|

市場調查報告書

商品編碼

1783241

CF 和 CFRP 市場(按樹脂類型、前體類型、產地、製造流程、最終用途產業和地區分類)- 預測至 2030 年CF & CFRP Market by Precursor Type (PAN, Pitch), Source, Resin Type, Manufacturing Process (Lay-Up, Compression Molding, Resin Transfer Molding, Filament Winding, Injection Molding, Pultrusion), End-use Industry, and Region - Forecast to 2030 |

||||||

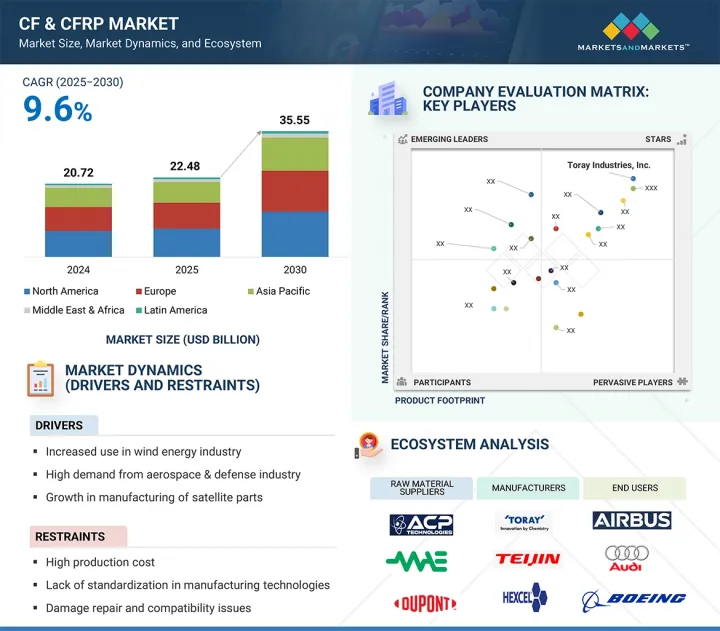

預計 2025 年 CFRP 市場規模將達到 224.8 億美元,2025 年至 2030 年的複合年成長率為 9.6%,2030 年將達到 355.5 億美元。

| 調查範圍 | |

|---|---|

| 調查年份 | 2022-2030 |

| 基準年 | 2024 |

| 預測期 | 2025-2030 |

| 對價單位 | 金額(百萬美元)和數量(千噸) |

| 部分 | 按樹脂類型、前驅物類型、產地、製造流程、最終用途產業和地區 |

| 目標區域 | 歐洲、北美、亞太地區、中東和非洲、拉丁美洲 |

瀝青前驅體憑藉其獨特的性能組合以及高性能行業日益成長的需求,佔據第二大市場佔有率。雖然聚丙烯腈 (PAN) 仍然是主要的前驅體,但源自石油基瀝青的瀝青基碳纖維具有優異的機械性能和高熱穩定性。其優異的抗張強度超過 5 GPa,可與鋼材媲美。此外,其剛性重量比是鋁的兩倍,使其成為輕量化應用的理想選擇。瀝青碳纖維具有卓越的耐腐蝕、耐化學性和耐極端溫度性能,使其能夠在惡劣環境中使用。其高導熱性使其能夠高效散熱,非常適合熱敏應用。

原生碳纖維憑藉其優異的性能(包括輕量化、高剛度和耐化學性)佔據最大的市場佔有率,使其成為航太、國防、汽車、風力發電和體育用品等終端行業不可或缺的材料。這些行業依賴輕量化材料來提升飛機和車輛的燃油性能。原生碳纖維因其成熟的製造流程和穩定的品質而備受青睞。雖然再生碳纖維作為一種永續的替代品越來越受歡迎,但原生碳纖維憑藉其出色的機械性能和在結構部件中的多功能性仍然佔據主導地位。

熱塑性塑膠佔據了整個碳纖維增強塑膠市場的第二大佔有率。熱塑性碳纖維增強塑膠具有高抗衝擊性、快速加工、可回收和易於儲存等特點,對尋求經濟高效且永續解決方案的行業越來越有吸引力。這些特性在汽車、航太和國防等終端產業尤為有利,因為快速生產、輕量化和環保對這些產業至關重要。熱塑性塑膠技術的進步進一步提高了其機械性能,使其能夠與熱固性碳纖維增強塑膠進行更緊密的競爭,並推動其在各種應用中的普及。

纏繞成型佔據了整個碳纖維和碳纖維增強複合材料市場的第二大佔有率。在絲捲繞製程中,旋轉的心軸可作為模具,形成產品的內外層壓板表面。此製程允許高纖維負載,從而產生高強度重量比的層壓板。此製程可用於生產中空或圓形零件,例如壓縮空氣罐、高壓二氧化碳罐和瓶、軟水器系統、救援空氣罐、遊艇桅杆、壓縮天然氣罐、電線杆和其他建築材料。這種自動化方法用於製造高度工程化的結構,確保均勻性、精確性和高效生產,並將浪費降至最低。

預計在預測期內,體育用品產業將成為 CFRP 市場中成長速度第二快的產業。對輕量化、高性能設備的需求推動了對 CFRP 的需求,因為它可以提高運動表現和使用者體驗。 CFRP 卓越的強度重量比使製造商能夠製造比用傳統材料製成的產品更輕、更堅固的產品,例如自行車、網球拍、高爾夫球桿、滑雪板和曲棍球棒。職業運動的興起、消費者對健身的興趣日益濃厚以及贊助和媒體曝光的增加進一步刺激了這種需求,鼓勵製造商繼續創新和採用 CFRP 技術。 CFRP 製造技術的進步提高了產品的耐用性,從而使該材料能夠用於更廣泛的身體活動設備中。

預計北美將成為預測期內 CFRP 市場成長最快的地區。預計未來幾年北美市場將經歷顯著成長,因為對風力發電計劃的需求不斷成長,推動了對風力渦輪機葉片更有效率、更耐用的 CFRP 材料的需求。 CFRP 透過減輕重量、增強耐腐蝕性和提高性能來幫助實現這些目標。該地區正在不斷投資研發,以滿足不斷變化的市場需求和監管要求。例如,在美國,風力發電機葉片產業對 CFRP 產品的需求不斷成長,以製造輕型電動車,為環境永續性做出貢獻,同時減少碳排放。這推動了新的 CFRP 製造流程和產品的開發,包括使用再生材料和創造可提高汽車燃油效率的輕量材料。

本報告研究了全球 CF 和 CFRP 市場,並按樹脂類型、前體類型、產地、製造流程、最終用途行業、區域趨勢和參與市場的公司概況進行細分。

目錄

第1章 引言

第2章調查方法

第3章執行摘要

第4章重要考察

第5章市場概述

- 介紹

- 市場動態

- 波特五力分析

- 主要相關人員和採購標準

- 供應鏈分析

- 生態系分析

- 定價分析

- 價值鏈分析

- 貿易分析

- 技術分析

- 人工智慧/生成式人工智慧對碳纖維和碳纖維增強塑膠市場的影響

- 宏觀經濟展望

- 專利分析

- 監管狀況

- 2025-2026年主要會議和活動

- 案例研究分析

- 影響客戶業務的趨勢/中斷

- 投資金籌措場景

- 2025年美國關稅的影響-碳纖維和碳纖維增強塑膠市場

第6章 CFRP市場(依樹脂類型)

- 介紹

- 熱固性

- 熱塑性塑膠

第7章 CF 市場(依前驅類型)

- 介紹

- 聚丙烯腈碳纖維

- 瀝青基碳纖維

第 8 章:CF 市場(按來源)

- 介紹

- 原生碳纖維

- 再生碳纖維

第9章 CFRP市場(按製造程序)

- 介紹

- 積層法過程

- 壓縮成型工藝

- 樹脂轉注成形工藝

- 絲捲繞製程

- 射出成型工藝

- 拉擠工藝

- 其他

第 10 章 CFRP 市場(依最終用途產業)

- 介紹

- 航太和國防

- 風力發電

- 車

- 體育用品

- 土木工程

- 管道和儲罐

- 船

- 醫療保健

- 電機與電子工程

- 其他

第11章 CFRP市場(按地區)

- 介紹

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

第12章競爭格局

- 概述

- 主要參與企業的策略/優勢

- 2024年收益分析

- 2024年市場佔有率分析

- 品牌/產品比較分析

- 公司估值矩陣:2024 年關鍵參與企業

- 公司估值矩陣:Start-Ups/中小企業,2024 年

- 估值和財務指標

- 競爭場景

第13章:公司簡介

- 主要參與企業

- TORAY INDUSTRIES, INC.

- TEIJIN LIMITED

- MITSUBISHI CHEMICAL CORPORATION

- HEXCEL CORPORATION

- SYENSQO

- SGL CARBON

- HS HYOSUNG ADVANCED MATERIALS

- ZHONGFU SHENYING CARBON FIBER CO., LTD.

- KUREHA CORPORATION

- DOWAKSA

- WEIHAI GUANGWEI COMPOSITE MATERIALS CO., LTD.

- UMATEX

- JILIN CHEMICAL FIBER GROUP CO., LTD.

- JIANGSU HENGSHEN CO., LTD.

- CHINA NATIONAL BLUESTAR(GROUP)CO., LTD.

- 其他公司

- TAEKWANG INDUSTRIAL CO., LTD.

- GEN 2 CARBON

- NIPPON GRAPHITE FIBER CO., LTD.

- CHANGZHOU JLON COMPOSITE CO., LTD.

- MALLINDA

- BCIRCULAR

- VARTEGA INC.

- JILIN TANGU CARBON FIBER CO., LTD.

- WUXI GDE TECHNOLOGY CO., LTD.

- SINOFIBERS TECHNOLOGY CO., LTD.

- JILIN JIYAN HIGH-TECH FIBERS CO., LTD.

第14章 附錄

The CFRP market is estimated at USD 22.48 billion in 2025 and is projected to reach USD 35.55 billion by 2030, at a CAGR of 9.6% from 2025 to 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Kiloton) |

| Segments | Precursor type, source, resin type, manufacturing process, end-use industry, and region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and Latin America |

Pitch precursor accounted for the second-largest share due to its unique combination of properties and the growing demand in high-performance industries. While polyacrylonitrile (PAN) remains the dominant precursor, pitch-based carbon fibers derived from petroleum-based pitch offer superior mechanical properties and high thermal stability. They possess excellent tensile strength, exceeding 5 GPa, which is comparable to steel. Moreover, their specific stiffness is twice that of aluminum, making them ideal for lightweight applications. Pitch carbon fibers exhibit exceptional resistance to corrosion, chemicals, and extreme temperatures, enabling their use in demanding environments. Their high thermal conductivity ensures efficient heat dissipation, making them suitable for heat-sensitive applications.

''In terms of value, virgin carbon fiber accounted for the largest share of the overall CF market.''

The virgin segment accounted for the largest market share due to its exceptional properties, including its lightweight structure, stiffness, and chemical resistance, which make it indispensable in end-use industries like aerospace & defense, automotive, wind energy, and sporting goods. These industries rely on lightweight materials for improved fuel performance in aircraft and vehicles. The use of virgin carbon fiber is preferred due to its established manufacturing processes and consistent quality, which are critical for high-performance applications. While recycled carbon fiber is gaining traction as a sustainable alternative, virgin carbon fiber remains dominant because of its outstanding mechanical properties and versatile use in structural components.

''In terms of value, thermoplastic accounted for the second-largest share of the overall CFRP market.''

Thermoplastic resin accounted for the second-largest market share in the overall CFRP market. Thermoplastic CFRPs offer high impact resistance, shorter processing times, recyclability, and easier storage, which makes them increasingly attractive for industries seeking cost-effective and sustainable solutions. These properties are particularly beneficial in end-use industries like automotive and aerospace & defense, where rapid production, lightweighting, and environmental considerations are critical. Advancements in thermoplastic resin technology have further improved their mechanical performance, allowing them to compete more closely with thermosetting CFRPs and driving their adoption in various applications.

''In terms of value, filament winding process accounted for the second-largest share of the overall CFRP market.''

Filament winding accounted for the second-largest share of the overall CF & CFRP market. In the filament winding process, a rotating mandrel serves as a mold to create an inner surface and a laminate surface outside the product. This process achieves a high degree of fiber loading, resulting in laminates with a high strength-to-weight ratio. It manufactures hollow or circular components such as compressed air tanks, high-pressure CO2 tanks & bottles, water softener systems, rescue air tanks, sailboat masts, CNG tanks, light poles, and other construction materials. This automated method is utilized to produce highly engineered structures, ensuring uniformity, precision, and efficient production with minimal waste.

"The Sporting Goods industry is projected to be the second-fastest-growing end-use industry during the forecast period."

The sporting goods industry is expected to register the second-fastest growth in the CFRP market during the forecast period. As demand for lightweight, high-performance equipment enhances athletic performance and user experience, the need for CFRP is increasing. The excellent strength-to-weight ratio of CFRP enables manufacturers to create products such as bicycles, tennis racquets, golf clubs, skis, and hockey sticks that are both lightweight and stronger than those made from traditional materials. The rise in professional sports, increasing consumer interest in fitness, and expanding sponsorships and media coverage have further fueled this demand, prompting manufacturers to continuously innovate and adopt CFRP technologies. Advancements in CFRP production technology have improved product durability and made these materials more accessible to a broader range of sporting activities goods.

"North America is projected to register the highest growth rate in the CFRP market during the forecast period."

North America is projected to be the fastest-growing region in the CFRP market during the forecast period. The North American market will see significant growth in the coming years due to a rising demand for wind energy projects, which has driven the need for more efficient and durable CFRP materials for wind turbine blades. CFRP can help achieve these objectives by reducing weight, enhancing corrosion resistance, and improving performance. The region is continually investing in research & development to meet evolving market demands and regulatory requirements. For instance, there is a growing demand for CFRP products in US from automotive sector for manufacturing lightweight electric vehicles, thereby contributing to environmental sustainability while reducing carbon emissions. This has led to the development of new CFRP manufacturing processes and products, such as using recycled materials or producing lightweight materials that can enhance fuel efficiency in vehicles.

This study has been validated through primary interviews with industry experts globally. The primary sources have been divided into the following three categories:

- By Company Type: Tier 1 - 40%, Tier 2 - 33%, and Tier 3 - 27%

- By Designation: C-level - 50%, Director-level - 30%, and Managers - 20%

- By Region: North America - 15%, Europe - 50%, Asia Pacific - 20%, the Middle East & Africa - 5%, and Latin America - 10%

The report provides a comprehensive analysis of the following companies:

Prominent companies in this market include Toray Industries, Inc. (Japan), Teijin Limited (Japan), Mitsubishi Chemical Corporation (Japan), Hexcel Corporation (US), Syensqo (Belgium), SGL Carbon (Germany), HS Hyosung Advanced Materials (South Korea), Zhongfu Shenying Carbon Fiber Co., Ltd. (China), Kureha Corporation (Japan), DowAksa (Turkey), Weihai Guangwei Composite Materials Co., Ltd. (China), UMATEX (Russia), Jilin Chemical Fiber Group Co., Ltd. (China), Jiangsu Hengshen Co., Ltd. (China), and China National Bluestar (Group) Co., Ltd. (China).

Research coverage

This research report categorizes the CF & CFRP market by precursor type (PAN and pitch), source (virgin and recycled), resin type (thermosetting and thermoplastic), manufacturing process (lay-up, compression molding, resin transfer molding, filament winding, injection molding, and pultrusion), end-use industry (aerospace & defense, automotive, wind energy, pipe & tank, sporting goods, civil engineering, medical, marine, and electrical & electronics), and region (North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America). The scope of the report includes detailed information about the major factors influencing the growth of the CF & CFRP market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted in order to provide insights into their business overview, solutions and services, key strategies, and recent developments in the CF & CFRP market are all covered. This report includes a competitive analysis of upcoming startups in the CF & CFRP market ecosystem.

Reasons to buy this report:

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall CF & CFRP market and the subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (growth in manufacturing of satellite parts, high demand from aerospace & defense industry, rising adoption in automobile applications due to stringent eco-friendly regulations, increased use in wind energy industry, and rising demand for regular tow carbon in pressure vessels), restraints (high production cost, lack of standardization in manufacturing technologies, and damage repair and compatibility issues), opportunities (increased investments in the development of low-cost coal-based carbon fibers, potential opportunities in new applications, increasing demand for fuel cell electric vehicles (FCEVs), increasing use in 3D printing, advancements in carbon fiber recycling technologies), and challenges (production of low-cost carbon fiber, capital-intensive production and complex manufacturing processes, and recyclability issues) influencing the growth of the CF & CFRP market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the CF & CFRP market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the CF & CFRP market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the CF & CFRP market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Toray Industries, Inc. (Japan), Teijin Limited (Japan), Mitsubishi Chemical Corporation (Japan), Hexcel Corporation (US), Syensqo (Belgium), SGL Carbon (Germany), HS Hyosung Advanced Materials (South Korea), Zhongfu Shenying Carbon Fiber Co., Ltd. (China), Kureha Corporation (Japan), DowAksa (Turkey), Weihai Guangwei Composite Materials Co., Ltd. (China), UMATEX (Russia), Jilin Chemical Fiber Group Co., Ltd. (China), Jiangsu Hengshen Co., Ltd. (China), and China National Bluestar (Group) Co., Ltd. (China) in the CF & CFRP market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS OF STUDY

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key primary participants

- 2.1.2.3 Breakdown of primary interviews

- 2.1.2.4 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 BASE NUMBER CALCULATION

- 2.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 2.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 2.4 MARKET FORECAST APPROACH

- 2.4.1 SUPPLY SIDE

- 2.4.2 DEMAND SIDE

- 2.5 DATA TRIANGULATION

- 2.6 FACTOR ANALYSIS

- 2.7 RESEARCH ASSUMPTIONS

- 2.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CF & CFRP MARKET

- 4.2 CFRP MARKET, BY END-USE INDUSTRY AND REGION

- 4.3 CF MARKET, BY PRECURSOR

- 4.4 CF MARKET, BY SOURCE

- 4.5 CFRP MARKET, BY RESIN TYPE

- 4.6 CFRP MARKET, BY MANUFACTURING PROCESS

- 4.7 CFRP MARKET, BY END-USE INDUSTRY

- 4.8 CFRP MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growth in manufacturing of satellite parts

- 5.2.1.2 High usage in aerospace & defense industry

- 5.2.1.3 Rising adoption in automobile applications due to stringent eco-friendly regulations

- 5.2.1.4 Increased use in wind energy industry

- 5.2.1.5 Rising demand for regular tow carbon in pressure vessels

- 5.2.2 RESTRAINTS

- 5.2.2.1 High production cost

- 5.2.2.2 Lack of standardization in manufacturing technologies

- 5.2.2.3 Damage repair and compatibility issues

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increased investments in development of low-cost coal-based carbon fibers

- 5.2.3.2 Potential opportunities in new applications

- 5.2.3.3 Increasing demand for fuel cell electric vehicles

- 5.2.3.4 Increasing use in 3D printing

- 5.2.3.5 Advancements in carbon fiber recycling technologies

- 5.2.4 CHALLENGES

- 5.2.4.1 Production of low-cost carbon fiber

- 5.2.4.2 Capital-intensive production and complex manufacturing process

- 5.2.4.3 Recyclability issues

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 THREAT OF NEW ENTRANTS

- 5.3.2 THREAT OF SUBSTITUTES

- 5.3.3 BARGAINING POWER OF SUPPLIERS

- 5.3.4 BARGAINING POWER OF BUYERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.4.2 BUYING CRITERIA

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 ECOSYSTEM ANALYSIS

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY, 2024

- 5.7.2 AVERAGE SELLING PRICE, BY SOURCE

- 5.7.3 AVERAGE SELLING PRICE, BY PRECURSOR TYPE

- 5.7.4 AVERAGE SELLING PRICE, BY END-USE INDUSTRY

- 5.7.5 AVERAGE SELLING PRICE, BY REGION

- 5.8 VALUE CHAIN ANALYSIS

- 5.9 TRADE ANALYSIS

- 5.9.1 EXPORT SCENARIO (HS CODE 681511)

- 5.9.2 IMPORT SCENARIO (HS CODE 681511)

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGIES FOR CFRP MANUFACTURING PROCESSES

- 5.10.1.1 Rapid integrated molding technology

- 5.10.1.2 Vacuum-assisted resin transfer molding

- 5.10.1.3 Out of autoclave technology

- 5.10.2 COMPLEMENTARY TECHNOLOGIES FOR MANUFACTURING CFRP

- 5.10.2.1 Automated fiber placement

- 5.10.2.2 3D printing

- 5.10.1 KEY TECHNOLOGIES FOR CFRP MANUFACTURING PROCESSES

- 5.11 IMPACT OF AI/GEN AI ON CF & CFRP MARKET

- 5.11.1 TOP USE CASES AND MARKET POTENTIAL

- 5.11.2 BEST PRACTICES IN CF & CFRP MARKET

- 5.11.3 CASE STUDIES OF AI IMPLEMENTATION IN CF & CFRP MARKET

- 5.12 MACROECONOMIC OUTLOOK

- 5.12.1 INTRODUCTION

- 5.12.2 GDP TRENDS AND FORECAST

- 5.12.3 TRENDS IN GLOBAL AEROSPACE & DEFENSE INDUSTRY

- 5.12.4 TRENDS IN GLOBAL WIND ENERGY INDUSTRY

- 5.12.5 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.13 PATENT ANALYSIS

- 5.13.1 INTRODUCTION

- 5.13.2 METHODOLOGY

- 5.13.3 PATENT TYPES

- 5.13.4 INSIGHTS

- 5.13.5 LEGAL STATUS

- 5.13.6 JURISDICTION ANALYSIS

- 5.13.7 TOP APPLICANTS

- 5.14 REGULATORY LANDSCAPE

- 5.14.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.15 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.16 CASE STUDY ANALYSIS

- 5.16.1 MITSUBISHI'S DEVELOPMENT OF CARBON FIBER-REINFORCED PLASTICS FOR STRUCTURAL AIRCRAFT PARTS

- 5.16.2 SGL CARBON'S CLIMATE-FRIENDLY CARBON FIBER TO REVOLUTIONIZE SUSTAINABLE MANUFACTURING

- 5.16.3 TRUE TEMPER SPORTS PARTNERS WITH HEXCEL CORPORATION FOR FIRST GOLF SHAFT LINE

- 5.17 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.18 INVESTMENT AND FUNDING SCENARIO

- 5.19 IMPACT OF 2025 US TARIFF - CF & CFRP MARKET

- 5.19.1 INTRODUCTION

- 5.19.2 KEY TARIFF RATES

- 5.19.3 PRICE IMPACT ANALYSIS

- 5.19.4 IMPACTS ON COUNTRY/REGION

- 5.19.4.1 US

- 5.19.4.2 Europe

- 5.19.4.3 Asia Pacific

- 5.19.5 IMPACT ON END-USE INDUSTRIES

6 CFRP MARKET, BY RESIN TYPE

- 6.1 INTRODUCTION

- 6.2 THERMOSETTING

- 6.2.1 SUPERIOR RESISTANCE TO HIGH TEMPERATURES TO PROPEL MARKET

- 6.2.2 EPOXY

- 6.2.2.1 Increasing demand for epoxy resins from high-end applications, such as aerospace & defense, to propel market

- 6.2.3 VINYL ESTER

- 6.2.3.1 Increased application in transportation, marine, & pipe & tank industries to drive market

- 6.2.4 POLYESTER

- 6.2.4.1 High strength, high rigidity, low temperature impact resistance, and good electrical properties to drive adoption

- 6.2.5 OTHER THERMOSETTING RESINS

- 6.3 THERMOPLASTIC

- 6.3.1 EASY RECYCLABILITY TO DRIVE ADOPTION

- 6.3.2 POLYETHERETHERKETONE (PEEK)

- 6.3.2.1 Extensive use in aerospace & defense applications to drive market

- 6.3.3 POLYAMIDE (PA)

- 6.3.3.1 Resistance to wear, heat, and chemicals, and good friction to support market growth

- 6.3.4 POLYPROPYLENE (PP)

- 6.3.4.1 Significant demand in automotive applications to drive market

- 6.3.5 OTHER THERMOPLASTIC RESINS

7 CF MARKET, BY PRECURSOR TYPE

- 7.1 INTRODUCTION

- 7.2 POLYACRYLONITRILE-BASED CARBON FIBERS

- 7.2.1 EXTENSIVE USE OF STRUCTURAL MATERIAL COMPOSITES IN AEROSPACE & DEFENSE INDUSTRY TO DRIVE MARKET

- 7.2.2 PAN-BASED CARBON FIBER, BY TOW SIZE

- 7.2.2.1 Small tow (<24K)

- 7.2.2.1.1 Small tow carbon fiber finds major applications in aerospace industry

- 7.2.2.2 Large tow (>24K)

- 7.2.2.2.1 Wind energy major application of large tow carbon fiber

- 7.2.2.1 Small tow (<24K)

- 7.3 PITCH-BASED CARBON FIBER

- 7.3.1 INCREASED USE IN APPLICATIONS REQUIRING HIGH THERMAL CONDUCTIVITY AND ELECTRIC CONDUCTIVITY TO DRIVE MARKET

- 7.3.2 PITCH-BASED CARBON FIBER, BY TOW SIZE

8 CF MARKET, BY SOURCE

- 8.1 INTRODUCTION

- 8.2 VIRGIN CARBON FIBER

- 8.2.1 BETTER THERMAL AND MECHANICAL PROPERTIES TO DRIVE MARKET

- 8.3 RECYCLED CARBON FIBER

- 8.3.1 GROWING DEMAND FOR SUSTAINABILITY TO DRIVE ADOPTION

9 CFRP MARKET, BY MANUFACTURING PROCESS

- 9.1 INTRODUCTION

- 9.2 LAY-UP PROCESS

- 9.2.1 ABILITY TO PROVIDE SUPERIOR STRENGTH AND WEIGHT TO INCREASE DEMAND

- 9.3 COMPRESSION MOLDING PROCESS

- 9.3.1 SHORT CYCLE TIME AND HIGH PRODUCTION RATE TO DRIVE DEMAND

- 9.4 RESIN TRANSFER MOLDING PROCESS

- 9.4.1 INCREASED COMPRESSION AND OUTSTANDING STRENGTH-TO-WEIGHT RATIOS TO DRIVE DEMAND

- 9.5 FILAMENT WINDING PROCESS

- 9.5.1 NEED FOR HIGHLY ENGINEERED STRUCTURES TO DRIVE ADOPTION

- 9.6 INJECTION MOLDING PROCESS

- 9.6.1 USAGE IN LOW-VOLUME AND LARGE-SIZED COMPONENTS TO DRIVE ADOPTION

- 9.7 PULTRUSION PROCESS

- 9.7.1 COST EFFECTIVE PROCESS FOR RIGID STRUCTURES-KEY FACTOR DRIVING MARKET GROWTH

- 9.8 OTHER MANUFACTURING PROCESSES

10 CFRP MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 AEROSPACE & DEFENSE

- 10.2.1 SUPERIOR AND LIGHTWEIGHT CHARACTERISTICS OF CFRP TO DRIVE MARKET

- 10.2.2 INTERIOR PARTS

- 10.2.3 EXTERIOR PARTS

- 10.3 WIND ENERGY

- 10.3.1 HIGH STRENGTH AND WEIGHT REDUCTION TO DRIVE MARKET

- 10.4 AUTOMOTIVE

- 10.4.1 INCREASING EFFICIENCY TO DRIVE MARKET

- 10.5 SPORTING GOODS

- 10.5.1 GROWING DEMAND FOR CFRP IN SPORTING GOODS TO DRIVE MARKET

- 10.6 CIVIL ENGINEERING

- 10.6.1 GROWING DEMAND FOR STRUCTURAL STRENGTHENING AND BRIDGE DECK REINFORCEMENT APPLICATIONS TO DRIVE MARKET

- 10.7 PIPE & TANK

- 10.7.1 INCREASING DEMAND FOR TYPE IV CYLINDERS TO DRIVE MARKET

- 10.8 MARINE

- 10.8.1 ANTI-CORROSION AND LIGHTWEIGHT PROPERTIES TO DRIVE MARKET

- 10.9 MEDICAL

- 10.9.1 HIGH STRENGTH, LOW WEIGHT, CORROSION RESISTANCE, AND BIOCOMPATIBILITY TO DRIVE MARKET

- 10.10 ELECTRICAL & ELECTRONICS

- 10.10.1 SUPERIOR MECHANICAL PROPERTIES TO DRIVE MARKET

- 10.11 OTHER END-USE INDUSTRIES

11 CFRP MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: CFRP MARKET, BY RESIN TYPE

- 11.2.2 NORTH AMERICA: CFRP MARKET, BY MANUFACTURING PROCESS

- 11.2.3 NORTH AMERICA: CFRP MARKET, BY END-USE INDUSTRY

- 11.2.4 NORTH AMERICA: CFRP MARKET, BY COUNTRY

- 11.2.4.1 US

- 11.2.4.1.1 Presence of well-established industries to drive market

- 11.2.4.2 Canada

- 11.2.4.2.1 Presence of well-established aerospace industry to fuel demand

- 11.2.4.1 US

- 11.3 EUROPE

- 11.3.1 EUROPE: CFRP MARKET, BY RESIN TYPE

- 11.3.2 EUROPE: CFRP MARKET, BY MANUFACTURING PROCESS

- 11.3.3 EUROPE: CFRP MARKET, BY END-USE INDUSTRY

- 11.3.4 EUROPE: CFRP MARKET, BY COUNTRY

- 11.3.4.1 GERMANY

- 11.3.4.1.1 Growth of automotive and aerospace industries to drive market

- 11.3.4.2 France

- 11.3.4.2.1 Presence of major aircraft manufacturers to drive market

- 11.3.4.3 UK

- 11.3.4.3.1 Increasing demand for lightweight and high-performance materials to drive market

- 11.3.4.4 Italy

- 11.3.4.4.1 Growing demand for motorsports to drive market

- 11.3.4.5 Spain

- 11.3.4.5.1 High demand for CFRP from aerospace sector to drive market

- 11.3.4.6 Russia

- 11.3.4.6.1 Presence of major carbon fiber manufacturers to drive market

- 11.3.4.7 Rest of Europe

- 11.3.4.1 GERMANY

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: CFRP MARKET, BY RESIN TYPE

- 11.4.2 ASIA PACIFIC: CFRP MARKET, BY MANUFACTURING PROCESS

- 11.4.3 ASIA PACIFIC: CFRP MARKET, BY END-USE INDUSTRY

- 11.4.4 ASIA PACIFIC: CFRP MARKET, BY COUNTRY

- 11.4.4.1 China

- 11.4.4.1.1 Carbon fiber innovations in various sectors to drive market

- 11.4.4.2 Japan

- 11.4.4.2.1 Increasing use of CFRP in consumer electronics to drive market

- 11.4.4.3 Taiwan

- 11.4.4.3.1 Growing demand for bicycles to drive market

- 11.4.4.4 South Korea

- 11.4.4.4.1 Presence of major automotive companies to propel market

- 11.4.4.5 Rest of Asia Pacific

- 11.4.4.1 China

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 MIDDLE EAST & AFRICA: CFRP MARKET, BY RESIN TYPE

- 11.5.2 MIDDLE EAST & AFRICA: CFRP MARKET, BY MANUFACTURING PROCESS

- 11.5.3 MIDDLE EAST & AFRICA: CFRP MARKET, BY END-USE INDUSTRY

- 11.5.4 MIDDLE EAST & AFRICA: CFRP MARKET, BY COUNTRY

- 11.5.4.1 GCC Countries

- 11.5.4.1.1 UAE

- 11.5.4.1.1.1 Stringent energy-efficiency regulations to drive market

- 11.5.4.1.2 Saudi Arabia

- 11.5.4.1.2.1 High demand from pipe & tank industry to drive market

- 11.5.4.1.3 Rest of GCC Countries

- 11.5.4.1.1 UAE

- 11.5.4.2 South Africa

- 11.5.4.2.1 Growing wind energy, automotive, and aerospace & defense industries to drive market

- 11.5.4.3 Rest of Middle East & Africa

- 11.5.4.1 GCC Countries

- 11.6 LATIN AMERICA

- 11.6.1 LATIN AMERICA: CFRP MARKET, BY RESIN TYPE

- 11.6.2 LATIN AMERICA: CFRP MARKET, BY MANUFACTURING PROCESS

- 11.6.3 LATIN AMERICA: CFRP MARKET, BY END-USE INDUSTRY

- 11.6.4 LATIN AMERICA: CFRP MARKET, BY COUNTRY

- 11.6.4.1 Brazil

- 11.6.4.1.1 Growth of aerospace & defense and wind energy industries to drive market

- 11.6.4.2 Mexico

- 11.6.4.2.1 Automotive industry to be prominent consumer of CFRP

- 11.6.4.3 Rest of Latin America

- 11.6.4.1 Brazil

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS, 2024

- 12.4 MARKET SHARE ANALYSIS, 2024

- 12.5 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 12.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.6.1 STARS

- 12.6.2 EMERGING LEADERS

- 12.6.3 PERVASIVE PLAYERS

- 12.6.4 PARTICIPANTS

- 12.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.6.5.1 Company footprint

- 12.6.5.2 Region footprint

- 12.6.5.3 Source footprint

- 12.6.5.4 Precursor type footprint

- 12.6.5.5 Resin type footprint

- 12.6.5.6 Manufacturing process footprint

- 12.6.5.7 End-use industry footprint

- 12.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 RESPONSIVE COMPANIES

- 12.7.3 DYNAMIC COMPANIES

- 12.7.4 STARTING BLOCKS

- 12.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.7.5.1 Detailed list of key startups/SMEs

- 12.7.5.2 Competitive benchmarking of key startups/SMEs

- 12.8 COMPANY VALUATION AND FINANCIAL METRICS

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 TORAY INDUSTRIES, INC.

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.3.4 Other developments

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 TEIJIN LIMITED

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.3.4 Other developments

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 MITSUBISHI CHEMICAL CORPORATION

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 HEXCEL CORPORATION

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 SYENSQO

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches

- 13.1.5.3.2 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Key strengths

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses & competitive threats

- 13.1.6 SGL CARBON

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches

- 13.1.6.3.2 Deals

- 13.1.6.3.3 Expansions

- 13.1.6.4 MnM view

- 13.1.6.4.1 Key strengths

- 13.1.6.4.2 Strategic choices

- 13.1.6.4.3 Weaknesses & competitive threats

- 13.1.7 HS HYOSUNG ADVANCED MATERIALS

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches

- 13.1.7.3.2 Deals

- 13.1.7.3.3 Expansions

- 13.1.7.4 MnM view

- 13.1.7.4.1 Key strengths

- 13.1.7.4.2 Strategic choices

- 13.1.7.4.3 Weaknesses & competitive threats

- 13.1.8 ZHONGFU SHENYING CARBON FIBER CO., LTD.

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Expansions

- 13.1.8.4 MnM view

- 13.1.8.4.1 Key strengths

- 13.1.8.4.2 Strategic choices

- 13.1.8.4.3 Weaknesses & competitive threats

- 13.1.9 KUREHA CORPORATION

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 MnM view

- 13.1.9.3.1 Key strengths

- 13.1.9.3.2 Strategic choices

- 13.1.9.3.3 Weaknesses & competitive threats

- 13.1.10 DOWAKSA

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Expansions

- 13.1.10.4 MnM view

- 13.1.10.4.1 Key strengths

- 13.1.10.4.2 Strategic choices

- 13.1.10.4.3 Weaknesses & competitive threats

- 13.1.11 WEIHAI GUANGWEI COMPOSITE MATERIALS CO., LTD.

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.11.3 MnM view

- 13.1.11.3.1 Key strengths

- 13.1.11.3.2 Strategic choices

- 13.1.11.3.3 Weaknesses & competitive threats

- 13.1.12 UMATEX

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.12.3 MnM view

- 13.1.12.3.1 Key strengths

- 13.1.12.3.2 Strategic choices

- 13.1.12.3.3 Weaknesses & competitive threats

- 13.1.13 JILIN CHEMICAL FIBER GROUP CO., LTD.

- 13.1.13.1 Business overview

- 13.1.13.2 Products offered

- 13.1.13.3 MnM view

- 13.1.13.3.1 Key strengths

- 13.1.13.3.2 Strategic choices

- 13.1.13.3.3 Weaknesses & competitive threats

- 13.1.14 JIANGSU HENGSHEN CO., LTD.

- 13.1.14.1 Business overview

- 13.1.14.2 Products offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Expansions

- 13.1.14.4 MnM view

- 13.1.14.4.1 Key strengths

- 13.1.14.4.2 Strategic choices

- 13.1.14.4.3 Weaknesses & competitive threats

- 13.1.15 CHINA NATIONAL BLUESTAR (GROUP) CO., LTD.

- 13.1.15.1 Business overview

- 13.1.15.2 Products offered

- 13.1.15.3 MnM view

- 13.1.15.3.1 Key strengths

- 13.1.15.3.2 Strategic choices

- 13.1.15.3.3 Weaknesses & competitive threats

- 13.1.1 TORAY INDUSTRIES, INC.

- 13.2 OTHER PLAYERS

- 13.2.1 TAEKWANG INDUSTRIAL CO., LTD.

- 13.2.2 GEN 2 CARBON

- 13.2.3 NIPPON GRAPHITE FIBER CO., LTD.

- 13.2.4 CHANGZHOU JLON COMPOSITE CO., LTD.

- 13.2.5 MALLINDA

- 13.2.6 BCIRCULAR

- 13.2.7 VARTEGA INC.

- 13.2.8 JILIN TANGU CARBON FIBER CO., LTD.

- 13.2.9 WUXI GDE TECHNOLOGY CO., LTD.

- 13.2.10 SINOFIBERS TECHNOLOGY CO., LTD.

- 13.2.11 JILIN JIYAN HIGH-TECH FIBERS CO., LTD.

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS

List of Tables

- TABLE 1 NEW WIND POWER INSTALLATIONS (OFFSHORE), BY REGION, 2023-2033 (GW)

- TABLE 2 CF & CFRP MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 3 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END-USE INDUSTRY

- TABLE 4 KEY BUYING CRITERIA, BY END-USE INDUSTRY

- TABLE 5 CF & CFRP MARKET: ROLE IN ECOSYSTEM

- TABLE 6 AVERAGE SELLING PRICE OF CFRP MARKET OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY, 2024 (USD/KG)

- TABLE 7 AVERAGE SELLING PRICE OF CFRP, BY REGION, 2022-2030 (USD/KG)

- TABLE 8 TOP 10 EXPORTING COUNTRIES OF CARBON FIBERS IN 2024

- TABLE 9 TOP 10 IMPORTING COUNTRIES OF CARBON FIBERS IN 2024

- TABLE 10 TOP USE CASES AND MARKET POTENTIAL

- TABLE 11 BEST PRACTICES: COMPANIES IMPLEMENTING USE CASES

- TABLE 12 CASE STUDIES OF AI IMPLEMENTATION IN CF & CFRP MARKET

- TABLE 13 GDP PERCENTAGE (%) CHANGE, BY KEY COUNTRY, 2021-2029

- TABLE 14 CF & CFRP MARKET: TOTAL NUMBER OF PATENTS

- TABLE 15 LIST OF PATENTS BY TORAY INDUSTRIES, INC.

- TABLE 16 LIST OF PATENTS BY TEIJIN LIMITED

- TABLE 17 US: TOP 10 PATENT OWNERS IN LAST 10 YEARS

- TABLE 18 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 21 CF & CFRP MARKET: KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 22 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 23 KEY PRODUCT-RELATED TARIFFS EFFECTIVE FOR CF & CFRP

- TABLE 24 EXPECTED CHANGE IN PRICES AND IMPACT ON END-USE MARKET DUE TO TARIFFS

- TABLE 25 CFRP MARKET, BY RESIN TYPE, 2022-2024 (USD MILLION)

- TABLE 26 CFRP MARKET, BY RESIN TYPE, 2022-2024 (KILOTON)

- TABLE 27 CFRP MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 28 CFRP MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 29 THERMOSETTING: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 30 THERMOSETTING: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 31 THERMOSETTING: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 32 THERMOSETTING: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 33 THERMOSETTING: CFRP MARKET, BY RESIN TYPE, 2022-2024 (USD MILLION)

- TABLE 34 THERMOSETTING: CFRP MARKET, BY RESIN TYPE, 2022-2024 (KILOTON)

- TABLE 35 THERMOSETTING: CFRP MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 36 THERMOSETTING: CFRP MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 37 THERMOPLASTIC: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 38 THERMOPLASTIC: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 39 THERMOPLASTIC: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 40 THERMOPLASTIC: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 41 THERMOPLASTIC: CFRP MARKET, BY RESIN TYPE, 2022-2024 (USD MILLION)

- TABLE 42 THERMOPLASTIC: CFRP MARKET, BY RESIN TYPE, 2022-2024 (KILOTON)

- TABLE 43 THERMOPLASTIC: CFRP MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 44 THERMOPLASTIC: CFRP MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 45 CF MARKET, BY PRECURSOR TYPE, 2022-2024 (USD MILLION)

- TABLE 46 CF MARKET, BY PRECURSOR TYPE, 2022-2024 (KILOTON)

- TABLE 47 CF MARKET, BY PRECURSOR TYPE, 2025-2030 (USD MILLION)

- TABLE 48 CF MARKET, BY PRECURSOR TYPE, 2025-2030 (KILOTON)

- TABLE 49 PAN-BASED CF MARKET, BY TOW SIZE, 2022-2024 (USD MILLION)

- TABLE 50 PAN-BASED CF MARKET, BY TOW SIZE, 2022-2024 (KILOTON)

- TABLE 51 PAN-BASED CF MARKET, BY TOW SIZE, 2025-2030 (USD MILLION)

- TABLE 52 PAN-BASED CF MARKET, BY TOW SIZE, 2025-2030 (KILOTON)

- TABLE 53 PITCH-BASED CF MARKET, BY TOW SIZE, 2022-2024 (USD MILLION)

- TABLE 54 PITCH-BASED CF MARKET, BY TOW SIZE, 2022-2024 (KILOTON)

- TABLE 55 PITCH-BASED CF MARKET, BY TOW SIZE, 2025-2030 (USD MILLION)

- TABLE 56 PITCH-BASED CF MARKET, BY TOW SIZE, 2025-2030 (KILOTON)

- TABLE 57 CF MARKET, BY SOURCE, 2022-2024 (USD MILLION)

- TABLE 58 CF MARKET, BY SOURCE, 2022-2024 (KILOTON)

- TABLE 59 CF MARKET, BY SOURCE, 2025-2030 (USD MILLION)

- TABLE 60 CF MARKET, BY SOURCE, 2025-2030 (KILOTON)

- TABLE 61 VIRGIN: CF MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 62 VIRGIN: CF MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 63 VIRGIN: CF MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 64 VIRGIN: CF MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 65 RECYCLED: CF MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 66 RECYCLED: CF MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 67 RECYCLED: CF MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 68 RECYCLED: CF MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 69 CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (USD MILLION)

- TABLE 70 CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (KILOTON)

- TABLE 71 CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (USD MILLION)

- TABLE 72 CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (KILOTON)

- TABLE 73 LAY-UP PROCESS: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 74 LAY-UP PROCESS: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 75 LAY-UP PROCESS: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 76 LAY-UP PROCESS: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 77 COMPRESSION MOLDING PROCESS: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 78 COMPRESSION MOLDING PROCESS: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 79 COMPRESSION MOLDING PROCESS: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 80 COMPRESSION MOLDING PROCESS: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 81 RESIN TRANSFER MOLDING PROCESS: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 82 RESIN TRANSFER MOLDING PROCESS: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 83 RESIN TRANSFER MOLDING PROCESS: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 84 RESIN TRANSFER MOLDING PROCESS: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 85 FILAMENT WINDING PROCESS: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 86 FILAMENT WINDING PROCESS: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 87 FILAMENT WINDING PROCESS: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 88 FILAMENT WINDING PROCESS: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 89 INJECTION MOLDING PROCESS: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 90 INJECTION MOLDING PROCESS: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 91 INJECTION MOLDING PROCESS: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 92 INJECTION MOLDING PROCESS: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 93 PULTRUSION PROCESS: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 94 PULTRUSION PROCESS: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 95 PULTRUSION PROCESS: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 96 PULTRUSION PROCESS: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 97 OTHER MANUFACTURING PROCESSES: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 98 OTHER MANUFACTURING PROCESSES: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 99 OTHER MANUFACTURING PROCESSES: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 100 OTHER MANUFACTURING PROCESSES: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 101 CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 102 CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 103 CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 104 CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 105 NEW COMMERCIAL AIRPLANE DELIVERIES, 2025-2044

- TABLE 106 AEROSPACE & DEFENSE: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 107 AEROSPACE & DEFENSE: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 108 AEROSPACE & DEFENSE: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 109 AEROSPACE & DEFENSE: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 110 WIND ENERGY: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 111 WIND ENERGY: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 112 WIND ENERGY: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 113 WIND ENERGY: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 114 COST BENEFITS OF CARBON FIBER COMPOSITE COMPONENTS VS. STEEL COMPONENTS

- TABLE 115 AUTOMOTIVE: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 116 AUTOMOTIVE: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 117 AUTOMOTIVE: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 118 AUTOMOTIVE: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 119 SPORTING GOODS: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 120 SPORTING GOODS: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 121 SPORTING GOODS: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 122 SPORTING GOODS: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 123 CIVIL ENGINEERING: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 124 CIVIL ENGINEERING: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 125 CIVIL ENGINEERING: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 126 CIVIL ENGINEERING: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 127 PIPE & TANK: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 128 PIPE & TANK: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 129 PIPE & TANK: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 130 PIPE & TANK: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 131 MARINE: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 132 MARINE: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 133 MARINE: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 134 MARINE: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 135 MEDICAL: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 136 MEDICAL: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 137 MEDICAL: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 138 MEDICAL: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 139 ELECTRICAL & ELECTRONICS: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 140 ELECTRICAL & ELECTRONICS: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 141 ELECTRICAL & ELECTRONICS: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 142 ELECTRICAL & ELECTRONICS: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 143 OTHER END-USE INDUSTRIES: CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 144 OTHER END-USE INDUSTRIES: CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 145 OTHER END-USE INDUSTRIES: CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 146 OTHER END-USE INDUSTRIES: CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 147 CFRP MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 148 CFRP MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 149 CFRP MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 150 CFRP MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 151 NORTH AMERICA: CFRP MARKET, BY RESIN TYPE, 2022-2024 (USD MILLION)

- TABLE 152 NORTH AMERICA: CFRP MARKET, BY RESIN TYPE, 2022-2024 (KILOTON)

- TABLE 153 NORTH AMERICA: CFRP MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 154 NORTH AMERICA: CFRP MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 155 NORTH AMERICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (USD MILLION)

- TABLE 156 NORTH AMERICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (KILOTON)

- TABLE 157 NORTH AMERICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (USD MILLION)

- TABLE 158 NORTH AMERICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (KILOTON)

- TABLE 159 NORTH AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 160 NORTH AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 161 NORTH AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 162 NORTH AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 163 NORTH AMERICA: CFRP MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 164 NORTH AMERICA: CFRP MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 165 NORTH AMERICA: CFRP MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 166 NORTH AMERICA: CFRP MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 167 US: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 168 US: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 169 US: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 170 US: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 171 CANADA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 172 CANADA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 173 CANADA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 174 CANADA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 175 EUROPE: CFRP MARKET, BY RESIN TYPE, 2022-2024 (USD MILLION)

- TABLE 176 EUROPE: CFRP MARKET, BY RESIN TYPE, 2022-2024 (KILOTON)

- TABLE 177 EUROPE: CFRP MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 178 EUROPE: CFRP MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 179 EUROPE: CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (USD MILLION)

- TABLE 180 EUROPE: CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (KILOTON)

- TABLE 181 EUROPE: CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (USD MILLION)

- TABLE 182 EUROPE: CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (KILOTON)

- TABLE 183 EUROPE: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 184 EUROPE: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 185 EUROPE: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 186 EUROPE: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 187 EUROPE: CFRP MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 188 EUROPE: CFRP MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 189 EUROPE: CFRP MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 190 EUROPE: CFRP MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 191 GERMANY: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 192 GERMANY: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 193 GERMANY: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 194 GERMANY: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 195 FRANCE: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 196 FRANCE: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 197 FRANCE: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 198 FRANCE: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 199 UK: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 200 UK: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 201 UK: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 202 UK: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 203 ITALY: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 204 ITALY: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 205 ITALY: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 206 ITALY: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 207 SPAIN: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 208 SPAIN: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 209 SPAIN: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 210 SPAIN: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 211 RUSSIA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 212 RUSSIA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 213 RUSSIA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 214 RUSSIA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 215 REST OF EUROPE: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 216 REST OF EUROPE: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 217 REST OF EUROPE: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 218 REST OF EUROPE: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 219 ASIA PACIFIC: CFRP MARKET, BY RESIN TYPE, 2022-2024 (USD MILLION)

- TABLE 220 ASIA PACIFIC: CFRP MARKET, BY RESIN TYPE, 2022-2024 (KILOTON)

- TABLE 221 ASIA PACIFIC: CFRP MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 222 ASIA PACIFIC: CFRP MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 223 ASIA PACIFIC: CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (USD MILLION)

- TABLE 224 ASIA PACIFIC: CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (KILOTON)

- TABLE 225 ASIA PACIFIC: CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (USD MILLION)

- TABLE 226 ASIA PACIFIC: CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (KILOTON)

- TABLE 227 ASIA PACIFIC: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 228 ASIA PACIFIC: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 229 ASIA PACIFIC: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 230 ASIA PACIFIC: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 231 ASIA PACIFIC: CFRP MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 232 ASIA PACIFIC: CFRP MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 233 ASIA PACIFIC: CFRP MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 234 ASIA PACIFIC: CFRP MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 235 CHINA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 236 CHINA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 237 CHINA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 238 CHINA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 239 JAPAN: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 240 JAPAN: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 241 JAPAN: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 242 JAPAN: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 243 TAIWAN: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 244 TAIWAN: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 245 TAIWAN: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 246 TAIWAN: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 247 SOUTH KOREA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 248 SOUTH KOREA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 249 SOUTH KOREA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 250 SOUTH KOREA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 251 REST OF ASIA PACIFIC: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 252 REST OF ASIA PACIFIC: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 253 REST OF ASIA PACIFIC: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 254 REST OF ASIA PACIFIC: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 255 MIDDLE EAST & AFRICA: CFRP MARKET, BY RESIN TYPE, 2022-2024 (USD MILLION)

- TABLE 256 MIDDLE EAST & AFRICA: CFRP MARKET, BY RESIN TYPE, 2022-2024 (KILOTON)

- TABLE 257 MIDDLE EAST & AFRICA: CFRP MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 258 MIDDLE EAST & AFRICA: CFRP MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 259 MIDDLE EAST & AFRICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (USD MILLION)

- TABLE 260 MIDDLE EAST & AFRICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (KILOTON)

- TABLE 261 MIDDLE EAST & AFRICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (USD MILLION)

- TABLE 262 MIDDLE EAST & AFRICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (KILOTON)

- TABLE 263 MIDDLE EAST & AFRICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 264 MIDDLE EAST & AFRICA: CFRP MARKET, BY END-USE INDUSTRY, BY REGION, 2022-2024 (KILOTON)

- TABLE 265 MIDDLE EAST & AFRICA: CFRP MARKET, BY END-USE INDUSTRY, BY REGION, 2025-2030 (USD MILLION)

- TABLE 266 MIDDLE EAST & AFRICA: CFRP MARKET, BY END-USE INDUSTRY, BY REGION, 2025-2030 (KILOTON)

- TABLE 267 MIDDLE EAST & AFRICA: CFRP MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 268 MIDDLE EAST & AFRICA: CFRP MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 269 MIDDLE EAST & AFRICA: CFRP MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 270 MIDDLE EAST & AFRICA: CFRP MARKET, BY COUNTRY 2025-2030 (KILOTON)

- TABLE 271 UAE: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 272 UAE: CFRP MARKET, BY END-USE INDUSTRY, BY REGION, 2022-2024 (KILOTON)

- TABLE 273 UAE: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 274 UAE: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 275 SAUDI ARABIA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 276 SAUDI ARABIA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 277 SAUDI ARABIA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 278 SAUDI ARABIA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 279 REST OF GCC COUNTRIES: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 280 REST OF GCC COUNTRIES: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 281 REST OF GCC COUNTRIES: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 282 REST OF GCC COUNTRIES: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 283 SOUTH AFRICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 284 SOUTH AFRICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 285 SOUTH AFRICA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 286 SOUTH AFRICA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 287 REST OF MIDDLE EAST & AFRICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 288 REST OF MIDDLE EAST & AFRICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 289 REST OF MIDDLE EAST & AFRICA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 290 REST OF MIDDLE EAST & AFRICA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 291 LATIN AMERICA: CFRP MARKET, BY RESIN TYPE, 2022-2024 (USD MILLION)

- TABLE 292 LATIN AMERICA: CFRP MARKET, BY RESIN TYPE, 2022-2024 (KILOTON)

- TABLE 293 LATIN AMERICA: CFRP MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 294 LATIN AMERICA: CFRP MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 295 LATIN AMERICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (USD MILLION)

- TABLE 296 LATIN AMERICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2022-2024 (KILOTON)

- TABLE 297 LATIN AMERICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (USD MILLION)

- TABLE 298 LATIN AMERICA: CFRP MARKET, BY MANUFACTURING PROCESS, 2025-2030 (KILOTON)

- TABLE 299 LATIN AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 300 LATIN AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 301 LATIN AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 302 LATIN AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 303 LATIN AMERICA: CFRP MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 304 LATIN AMERICA: CFRP MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 305 LATIN AMERICA: CFRP MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 306 LATIN AMERICA: CFRP MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 307 BRAZIL: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 308 BRAZIL: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 309 BRAZIL: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 310 BRAZIL: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 311 MEXICO: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 312 MEXICO: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 313 MEXICO: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 314 MEXICO: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 315 REST OF LATIN AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 316 REST OF LATIN AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 317 REST OF LATIN AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 318 REST OF LATIN AMERICA: CFRP MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 319 CF & CFRP MARKET: KEY STRATEGIES ADOPTED BY MAJOR PLAYERS, JANUARY 2020-MARCH 2025

- TABLE 320 CF & CFRP MARKET: DEGREE OF COMPETITION, 2024

- TABLE 321 CF & CFRP MARKET: REGION FOOTPRINT

- TABLE 322 CF & CFRP MARKET: SOURCE FOOTPRINT

- TABLE 323 CF & CFRP MARKET: PRECURSOR TYPE FOOTPRINT

- TABLE 324 CF & CFRP MARKET: RESIN TYPE FOOTPRINT

- TABLE 325 CF & CFRP MARKET: MANUFACTURING PROCESS FOOTPRINT

- TABLE 326 CF & CFRP MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 327 CF & CFRP MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 328 CF & CFRP MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (1/2)

- TABLE 329 CF& CFRP MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (2/2)

- TABLE 330 CF & CFRP MARKET: PRODUCT LAUNCHES, JANUARY 2020-MAY 2025

- TABLE 331 CF & CFRP MARKET: DEALS, JANUARY 2020-MAY 2025

- TABLE 332 CF & CFRP MARKET: EXPANSIONS, JANUARY 2020-MAY 2025

- TABLE 333 TORAY INDUSTRIES, INC.: COMPANY OVERVIEW

- TABLE 334 TORAY INDUSTRIES, INC.: PRODUCTS OFFERED

- TABLE 335 TORAY INDUSTRIES, INC.: PRODUCT LAUNCHES

- TABLE 336 TORAY INDUSTRIES, INC.: DEALS

- TABLE 337 TORAY INDUSTRIES, INC.: EXPANSIONS

- TABLE 338 TORAY INDUSTRIES, INC.: OTHER DEVELOPMENTS

- TABLE 339 TEIJIN LIMITED: COMPANY OVERVIEW

- TABLE 340 TEIJIN LIMITED: PRODUCTS OFFERED

- TABLE 341 TEIJIN LIMITED: PRODUCT LAUNCHES

- TABLE 342 TEIJIN LIMITED: DEALS

- TABLE 343 TEIJIN LIMITED: EXPANSIONS

- TABLE 344 TEIJIN LIMITED: OTHER DEVELOPMENTS

- TABLE 345 MITSUBISHI CHEMICAL CORPORATION: COMPANY OVERVIEW

- TABLE 346 MITSUBISHI CHEMICAL CORPORATION: PRODUCTS OFFERED

- TABLE 347 MITSUBISHI CHEMICAL CORPORATION: PRODUCT LAUNCHES

- TABLE 348 MITSUBISHI CHEMICAL CORPORATION: DEALS

- TABLE 349 HEXCEL CORPORATION: COMPANY OVERVIEW

- TABLE 350 HEXCEL CORPORATION: PRODUCTS OFFERED

- TABLE 351 HEXCEL CORPORATION: PRODUCT LAUNCHES

- TABLE 352 HEXCEL CORPORATION: DEALS

- TABLE 353 HEXCEL CORPORATION: EXPANSIONS

- TABLE 354 SYENSQO: COMPANY OVERVIEW

- TABLE 355 SYENSQO: PRODUCTS OFFERED

- TABLE 356 SYENSQO: PRODUCT LAUNCHES

- TABLE 357 SYENSQO: DEALS

- TABLE 358 SGL CARBON: COMPANY OVERVIEW

- TABLE 359 SGL CARBON: PRODUCTS OFFERED

- TABLE 360 SGL CARBON: PRODUCT LAUNCHES

- TABLE 361 SGL CARBON: DEALS

- TABLE 362 SGL CARBON: EXPANSIONS

- TABLE 363 HS HYOSUNG ADVANCED MATERIALS: COMPANY OVERVIEW

- TABLE 364 HS HYOSUNG ADVANCED MATERIALS: PRODUCTS OFFERED

- TABLE 365 HS HYOSUNG ADVANCED MATERIALS: PRODUCT LAUNCHES

- TABLE 366 HS HYOSUNG ADVANCED MATERIALS: DEALS

- TABLE 367 HS HYOSUNG ADVANCED MATERIALS: EXPANSIONS

- TABLE 368 ZHONGFU SHENYING CARBON FIBER CO., LTD.: COMPANY OVERVIEW

- TABLE 369 ZHONGFU SHENYING CARBON FIBER CO., LTD.: PRODUCTS OFFERED

- TABLE 370 ZHONGFU SHENYING CARBON FIBER CO., LTD.: EXPANSIONS

- TABLE 371 KUREHA CORPORATION: COMPANY OVERVIEW

- TABLE 372 KUREHA CORPORATION: PRODUCTS OFFERED

- TABLE 373 DOWAKSA: COMPANY OVERVIEW

- TABLE 374 DOWAKSA: PRODUCTS OFFERED

- TABLE 375 DOWAKSA: EXPANSIONS

- TABLE 376 WEIHAI GUANGWEI COMPOSITE MATERIALS CO., LTD.: COMPANY OVERVIEW

- TABLE 377 WEIHAI GUANGWEI COMPOSITE MATERIALS CO., LTD.: PRODUCTS OFFERED

- TABLE 378 UMATEX: COMPANY OVERVIEW

- TABLE 379 UMATEX: PRODUCTS OFFERED

- TABLE 380 JILIN CHEMICAL FIBER GROUP CO., LTD.: COMPANY OVERVIEW

- TABLE 381 JILIN CHEMICAL FIBER GROUP CO., LTD.: PRODUCTS OFFERED

- TABLE 382 JIANGSU HENGSHEN CO., LTD.: COMPANY OVERVIEW

- TABLE 383 JIANGSU HENGSHEN CO., LTD.: PRODUCTS OFFERED

- TABLE 384 JIANGSU HENGSHEN CO., LTD.: EXPANSIONS

- TABLE 385 CHINA NATIONAL BLUESTAR (GROUP) CO., LTD.: COMPANY OVERVIEW

- TABLE 386 CHINA NATIONAL BLUESTAR (GROUP) CO., LTD.: PRODUCTS OFFERED

- TABLE 387 TAEKWANG INDUSTRIAL CO., LTD.: COMPANY OVERVIEW

- TABLE 388 GEN 2 CARBON: COMPANY OVERVIEW

- TABLE 389 NIPPON GRAPHITE FIBER CO., LTD.: COMPANY OVERVIEW

- TABLE 390 CHANGZHOU JLON COMPOSITE CO., LTD.: COMPANY OVERVIEW

- TABLE 391 MALLINDA: COMPANY OVERVIEW

- TABLE 392 BCIRCULAR: COMPANY OVERVIEW

- TABLE 393 VARTEGA INC.: COMPANY OVERVIEW

- TABLE 394 JILIN TANGU CARBON FIBER CO., LTD.: COMPANY OVERVIEW

- TABLE 395 WUXI GDE TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

- TABLE 396 SINOFIBERS TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

- TABLE 397 JILIN JIYAN HIGH-TECH FIBERS CO., LTD.: COMPANY OVERVIEW

List of Figures

- FIGURE 1 CF & CFRP MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 CF & CFRP MARKET: RESEARCH DESIGN

- FIGURE 3 CF & CFRP MARKET: BOTTOM-UP APPROACH

- FIGURE 4 CF & CFRP MARKET: TOP-DOWN APPROACH

- FIGURE 5 CF & CFRP MARKET: DATA TRIANGULATION

- FIGURE 6 PAN-BASED CARBON FIBERS SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 7 VIRGIN CARBON FIBER SEGMENT TO DOMINATE MARKET IN 2025

- FIGURE 8 THERMOSETTING SEGMENT TO DOMINATE MARKET FROM 2025 TO 2030

- FIGURE 9 FILAMENT WINDING SEGMENT TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- FIGURE 10 AEROSPACE & DEFENSE SEGMENT TO DOMINATE MARKET BETWEEN 2025 & 2030

- FIGURE 11 NORTH AMERICA TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 12 INCREASING DEMAND FROM WIND ENERGY TO DRIVE MARKET

- FIGURE 13 WIND ENERGY SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 14 PAN-BASED CARBON FIBERS SEGMENT TO REGISTER HIGHER CAGR IN MARKET, BY VOLUME

- FIGURE 15 RECYCLED CARBON FIBERS SEGMENT TO REGISTER HIGHER CAGR, BY VOLUME, DURING FORECASTED PERIOD

- FIGURE 16 THERMOPLASTIC RESINS SEGMENT TO REGISTER HIGHER CAGR DURING FORECASTED PERIOD

- FIGURE 17 FILAMENT WINDING SEGMENT TO REGISTER HIGHEST CAGR, BY VOLUME, DURING FORECAST PERIOD

- FIGURE 18 PIPE & TANK SEGMENT TO REGISTER HIGHEST CAGR DURING FORECASTED PERIOD

- FIGURE 19 CHINA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 20 CF & CFRP MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 21 CF & CFRP MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END-USE INDUSTRY

- FIGURE 23 KEY BUYING CRITERIA, BY END-USE INDUSTRY

- FIGURE 24 CF & CFRP MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 25 CF & CFRP MARKET: KEY STAKEHOLDERS IN ECOSYSTEM

- FIGURE 26 AVERAGE SELLING PRICE TREND OF CFRP OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY, 2024 (USD/KG)

- FIGURE 27 AVERAGE SELLING PRICE, 2022-2024 (USD/KG)

- FIGURE 28 CF & CFRP MARKET: VALUE CHAIN ANALYSIS

- FIGURE 29 EXPORT DATA OF HS CODE 681511-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2022-2024 (USD THOUSAND)

- FIGURE 30 IMPORT DATA OF HS CODE 681511-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2022-2024 (USD THOUSAND)

- FIGURE 31 PATENT ANALYSIS, BY PATENT TYPE

- FIGURE 32 PATENT PUBLICATION TRENDS, JANUARY 2015-DECEMBER 2024

- FIGURE 33 CF & CFRP MARKET: LEGAL STATUS OF PATENTS

- FIGURE 34 CHINA JURISDICTION REGISTERED HIGHEST NUMBER OF PATENTS

- FIGURE 35 TORAY INDUSTRIES, INC. REGISTERED HIGHEST NUMBER OF PATENTS

- FIGURE 36 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 37 CF & CFRP MARKET: DEALS AND FUNDING SOARED IN 2021

- FIGURE 38 THERMOSETTING SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 39 PAN-BASED CARBON FIBERS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 40 VIRGIN CARBON FIBER SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 41 FILAMENT WINDING PROCESS SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 42 AEROSPACE & DEFENSE INDUSTRY TO LEAD CONSUMPTION OF CFRP IN 2030

- FIGURE 43 GERMANY TO BE FASTEST-GROWING CFRP MARKET DURING FORECAST PERIOD

- FIGURE 44 NORTH AMERICA: CFRP MARKET SNAPSHOT

- FIGURE 45 EUROPE: CFRP MARKET SNAPSHOT

- FIGURE 46 ASIA PACIFIC: CFRP MARKET SNAPSHOT

- FIGURE 47 CF & CFRP MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2020-2024 (USD MILLION)

- FIGURE 48 CF & CFRP MARKET SHARE ANALYSIS, 2024

- FIGURE 49 CF & CFRP MARKET: TOP TRENDING BRANDS/PRODUCTS

- FIGURE 50 CF & CFRP MARKET: BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 51 CF & CFRP MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 52 CF & CFRP MARKET: COMPANY FOOTPRINT

- FIGURE 53 CF & CFRP MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 54 CF & CFRP MARKET: EV/EBITDA OF KEY VENDORS

- FIGURE 55 CF & CFRP MARKET: COMPANY VALUATION, 2024 (USD BILLION)

- FIGURE 56 CF & CFRP MARKET: YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 57 TORAY INDUSTRIES, INC.: COMPANY SNAPSHOT

- FIGURE 58 TEIJIN LIMITED: COMPANY SNAPSHOT

- FIGURE 59 MITSUBISHI CHEMICAL CORPORATION: COMPANY SNAPSHOT

- FIGURE 60 HEXCEL CORPORATION: COMPANY SNAPSHOT

- FIGURE 61 SYENSQO: COMPANY SNAPSHOT

- FIGURE 62 SGL CARBON: COMPANY SNAPSHOT

- FIGURE 63 HS HYOSUNG ADVANCED MATERIALS: COMPANY SNAPSHOT

- FIGURE 64 ZHONGFU SHENYING CARBON FIBER CO., LTD.: COMPANY SNAPSHOT

- FIGURE 65 KUREHA CORPORATION: COMPANY SNAPSHOT

- FIGURE 66 WEIHAI GUANGWEI COMPOSITE MATERIALS CO., LTD.: COMPANY SNAPSHOT

全球碳水化合物市場,2026-2030年

全球碳水化合物市場,2026-2030年 中間相瀝青基碳纖維市場按產品形式、纖維類型、應用和最終用途產業分類-全球預測(2026-2032 年)

中間相瀝青基碳纖維市場按產品形式、纖維類型、應用和最終用途產業分類-全球預測(2026-2032 年) 碳纖維:全球市場

碳纖維:全球市場 CABKOMA市場規模、佔有率和成長分析(按類型、應用和地區分類)-2026-2033年產業預測

CABKOMA市場規模、佔有率和成長分析(按類型、應用和地區分類)-2026-2033年產業預測 碳纖維市場預測至2032年:按產品類型、原料、纖維類型、應用、最終用戶和地區分類的全球分析

碳纖維市場預測至2032年:按產品類型、原料、纖維類型、應用、最終用戶和地區分類的全球分析 碳纖維市場-全球產業規模、佔有率、趨勢、機會和預測,依原料、產品類型、纖維類型、模量、應用、最終用途產業、地區和競爭格局分類,2020-2030年預測

碳纖維市場-全球產業規模、佔有率、趨勢、機會和預測,依原料、產品類型、纖維類型、模量、應用、最終用途產業、地區和競爭格局分類,2020-2030年預測 航太複合材料碳纖維回收市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

航太複合材料碳纖維回收市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 短切碳纖維:全球市佔率及排名、總收入及需求預測(2025-2031年)熱塑性碳纖維複合材料:全球市佔率及排名、總收入及需求預測(2025-2031年)運動用品用碳纖維:全球市佔率及排名、總收入及需求預測(2025-2031年)

短切碳纖維:全球市佔率及排名、總收入及需求預測(2025-2031年)熱塑性碳纖維複合材料:全球市佔率及排名、總收入及需求預測(2025-2031年)運動用品用碳纖維:全球市佔率及排名、總收入及需求預測(2025-2031年)