|

市場調查報告書

商品編碼

1854902

全球表面處理化學品市場(至2032年)依產品類型(電鍍化學品、轉化膜、陽極氧化化學品、鈍化化學品、脫漆劑、清潔劑)、加工方法、基材、終端用戶產業和地區分類Surface Treatment Chemical Market by Product Type (Plating Chemicals, Conversion Coating, Anodizing Chemicals, Passivation Chemicals, Paint Strippers, Cleaners), Treatment Method, Base Material, End-Use Industry, and Region - Global Forecast to 2032 |

||||||

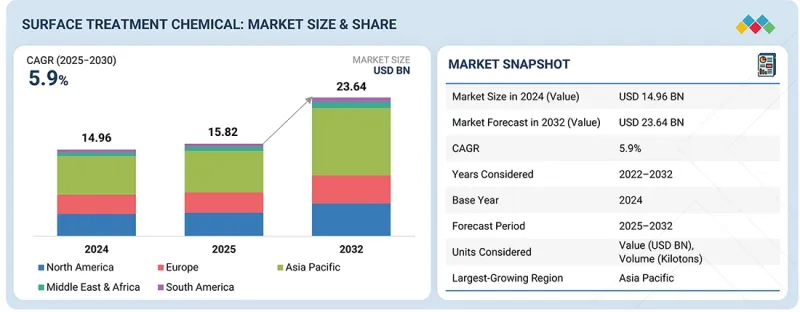

預計表面處理化學品市場將從 2025 年的 158.2 億美元成長到 2032 年的 236.4 億美元,預測期內複合年成長率為 5.9%。

| 調查範圍 | |

|---|---|

| 調查年度 | 2022-2032 |

| 基準年 | 2024 |

| 預測期 | 2025-2030 |

| 單元 | 金額(美元)和數量(千噸) |

| 部分 | 按產品類型、加工方法、基材、最終用戶產業和地區分類 |

| 目標區域 | 歐洲、北美、亞太地區、中東和非洲、南美 |

由於脫漆劑在去除金屬、木材和複合材料等表面的漆膜和殘留物方面發揮著至關重要的作用,因此它是表面處理化學品市場中成長速度第四快的產品類型。脫漆劑廣泛應用於汽車、航太、建築和工業維修業的噴漆、塗裝和維修預處理流程。化學脫漆劑能夠快速均勻地溶解頑固的漆膜,從而縮短施工時間並獲得高品質的處理效果。這種高效性使其成為大規模生產和再製造過程中不可或缺的化學物質。

從技術角度來看,現代脫漆劑採用溶劑型、鹼性和生物基化學技術來分解聚合物塗層,而不會傷害基材。這使得它們可用於多種材料,包括鋼、鋁、複合材料和塑膠。此外,它們還符合環保和安全法規,例如低VOC和無鉻。高效、廣泛的材料相容性和合規性等優勢,使得脫漆劑市場始終保持第二大市場佔有率。

“在預測期內,電氣和電子行業將成為成長最快的終端用戶行業”

這是由於電子設備的密度不斷提高、小型化程度不斷降低以及性能不斷提升,進而對錶面處理的精度、可靠性和耐久性提出了更高的要求。表面處理化學品對於確保印刷電路基板、連接器、半導體、機殼等零件的附著力、耐腐蝕性和電絕緣性至關重要。高密度元件的精密塗層、增強的溫度控管和絕緣性能,以及低VOC、無鹵素和符合RoHS指令等環保法規,都大大推動了市場對錶面處理化學品的需求。此外,5G基礎設施、物聯網設備、電動車電子產品和工業自動化等高附加價值應用的快速發展也推動了對特種表面處理化學品的需求。這些技術和法規因素的共同作用,已使電氣和電子產業穩居全球第三大終端用戶產業之列。

“預計在預測期內,歐洲將佔據第二大市場佔有率。”

歐洲擁有汽車、航太、工業機械和電子等先進工業領域,在全球表面處理化學品市場佔有第二大佔有率。大眾、空中巴士、寶馬和西門子等主要汽車製造商集中於此,廣泛採用先進的表面處理技術,用於防鏽、提高耐磨性和改善外觀。法國、德國和英國的航太業尤其擁有嚴格的安全和性能標準,推動了對高性能被覆劑和電鍍化學品的需求。此外,歐洲的環境法規,例如REACH法規(化學品註冊、評估、授權和限制)和ELV指令(報廢車輛指令),正在加速向低VOC、無六價鉻和環保化學品的轉型。這永續漢高、BASF、Chemetall和PPG工業等主要企業能夠將自身打造成為開發和供應永續高性能表面處理解決方案的中心。因此,歐洲有望繼續保持其在表面處理化學品市場的強大影響力,成為兼具永續性和技術創新的市場中心。

本報告調查了全球表面處理化學品市場,並提供了市場概況、影響市場成長的各種因素分析、技術和專利趨勢、法律制度、案例研究、市場規模趨勢和預測、按各個細分市場、地區/主要國家進行的詳細分析、競爭格局以及主要企業的概況。

目錄

第1章 引言

第2章調查方法

第3章執行摘要

第4章重要考察

第5章 市場概覽

- 市場動態

- 促進要素

- 抑制因素

- 機會

- 任務

- 波特五力分析

- 主要相關利益者和採購標準

- 總體經濟指標

- 價值鏈分析

- 生態系分析

- 案例研究分析

- 監管狀態

- 技術分析

- 影響客戶業務的趨勢/干擾因素

- 貿易分析

- 大型會議和活動

- 定價分析

- 投資和資金籌措方案

- 專利分析

- 2025年美國關稅的影響

6. 依產品類型分類的表面處理化學品市場

- 電鍍化學品

- 化學轉化塗層劑

- 陽極處理化學品

- 鈍化化學品

- 油漆去除劑

- 清潔工

- 其他

7. 依處理方法分類的表面處理化學品市場

- 電鍍

- 化學處理

- 熱噴塗

- 熱浸電鍍

- 其他

8. 依基材分類的表面處理化學品市場

- 金屬

- 塑膠

- 木頭

- 玻璃

- 複合材料

- 其他

9. 依終端用戶產業分類的表面處理化學品市場

- 運輸

- 建造

- 電機與電子工程

- 包裝

- 工業機械

- 纖維

- 其他

10. 各地區表面處理化學品市場

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他

- 中東和非洲

- 海灣合作理事會國家

- 南非

- 其他

- 南美洲

- 巴西

- 阿根廷

- 其他

第11章 競爭格局

- 概述

- 主要參與企業的策略/優勢

- 收入分析

- 市佔率分析

- 估值和財務指標

- 產品比較分析

- 公司評估矩陣:主要企業

- 公司估值矩陣:Start-Ups/中小企業

- 競爭場景

第12章:公司簡介

- 主要企業

- HENKEL AG & CO. KGAA

- CHEMETALL GMBH

- PPG INDUSTRIES, INC.

- MKS ATOTECH

- ELEMENT SOLUTIONS INC

- NIPPON PAINT HOLDINGS CO., LTD.

- NIHON PARKERIZING CO., LTD.

- AXALTA COATING SYSTEMS, LLC

- NOF CORPORATION

- DOW

- THE SHERWIN-WILLIAMS COMPANY

- AKZO NOBEL NV

- 其他主要企業

- QUAKER HOUGHTON

- MCGEAN-ROHCO INC.

- EVONIK

- JCU INTERNATIONAL, INC.

- CHEMBOND MATERIAL TECHNOLOGIES PVT. LTD.

- CHEMISCHE WERKE KLUTHE GMBH

- DUBOIS CHEMICALS

- WUHAN JADECHEM INTERNATIONAL TRADE CO., LTD.

- SURTEC

- CHEMTECH SURFACE FINISHING PVT. LTD.

- AUROMEX CO., LTD.

- VANCHEM PERFORMANCE CHEMICALS

- AD INTERNATIONAL BV

- COLUMBIA CHEMICAL

- ASTENA HOLDINGS CO., LTD.

- ARTEK SURFIN CHEMICALS LTD.

- GRAUER & WEIL (INDIA) LIMITED

第13章附錄

The surface treatment chemical market is projected to grow from USD 15.82 Billion in 2025 to USD 23.64 Billion by 2032, at a CAGR of 5.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million), Volume (Kilotons) |

| Segments | By Product Type, By Treatment Method, By Base Material, By End-Use Industry, and Region |

| Regions covered | Europe, North America, Asia Pacific, the Middle East & Africa, and South America |

Paint strippers is expected to be fourth fastest growing product type in the surface treatment chemical market due to their critical role in removing coatings, paints, and surface residues from metal, wood, and composite substrates across multiple industries. They are widely used in automotive, aerospace, construction, and industrial maintenance for surface preparation before painting, coating, or repair. The effectiveness of chemical paint strippers in dissolving tough coatings quickly and uniformly reduces labor time and ensures high-quality finishing, making them indispensable in large-scale manufacturing and refurbishment operations.

Technically, modern paint strippers leverage solvents, alkaline solutions, and innovative bio-based chemistries that penetrate and break down polymeric coatings without damaging the substrate. This versatility allows them to handle diverse materials-steel, aluminum, composites, and plastics-while meeting stricter environmental and safety regulations, such as low-VOC and chromium-free formulations. The combination of high efficiency, broad material compatibility, and regulatory compliance drives strong demand, maintaining paint strippers as the second-largest segment in the surface treatment chemical market..

''In terms of value, plastic as base material is expected to be the fastest growing of the overall surface treatment chemical market.''

Plastics hold the fastest growing market as a base material in the surface treatment chemical market due to several unique technical and industrial factors. The rapid adoption of high-performance engineering plastics (such as PEEK, Nylon, and polyimides) in sectors like automotive, electronics, and medical devices has increased the need for specialized chemical treatments to enhance surface functionality, such as scratch resistance, chemical resistance, and thermal stability.

Plastics often require anti-static, hydrophobic, or hydrophilic surface properties, depending on the application-necessitating advanced chemical treatments like plasma-assisted or chemical etching processes. As industries shift toward lightweighting and flexible components, more intricate plastic geometries are used, demanding precise and uniform surface treatments that only specialized chemical solutions can achieve. Increasing regulatory pressure for environmentally safe and non-toxic surface treatment solutions in consumer-facing plastic products has encouraged the use of engineered chemicals that provide performance without compromising safety or compliance.

"During the forecast period, electrical & electronics end use industry is projected to have fastest growing market."

The Electrical & Electronics sector accounts for the fastest growing end-use segment in the surface treatment chemical market, driven by the increasing complexity, miniaturization, and performance requirements of modern electronic devices. Surface treatment chemicals play a critical role in ensuring reliable adhesion, corrosion resistance, and electrical insulation for components such as printed circuit boards, connectors, semiconductors, and housings. Demand is underpinned by the need for precise coating deposition on high-density components, enhanced thermal management and dielectric properties, and compliance with global environmental and safety regulations, including low-VOC, halogen-free, and RoHS standards. The rapid adoption of high-value applications, including 5G infrastructure, IoT devices, EV electronics, and industrial automation, further drives the use of specialized surface treatment chemistries tailored to diverse substrates. Collectively, these technical and regulatory factors solidify Electrical & Electronics as the third-largest end-use segment in the surface treatment chemical market.

"During the forecast period, the surface treatment chemical market in Europe region is projected to have second largest market share."

Europe holds the second-largest share of the global surface treatment chemical market, supported by its well-established automotive, aerospace, industrial machinery, and electronics sectors. The region is home to leading OEMs such as Volkswagen, Airbus, BMW, and Siemens, all of which require advanced surface treatment solutions for corrosion protection, wear resistance, and improved aesthetic finishes. The aerospace hubs in France, Germany, and the UK are particularly significant, as the stringent performance and safety standards in aviation necessitate the use of high-performance coatings and plating chemicals. Another driver is Europe's strict regulatory framework, such as REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals) and ELV (End-of-Life Vehicles) directives, which have accelerated the adoption of eco-friendly, low-VOC, and hexavalent-chromium-free surface treatment formulations. This has prompted innovation from major players like Henkel AG & Co. KGaA, BASF SE, Chemetall GmbH, and PPG Industries, positioning Europe as a hub for sustainable and advanced solutions.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type- Tier 1- 60%, Tier 2- 20%, and Tier 3- 20%

- By Designation- C Level- 33%, Director Level- 33%, and Managers- 34%

- By Region- North America- 20%, Europe- 25%, Asia Pacific- 25%, Middle East & Africa- 15%, and Latin America- 15%

The report provides a comprehensive analysis of company profiles:

Prominent companies Chemetall gmbH (Germany), Henkel AG & Co. KGaA (Germany), Nippon Paint Holdings Co., Ltd. (Japan), PPG INDUSTRIES, INC. (US), Nihon Parkerizing Co., Ltd. (Japan), MKS Atotech (Germany), Element Solutions Inc (US), Axalta Coating Systems , LLC (US), Dow (US), The Sherwin-Williams Compant (US), AkzoNobel (Netherlands).

Research Coverage

This research report categorizes the surface treatment chemical market by product type (Plating Chemicals, Conversion Coating, Anodizing Chemicals, Passivation Chemicals, Paint Strippers, Cleaners Others), by treatment Method (Electroplating, Chemical Treatment, Thermal Spraying, Hot Dipping and Other), by Base Material (Metals, Plastics, Wood, Glass and Composites). End-Use Industry Region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the surface treatment chemical market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted in order to provide insights into their business overview, solutions, and services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the surface treatment chemical market are all covered. This report includes a competitive analysis of upcoming startups in the surface treatment chemical market ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall surface treatment chemical market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Robust demand from automotive sectors, Semiconductor growth creating demand in the market), restraints (Stringent compliance standards pose barriers to surface treatment chemical market), opportunities (Technological advancements in smart treatments, Growing adoption of lightweight aluminum alloys in EVs driving need for specialized pretreatment and coating solutions) and challenges (High costs and technical hurdles in adopting surface treatment chemicals)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the surface treatment chemical market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the surface treatment chemical market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the surface treatment chemical market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Chemetall gmbH (Germany), Henkel AG & Co. KGaA (Germany), Nippon Paint Holdings Co., Ltd. (Japan), PPG INDUSTRIES, INC. (US), Nihon Parkerizing Co., Ltd. (Japan), MKS Atotech (Germany), Element Solutions Inc (US), Axalta Coating Systems , LLC (US), Dow (US), The Sherwin-Williams Compant (US), AkzoNobel (Netherlands) among others in the surface treatment chemical market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 List of primary interview participants-demand and supply sides

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of interviews with experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 FORECAST NUMBER CALCULATION

- 2.4 DATA TRIANGULATION

- 2.5 FACTOR ANALYSIS

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 OPPORTUNITIES FOR PLAYERS IN SURFACE TREATMENT CHEMICALS MARKET

- 4.2 SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE

- 4.3 SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD

- 4.4 SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL

- 4.5 SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY

- 4.6 SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Robust demand from automotive sector

- 5.2.1.2 Semiconductor industry growth creating demand

- 5.2.1.3 Industrialization and infrastructure growth in emerging economies

- 5.2.2 RESTRAINTS

- 5.2.2.1 Stringent compliance standards

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Technological advancements in smart treatments

- 5.2.3.2 Growing adoption of lightweight aluminum alloys in EVs demanding specialized pretreatment and coating solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 High costs and technical hurdles in adopting surface treatment chemicals

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 BARGAINING POWER OF SUPPLIERS

- 5.3.2 BARGAINING POWER OF BUYERS

- 5.3.3 THREAT OF NEW ENTRANTS

- 5.3.4 THREAT OF SUBSTITUTES

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.4 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.4.2 BUYING CRITERIA

- 5.5 MACROECONOMIC INDICATORS

- 5.5.1 GLOBAL GDP TRENDS

- 5.6 VALUE CHAIN ANALYSIS

- 5.6.1 RAW MATERIAL SUPPLIERS

- 5.6.2 MANUFACTURERS

- 5.6.3 DISTRIBUTORS

- 5.6.4 END USERS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 CASE STUDY ANALYSIS

- 5.8.1 HOUGHTON DELIVERS SUSTAINABLE SURFACE SOLUTIONS FOR AUTOMOTIVE AND AEROSPACE INDUSTRIES

- 5.8.2 DUBOIS TRANSFORMS PRETREATMENT CHALLENGES INTO SUSTAINABLE RESULTS

- 5.8.3 YAMAHA AND METALUMEN ACHIEVE NEXT-LEVEL PERFORMANCE WITH VANCHEM SOLUTIONS

- 5.9 REGULATORY LANDSCAPE

- 5.9.1 REGULATIONS

- 5.9.1.1 Europe

- 5.9.1.2 Asia Pacific

- 5.9.1.3 North America

- 5.9.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.9.1 REGULATIONS

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGIES

- 5.10.1.1 Enabling 2.xD/3D packaging through chemistry

- 5.10.1.2 Advanced functional and nanostructured coatings

- 5.10.2 COMPLEMENTARY TECHNOLOGIES

- 5.10.2.1 Laser-assisted surface preparation

- 5.10.1 KEY TECHNOLOGIES

- 5.11 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.12 TRADE ANALYSIS

- 5.12.1 EXPORT SCENARIO

- 5.12.2 IMPORT SCENARIO

- 5.13 KEY CONFERENCES AND EVENTS, 2025-2027

- 5.14 PRICING ANALYSIS

- 5.14.1 AVERAGE SELLING PRICE TREND OF SURFACE TREATMENT CHEMICALS, BY REGION, 2022-2024

- 5.14.2 AVERAGE SELLING PRICE TREND OF SURFACE TREATMENT CHEMICALS, BY APPLICATION, 2022-2024

- 5.14.3 AVERAGE SELLING PRICES OF SURFACE TREATMENT CHEMICALS OFFERED BY KEY PLAYERS, BY APPLICATION, 2024

- 5.15 INVESTMENT AND FUNDING SCENARIO

- 5.16 PATENT ANALYSIS

- 5.16.1 APPROACH

- 5.16.2 DOCUMENT TYPES

- 5.16.3 PUBLICATION TRENDS, 2014-2024

- 5.16.4 INSIGHTS

- 5.16.5 LEGAL STATUS OF PATENTS

- 5.16.6 JURISDICTION ANALYSIS FROM 2014 TO 2024

- 5.16.7 TOP COMPANIES/APPLICANTS

- 5.16.8 TOP 10 PATENT OWNERS (US) 2014-2024

- 5.17 IMPACT OF 2025 US TARIFF - SURFACE TREATMENT CHEMICALS MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON KEY COUNTRIES/REGIONS

- 5.17.4.1 North America

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.5 IMPACT ON END-USE INDUSTRIES

6 SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE

- 6.1 INTRODUCTION

- 6.2 PLATING CHEMICAL

- 6.2.1 ENHANCED CORROSION RESISTANCE, WEAR RESISTANCE, AND ELECTRICAL CONDUCTIVITY

- 6.3 CONVERSION COATING

- 6.3.1 RELIABLE PRETREATMENT FOR AUTOMOTIVE AND INDUSTRIAL METALS

- 6.4 ANODIZING CHEMICAL

- 6.4.1 TRANSFORMING SURFACES WITH INNOVATIVE ANODIZING CHEMICALS

- 6.5 PASSIVATION CHEMICAL

- 6.5.1 PASSIVATION FOR HIGH-INTEGRITY STAINLESS STEEL APPLICATIONS

- 6.6 PAINT STRIPPER

- 6.6.1 PROTECTING SUBSTRATES WHILE REMOVING COATINGS

- 6.7 CLEANERS

- 6.7.1 INDUSTRIAL CLEANERS THAT PROTECT AND PREPARE SURFACES

- 6.8 OTHER PRODUCT TYPES

7 SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD

- 7.1 INTRODUCTION

- 7.2 ELECTROPLATING

- 7.2.1 ENHANCING DURABILITY AND FUNCTIONALITY WITH ELECTROPLATING

- 7.3 CHEMICAL TREATMENT

- 7.3.1 IMPROVING PAINT ADHESION AND COATING DURABILITY

- 7.4 THERMAL SPRAYING

- 7.4.1 PROTECTIVE AND FUNCTIONAL COATINGS FOR EXTREME ENVIRONMENTS

- 7.5 HOT DIPPING

- 7.5.1 RELIABLE IN APPLICATIONS WHERE DURABILITY AND LOW MAINTENANCE ARE ESSENTIAL

- 7.6 OTHER TREATMENT METHODS

8 SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL

- 8.1 INTRODUCTION

- 8.2 METALS

- 8.2.1 ADVANCED METAL PRETREATMENT FOR HIGH-QUALITY FINISHES

- 8.3 PLASTICS

- 8.3.1 IMPROVING WETTABILITY AND ADHESION ON POLYOLEFINS

- 8.4 WOOD

- 8.4.1 PROTECTING WOOD WHILE MAINTAINING TEXTURE AND FINISH

- 8.5 GLASS

- 8.5.1 SUPERIOR ADHESION AND ELECTRICAL PERFORMANCE FOR GLASS

- 8.6 COMPOSITES

- 8.6.1 HIGH-PRECISION TREATMENTS FOR ENHANCED COMPOSITE ADHESION

- 8.7 OTHER BASE MATERIALS

9 SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY

- 9.1 INTRODUCTION

- 9.2 TRANSPORTATION

- 9.2.1 RUST PROTECTION AS CORE TRANSPORTATION PRIORITY

- 9.3 CONSTRUCTION

- 9.3.1 IMPROVING INFRASTRUCTURE RESILIENCE THROUGH SURFACE TREATMENTS

- 9.4 ELECTRICAL & ELECTRONICS

- 9.4.1 PROTECTING ELECTRONICS WITH CORROSION-RESISTANT COATINGS

- 9.5 PACKAGING

- 9.5.1 RISING IMPORTANCE OF SURFACE PREPARATION FOR PACKAGING MATERIALS

- 9.6 INDUSTRIAL MACHINERY

- 9.6.1 SURFACE CLEANING AND PREPARATION FOR HEAVY-DUTY APPLICATIONS

- 9.7 TEXTILES

- 9.7.1 EXPANDING APPLICATIONS OF FUNCTIONAL TEXTILE TREATMENTS

- 9.8 OTHER END-USE INDUSTRIES

10 SURFACE TREATMENT CHEMICALS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 US

- 10.2.1.1 Growing demand for automobiles influenced by EV sales to drive market

- 10.2.2 CANADA

- 10.2.2.1 Government investment to reduce import reliance to benefit automotive sector

- 10.2.3 MEXICO

- 10.2.3.1 Manufacturing and nearshoring to drive industrial market

- 10.2.1 US

- 10.3 EUROPE

- 10.3.1 GERMANY

- 10.3.1.1 Fast growth of electrical & electronics industry to drive market

- 10.3.2 FRANCE

- 10.3.2.1 Transportation and construction to drive market

- 10.3.3 UK

- 10.3.3.1 Automotive export orientation propels market

- 10.3.4 ITALY

- 10.3.4.1 Robust manufacturing base across electrical & electronics to drive market

- 10.3.5 SPAIN

- 10.3.5.1 Growing applications in automotive and electronic industries to drive market

- 10.3.6 REST OF EUROPE

- 10.3.1 GERMANY

- 10.4 ASIA PACIFIC

- 10.4.1 CHINA

- 10.4.1.1 Growing population, industrialization, and urbanization to support market

- 10.4.2 JAPAN

- 10.4.2.1 Evolving electrical & electronics industry to increase demand

- 10.4.3 INDIA

- 10.4.3.1 Growing FDI in manufacturing industry to support market growth

- 10.4.4 SOUTH KOREA

- 10.4.4.1 Government initiative to drive market

- 10.4.5 REST OF ASIA PACIFIC

- 10.4.1 CHINA

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 GCC COUNTRIES

- 10.5.1.1 Saudi Arabia

- 10.5.1.1.1 Saudi Vision 2030 to drive market

- 10.5.1.2 Rest of GCC countries

- 10.5.1.1 Saudi Arabia

- 10.5.2 SOUTH AFRICA

- 10.5.2.1 Construction to support steady market growth

- 10.5.3 REST OF MIDDLE EAST & AFRICA

- 10.5.1 GCC COUNTRIES

- 10.6 SOUTH AMERICA

- 10.6.1 BRAZIL

- 10.6.1.1 Construction industry to drive market

- 10.6.2 ARGENTINA

- 10.6.2.1 Transportation sector to drive market

- 10.6.3 REST OF SOUTH AMERICA

- 10.6.1 BRAZIL

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 11.3 REVENUE ANALYSIS

- 11.4 MARKET SHARE ANALYSIS

- 11.4.1 HENKEL AG & CO. KGAA

- 11.4.2 CHEMETALL GMBH

- 11.4.3 PPG INDUSTRIES, INC.

- 11.4.4 MKS ATOTECH

- 11.4.5 ELEMENT SOLUTIONS INC.

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.6 PRODUCT COMPARISON ANALYSIS

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.7.5.1 Company footprint

- 11.7.5.2 Region footprint

- 11.7.5.3 Product type footprint

- 11.7.5.4 Treatment method footprint

- 11.7.5.5 Base material footprint

- 11.7.5.6 End-use industry footprint

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2024

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of key startups/SMEs

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES

- 11.9.2 EXPANSIONS

- 11.9.3 DEALS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 HENKEL AG & CO. KGAA

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 CHEMETALL GMBH

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Expansions

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 PPG INDUSTRIES, INC.

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 MnM view

- 12.1.4 MKS ATOTECH

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 ELEMENT SOLUTIONS INC

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Expansions

- 12.1.5.4 Recent developments

- 12.1.5.4.1 Deals

- 12.1.5.5 MnM view

- 12.1.5.5.1 Key strengths

- 12.1.5.5.2 Strategic choices

- 12.1.5.5.3 Weaknesses and competitive threats

- 12.1.6 NIPPON PAINT HOLDINGS CO., LTD.

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product Launches

- 12.1.6.4 MnM view

- 12.1.6.4.1 Key strengths

- 12.1.6.4.2 Strategic choices

- 12.1.6.4.3 Weaknesses and competitive threats

- 12.1.7 NIHON PARKERIZING CO., LTD.

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Expansions

- 12.1.7.4 MnM view

- 12.1.7.4.1 Key strengths

- 12.1.7.4.2 Strategic choices

- 12.1.7.4.3 Weaknesses and competitive threats

- 12.1.8 AXALTA COATING SYSTEMS, LLC

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 MnM view

- 12.1.9 NOF CORPORATION

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.9.3 MnM view

- 12.1.10 DOW

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.10.3 MnM view

- 12.1.11 THE SHERWIN-WILLIAMS COMPANY

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.11.3 MnM view

- 12.1.12 AKZO NOBEL N.V.

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.12.3 MnM view

- 12.1.1 HENKEL AG & CO. KGAA

- 12.2 OTHER KEY PLAYERS

- 12.2.1 QUAKER HOUGHTON

- 12.2.2 MCGEAN-ROHCO INC.

- 12.2.3 EVONIK

- 12.2.4 JCU INTERNATIONAL, INC.

- 12.2.5 CHEMBOND MATERIAL TECHNOLOGIES PVT. LTD.

- 12.2.6 CHEMISCHE WERKE KLUTHE GMBH

- 12.2.7 DUBOIS CHEMICALS

- 12.2.8 WUHAN JADECHEM INTERNATIONAL TRADE CO., LTD.

- 12.2.9 SURTEC

- 12.2.10 CHEMTECH SURFACE FINISHING PVT. LTD.

- 12.2.11 AUROMEX CO., LTD.

- 12.2.12 VANCHEM PERFORMANCE CHEMICALS

- 12.2.13 AD INTERNATIONAL B.V.

- 12.2.14 COLUMBIA CHEMICAL

- 12.2.15 ASTENA HOLDINGS CO., LTD.

- 12.2.16 ARTEK SURFIN CHEMICALS LTD.

- 12.2.17 GRAUER & WEIL (INDIA) LIMITED

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS

List of Tables

- TABLE 1 SURFACE TREATMENT CHEMICALS MARKET: MOTOR VEHICLE PRODUCTION BY KEY COUNTRIES IN 2024 (UNITS)

- TABLE 2 SURFACE TREATMENT CHEMICALS MARKET: IMPACT OF PORTER'S FIVE FORCES

- TABLE 3 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR KEY END-USE INDUSTRIES (%)

- TABLE 4 KEY BUYING CRITERIA FOR KEY END-USE INDUSTRIES

- TABLE 5 PROJECTED REAL GDP GROWTH (ANNUAL PERCENT CHANGE) OF KEY COUNTRIES, 2021-2030

- TABLE 6 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 7 SURFACE TREATMENT CHEMICALS MARKET: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 SURFACE TREATMENT CHEMICALS MARKET: KEY CONFERENCES AND EVENTS, 2025-2027

- TABLE 9 AVERAGE SELLING PRICE TREND OF SURFACE TREATMENT CHEMICALS, BY REGION, 2022-2024 (USD/KG)

- TABLE 10 TOTAL PATENT COUNT FOR YEAR 2014-2024

- TABLE 11 TOP 10 PATENT OWNERS 2014-2014

- TABLE 12 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 13 SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 14 SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (USD MILLION)

- TABLE 15 SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 16 SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (KILOTON)

- TABLE 17 SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (USD MILLION)

- TABLE 18 SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (USD MILLION)

- TABLE 19 SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (KILOTON)

- TABLE 20 SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (KILOTON)

- TABLE 21 SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (USD MILLION)

- TABLE 22 SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (USD MILLION)

- TABLE 23 SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (KILOTON)

- TABLE 24 SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (KILOTON)

- TABLE 25 SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 26 SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 27 SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 28 SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 29 SURFACE TREATMENT CHEMICALS MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 30 SURFACE TREATMENT CHEMICALS MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 31 SURFACE TREATMENT CHEMICALS MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 32 SURFACE TREATMENT CHEMICALS MARKET, BY REGION, 2025-2032 (KILOTON)

- TABLE 33 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 34 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 35 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 36 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2025-2032 (KILOTON)

- TABLE 37 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 38 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (USD MILLION)

- TABLE 39 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 40 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (KILOTON)

- TABLE 41 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (USD MILLION)

- TABLE 42 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (USD MILLION)

- TABLE 43 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (KILOTON)

- TABLE 44 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (KILOTON)

- TABLE 45 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (USD MILLION)

- TABLE 46 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (USD MILLION)

- TABLE 47 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (KILOTON)

- TABLE 48 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (KILOTON)

- TABLE 49 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 50 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 51 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 52 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 53 US: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 54 US: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 55 US: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 56 US: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 57 CANADA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 58 CANADA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 59 CANADA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 60 CANADA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 61 MEXICO: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 62 MEXICO: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 63 MEXICO: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 64 MEXICO: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 65 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 66 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 67 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 68 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2025-2032 (KILOTON)

- TABLE 69 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 70 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (USD MILLION)

- TABLE 71 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 72 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (KILOTON)

- TABLE 73 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (USD MILLION)

- TABLE 74 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (USD MILLION)

- TABLE 75 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (KILOTON)

- TABLE 76 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (KILOTON)

- TABLE 77 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (USD MILLION)

- TABLE 78 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (USD MILLION)

- TABLE 79 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (KILOTON)

- TABLE 80 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (KILOTON)

- TABLE 81 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 82 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 83 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 84 EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 85 GERMANY: SURFACE TREATMENT CHEMICALS MARKET, BY, 2022-2024 (USD MILLION)

- TABLE 86 GERMANY: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 87 GERMANY: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 88 GERMANY: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 89 FRANCE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 90 FRANCE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 91 FRANCE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 92 FRANCE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 93 UK: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 94 UK: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 95 UK: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 96 UK: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 97 ITALY: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 98 ITALY: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 99 ITALY: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 100 ITALY: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 101 SPAIN: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 102 SPAIN: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 103 SPAIN: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 104 SPAIN: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 105 REST OF EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 106 REST OF EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 107 REST OF EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 108 REST OF EUROPE: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 109 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 110 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 111 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 112 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2025-2032 (KILOTON)

- TABLE 113 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 114 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (USD MILLION)

- TABLE 115 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 116 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (KILOTON)

- TABLE 117 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (USD MILLION)

- TABLE 118 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (USD MILLION)

- TABLE 119 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (KILOTON)

- TABLE 120 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (KILOTON)

- TABLE 121 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (USD MILLION)

- TABLE 122 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (USD MILLION)

- TABLE 123 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (KILOTON)

- TABLE 124 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (KILOTON)

- TABLE 125 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 126 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 127 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 128 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 129 CHINA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 130 CHINA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 131 CHINA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 132 CHINA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 133 JAPAN: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 134 JAPAN: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 135 JAPAN: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 136 JAPAN: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 137 INDIA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 138 INDIA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 139 INDIA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 140 INDIA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 141 SOUTH KOREA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 142 SOUTH KOREA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 143 SOUTH KOREA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 144 SOUTH KOREA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 145 REST OF ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 146 REST OF ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 147 REST OF ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 148 REST OF ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 149 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 150 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 151 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 152 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2025-2032 (KILOTON)

- TABLE 153 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 154 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (USD MILLION)

- TABLE 155 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 156 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (KILOTON)

- TABLE 157 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (USD MILLION)

- TABLE 158 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (USD MILLION)

- TABLE 159 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (KILOTON)

- TABLE 160 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (KILOTON)

- TABLE 161 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (USD MILLION)

- TABLE 162 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (USD MILLION)

- TABLE 163 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (KILOTON)

- TABLE 164 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (KILOTON)

- TABLE 165 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USER, 2022-2024 (USD MILLION)

- TABLE 166 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USER, 2025-2032 (USD MILLION)

- TABLE 167 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USER, 2022-2024 (KILOTON)

- TABLE 168 MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USER, 2025-2032 (KILOTON)

- TABLE 169 SAUDI ARABIA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 170 SAUDI ARABIA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 171 SAUDI ARABIA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 172 SAUDI ARABIA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 173 REST OF GCC COUNTRIES: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 174 REST OF GCC COUNTRIES: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 175 REST OF GCC COUNTRIES: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 176 REST OF GCC COUNTRIES: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 177 SOUTH AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 178 SOUTH AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 179 SOUTH AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 180 SOUTH AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 181 REST OF MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 182 REST OF MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 183 REST OF MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 184 REST OF MIDDLE EAST & AFRICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 185 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 186 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 187 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 188 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY, 2025-2032 (KILOTON)

- TABLE 189 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 190 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (USD MILLION)

- TABLE 191 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 192 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE, 2025-2032 (KILOTON)

- TABLE 193 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (USD MILLION)

- TABLE 194 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (USD MILLION)

- TABLE 195 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2022-2024 (KILOTON)

- TABLE 196 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD, 2025-2032 (KILOTON)

- TABLE 197 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (USD MILLION)

- TABLE 198 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (USD MILLION)

- TABLE 199 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2022-2024 (KILOTON)

- TABLE 200 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL, 2025-2032 (KILOTON)

- TABLE 201 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 202 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 203 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 204 SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 205 BRAZIL: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 206 BRAZIL: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 207 BRAZIL: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 208 BRAZIL: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 209 ARGENTINA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 210 ARGENTINA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 211 ARGENTINA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 212 ARGENTINA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 213 REST OF SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 214 REST OF SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (USD MILLION)

- TABLE 215 REST OF SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 216 REST OF SOUTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY, 2025-2032 (KILOTON)

- TABLE 217 SURFACE TREATMENT CHEMICALS MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY MANUFACTURERS, 2021-2025

- TABLE 218 SURFACE TREATMENT CHEMICALS MARKET: DEGREE OF COMPETITION, 2024

- TABLE 219 SURFACE TREATMENT CHEMICALS MARKET: REGION FOOTPRINT

- TABLE 220 SURFACE TREATMENT CHEMICALS MARKET: PRODUCT TYPE FOOTPRINT

- TABLE 221 SURFACE TREATMENT CHEMICALS MARKET: TREATMENT METHOD FOOTPRINT

- TABLE 222 SURFACE TREATMENT CHEMICALS MARKET: BASE MATERIAL FOOTPRINT

- TABLE 223 SURFACE TREATMENT CHEMICALS MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 224 SURFACE TREATMENT CHEMICALS MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 225 SURFACE TREATMENT CHEMICALS MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- TABLE 226 SURFACE TREATMENT CHEMICALS MARKET: PRODUCT LAUNCHES, JANUARY 2021-JUNE 2025

- TABLE 227 SURFACE CHEMICAL TREATMENT MARKET: EXPANSIONS, JANUARY 2021-JUNE 2025

- TABLE 228 SURFACE TREATMENT CHEMICAL: DEALS, JANUARY 2021-JUNE 2025

- TABLE 229 HENKEL AG & CO. KGAA: COMPANY OVERVIEW

- TABLE 230 HENKEL AG & CO. KGAA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 231 HENKEL AG & CO. KGAA: DEALS, JANUARY 2021-JUNE 2025

- TABLE 232 CHEMETALL GMBH: COMPANY OVERVIEW

- TABLE 233 CHEMETALL GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 234 CHEMETALL GMBH: EXPANSIONS, JANUARY 2021-JUNE 2025

- TABLE 235 PPG INDUSTRIES, INC.: COMPANY OVERVIEW

- TABLE 236 PPG INDUSTRIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 MKS ATOTECH: COMPANY OVERVIEW

- TABLE 238 MKS ATOTECH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 239 MKS ATOTECH: DEALS, JANUARY 2021-JUNE 2025

- TABLE 240 ELEMENT SOLUTIONS INC: COMPANY OVERVIEW

- TABLE 241 ELEMENT SOLUTIONS INC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 242 ELEMENT SOLUTIONS INC: EXPANSIONS, JANUARY 2021-JUNE 2025

- TABLE 243 ELEMENT SOLUTIONS INC: DEALS, JANUARY 2021-JUNE 2025

- TABLE 244 NIPPON PAINT HOLDINGS CO., LTD.: COMPANY OVERVIEW

- TABLE 245 NIPPON PAINT HOLDINGS CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 246 NIPPON PAINT HOLDINGS CO., LTD.: PRODUCT LAUNCHES, JANUARY 2021-JUNE 2025

- TABLE 247 NIHON PARKERIZING CO., LTD.: COMPANY OVERVIEW

- TABLE 248 NIHON PARKERIZING CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 249 NIHON PARKERIZING CO., LTD.: EXPANSIONS, JANUARY 2021-JUNE 2025

- TABLE 250 AXALTA COATING SYSTEMS, LLC: COMPANY OVERVIEW

- TABLE 251 AXALTA COATING SYSTEMS, LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 252 NOF CORPORATION: COMPANY OVERVIEW

- TABLE 253 NOF CORPORATION.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 254 DOW: COMPANY OVERVIEW

- TABLE 255 DOW: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 256 THE SHERWIN-WILLIAMS COMPANY

- TABLE 257 THE SHERWIN-WILLIAMS COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 258 AKZO NOBEL N.V.: COMPANY OVERVIEW

- TABLE 259 AKZO NOBEL N.V.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 260 QUAKER HOUGHTON: COMPANY OVERVIEW

- TABLE 261 MCGEAN-ROHCO INC.: COMPANY OVERVIEW

- TABLE 262 EVONIK: COMPANY OVERVIEW

- TABLE 263 JCU INTERNATIONAL, INC.: COMPANY OVERVIEW

- TABLE 264 CHEMBOND MATERIAL TECHNOLOGIES PVT. LTD.: COMPANY OVERVIEW

- TABLE 265 CHEMISCHE WERKE KLUTHE GMBH: COMPANY OVERVIEW

- TABLE 266 DUBOIS CHEMICALS: COMPANY OVERVIEW

- TABLE 267 WUHAN JADECHEM INTERNATIONAL TRADE CO., LTD.: COMPANY OVERVIEW

- TABLE 268 SURTEC: COMPANY OVERVIEW

- TABLE 269 CHEMTECH SURFACE FINISHING PVT. LTD.: COMPANY OVERVIEW

- TABLE 270 AUROMEX CO., LTD.: COMPANY OVERVIEW

- TABLE 271 VANCHEM PERFORMANCE CHEMICALS: COMPANY OVERVIEW

- TABLE 272 AD INTERNATIONAL B.V.: COMPANY OVERVIEW

- TABLE 273 COLUMBIA CHEMICAL: COMPANY OVERVIEW

- TABLE 274 ASTENA HOLDINGS CO., LTD.: COMPANY OVERVIEW

- TABLE 275 ARTEK SURFIN CHEMICALS LTD.: COMPANY OVERVIEW

- TABLE 276 GRAUER & WEIL (INDIA) LIMITED: COMPANY OVERVIEW

List of Figures

- FIGURE 1 SURFACE TREATMENT CHEMICALS MARKET: SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 SURFACE TREATMENT CHEMICALS MARKET: RESEARCH DESIGN

- FIGURE 3 SURFACE TREATMENT CHEMICALS MARKET: BOTTOM-UP APPROACH

- FIGURE 4 SURFACE TREATMENT CHEMICALS MARKET: TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 6 DEMAND-SIDE FORECAST PROJECTIONS

- FIGURE 7 SURFACE TREATMENT CHEMICALS MARKET: DATA TRIANGULATION

- FIGURE 8 PLATING CHEMICALS SEGMENT TO HOLD LARGEST MARKET SHARE IN 2032

- FIGURE 9 ELECTROPLATING SEGMENT TO LEAD MARKET IN 2032

- FIGURE 10 PLASTICS SEGMENT TO GROW FASTEST DURING FORECAST PERIOD

- FIGURE 11 TRANSPORTATION INDUSTRY TO BE LARGEST DURING FORECAST PERIOD

- FIGURE 12 ASIA PACIFIC TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 13 EMERGING ECONOMIES TO OFFER ATTRACTIVE OPPORTUNITIES DURING FORECAST PERIOD

- FIGURE 14 PLATING CHEMICALS TO CAPTURE LARGEST MARKET SHARE BY 2032

- FIGURE 15 ELECTROPLATING TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 16 METALS TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 17 TRANSPORTATION INDUSTRY TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 18 MARKET IN INDIA TO REGISTER HIGHEST CAGR FROM 2025 TO 2032

- FIGURE 19 SURFACE TREATMENT CHEMICALS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 20 SURFACE TREATMENT CHEMICALS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 21 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF KEY END-USE INDUSTRIES

- FIGURE 22 KEY BUYING CRITERIA FOR KEY END-USE INDUSTRIES

- FIGURE 23 SURFACE TREATMENT CHEMICALS MARKET VALUE CHAIN

- FIGURE 24 SURFACE TREATMENT CHEMICALS MARKET: ECOSYSTEM

- FIGURE 25 SURFACE TREATMENT CHEMICALS MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 26 EXPORT DATA FOR HS CODE 340290-COMPLIANT PRODUCTS, BY COUNTRY (USD THOUSAND)

- FIGURE 27 IMPORT DATA HS CODE 340290-COMPLIANT PRODUCTS, BY COUNTRY (USD THOUSAND)

- FIGURE 28 AVERAGE SELLING PRICE TREND OF SURFACE TREATMENT CHEMICALS, BY REGION (USD/KG), 2022-2024

- FIGURE 29 AVERAGE SELLING PRICE TREND OF SURFACE TREATMENT CHEMICALS, BY APPLICATION (USD/KG), 2022-2024

- FIGURE 30 AVERAGE SELLING PRICES OF SURFACE TREATMENT CHEMICALS OFFERED BY KEY PLAYERS, BY APPLICATION (USD/KG)

- FIGURE 31 SURFACE TREATMENT CHEMICALS MARKET: INVESTMENT AND FUNDING SCENARIO

- FIGURE 32 TOTAL NUMBER OF PATENTS FOR 2014-2024

- FIGURE 33 NUMBER OF PATENTS YEAR-WISE FROM 2014 TO 2024

- FIGURE 34 PATENT ANALYSIS, BY LEGAL STATUS

- FIGURE 35 TOP JURISDICTIONS, BY DOCUMENT FROM 2014 TO 2024

- FIGURE 36 TOP 10 COMPANIES/APPLICANTS WITH HIGHEST NUMBER OF PATENTS FOR 2014-2024

- FIGURE 37 PLATING CHEMICALS SEGMENT TO HOLD LARGER SHARE OF SURFACE TREATMENT CHEMICALS MARKET IN 2025

- FIGURE 38 ELECTROPLATING TREATMENT METHOD TO HOLD LARGER SHARE OF SURFACE TREATMENT CHEMICALS MARKET IN 2025

- FIGURE 39 METALS SEGMENT TO LEAD SURFACE TREATMENT CHEMICALS MARKET IN 2025

- FIGURE 40 TRANSPORTATION SEGMENT TO HOLD LARGEST SHARE OF SURFACE TREATMENT CHEMICALS MARKET IN 2025

- FIGURE 41 INDIA TO BE FASTEST-GROWING MARKET FOR SURFACE TREATMENT CHEMICALS DURING FORECAST PERIOD

- FIGURE 42 NORTH AMERICA: SURFACE TREATMENT CHEMICALS MARKET SNAPSHOT

- FIGURE 43 ASIA PACIFIC: SURFACE TREATMENT CHEMICALS MARKET SNAPSHOT

- FIGURE 44 SURFACE TREATMENT CHEMICALS MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2022-2024 (USD BILLION)

- FIGURE 45 SURFACE TREATMENT CHEMICALS MARKET SHARE ANALYSIS, 2024

- FIGURE 46 SURFACE TREATMENT CHEMICALS MARKET: COMPANY VALUATION OF KEY COMPANIES, 2024 (USD BILLION)

- FIGURE 47 SURFACE TREATMENT CHEMICALS MARKET: FINANCIAL METRICS OF KEY COMPANIES, 2024

- FIGURE 48 SURFACE TREATMENT CHEMICALS MARKET: PRODUCT COMPARISON

- FIGURE 49 SURFACE TREATMENT CHEMICALS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 50 SURFACE TREATMENT CHEMICALS MARKET: COMPANY FOOTPRINT

- FIGURE 51 SURFACE TREATMENT CHEMICALS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 52 HENKEL AG & CO. KGAA: COMPANY SNAPSHOT

- FIGURE 53 CHEMETALL GMBH: COMPANY SNAPSHOT

- FIGURE 54 PPG INDUSTRIES, INC.: COMPANY SNAPSHOT

- FIGURE 55 MKS ATOTECH: COMPANY SNAPSHOT

- FIGURE 56 ELEMENT SOLUTIONS INC: COMPANY SNAPSHOT

- FIGURE 57 NIPPON PAINT HOLDINGS CO., LTD.: COMPANY SNAPSHOT

- FIGURE 58 NIHON PARKERIZING CO., LTD.: COMPANY SNAPSHOT

- FIGURE 59 AXALTA COATING SYSTEMS, LLC: COMPANY SNAPSHOT

- FIGURE 60 NOF CORPORATION: COMPANY SNAPSHOT

- FIGURE 61 DOW: COMPANY SNAPSHOT

- FIGURE 62 THE SHERWIN-WILLIAMS COMPANY: COMPANY SNAPSHOT

- FIGURE 63 AKZO NOBEL N.V.: COMPANY SNAPSHOT

混凝土表面處理劑市場:依處理類型、產品形式、應用方法及最終用途產業分類-2026-2032年全球市場預測

混凝土表面處理劑市場:依處理類型、產品形式、應用方法及最終用途產業分類-2026-2032年全球市場預測 2026年全球混凝土表面加固劑市場報告化學表面處理市場:按產品類型、基材、處理類型、流動類型、設備類型、應用和最終用戶分類 - 全球預測 2026-2032船舶隔音材料市場按材料類型、船舶類型、應用領域、安裝類型和供應來源分類-全球預測,2026-2032年

2026年全球混凝土表面加固劑市場報告化學表面處理市場:按產品類型、基材、處理類型、流動類型、設備類型、應用和最終用戶分類 - 全球預測 2026-2032船舶隔音材料市場按材料類型、船舶類型、應用領域、安裝類型和供應來源分類-全球預測,2026-2032年 表面處理化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

表面處理化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球交通運輸路面材料市場規模、佔有率、趨勢和成長分析報告全球成品生產線市場規模、佔有率、趨勢及成長分析報告(2026-2034)

2026-2034年全球交通運輸路面材料市場規模、佔有率、趨勢和成長分析報告全球成品生產線市場規模、佔有率、趨勢及成長分析報告(2026-2034) 全球工業低摩擦表面材料市場:預測(至2034年)-按材料類型、塗層技術、功能、應用、最終用戶和地區進行分析2026年全球化學表面處理市場報告2026年全球成品生產線市場報告

全球工業低摩擦表面材料市場:預測(至2034年)-按材料類型、塗層技術、功能、應用、最終用戶和地區進行分析2026年全球化學表面處理市場報告2026年全球成品生產線市場報告