|

市場調查報告書

商品編碼

1796403

全球二手電動車電池市場:應用、電動車銷售動態、電動車電池需求和潛在轉換率、價值鏈、生態系統和經營模式分析、區域 - 預測(至 2030 年)Second Life EV Battery Market by Application (Utility Scale, Commercial/Industrial, Residential), EV Sales Dynamics, EV Battery Demand & Potential Conversion Rate, Value Chain, Ecosystem & Business Model Analysis, and Region - Forecast to 2030 |

||||||

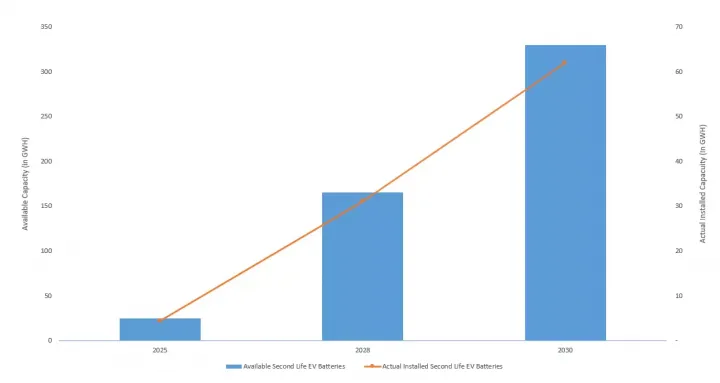

2025年全球二手電動車電池市場規模估計為25-30 GWH,預計2030年將達到330-350 GWH,預測期內複合年成長率約為65%。

市場快速成長主要得益於積極主動且支持性的法規結構、產業策略以及促進循環經濟原則和能源安全的技術資金。歐盟電池指令和「地平線歐洲」等資助計畫旨在加強歐洲的電池轉移基礎設施,並制定明確的報廢標準。聯邦政府的激勵措施,例如《通膨削減法案》下的稅額扣抵和美國能源部資助的先導計畫,以及亞洲國家日益壯大的官民合作關係關係(包括補貼和雄心勃勃的電池回收再利用目標),正在支持能源轉型目標,同時加速對電動車二次電池的需求。

工業領域是二次電動汽車電池的第二大應用領域。

由於對備用電源、需求費用減少、電動車充電站、行動模組化儲存以及倉庫和資料中心的太陽能最佳化的需求不斷成長,預計工業應用領域將為二手電動車電池帶來發展動力。電動車充電站是這一領域很有前景的用例。電動車電池的剩餘容量為 70-80%,可滿足不斷電系統(UPS) 和微電網穩定的中等週期需求(每年 50-150 次循環),支援其用於備用電源和尖峰負載管理。日產、雷諾、特斯拉、Connected Energy(英國)和 Enel X(義大利)等主要企業正在與公用事業和技術合作夥伴合作,在 C&I 領域部署二手電池。例如,Connected Energy 已在英國的電動車充電中心安裝了系統,而 Enel X 正在義大利機場試行能源儲存解決方案。其他計劃,例如戴姆勒的15兆瓦工業儲能系統,以及亞馬遜在其物流中心部署的二手電動車電池,將有助於企業實現永續性目標。此外,將這些電池與現場太陽能和風能發電結合,將減少對電網的依賴,並每年將碳足跡減少10-20%,從而提高永續性和成本效益。從策略上講,企業可以透過將儲能和再利用設施設在需求旺盛的地區,從而最佳化能源管理並節省成本,從而實現經濟效益最大化。

歐洲將佔據電動車二次電池的最大佔有率。

歐洲是電動車二次電池的主要市場之一,該地區非常重視循環經濟並具有支持性的法規環境。該地區是全球汽車原始設備製造商和電動汽車電池可再生公司的所在地。該國實現近 42%可再生能源發電的目標正在推動對公用電網規模電池儲存和工業備用的需求。為此,雷諾於 2018 年啟動了其先進電池儲存計劃,將新舊電動車電池結合二手。 60 兆瓦時的電池系統安裝在法國和德國各地,用於儲存再生能源來源產生的電力。日產、寶馬和奧迪等其他原始設備製造商的類似計劃符合歐洲到 2030 年實現淨零排放的目標。

本報告研究了全球二手電動車電池市場,並提供了有關市場生態系統、技術藍圖、價值鏈、各種經營模式及其收益來源的資訊。

目錄

第1章 引言

第2章執行摘要

第3章 市場評估

- 介紹

- 市場規模與成長軌跡

- 純電動車銷量及預測

- 電動汽車電池市場需求及預測

- 電池化學產品組合策略

- 成本績效矩陣:依化學成分

- 電動車二次電池:技術藍圖

- 電池評估技術

- 電池管理系統的創新

- 系統整合創新

- 軟體平台策略

- 電動車市場滲透率與二次利用轉換率

第4章價值鏈分析

- 價值鏈

- 電動車二次電池:每個階段都增值

- 收集和物流

- 測試與評估

- 翻新和重新利用

- 應用開發和整合

- 經銷/市場開發

- 回收舊產品

第5章電動車電池再利用市場(按應用)

- 介紹

- 公用事業規模電網服務

- 工業

- 住宅用途

第6章區域市場分析

- 介紹

- 北美洲

- 概述

- 主要投資促進因素和政府舉措

- 成長前景和結論

- 歐洲

- 概述

- 到 2030 年實現策略合作、可擴展應用和市場準備

- 展望與結論

- 亞太地區

- 概述

- 製造業領導力卓越

- 展望與結論

第7章 競爭態勢

- 競爭定位

- 經營模式

- 自有模型

- 收益來源

- 客戶獲取策略

- 盈利分析

- 全球OEM二次電動汽車電池安裝計劃與產能

- 主要電池轉換供應商及其當前和預計的未來產能

第8章:戰略建議

第9章主要企業策略概況

- 汽車原廠設備製造商

- TESLA

- TOYOTA MOTOR CORPORATION

- NISSAN MOTOR CO., LTD.

- AB VOLVO

- VOLKSWAGEN GROUP

- BMW AG

- 能源儲存和二次電池專家

- CONNECTED ENERGY

- B2U STORAGE SOLUTIONS, INC.

- REJOULE

- EATON

- E.BATTERY SYSTEMS AG

第10章 附錄

The second life EV battery market is estimated at ~25-30 GWH in 2025 and is projected to reach ~330-350 GWH in 2030 at a CAGR of ~65% during the forecast period. The rapid growth of the second life EV battery market is significantly driven by proactive, supportive regulatory frameworks, industrial strategies, and technology funding to promote circular economy principles and energy security. Initiatives like the EU Battery Directive and funding programs like Horizon Europe are aimed at boosting battery repurposing infrastructure and setting clear end-of-life standards in Europe. Federal incentives, including tax credits under the Inflation Reduction Act and DOE-funded pilot projects (US) and scaling public-private partnerships, with subsidies and ambitious battery recycling & reuse targets in Asian countries, support energy transition targets while accelerating the second life EV battery market demand.

The commercial & industrial segment is the second prominent application of second Life EV batteries.

The commercial & industrial application segment is expected to gain momentum for second life EV battery usage with the growing demand for backup power, demand charge reduction, EV charging stations, mobile & modular storage, and solar energy optimization in warehouses or data centers. Among these, EV charging stations represent this segment's promising use case. EV batteries are left with 70-80% residual capacity and adaptability to medium-cycle demands, such as 50-150 cycles annually for uninterruptible power supply (UPS) and microgrid stabilization, which support their usage for backup power and peak load management. Leading companies like Nissan, Renault, Tesla, Connected Energy (UK), and Enel X (Italy) are advancing second-life battery deployments in the C&I sector, often collaborating with utilities and technology partners. For example, Connected Energy has implemented systems at UK EV charging hubs, while Enel X pilots energy storage solutions at Italian airports. Other projects like Daimler's 15 MW industrial storage system and Amazon's deployment of second life EV batteries into logistics centers will contribute to the commitment toward their corporate sustainability goals. Furthermore, integrating these batteries with on-site solar or wind generation improves sustainability and cost-effectiveness by reducing reliance on grid power and minimizing the carbon footprint by 10-20% annually. Strategically, businesses can maximize economic benefits by co-locating storage and reuse facilities at high-power demand sites, enabling optimized energy management and cost savings.

Europe accounts for a significant market share of second life EV batteries.

Europe is one of the prominent markets for second-life EV batteries with a strong focus on the circular economy and a supportive regulatory environment. The region is home to global automotive OEMs and repurposing companies for EV batteries. Regional efforts such as integration of advanced renewable energy with a target to generate nearly 42% of electricity from these sources will drive demand for utility & grid-scale storage and industrial backups. In line with this, Renault launched an "advanced battery storage program" in 2018 using a combination of new and used EV batteries. It has an energy of 60 MWh battery and is installed in various parts across France and Germany, and is equipped to store electricity generated from renewable sources. Similar projects from other OEMs like Nissan, BMW, and Audi are aligned with Europe's net-zero target by 2030. In addition, some of the promising European EV battery repurposers include Connected Energy (UK), Allye Energy (UK), Zenobe (UK), Voltfang (Germany), BeePlanet Factory (Spain), Libattion (Switzerland), and The Mobility House (Germany). These players are responsible for developing large-scale stationary storage using batteries from passenger cars, trucks & buses, and commercial fleets. Government support, such as USD 1.97 billion allocated through Horizon Europe for battery innovation, combined with corporate initiatives like Volkswagen's plan to reuse 40 GWh of second-life batteries, is helping reduce entry barriers. Additionally, the region's well-established recycling ecosystem, spearheaded by companies like Northvolt, contributes to the scalability of the market. In line with the strong pipeline of new entrants in the repurposed arena and the high-end project activity in Europe, this regional leadership is expected to remain instrumental in the long run.

Research Coverage:

The report provides an in-depth analysis of the second-life EV battery market, focusing on the market ecosystem, technology roadmap, value chain analysis, various business model & their revenue streams, and potential installation demand by application (utility-scale grid services, commercial & industrial, and residential) and region (Asia Pacific, Europe, and North America). It examines EV sales trends (passenger cars & commercial vehicles), current & futuristic EV battery demand (lithium-ion, nickel-metal hydride, solid-state, and other battery chemistries), and performance/cost matrix by different battery chemistries, and EV market penetration to second life conversion rates.

Additionally, the report assesses the effects of the rising EV stocks and presents a future outlook based on industry-wise consumption patterns. It includes detailed information about the significant factors boosting the global demand and key growth impetuses. A thorough analysis of key industry players provides insights into their business overviews, product offerings, key strategies, contracts, partnerships, agreements, product launches, mergers, and acquisitions.

Key Benefits of Buying this Report:

The report provides valuable information for current vs. projected second-life EV battery installation capabilities across key global markets. It will assist stakeholders in understanding the competitive landscape, positioning their businesses more effectively, and planning appropriate go-to-market strategies. Additionally, the report will offer insights into the current market conditions and highlight different ownership models & their revenue profit streams within the industry.

The report provides insights into the following points:

- Analysis of critical technology roadmap parameters such as battery assessment & testing approaches, cell-level & algorithm-based battery management system, various system integration techniques, and software platform strategies

- Market Development: Comprehensive market information (the report analyzes & recommends the most dominant application demand across the considered regions under the scope)

- Market Diversification: Exhaustive information about strategic collaborations, potential geography expansion, recent projections & their capacity, and investments in the second-life EV battery industry

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product/technology offerings of leading OEMs & battery storage specialists such as Tesla, Volvo, Toyota Motor Corporation, BMW Group, Nissan Motor Corporation, Connected Energy, B2U Storage solutions, and Rejoule

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 GLOBAL SECOND LIFE EV BATTERY INDUSTRY OVERVIEW

- 1.1.1 MAJOR DEMAND ZONES AND APPLICATIONS FOR SECOND LIFE EV BATTERIES

- 1.2 SECOND LIFE EV BATTERY MARKET DEFINITION & CONCEPT

- 1.3 INDUSTRY ECOSYSTEM

2 EXECUTIVE SUMMARY

- 2.1 REPORT SUMMARY

3 MARKET ASSESSMENT

- 3.1 INTRODUCTION

- 3.2 MARKET SIZING & GROWTH TRAJECTORY

- 3.2.1 BATTERY EV SALES & FORECASTS

- 3.2.1.1 Electric passenger car sales & forecast

- 3.2.1.2 Electric commercial vehicle sales & forecast

- 3.2.2 EV BATTERY MARKET DEMAND & FORECAST

- 3.2.2.1 EV battery market, by battery chemistry, 2024 vs. 2035 (Thousand Units)

- 3.2.2.2 Upcoming EV models and their battery chemistries, 2025-2026

- 3.2.2.3 Regional demand patterns for EV batteries

- 3.2.2.3.1 Asia Pacific

- 3.2.2.3.1.1 Asia Pacific: Cell supplier-wise battery demand, 2022-2024 (Megawatt-hour)

- 3.2.2.3.2 Europe

- 3.2.2.3.2.1 Europe: Cell supplier-wise battery demand, 2022-2024 (Megawatt-hour)

- 3.2.2.3.3 North America

- 3.2.2.3.3.1 North America: Cell supplier-wise battery demand, 2022-2024 (Megawatt-hour)

- 3.2.2.3.1 Asia Pacific

- 3.2.3 BATTERY CHEMISTRY PORTFOLIO STRATEGY

- 3.2.3.1 Lithium-ion categories (NMC, LFP, NCA, LTO)

- 3.2.3.1.1 Lithium-ion battery cell specifications

- 3.2.3.1.2 Lithium iron phosphate

- 3.2.3.1.3 Nickel manganese cobalt

- 3.2.3.1.4 Lithium iron manganese phosphate

- 3.2.3.2 Nickel-metal hydride

- 3.2.3.3 Solid-state batteries

- 3.2.3.4 Other battery types

- 3.2.3.1 Lithium-ion categories (NMC, LFP, NCA, LTO)

- 3.2.4 PERFORMANCE/COST MATRIX, BY CHEMISTRY

- 3.2.1 BATTERY EV SALES & FORECASTS

- 3.3 SECOND LIFE EV BATTERY: TECHNOLOGY ROADMAP

- 3.3.1 BATTERY ASSESSMENT TECHNOLOGIES

- 3.3.1.1 Non-invasive testing methods

- 3.3.1.2 AI-based degradation prediction

- 3.3.2 BATTERY MANAGEMENT SYSTEM INNOVATIONS

- 3.3.2.1 Adaptive control algorithm

- 3.3.2.2 Cell-level management system

- 3.3.3 SYSTEM INTEGRATION INNOVATIONS

- 3.3.3.1 Modular architecture development

- 3.3.3.2 Thermal management innovation

- 3.3.3.3 Advancements in power electronics

- 3.3.4 SOFTWARE PLATFORM STRATEGY

- 3.3.4.1 Energy management system

- 3.3.4.2 Market participation software

- 3.3.1 BATTERY ASSESSMENT TECHNOLOGIES

- 3.4 EV MARKET PENETRATION INTO SECOND LIFE CONVERSION RATES

4 VALUE CHAIN ANALYSIS

- 4.1 VALUE CHAIN

- 4.1.1 SECOND LIFE EV BATTERY: VALUE ADDITION BY STAGE

- 4.1.2 COLLECTION & LOGISTICS

- 4.1.2.1 Key players and their recent developments in collection & logistics

- 4.1.3 TESTING & ASSESSMENT

- 4.1.3.1 Key players and their recent developments in testing capabilities

- 4.1.4 REFURBISHMENT & REPURPOSING

- 4.1.4.1 Major specialists and their recent developments in repurposing

- 4.1.5 APPLICATION DEVELOPMENT & INTEGRATION

- 4.1.5.1 Prominent application developers & integration providers and their recent developments

- 4.1.6 DISTRIBUTION & MARKET DEPLOYMENT

- 4.1.6.1 Key market deployment players and their recent developments

- 4.1.7 END-OF-LIFE RECYCLING

- 4.1.7.1 Key end-of-life recyclers and their recent developments

5 SECOND LIFE EV BATTERY MARKET, BY APPLICATION

- 5.1 INTRODUCTION

- 5.2 UTILITY-SCALE GRID SERVICES

- 5.2.1 PROMINENT UTILITY-SCALE PROVIDERS & THEIR CAPACITIES

- 5.2.2 RENEWABLE ENERGY

- 5.2.2.1 Solar power

- 5.2.2.2 Wind energy

- 5.3 COMMERCIAL & INDUSTRIAL

- 5.3.1 EV CHARGING STATIONS

- 5.3.2 EV CHARGING STATION SITES EQUIPPED WITH SECOND LIFE EV BATTERIES, BY REGION

- 5.4 RESIDENTIAL APPLICATION

6 REGIONAL MARKET ANALYSIS

- 6.1 INTRODUCTION

- 6.2 NORTH AMERICA

- 6.2.1 OVERVIEW

- 6.2.1.1 Key players and their second life EV battery installation projects

- 6.2.2 MAJOR INVESTMENT DRIVERS & GOVERNMENT INITIATIVES

- 6.2.3 GROWTH OUTLOOK & CONCLUSION

- 6.2.1 OVERVIEW

- 6.3 EUROPE

- 6.3.1 OVERVIEW

- 6.3.1.1 Key players and their second life EV battery installation projects

- 6.3.2 STRATEGIC ALIGNMENT, SCALABLE APPLICATIONS, AND MARKET READINESS BY 2030

- 6.3.3 OUTLOOK & CONCLUSION

- 6.3.1 OVERVIEW

- 6.4 ASIA PACIFIC

- 6.4.1 OVERVIEW

- 6.4.1.1 Key players and their second life EV battery installation projects

- 6.4.2 MANUFACTURING LEADERSHIP EXCELLENCE

- 6.4.3 OUTLOOK & CONCLUSION

- 6.4.1 OVERVIEW

7 COMPETITIVE LANDSCAPE

- 7.1 COMPETITIVE POSITIONING

- 7.2 BUSINESS MODELS

- 7.2.1 OWNERSHIP MODELS

- 7.2.1.1 Battery leasing & rentals

- 7.2.1.2 Battery-as-a-service (BaaS)

- 7.2.1.3 Mobile BESS for temporary power supply

- 7.2.1.4 Energy-as-a-service (EaaS)

- 7.2.2 REVENUE STREAMS

- 7.2.3 CUSTOMER ACQUISITION STRATEGIES

- 7.2.4 PROFITABILITY ANALYSIS

- 7.2.1 OWNERSHIP MODELS

- 7.3 GLOBAL OEMS' SECOND LIFE EV BATTERY INSTALLATION PROJECTS & THEIR CAPACITIES

- 7.4 KEY BATTERY REPURPOSERS AND THEIR CURRENT VS. PROJECTED CAPACITY

8 STRATEGIC RECOMMENDATIONS

9 KEY PLAYERS' STRATEGIC PROFILES

- 9.1 AUTOMOTIVE OEMS

- 9.1.1 TESLA

- 9.1.1.1 Overview

- 9.1.1.2 Recent financials

- 9.1.1.3 Tesla: Global EV sales, by key model

- 9.1.1.4 Strategic approach toward second life EV batteries

- 9.1.1.5 Recent developments, 2019-2025

- 9.1.2 TOYOTA MOTOR CORPORATION

- 9.1.2.1 Overview

- 9.1.2.2 Recent financials

- 9.1.2.3 Toyota Motor Corporation: Global EV sales, by key model

- 9.1.2.4 Strategic approach toward second life EV batteries

- 9.1.2.5 Recent developments, 2019-2025

- 9.1.3 NISSAN MOTOR CO., LTD.

- 9.1.3.1 Overview

- 9.1.3.2 Recent financials

- 9.1.3.3 Nissan Motors Co., Ltd.: Global EV sales, by key model

- 9.1.3.4 Continued investment in global network expansion for battery collection and repurposing technologies

- 9.1.3.5 Recent developments, 2010-2025

- 9.1.4 AB VOLVO

- 9.1.4.1 Overview

- 9.1.4.2 Recent financials

- 9.1.4.3 Strategic approach toward second life EV batteries

- 9.1.4.4 Recent developments, 2022-2023

- 9.1.5 VOLKSWAGEN GROUP

- 9.1.5.1 Overview

- 9.1.5.2 Recent financials

- 9.1.5.3 Volkswagen Group: Global EV sales, by key model

- 9.1.5.4 Strategic approach toward second life EV batteries

- 9.1.5.5 Recent developments, 2021-2025

- 9.1.6 BMW AG

- 9.1.6.1 Overview

- 9.1.6.2 Recent financials

- 9.1.6.3 BMW AG: Global EV sales, by key model

- 9.1.6.4 Strategic approach toward second life EV batteries

- 9.1.6.5 Recent developments, 2020-2025

- 9.1.1 TESLA

- 9.2 ENERGY STORAGE & SECOND LIFE BATTERY SPECIALISTS

- 9.2.1 CONNECTED ENERGY

- 9.2.1.1 Overview

- 9.2.1.2 Products, capacity, and applications

- 9.2.1.3 Recent developments, 2021-2025

- 9.2.2 B2U STORAGE SOLUTIONS, INC.

- 9.2.2.1 Overview

- 9.2.2.2 Products, capacity, and application

- 9.2.2.3 Recent developments, 2021-2024

- 9.2.3 REJOULE

- 9.2.3.1 Overview

- 9.2.3.2 Products, capacity, and application

- 9.2.3.3 Projects

- 9.2.3.4 Recent developments, 2023-2025

- 9.2.4 EATON

- 9.2.4.1 Overview

- 9.2.4.2 Recent financials

- 9.2.4.3 Products, capacity, and application

- 9.2.4.4 Recent developments, 2024

- 9.2.5 E.BATTERY SYSTEMS AG

- 9.2.5.1 Overview

- 9.2.5.2 Products, capacity, and application

- 9.2.5.3 Recent developments, 2021-2025

- 9.2.1 CONNECTED ENERGY

10 APPENDIX

- 10.1 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 10.2 AUTHOR DETAILS

List of Tables

- TABLE 1 ELECTRIC PASSENGER CAR SALES, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 2 ELECTRIC PASSENGER CAR SALES, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 3 ELECTRIC COMMERCIAL VEHICLES MARKET, BY VEHICLE TYPE, 2019-2023 (UNITS)

- TABLE 4 ELECTRIC COMMERCIAL VEHICLES MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- TABLE 5 EV BATTERY MARKET, BY BATTERY TYPE, 2019-2023 (THOUSAND UNITS)

- TABLE 6 EV BATTERY MARKET, BY BATTERY TYPE, 2024-2030 (THOUSAND UNITS)

- TABLE 7 EV BATTERY MARKET, BY BATTERY TYPE, 2031-2035 (THOUSAND UNITS)

- TABLE 8 BATTERY CHEMISTRIES IN CURRENT AND UPCOMING EV MODELS, BY OEM, 2025-2026

- TABLE 9 ASIA PACIFIC: CELL SUPPLIER-WISE BATTERY DEMAND PATTERN, 2022-2024 (MWH)

- TABLE 10 EUROPE: CELL SUPPLIER-WISE BATTERY DEMAND PATTERN, 2022-2024 (MWH)

- TABLE 11 NORTH AMERICA: CELL SUPPLIER-WISE BATTERY DEMAND PATTERN, 2022-2024 (MWH)

- TABLE 12 LITHIUM-ION: EV BATTERY MARKET, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 13 LITHIUM-ION: EV BATTERY MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 14 LITHIUM-ION: EV BATTERY MARKET, BY REGION, 2031-2035 (THOUSAND UNITS)

- TABLE 15 COMPARISON BETWEEN LITHIUM-ION BATTERY CHEMISTRIES

- TABLE 16 LITHIUM IRON PHOSPHATE: EV BATTERY MARKET, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 17 LITHIUM IRON PHOSPHATE: EV BATTERY MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 18 LITHIUM IRON PHOSPHATE: EV BATTERY MARKET, BY REGION, 2031-2035 (THOUSAND UNITS)

- TABLE 19 NICKEL MANGANESE COBALT: EV BATTERY MARKET, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 20 NICKEL MANGANESE COBALT: EV BATTERY MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 21 NICKEL MANGANESE COBALT: EV BATTERY MARKET, BY REGION, 2031-2035 (THOUSAND UNITS)

- TABLE 22 NICKEL-METAL HYDRIDE: EV BATTERY MARKET, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 23 NICKEL-METAL HYDRIDE: EV BATTERY MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 24 NICKEL-METAL HYDRIDE: EV BATTERY MARKET, BY REGION, 2031-2035 (THOUSAND UNITS)

- TABLE 25 SOLID-STATE BATTERIES: RECENT DEVELOPMENTS

- TABLE 26 SOLID-STATE BATTERIES: EV BATTERY MARKET, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 27 SOLID-STATE BATTERIES: EV BATTERY MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 28 SOLID-STATE BATTERIES: EV BATTERY MARKET, BY REGION, 2031-2035 (THOUSAND UNITS)

- TABLE 29 OTHER BATTERY TYPES: EV BATTERY MARKET, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 30 OTHER BATTERY TYPES: EV BATTERY MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 31 OTHER BATTERY TYPES: EV BATTERY MARKET, BY REGION, 2031-2035 (THOUSAND UNITS)

- TABLE 32 EV BATTERY CHEMISTRIES: COST VS. PERFORMANCE COMPARISON

- TABLE 33 NON-INVASIVE TESTING METHODS

- TABLE 34 LIST OF COMPANIES INVOLVED IN NON-INVASIVE TESTING METHODS

- TABLE 35 ADVANTAGES OF AI-BASED DEGRADATION PREDICTION TECHNOLOGY

- TABLE 36 BENEFITS OF ADAPTIVE CONTROL ALGORITHMS IN SECOND LIFE EV BATTERY MANAGEMENT SYSTEM (BMS)

- TABLE 37 MAJOR COMPANIES INVOLVED IN SECOND LIFE BATTERY INTEGRATION INNOVATION

- TABLE 38 LIST OF COMPANIES WORKING ON MODULAR ARCHITECTURE INTEGRATION FOR SECOND LIFE EV BATTERIES

- TABLE 39 KEY DEVELOPMENTS UNDERTAKEN BY COMPANIES IN POWER ELECTRONICS

- TABLE 40 COMPANIES WORKING ON ENERGY MANAGEMENT SYSTEM (EMS) FOR SECOND LIFE EV BATTERIES

- TABLE 41 VALUE CHAIN: STAGE-WISE VALUE DISTRIBUTION (%)

- TABLE 42 RECENT DEVELOPMENTS UNDERTAKEN BY PLAYERS IN MAINTAINING COLLECTION & LOGISTICS OF SECOND LIFE EV BATTERIES

- TABLE 43 RECENT DEVELOPMENTS UNDERTAKEN BY KEY PLAYERS IN TESTING AND ASSESSMENT OF SECOND LIFE EV BATTERIES

- TABLE 44 RECENT DEVELOPMENTS UNDERTAKEN BY KEY PLAYERS IN REFURBISHMENT AND REPURPOSING OF SECOND LIFE EV BATTERIES

- TABLE 45 KEY PLAYERS INVOLVED IN APPLICATION DEVELOPMENT AND INTEGRATION OF SECOND LIFE BATTERIES

- TABLE 46 KEY PLAYERS INVOLVED IN APPLICATION DISTRIBUTION AND MARKET DEPLOYMENT OF SECOND LIFE BATTERY

- TABLE 47 KEY PLAYERS INVOLVED IN END-OF-LIFE RECYCLING OF SECOND LIFE BATTERIES

- TABLE 48 KEY UTILITY-SCALE SECOND LIFE EV BATTERY STORAGE PROJECTS AND DEPLOYMENTS

- TABLE 49 KEY COMMERCIAL & INDUSTRIAL APPLICATIONS

- TABLE 50 EV CHARGING STATIONS AND SITES EQUIPPED WITH SECOND LIFE EV BATTERIES, BY REGION

- TABLE 51 NORTH AMERICA: KEY PLAYERS AND THEIR DEVELOPMENTS

- TABLE 52 EUROPE: KEY PLAYERS AND THEIR DEVELOPMENTS

- TABLE 53 ASIA PACIFIC: KEY PLAYERS AND THEIR DEVELOPMENTS

- TABLE 54 OWNERSHIP MODELS & THEIR BUSINESS OUTCOMES

- TABLE 55 BUSINESS MODELS & THEIR CASH FLOW APPROACH

- TABLE 56 KEY OEMS' SECOND LIFE EV BATTERY INSTALLATION PROJECTS & THEIR CAPACITIES

- TABLE 57 KEY BATTERY REPURPOSERS AND THEIR CURRENT VS. PROJECTED CAPACITY

- TABLE 58 TESLA: RECENT FINANCIALS, 2023 VS. 2024

- TABLE 59 TESLA: GLOBAL EV SALES, 2022-2024

- TABLE 60 TOYOTA MOTOR CORPORATION: RECENT FINANCIALS, 2023 VS. 2024

- TABLE 61 TOYOTA MOTOR CORPORATION: GLOBAL EV SALES, 2022-2024

- TABLE 62 NISSAN MOTORS CO., LTD.: RECENT FINANCIALS, 2023 VS. 2024

- TABLE 63 NISSAN MOTORS CO., LTD.: GLOBAL EV SALES, 2022-2024

- TABLE 64 AB VOLVO: RECENT FINANCIALS, 2023 VS. 2024

- TABLE 65 VOLKSWAGEN GROUP: RECENT FINANCIALS, 2023 VS. 2024

- TABLE 66 VOLKSWAGEN GROUP: GLOBAL EV SALES, 2022-2024

- TABLE 67 BMW AG: RECENT FINANCIALS, 2023 VS. 2024

- TABLE 68 BMW AG: GLOBAL EV SALES, 2022-2024

- TABLE 69 CONNECTED ENERGY: PRODUCTS OFFERED

- TABLE 70 B2U STORAGE SOLUTIONS, INC.: PRODUCTS OFFERED

- TABLE 71 REJOULE: PRODUCTS OFFERED

- TABLE 72 REJOULE: PROJECTS

- TABLE 73 EATON: RECENT FINANCIALS, 2023 VS. 2024

- TABLE 74 EATON: PRODUCTS OFFERED

- TABLE 75 E.BATTERY SYSTEMS AG: PRODUCTS OFFERED

List of Figures

- FIGURE 1 LIFE CYCLE OF EV BATTERIES OFFERING SECOND LIFE APPLICATIONS

- FIGURE 2 SECOND LIFE EV BATTERY INDUSTRY ECOSYSTEM

- FIGURE 3 SECOND LIFE EV BATTERY MARKET OUTLOOK

- FIGURE 4 ELECTRIC COMMERCIAL VEHICLES MARKET, BY VEHICLE TYPE, 2024 VS. 2030 (UNITS)

- FIGURE 5 LITHIUM-ION SEGMENT TO ACCOUNT FOR LARGEST MARKET DURING FORECAST PERIOD

- FIGURE 6 ASIA PACIFIC TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 7 LITHIUM-ION: COMPARISON BETWEEN WH/KG AND WH/L

- FIGURE 8 EVS EQUIPPED WITH LITHIUM-ION BATTERIES

- FIGURE 9 LITHIUM-ION BATTERY CELL SPECIFICATIONS

- FIGURE 10 COMPARISON BETWEEN LFP AND LITHIUM-ION BATTERIES

- FIGURE 11 COMPARISON BETWEEN LFP AND NCA/NMC BATTERY CHEMISTRIES

- FIGURE 12 FEATURES AND ADVANTAGES OF SODIUM-ION BATTERIES

- FIGURE 13 GLOBALLY AVAILABLE SECOND LIFE EV BATTERY CAPACITY VS. ACTUAL INSTALLED SECOND LIFE EV BATTERY CAPACITY, 2025 VS. 2030 (GIGAWATT-HOURS)

- FIGURE 14 SECOND LIFE EV BATTERY VALUE CHAIN: VALUE ADDED BY STAGE

- FIGURE 15 SECOND LIFE EV BATTERY MARKET, BY APPLICATION, 2025-2030 (GWH)

- FIGURE 16 GLOBAL EV BATTERY CAPACITY AVAILABILITY VS. ACTUAL INSTALLATION, 2025-2030 (GWH)

- FIGURE 17 SECOND LIFE EV BATTERY MARKET, BY REGION, 2025-2030 (GWH)

- FIGURE 18 SECOND LIFE EV BATTERIES: POTENTIAL BUSINESS MODELS

- FIGURE 19 STRATEGIC RECOMMENDATIONS FOR VARIOUS STAKEHOLDERS

電動車電池二次利用市場:2026-2032年全球市場預測(按電池類型、電池容量、來源、系統結構、銷售管道和應用分類)

電動車電池二次利用市場:2026-2032年全球市場預測(按電池類型、電池容量、來源、系統結構、銷售管道和應用分類) 電動車電池二次利用市場預測—全球電池化學成分、再利用製程、容量範圍、應用、最終用戶和地區分析—2034年

電動車電池二次利用市場預測—全球電池化學成分、再利用製程、容量範圍、應用、最終用戶和地區分析—2034年 2035年電動車電池二手市場分析與預測:按類型、產品、服務、技術、組件、應用、最終用戶、功能、安裝類型和解決方案分類

2035年電動車電池二手市場分析與預測:按類型、產品、服務、技術、組件、應用、最終用戶、功能、安裝類型和解決方案分類 2026-2030年全球電動車電池二次利用市場

2026-2030年全球電動車電池二次利用市場 電動車電池二次利用市場-策略性洞察與預測(2026-2031年)

電動車電池二次利用市場-策略性洞察與預測(2026-2031年) First Life電動車電池全球市場報告(2026年)

First Life電動車電池全球市場報告(2026年) 全球電動汽車電池市場(至2040年):依電池類型、應用、終端用戶產業和地區劃分-產業趨勢和全球預測

全球電動汽車電池市場(至2040年):依電池類型、應用、終端用戶產業和地區劃分-產業趨勢和全球預測 全球電動車二手電池市場:市場規模、佔有率、趨勢分析(按最終用途、應用和地區分類)、展望和預測(2025-2032 年)全球二手電動車電池市場:預測至2032年-按電池化學成分、供應來源、經營模式、技術、應用和區域進行分析到 2030 年第二次電動車電池市場預測:按電池類型、電池容量、車輛類型、應用、最終用戶和地區進行的全球分析

全球電動車二手電池市場:市場規模、佔有率、趨勢分析(按最終用途、應用和地區分類)、展望和預測(2025-2032 年)全球二手電動車電池市場:預測至2032年-按電池化學成分、供應來源、經營模式、技術、應用和區域進行分析到 2030 年第二次電動車電池市場預測:按電池類型、電池容量、車輛類型、應用、最終用戶和地區進行的全球分析