S PURCHASE ORDER PROCESSING BY AUTOMATING MULTI-LANGUAGE DOCUMENTS

- 6.7.3 DOCSUMO ACCELERATES NS TRUCKING'S DISPATCH TICKET PROCESSING BY 4X WITH AI DATA EXTRACTION

- 6.7.4 INDICO DATA CUTS GLOBAL SPECIALTY INSURER'S SUBMISSION PROCESSING TIME TO UNDER 30 SECONDS WITH AI AUTOMATION

- 6.7.5 ROSSUM BOOSTS VEOLIA'S INVOICE PROCESSING SPEED BY 8X WITH AI-DRIVEN WORKFLOW AUTOMATION

- 6.8 KEY CONFERENCES AND EVENTS, 2025-2026

- 6.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 7.1 KEY EMERGING TECHNOLOGIES

- 7.1.1 OCR

- 7.1.2 NLP

- 7.1.3 COMPUTER VISION

- 7.1.4 NEURAL NETWORKS

- 7.1.5 LLM

- 7.1.6 KNOWLEDGE GRAPHS

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 RPA

- 7.2.2 CLOUD COMPUTING

- 7.2.3 DATA ANNOTATION AND LABELING

- 7.2.4 CYBERSECURITY

- 7.2.5 DATABASE & DATA LAKE TECHNOLOGIES

- 7.3 ADJACENT TECHNOLOGIES

- 7.3.1 SPEECH-TO-TEXT AND VOICE RECOGNITION

- 7.3.2 DIGITAL IDENTITY VERIFICATION

- 7.3.3 BLOCKCHAIN

- 7.3.4 INTERNET OF THINGS (IOT)

- 7.3.5 AUGMENTED AND VIRTUAL REALITY (AR/VR)

- 7.4 PATENT ANALYSIS

- 7.4.1 METHODOLOGY

- 7.4.2 PATENTS FILED, BY DOCUMENT TYPE, 2016-2025

- 7.4.3 INNOVATION AND PATENT APPLICATIONS

- 7.5 FUTURE APPLICATIONS

8 REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 REGULATIONS

- 8.1.2.1 North America

- 8.1.2.1.1 Executive Order 14110 on Safe, Secure, and Trustworthy AI (US)

- 8.1.2.1.2 Artificial Intelligence and Data Act-AIDA (Canada)

- 8.1.2.2 Europe

- 8.1.2.2.1 Europe Artificial Intelligence Act (European Union)

- 8.1.2.2.2 General Data Protection Regulation (European Union)

- 8.1.2.2.3 Data Protection Act 2018 (UK)

- 8.1.2.2.4 Federal Data Protection Act (Germany)

- 8.1.2.2.5 French Data Protection Act (France)

- 8.1.2.2.6 Personal Data Protection Code-Legislative Decree 196/2003 (Italy)

- 8.1.2.2.7 Organic Law 3/2018 (Spain)

- 8.1.2.2.8 UAVG and Public-Sector Algorithm Transparency (Netherlands)

- 8.1.2.3 Asia Pacific

- 8.1.2.3.1 Interim Measures for the Management of Generative AI Services (China)

- 8.1.2.3.2 Digital Personal Data Protection Act, 2023 (India)

- 8.1.2.3.3 Act on the Protection of Personal Information (Japan)

- 8.1.2.3.4 Basic Act on Artificial Intelligence (South Korea)

- 8.1.2.3.5 Personal Data Protection Act (Singapore)

- 8.1.2.4 Middle East & Africa

- 8.1.2.4.1 Federal Decree-Law No. 45 of 2021 on the Protection of Personal Data (UAE)

- 8.1.2.4.2 Personal Data Protection Law (KSA)

- 8.1.2.4.3 Protection of Personal Information Act (South Africa)

- 8.1.2.4.4 Personal Data Privacy Protection Law (Qatar)

- 8.1.2.4.5 Law on the Protection of Personal Data No. 6698 (Turkey)

- 8.1.2.5 Latin America

- 8.1.2.5.1 General Data Protection Law - LGPD (Brazil)

- 8.1.2.5.2 Federal Law on Protection of Personal Data Held by Private Parties (Mexico)

- 8.1.2.5.3 Personal Data Protection Law No. 25,326 (Argentina)

- 8.1.2.1 North America

9 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 9.1 DECISION-MAKING PROCESS

- 9.1.1 STRATEGIC EVALUATION AND BUSINESS CASE ALIGNMENT

- 9.1.2 TECHNICAL VALIDATION AND VENDOR DIFFERENTIATION

- 9.1.3 PROCUREMENT, CHANGE MANAGEMENT, AND LONG-TERM VALUE REALIZATION

- 9.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 9.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 9.2.2 BUYING CRITERIA

- 9.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 9.4 UNMET NEEDS FROM VARIOUS END-USER VERTICALS

- 9.5 MARKET PROFITABILITY

10 DOCUMENT AI MARKET, BY OFFERING

- 10.1 INTRODUCTION

- 10.1.1 DRIVERS: DOCUMENT AI MARKET, BY OFFERING

- 10.2 SOLUTIONS

- 10.2.1 IDP

- 10.2.1.1 Enabling high-accuracy extraction and automation of unstructured data

- 10.2.2 DOCUMENT WORKFLOW AUTOMATION

- 10.2.2.1 Bridging IDP and business operations for seamless processing

- 10.2.3 GEN AI DOCUMENT GENERATION

- 10.2.3.1 Redefining content creation and document authoring workflows

- 10.2.4 ECM & GOVERNANCE TOOLS

- 10.2.4.1 Ensuring security, compliance, and structured document management

- 10.2.1 IDP

- 10.3 SERVICES

- 10.3.1 PROFESSIONAL SERVICES

- 10.3.1.1 Enabling seamless implementation and strategic alignment of Document AI

- 10.3.1.2 Consulting & advisory

- 10.3.1.3 Deployment & integration

- 10.3.1.4 Support & training

- 10.3.2 MANAGED SERVICES

- 10.3.2.1 Enabling scalable and cost-effective Document AI operations

- 10.3.1 PROFESSIONAL SERVICES

- 10.4 DEPLOYMENT MODE

- 10.4.1 CLOUD

- 10.4.1.1 Accelerating time-to-value and global scalability of Document AI

- 10.4.2 ON-PREMISES

- 10.4.2.1 Essential for data-sensitive and regulated industries

- 10.4.1 CLOUD

11 DOCUMENT AI MARKET, BY DOCUMENT TYPE

- 11.1 INTRODUCTION

- 11.1.1 DRIVERS: DOCUMENT AI MARKET, BY DOCUMENT TYPE

- 11.2 STRUCTURED

- 11.2.1 DRIVING HIGH-VOLUME, HIGH-ACCURACY AUTOMATION AT SCALE

- 11.3 UNSTRUCTURED

- 11.3.1 POWERING NEXT WAVE OF INTELLIGENT DOCUMENT UNDERSTANDING

- 11.4 SEMI-STRUCTURED

- 11.4.1 BRIDGING RULE-BASED AUTOMATION AND ADAPTIVE AI MODELS

- 11.5 MULTIMODAL/MIXED CONTENT

- 11.5.1 UNLOCKING NEW FRONTIERS IN COMPLEX DATA UNDERSTANDING

12 DOCUMENT AI MARKET, BY USE CASE

- 12.1 INTRODUCTION

- 12.1.1 DRIVERS: DOCUMENT AI MARKET, BY USE CASE

- 12.2 FINANCE & ACCOUNTING

- 12.2.1 INVOICES & TAX FORMS

- 12.2.1.1 Streamlining payables with intelligent data extraction and validation

- 12.2.2 RECEIPTS & REIMBURSEMENT CLAIMS

- 12.2.2.1 Accelerating employee expense management through automated capture

- 12.2.3 BANK STATEMENTS

- 12.2.3.1 Enabling transparent financial reconciliation and anomaly detection

- 12.2.4 FINANCIAL REPORTS & REGULATORY FILINGS

- 12.2.4.1 Ensuring compliance and accuracy in complex disclosures

- 12.2.5 EXPENSE FORMS

- 12.2.5.1 Reducing manual entry and policy violations through context-aware automation

- 12.2.6 OTHER FINANCE & ACCOUNTING USE CASES

- 12.2.1 INVOICES & TAX FORMS

- 12.3 HR

- 12.3.1 RESUMES/CVS

- 12.3.1.1 Accelerating talent acquisition with AI-driven resume intelligence

- 12.3.2 ONBOARDING DOCUMENTS

- 12.3.2.1 Streamlining employee onboarding with intelligent document automation

- 12.3.3 PAYROLL

- 12.3.3.1 Automating payroll documentation for compliance and accuracy

- 12.3.4 POLICY DOCUMENT

- 12.3.4.1 Enforcing policy compliance through AI-driven document governance

- 12.3.5 OTHER HR USE CASES

- 12.3.1 RESUMES/CVS

- 12.4 LEGAL & COMPLIANCE

- 12.4.1 CONTRACTS

- 12.4.1.1 Automating contract lifecycle management for speed and risk reduction

- 12.4.2 AGREEMENTS

- 12.4.2.1 Streamlining agreement validation and compliance auditing through AI

- 12.4.3 NDAS

- 12.4.3.1 Enhancing confidentiality governance with automated NDA monitoring

- 12.4.4 REGULATORY FILINGS

- 12.4.4.1 Accelerating regulatory compliance through AI-enabled document intelligence

- 12.4.5 COMPLIANCE REPORTS

- 12.4.5.1 Ensuring continuous audit readiness with automated compliance documentation

- 12.4.6 OTHER LEGAL & COMPLIANCE USE CASES

- 12.4.1 CONTRACTS

- 12.5 CUSTOMER SERVICE

- 12.5.1 KYC DOCUMENTS

- 12.5.1.1 Accelerating customer verification and compliance through AI-powered KYC automation

- 12.5.2 CLAIM FORMS

- 12.5.2.1 Streamlining claim processing through context-aware document understanding

- 12.5.3 CUSTOMER FEEDBACK

- 12.5.3.1 Turning unstructured customer feedback into actionable insights with AI

- 12.5.4 SERVICE REQUEST

- 12.5.4.1 Automating service request handling for faster and more personalized support

- 12.5.5 OTHER CUSTOMER SERVICE USE CASES

- 12.5.1 KYC DOCUMENTS

- 12.6 MARKETING & SALES

- 12.6.1 PROPOSALS

- 12.6.1.1 Streamlining proposal creation and review with AI-powered document intelligence

- 12.6.2 RFP RESPONSES

- 12.6.2.1 Accelerating RFP lifecycle management with intelligent document automation

- 12.6.3 SURVEY RESULTS

- 12.6.3.1 Transforming customer insights from survey documents into strategic intelligence

- 12.6.4 CAMPAIGN COLLATERAL

- 12.6.4.1 Optimizing marketing content management with AI-driven document structuring

- 12.6.5 OTHER MARKETING & SALES USE CASES

- 12.6.1 PROPOSALS

- 12.7 SUPPLY CHAIN & LOGISTICS

- 12.7.1 PURCHASE ORDERS

- 12.7.1.1 Automating procurement approvals and supplier coordination with intelligent PO processing

- 12.7.2 DELIVERY NOTES

- 12.7.2.1 Streamlining goods receipt and verification through automated delivery note processing

- 12.7.3 BILLS OF LADING

- 12.7.3.1 Ensuring shipping accuracy and regulatory compliance with intelligent bill of lading processing

- 12.7.4 SHIPMENT MANIFESTS

- 12.7.4.1 Enabling real-time cargo visibility and tracking with AI-enabled manifest digitization

- 12.7.5 OTHER SUPPLY CHAIN & LOGISTICS USE CASES

- 12.7.1 PURCHASE ORDERS

13 DOCUMENT AI MARKET, BY VERTICAL

- 13.1 INTRODUCTION

- 13.1.1 DRIVERS: DOCUMENT AI MARKET, BY VERTICAL

- 13.2 BFSI

- 13.2.1 MODERNIZING HIGH-VOLUME FINANCIAL DOCUMENTATION WITH AI-DRIVEN PRECISION

- 13.3 TRANSPORTATION & LOGISTICS

- 13.3.1 AUTOMATING SHIPMENT AND COMPLIANCE DOCUMENTATION FOR FASTER SUPPLY CHAIN FLOWS

- 13.4 HEALTHCARE & LIFE SCIENCES

- 13.4.1 IMPROVING CLINICAL ACCURACY AND ADMINISTRATIVE EFFICIENCY WITH DOCUMENT AI

- 13.5 GOVERNMENT & PUBLIC SECTOR

- 13.5.1 ACCELERATING ADMINISTRATIVE EFFICIENCY AND CITIZEN SERVICES THROUGH DOCUMENT INTELLIGENCE

- 13.6 RETAIL & E-COMMERCE

- 13.6.1 ENHANCING TRANSACTION SPEED AND CUSTOMER EXPERIENCE WITH AUTOMATED DOCUMENT FLOWS

- 13.7 MANUFACTURING

- 13.7.1 DRIVING PRODUCTION EFFICIENCY AND COMPLIANCE WITH AUTOMATED DOCUMENT INTELLIGENCE

- 13.8 ENERGY & UTILITIES

- 13.8.1 STRENGTHENING REGULATORY COMPLIANCE AND ASSET MANAGEMENT WITH AI-DRIVEN DOCUMENT PROCESSING

- 13.9 TELECOMMUNICATIONS

- 13.9.1 STREAMLINING SERVICE DOCUMENTATION AND REGULATORY PROCESSES THROUGH AUTOMATION

- 13.10 EDUCATION

- 13.10.1 EMPOWERING EDUCATIONAL EFFICIENCY THROUGH AI-DRIVEN DOCUMENT INTELLIGENCE

- 13.11 OTHER VERTICALS

14 DOCUMENT AI MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 NORTH AMERICA: DOCUMENT AI MARKET DRIVERS

- 14.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 14.2.3 US

- 14.2.3.1 Innovation leadership and regulatory maturity to drive market

- 14.2.4 CANADA

- 14.2.4.1 Public sector digitization and cloud adoption to drive market

- 14.3 EUROPE

- 14.3.1 EUROPE: DOCUMENT AI MARKET DRIVERS

- 14.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 14.3.3 UK

- 14.3.3.1 Early enterprise digitalization and regulatory clarity to strengthen market

- 14.3.4 GERMANY

- 14.3.4.1 Manufacturing leadership and data sovereignty to drive Document AI adoption

- 14.3.5 FRANCE

- 14.3.5.1 Public sector digitization and language localization to boost market

- 14.3.6 ITALY

- 14.3.6.1 Modernization of public administration and BFSI to drive market

- 14.3.7 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 ASIA PACIFIC: DOCUMENT AI MARKET DRIVERS

- 14.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 14.4.3 CHINA

- 14.4.3.1 National digital ecosystem and e-government push to fuel demand for Document AI

- 14.4.4 INDIA

- 14.4.4.1 Digital governance and rapid cloud adoption to power Document AI uptake

- 14.4.5 JAPAN

- 14.4.5.1 Workforce automation and paperless initiatives to drive Document AI adoption

- 14.4.6 SOUTH KOREA

- 14.4.6.1 High digital readiness and AI integration to fuel market

- 14.4.7 SINGAPORE

- 14.4.7.1 Innovation-led adoption and regulatory clarity to strengthen market

- 14.4.8 REST OF ASIA PACIFIC

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET DRIVERS

- 14.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 14.5.3 SAUDI ARABIA

- 14.5.3.1 National digitalization and Vision 2030 to catalyze Document AI ecosystem

- 14.5.4 UAE

- 14.5.4.1 Early government adoption and smart infrastructure programs to drive Document AI leadership

- 14.5.5 SOUTH AFRICA

- 14.5.5.1 Urban enterprise digitalization and BFSI modernization to fuel the market

- 14.5.6 QATAR

- 14.5.6.1 Vision 2030 and national digital infrastructure investments to market

- 14.5.7 REST OF MIDDLE EAST & AFRICA

- 14.6 LATIN AMERICA

- 14.6.1 LATIN AMERICA: DOCUMENT AI MARKET DRIVERS

- 14.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 14.6.3 BRAZIL

- 14.6.3.1 Strict e-invoicing regulations and tax modernization programs to drive market

- 14.6.4 MEXICO

- 14.6.4.1 Tax digitalization and e-signature expansion to accelerate Document AI adoption

- 14.6.5 REST OF LATIN AMERICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 15.3 REVENUE ANALYSIS, 2020-2024

- 15.4 MARKET SHARE ANALYSIS, 2024

- 15.5 PRODUCT COMPARISON

- 15.5.1 PRODUCT COMPARATIVE ANALYSIS, BY DOCUMENT AI SOLUTION TYPE (IDP)

- 15.5.1.1 Document AI (Google)

- 15.5.1.2 Azure AI Document Intelligence (Microsoft)

- 15.5.1.3 Amazon Textract & Comprehend (AWS)

- 15.5.1.4 ABBYY Vantage (ABBYY)

- 15.5.1.5 Kofax TotalAgility (Tungsten Automation)

- 15.5.2 PRODUCT COMPARATIVE ANALYSIS, BY DOCUMENT AI SOLUTION TYPE (DOCUMENT WORKFLOW AUTOMATION)

- 15.5.2.1 UiPath Document Understanding (UiPath)

- 15.5.2.2 IQ Bot (Automation Anywhere)

- 15.5.2.3 Intelligent Capture & Magellan (OpenText)

- 15.5.2.4 IBM Watson Discovery & Automation (IBM)

- 15.5.2.5 Intelligent Document Processing Platform (Infrrd)

- 15.5.3 PRODUCT COMPARATIVE ANALYSIS, BY DOCUMENT AI SOLUTION TYPE (GEN AI DOCUMENT GENERATION)

- 15.5.3.1 Gamma's intelligent formatting and design tools (Gamma)

- 15.5.3.2 GPT-4/ChatGPT Enterprise (OpenAI)

- 15.5.3.3 Gen AI-enhanced IDP (Docsumo)

- 15.5.3.4 AI Writing Suite (QuillBot)

- 15.5.3.5 Claude AI (Anthropic)

- 15.5.4 PRODUCT COMPARATIVE ANALYSIS, BY DOCUMENT AI SOLUTION TYPE (ECM & GOVERNANCE TOOLS)

- 15.5.4.1 AI-powered Process & Content Governance (Appian)

- 15.5.4.2 Document Data Governance Cloud (Snowflake)

- 15.5.4.3 XtractEdge for Document Governance (EdgeVerve)

- 15.5.4.4 OnBase & Alfresco ECM (Hyland)

- 15.5.4.5 Intelligent Digital Preservation Platform (Docbyte)

- 15.5.1 PRODUCT COMPARATIVE ANALYSIS, BY DOCUMENT AI SOLUTION TYPE (IDP)

- 15.6 COMPANY VALUATION AND FINANCIAL METRICS

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.7.1 IDP, DOCUMENT WORKFLOW AUTOMATION, AND ECM & GOVERNANCE TOOLS

- 15.7.1.1 Stars

- 15.7.1.2 Emerging leaders

- 15.7.1.3 Pervasive players

- 15.7.1.4 Participants

- 15.7.2 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.7.2.1 Company footprint

- 15.7.2.2 Regional footprint

- 15.7.2.3 Offering footprint

- 15.7.2.4 Use case footprint

- 15.7.2.5 Vertical footprint

- 15.7.3 GENERATIVE AI DOCUMENT GENERATION

- 15.7.3.1 Stars

- 15.7.3.2 Emerging leaders

- 15.7.3.3 Pervasive players

- 15.7.3.4 Participants

- 15.7.4 COMPANY FOOTPRINT: KEY PLAYERS (GENERATIVE AI DOCUMENT GENERATION), 2024

- 15.7.4.1 Company footprint

- 15.7.4.2 Regional footprint

- 15.7.4.3 Offering footprint

- 15.7.4.4 Use case footprint

- 15.7.4.5 Vertical footprint

- 15.7.1 IDP, DOCUMENT WORKFLOW AUTOMATION, AND ECM & GOVERNANCE TOOLS

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.8.1 IDP, DOCUMENT WORKFLOW AUTOMATION, ECM & GOVERNANCE TOOLS

- 15.8.1.1 Progressive Companies

- 15.8.1.2 Responsive companies

- 15.8.1.3 Dynamic companies

- 15.8.1.4 Starting blocks

- 15.8.2 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 15.8.2.1 Detailed list of key startups/SMEs

- 15.8.2.2 Competitive benchmarking of key startups/SMEs

- 15.8.1 IDP, DOCUMENT WORKFLOW AUTOMATION, ECM & GOVERNANCE TOOLS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 15.9.2 DEALS

16 COMPANY PROFILES

- 16.1 INTRODUCTION

- 16.2 INTELLIGENT DOCUMENT PROCESSING

- 16.2.1 KEY PLAYERS

- 16.2.1.1 Google

- 16.2.1.1.1 Business overview

- 16.2.1.1.2 Products/Solutions/Services offered

- 16.2.1.1.3 Recent developments

- 16.2.1.1.3.1 Product launches and enhancements

- 16.2.1.1.3.2 Deals

- 16.2.1.1.4 MnM view

- 16.2.1.1.4.1 Key strengths

- 16.2.1.1.4.2 Strategic choices

- 16.2.1.1.4.3 Weaknesses and competitive threats

- 16.2.1.2 Microsoft

- 16.2.1.2.1 Business overview

- 16.2.1.2.2 Products/Solutions/Services offered

- 16.2.1.2.3 Recent developments

- 16.2.1.2.3.1 Product launches and enhancements

- 16.2.1.2.3.2 Deals

- 16.2.1.2.4 MnM view

- 16.2.1.2.4.1 Key strengths

- 16.2.1.2.4.2 Strategic choices

- 16.2.1.2.4.3 Weaknesses and competitive threats

- 16.2.1.3 Hyland

- 16.2.1.3.1 Business overview

- 16.2.1.3.2 Products/Solutions/Services offered

- 16.2.1.3.3 Recent developments

- 16.2.1.3.3.1 Product launches and enhancements

- 16.2.1.3.3.2 Deals

- 16.2.1.3.4 MnM view

- 16.2.1.3.4.1 Key strengths

- 16.2.1.3.4.2 Strategic choices

- 16.2.1.3.4.3 Weaknesses and competitive threats

- 16.2.1.4 IBM

- 16.2.1.4.1 Business overview

- 16.2.1.4.2 Products/Solutions/Services offered

- 16.2.1.4.3 Recent developments

- 16.2.1.4.3.1 Product launches and enhancements

- 16.2.1.4.3.2 Deals

- 16.2.1.4.4 MnM view

- 16.2.1.4.4.1 Key strengths

- 16.2.1.4.4.2 Strategic choices

- 16.2.1.4.4.3 Weaknesses and competitive threats

- 16.2.1.5 AWS

- 16.2.1.5.1 Business overview

- 16.2.1.5.2 Products/Solutions/Services offered

- 16.2.1.5.3 Recent developments

- 16.2.1.5.3.1 Product launches and enhancements

- 16.2.1.5.3.2 Deals

- 16.2.1.5.4 MnM view

- 16.2.1.5.4.1 Key strengths

- 16.2.1.5.4.2 Strategic choices

- 16.2.1.5.4.3 Weaknesses and competitive threats

- 16.2.1.6 Snowflake

- 16.2.1.6.1 Business overview

- 16.2.1.6.2 Products/Solutions/Services offered

- 16.2.1.6.3 Recent developments

- 16.2.1.6.3.1 Product launches and enhancements

- 16.2.1.6.3.2 Deals

- 16.2.1.7 Oracle

- 16.2.1.7.1 Business overview

- 16.2.1.7.2 Products/Solutions/Services offered

- 16.2.1.7.3 Recent developments

- 16.2.1.7.3.1 Product launches and enhancements

- 16.2.1.7.3.2 Deals

- 16.2.1.7.3.3 Other developments

- 16.2.1.8 Adobe

- 16.2.1.8.1 Business overview

- 16.2.1.8.2 Products/Solutions/Services offered

- 16.2.1.8.3 Recent developments

- 16.2.1.8.3.1 Product launches and enhancements

- 16.2.1.8.3.2 Deals

- 16.2.1.9 ABBYY

- 16.2.1.9.1 Business overview

- 16.2.1.9.2 Products/Solutions/Services offered

- 16.2.1.9.3 Recent developments

- 16.2.1.9.3.1 Product launches and enhancements

- 16.2.1.9.3.2 Deals

- 16.2.1.10 Automation Anywhere

- 16.2.1.10.1 Business overview

- 16.2.1.10.2 Products/Solutions/Services offered

- 16.2.1.10.3 Recent developments

- 16.2.1.10.3.1 Product launches and enhancements

- 16.2.1.10.3.2 Deals

- 16.2.1.11 UiPath

- 16.2.1.11.1 Business overview

- 16.2.1.11.2 Products/Solutions/Services offered

- 16.2.1.11.3 Recent developments

- 16.2.1.11.3.1 Product launches and enhancements

- 16.2.1.11.3.2 Deals

- 16.2.1.12 Appian

- 16.2.1.12.1 Business overview

- 16.2.1.12.2 Products/Solutions/Services offered

- 16.2.1.12.3 Recent developments

- 16.2.1.12.3.1 Product launches and enhancements

- 16.2.1.12.3.2 Deals

- 16.2.1.13 EdgeVerve (Infosys)

- 16.2.1.14 Tungsten Automation

- 16.2.1.15 OpenText

- 16.2.1.16 SAP

- 16.2.1.17 EXL

- 16.2.1.18 Salesforce

- 16.2.1.19 H20.ai

- 16.2.1.20 Scribe

- 16.2.1.21 Docketry

- 16.2.1.22 Cohere

- 16.2.1.1 Google

- 16.2.2 OTHER PLAYERS

- 16.2.2.1 Grooper

- 16.2.2.2 Hyperscience

- 16.2.2.3 DocDigitizer

- 16.2.2.4 Super.ai

- 16.2.2.5 Cinnamon AI

- 16.2.2.6 Docugami

- 16.2.2.7 DocByte

- 16.2.2.8 Infrrd

- 16.2.2.9 Rossum

- 16.2.2.10 Docubee

- 16.2.2.11 Docsumo

- 16.2.2.12 Checkbox

- 16.2.2.13 Mindee

- 16.2.1 KEY PLAYERS

- 16.3 GENERATIVE AI DOCUMENT GENERATION

- 16.3.1 KEY PLAYERS

- 16.3.1.1 OpenAI

- 16.3.1.1.1 Business overview

- 16.3.1.1.2 Products/Solutions/Services offered

- 16.3.1.1.3 Recent developments

- 16.3.1.1.3.1 Product launches and enhancements

- 16.3.1.1.3.2 Deals

- 16.3.1.2 Gamma

- 16.3.1.3 Upstage

- 16.3.1.4 Aidocmaker

- 16.3.1.5 Anthropic

- 16.3.1.6 Mistral AI

- 16.3.1.7 DocuPilot

- 16.3.1.8 Intellistack

- 16.3.1.9 HyperWrite (OthersideAI)

- 16.3.1.10 Lindy

- 16.3.1.11 QuillBot

- 16.3.1.1 OpenAI

- 16.3.1 KEY PLAYERS

17 ADJACENT AND RELATED MARKETS

- 17.1 INTRODUCTION

- 17.2 ARTIFICIAL INTELLIGENCE MARKET - GLOBAL FORECAST TO 2032

- 17.2.1 MARKET DEFINITION

- 17.2.2 MARKET OVERVIEW

- 17.2.2.1 Artificial intelligence (AI) market, by offering

- 17.2.2.2 Artificial intelligence (AI) market, by technology

- 17.2.2.3 Artificial intelligence (AI) market, by business function

- 17.2.2.4 Artificial intelligence (AI) market, by enterprise application

- 17.2.2.5 Artificial intelligence (AI) market, by end user

- 17.2.2.6 Artificial intelligence (AI) market, by region

- 17.3 AI DETECTOR MARKET - GLOBAL FORECAST TO 2030

- 17.3.1 MARKET DEFINITION

- 17.3.2 MARKET OVERVIEW

- 17.3.2.1 AI detector market, by offering

- 17.3.2.2 AI detector market, by detection modality

- 17.3.2.3 AI detector market, by application

- 17.3.2.4 AI detector market, by end user

- 17.3.2.5 AI detector market, by region

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS

List of Tables

- TABLE 1 USD EXCHANGE RATE, 2020-2024

- TABLE 2 PRIMARY INTERVIEWS

- TABLE 3 FACTOR ANALYSIS

- TABLE 4 DOCUMENT AI MARKET SIZE AND GROWTH RATE, 2020-2024 (USD MILLION, Y-O-Y %)

- TABLE 5 DOCUMENT AI MARKET SIZE AND GROWTH RATE, 2025-2030 (USD MILLION, Y-O-Y %)

- TABLE 6 IMPACT OF PORTER'S FIVE FORCES ON DOCUMENT AI MARKET

- TABLE 7 DOCUMENT AI MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 8 AVERAGE SELLING PRICE OF OFFERINGS, BY KEY PLAYER, 2025

- TABLE 9 AVERAGE SELLING PRICE, BY USE CASE, 2025

- TABLE 10 DOCUMENT AI MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 11 PATENTS FILED, 2016-2025

- TABLE 12 LIST OF TOP PATENTS IN DOCUMENT AI MARKET, 2024-2025

- TABLE 13 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE VERTICALS

- TABLE 19 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- TABLE 20 DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 21 DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 22 SOLUTIONS: DOCUMENT AI MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 23 SOLUTIONS: DOCUMENT AI MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 24 SOLUTIONS: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 25 SOLUTIONS: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 26 IDP: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 27 IDP: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 28 DOCUMENT WORKFLOW AUTOMATION: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 29 DOCUMENT WORKFLOW AUTOMATION: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 30 GEN AI DOCUMENT GENERATION: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 31 GEN AI DOCUMENT GENERATION: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 32 ECM & GOVERNANCE TOOLS: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 33 ECM & GOVERNANCE TOOLS: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 34 SERVICES: DOCUMENT AI MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 35 SERVICES: DOCUMENT AI MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 36 SERVICES: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 37 SERVICES: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 38 PROFESSIONAL SERVICES: DOCUMENT AI MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 39 PROFESSIONAL SERVICES: DOCUMENT AI MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 40 PROFESSIONAL SERVICES: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 41 PROFESSIONAL SERVICES: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 42 CONSULTING & ADVISORY: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 43 CONSULTING & ADVISORY: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 44 DEPLOYMENT & INTEGRATION: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 45 DEPLOYMENT & INTEGRATION: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 46 SUPPORT & TRAINING: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 47 SUPPORT & TRAINING: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 48 MANAGED SERVICES: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 49 MANAGED SERVICES: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 50 DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 51 DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 52 CLOUD: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 53 CLOUD: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 54 ON-PREMISES: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 55 ON-PREMISES: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 56 DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 57 DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 58 STRUCTURED: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 59 STRUCTURED: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 60 UNSTRUCTURED: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 61 UNSTRUCTURED: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 62 SEMI-STRUCTURED: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 63 SEMI-STRUCTURED: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 64 MULTIMODAL/MIXED CONTENT: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 65 MULTIMODAL/MIXED CONTENT: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 66 DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 67 DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 68 FINANCE & ACCOUNTING: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 69 FINANCE & ACCOUNTING: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 70 HR: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 71 HR: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 72 LEGAL & COMPLIANCE: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 73 LEGAL & COMPLIANCE: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 74 CUSTOMER SERVICE: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 75 CUSTOMER SERVICE: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 76 MARKETING & SALES: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 77 MARKETING & SALES: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 78 SUPPLY CHAIN & LOGISTICS: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 79 SUPPLY CHAIN & LOGISTICS: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 80 DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 81 DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 82 BFSI: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 83 BFSI: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 84 TRANSPORTATION & LOGISTICS: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 85 TRANSPORTATION & LOGISTICS: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 86 HEALTHCARE & LIFE SCIENCES: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 87 HEALTHCARE & LIFE SCIENCES: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 88 GOVERNMENT & PUBLIC SECTOR: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 89 GOVERNMENT & PUBLIC SECTOR: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 90 RETAIL & E-COMMERCE: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 91 RETAIL & E-COMMERCE: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 92 MANUFACTURING: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 93 MANUFACTURING: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 94 ENERGY & UTILITIES: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 95 ENERGY & UTILITIES: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 96 TELECOMMUNICATIONS: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 97 TELECOMMUNICATIONS: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 98 EDUCATION: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 99 EDUCATION: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 100 OTHER VERTICALS: DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 101 OTHER VERTICALS: DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 102 DOCUMENT AI MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 103 DOCUMENT AI MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 104 NORTH AMERICA: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 105 NORTH AMERICA: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 106 NORTH AMERICA: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 107 NORTH AMERICA: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 108 NORTH AMERICA: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 109 NORTH AMERICA: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 110 NORTH AMERICA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 111 NORTH AMERICA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 112 NORTH AMERICA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 113 NORTH AMERICA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 114 NORTH AMERICA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 115 NORTH AMERICA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 116 NORTH AMERICA: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 117 NORTH AMERICA: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 118 NORTH AMERICA: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 119 NORTH AMERICA: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 120 NORTH AMERICA: DOCUMENT AI MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 121 NORTH AMERICA: DOCUMENT AI MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 122 US: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 123 US: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 124 US: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 125 US: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 126 US: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 127 US: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 128 US: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 129 US: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 130 US: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 131 US: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 132 US: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 133 US: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 134 US: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 135 US: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 136 US: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 137 US: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 138 CANADA: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 139 CANADA: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 140 CANADA: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 141 CANADA: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 142 CANADA: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 143 CANADA: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 144 CANADA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 145 CANADA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 146 CANADA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 147 CANADA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 148 CANADA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 149 CANADA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 150 CANADA: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 151 CANADA: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 152 CANADA: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 153 CANADA: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 154 EUROPE: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 155 EUROPE: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 156 EUROPE: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 157 EUROPE: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 158 EUROPE: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 159 EUROPE: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 160 EUROPE: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 161 EUROPE: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 162 EUROPE: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 163 EUROPE: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 164 EUROPE: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 165 EUROPE: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 166 EUROPE: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 167 EUROPE: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 168 EUROPE: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 169 EUROPE: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 170 EUROPE: DOCUMENT AI MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 171 EUROPE: DOCUMENT AI MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 172 UK: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 173 UK: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 174 UK: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 175 UK: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 176 UK: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 177 UK: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 178 UK: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 179 UK: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 180 UK: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 181 UK: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 182 UK: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 183 UK: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 184 UK: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 185 UK: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 186 UK: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 187 UK: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 188 GERMANY: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 189 GERMANY: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 190 GERMANY: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 191 GERMANY: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 192 GERMANY: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 193 GERMANY: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 194 GERMANY: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 195 GERMANY: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 196 GERMANY: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 197 GERMANY: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 198 GERMANY: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 199 GERMANY: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 200 GERMANY: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 201 GERMANY: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 202 GERMANY: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 203 GERMANY: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 204 FRANCE: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 205 FRANCE: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 206 FRANCE: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 207 FRANCE: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 208 FRANCE: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 209 FRANCE: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 210 FRANCE: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 211 FRANCE: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 212 FRANCE: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 213 FRANCE: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 214 FRANCE: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 215 FRANCE: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 216 FRANCE: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 217 FRANCE: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 218 FRANCE: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 219 FRANCE: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 220 ITALY: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 221 ITALY: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 222 ITALY: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 223 ITALY: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 224 ITALY: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 225 ITALY: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 226 ITALY: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 227 ITALY: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 228 ITALY: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 229 ITALY: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 230 ITALY: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 231 ITALY: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 232 ITALY: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 233 ITALY: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 234 ITALY: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 235 ITALY: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 236 REST OF EUROPE: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 237 REST OF EUROPE: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 238 REST OF EUROPE: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 239 REST OF EUROPE: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 240 REST OF EUROPE: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 241 REST OF EUROPE: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 242 REST OF EUROPE: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 243 REST OF EUROPE: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 244 REST OF EUROPE: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 245 REST OF EUROPE: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 246 REST OF EUROPE: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 247 REST OF EUROPE: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 248 REST OF EUROPE: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 249 REST OF EUROPE: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 250 REST OF EUROPE: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 251 REST OF EUROPE: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 252 ASIA PACIFIC: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 253 ASIA PACIFIC: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 254 ASIA PACIFIC: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 255 ASIA PACIFIC: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 256 ASIA PACIFIC: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 257 ASIA PACIFIC: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 258 ASIA PACIFIC: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 259 ASIA PACIFIC: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 260 ASIA PACIFIC: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 261 ASIA PACIFIC: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 262 ASIA PACIFIC: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 263 ASIA PACIFIC: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 264 ASIA PACIFIC: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 265 ASIA PACIFIC: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 266 ASIA PACIFIC: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 267 ASIA PACIFIC: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 268 ASIA PACIFIC: DOCUMENT AI MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 269 ASIA PACIFIC: DOCUMENT AI MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 270 CHINA: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 271 CHINA: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 272 CHINA: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 273 CHINA: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 274 CHINA: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 275 CHINA: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 276 CHINA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 277 CHINA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 278 CHINA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 279 CHINA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 280 CHINA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 281 CHINA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 282 CHINA: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 283 CHINA: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 284 CHINA: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 285 CHINA: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 286 INDIA: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 287 INDIA: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 288 INDIA: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 289 INDIA: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 290 INDIA: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 291 INDIA: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 292 INDIA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 293 INDIA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 294 INDIA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 295 INDIA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 296 INDIA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 297 INDIA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 298 INDIA: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 299 INDIA: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 300 INDIA: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 301 INDIA: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 302 JAPAN: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 303 JAPAN: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 304 JAPAN: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 305 JAPAN: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 306 JAPAN: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 307 JAPAN: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 308 JAPAN: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 309 JAPAN: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 310 JAPAN: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 311 JAPAN: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 312 JAPAN: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 313 JAPAN: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 314 JAPAN: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 315 JAPAN: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 316 JAPAN: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 317 JAPAN: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 318 SOUTH KOREA: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 319 SOUTH KOREA: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 320 SOUTH KOREA: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 321 SOUTH KOREA: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 322 SOUTH KOREA: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 323 SOUTH KOREA: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 324 SOUTH KOREA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 325 SOUTH KOREA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 326 SOUTH KOREA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 327 SOUTH KOREA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 328 SOUTH KOREA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 329 SOUTH KOREA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 330 SOUTH KOREA: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 331 SOUTH KOREA: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 332 SOUTH KOREA: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 333 SOUTH KOREA: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 334 SINGAPORE: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 335 SINGAPORE: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 336 SINGAPORE: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 337 SINGAPORE: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 338 SINGAPORE: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 339 SINGAPORE: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 340 SINGAPORE: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 341 SINGAPORE: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 342 SINGAPORE: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 343 SINGAPORE: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 344 SINGAPORE: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 345 SINGAPORE: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 346 SINGAPORE: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 347 SINGAPORE: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 348 SINGAPORE: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 349 SINGAPORE: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 350 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 351 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 352 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 353 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 354 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 355 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 356 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 357 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 358 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 359 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 360 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 361 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 362 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 363 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 364 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 365 REST OF ASIA PACIFIC: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 366 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 367 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 368 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 369 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 370 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 371 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 372 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 373 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 374 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 375 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 376 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 377 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 378 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 379 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 380 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 381 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 382 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 383 MIDDLE EAST & AFRICA: DOCUMENT AI MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 384 SAUDI ARABIA: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 385 SAUDI ARABIA: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 386 SAUDI ARABIA: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 387 SAUDI ARABIA: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 388 SAUDI ARABIA: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 389 SAUDI ARABIA: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 390 SAUDI ARABIA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 391 SAUDI ARABIA: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 392 SAUDI ARABIA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 393 SAUDI ARABIA: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 394 SAUDI ARABIA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 395 SAUDI ARABIA: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 396 SAUDI ARABIA: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 397 SAUDI ARABIA: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 398 SAUDI ARABIA: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 399 SAUDI ARABIA: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 400 UAE: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 401 UAE: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 402 UAE: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 403 UAE: DOCUMENT AI MARKET, BY SOLUTION 2025-2030 (USD MILLION)

- TABLE 404 UAE: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 405 UAE: DOCUMENT AI MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 406 UAE: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 407 UAE: DOCUMENT AI MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 408 UAE: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 409 UAE: DOCUMENT AI MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 410 UAE: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 411 UAE: DOCUMENT AI MARKET, BY DOCUMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 412 UAE: DOCUMENT AI MARKET, BY USE CASE, 2020-2024 (USD MILLION)

- TABLE 413 UAE: DOCUMENT AI MARKET, BY USE CASE, 2025-2030 (USD MILLION)

- TABLE 414 UAE: DOCUMENT AI MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 415 UAE: DOCUMENT AI MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 416 SOUTH AFRICA: DOCUMENT AI MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 417 SOUTH AFRICA: DOCUMENT AI MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 418 SOUTH AFRICA: DOCUMENT AI MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 419 SOUTH AFRICA: DOCUMENT AI MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 420 SOUTH AFRICA: DOCUMENT AI MARKET, BY SERVICE, 2020-2024 (USD MILLION)