|

市場調查報告書

商品編碼

1777132

全球醫用塗料市場(按塗層類型、材料、基材、應用和地區分類)- 預測至 2030 年Medical Coatings Market by Coating Type (Active, Passive), By Material (Polymers, Metals), By Application (Medical Devices, Medical Implants, Medical Equipment & Tools), By Region - Global Forecast to 2030 |

||||||

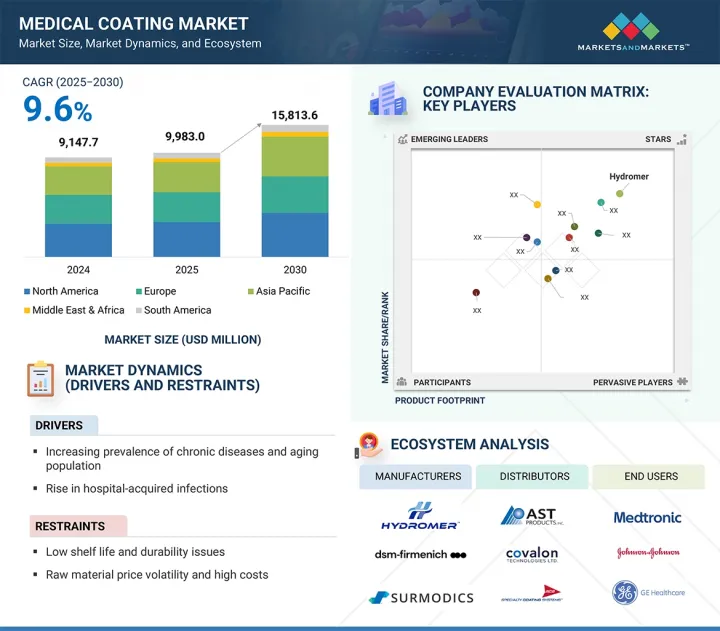

預計醫療塗料市場規模將從 2025 年的 99.83 億美元成長至 2030 年的 158.136 億美元,複合年成長率為 9.6%。

| 調查範圍 | |

|---|---|

| 調查年份 | 2022-2030 |

| 基準年 | 2024 |

| 預測期 | 2025-2030 |

| 對價單位 | 千噸,價值(百萬美元) |

| 部分 | 按塗層類型、材料、基材、應用和地區 |

| 目標區域 | 亞太地區、北美、歐洲、中東和非洲、南美 |

醫療保健領域對醫療設備日益成長的需求是醫療塗料市場成長的主要驅動力。人口老化和慢性病發病率上升推動了對植入、導管和手術器械等塗層器械的需求,這有助於推動市場成長和技術創新。

由於所有組織和醫療機構都廣泛且日益廣泛地使用塗層設備,預計醫療設備領域將成為預測期內醫用塗層市場以金額為準最大的應用領域。各種塗層醫療設備的採用主要受慢性病發病率上升、世界老齡化人口成長以及微創外科手術的進步所驅動,所有這些都需要性能增強、更安全、更易於使用的醫療設備。醫用塗層對許多醫療設備至關重要,例如導管、支架、導管導引線、整形外科植入和手術器械,並提供優異的潤滑性、生物相容性和抗菌性能。這些塗層可減少摩擦、最大限度地減少組織創傷、降低感染風險並提高器械的性能和保存期限。此外,醫院內感染的增加使得抗菌和抗血栓塗層對於病人安全和滿足嚴格的監管標準至關重要。影像系統和精密儀器等醫療技術的創新顯著增加了對高性能醫用塗層的需求,以實現更精準、更少創傷的手術效果。因此,預計未來醫療設備市場將持續成長。

在預測期內,活性塗層是醫用塗層市場價值成長最快的塗層類型,這得益於對具有不同於以金額為準塗層的專業治療能力的創新解決方案日益成長的需求,這些解決方案旨在提高患者安全性和臨床療效。被動塗層僅在使用過程中提供表面保護(例如保護和潤滑),而活性塗層則旨在在應用部位釋放藥物、抗菌劑和生物活性分子。這種輸送方法對於高風險醫療設備(例如支架、導管和整形外科植入)至關重要,因為感染、血栓形成和發炎會威脅患者的成功管理。隨著醫院內感染的增加以及慢性疾病和併發症的增多,慢性患者的感染風險更高。中性粒細胞介導的發炎和感染等術後併發症會導致風險和成本不斷上升。因此,醫院和醫療保健提供者正在尋求更有效的塗層,以降低醫院內感染的風險並促進更快的康復。

北美是醫用塗料市場規模最大、成長最快的地區,其價值成長得益於先進的醫療服務體系、日益增多的醫療程序以及對醫療設備持續發展的堅定承諾。北美,尤其是美國,擁有眾多頂級醫療設備製造商和研究機構,他們正在創新用於心血管支架、整形外科植入、導管和手術器械等應用的下一代塗料。此外,北美對醫用塗料的需求不斷成長,這與人口老化加劇、慢性病盛行率上升以及對感染控制和患者安全的日益關注有關,而這些因素都需要先進的生物相容性抗菌塗料。

本報告研究了全球醫用塗料市場,提供了塗料類型、材料、基材、應用和地區的趨勢資訊,以及參與市場的公司概況。

目錄

第1章 引言

第2章調查方法

第3章執行摘要

第4章重要考察

第5章市場概述

- 介紹

- 市場動態

第6章 產業趨勢

- 價值鏈分析

- 生態系分析

- 波特五力分析

- 主要相關人員和採購標準

- 貿易分析

- 影響客戶業務的趨勢/中斷

- 技術分析

- 總體經濟指標

- 定價分析

- 監管狀況

- 人工智慧/生成式人工智慧的影響

- 2025-2026年主要會議和活動

- 案例研究分析

- 投資金籌措場景

- 專利分析

- 2025年美國關稅的影響—概述

- 主要關稅稅率

- 價格影響分析

- 對國家的影響

- 對終端產業的影響

第7章 醫用塗料市場(依塗料類型)

- 介紹

- 積極的

- 被動的

第8章 醫用塗料市場(依材料)

- 介紹

- 聚合物

- 金屬

- 其他

第9章 醫用塗料市場(依基材)

- 介紹

- 金屬

- 陶瓷製品

- 聚合物

- 複合材料

- 玻璃

第 10 章 醫用塗料市場(按應用)

- 介紹

- 醫療設備

- 醫療植入

- 醫療設備和工具

- 防護衣

- 其他

第 11 章醫用塗料市場(按地區)

- 介紹

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他

- 中東和非洲

- 海灣合作理事會國家

- 南非

- 其他

- 南美洲

- 巴西

- 阿根廷

- 其他

第12章競爭格局

- 概述

- 主要參與企業的策略/優勢

- 收益分析

- 市場佔有率分析

- 估值和財務指標

- 品牌/產品比較分析

- 公司估值矩陣:2024 年關鍵參與企業

- 公司估值矩陣:Start-Ups/中小企業,2024 年

- 競爭場景

第13章 公司簡介

- 主要參與企業

- HYDROMER

- DSM-FIRMENICH

- SURMODICS, INC.

- BIOCOAT INCORPORATED

- AST PRODUCTS INC

- COVALON TECHNOLOGIES

- FREUDENBERG MEDICAL

- HARLAND MEDICAL SYSTEMS, INC.

- MERIT MEDICAL SYSTEMS

- APPLIED MEDICAL COATINGS

- PPG INDUSTRIES, INC

- THE SHERWIN-WILLIAMS COMPANY

- 其他公司

- FORMACOAT

- TUA SYSTEMS

- APPLIED MEMBRANE TECHNOLOGIES

- A&A COATINGS

- CALICO COATINGS

- COATINGS2GO

- CURTISS-WRIGHT CORPORATION

- ENCAPSON

- ENDURA COATINGS

- MEDICOAT AG

- MILLER-STEPHENSON CHEMICAL COMPANY, INC.

- PRECISION COATING TECHNOLOGY & MANUFACTURING INC.

- SPECIALTY COATING SYSTEMS

第14章 附錄

The medical coating market is expected to reach USD 15,813.6 million by 2030, up from USD 9,983.0 million in 2025, growing at a CAGR of 9.6%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Kilotons; Value (USD Million) |

| Segments | Coating Type, Material, Substrate, and Application |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, and South America |

The rising demand for medical devices in the healthcare sector significantly drives the growth of the medical coating market, as coatings continue to evolve and become crucial for the safety, performance, and durability of devices. An aging population and a higher prevalence of chronic diseases create a greater need for coated devices such as implants, catheters, and surgical instruments, thereby supporting market growth and fostering innovation.

"Based on application, medical devices will be the largest application in the medical coating market during the forecast period, in terms of value."

The medical devices application segment is projected to be the largest in the medical coating market by value during the forecast period due to the widespread and increasing use of coated devices across all organizations and healthcare settings. The adoption of various coated medical devices is mainly driven by the rising rates of chronic diseases, the growing aging global population, and advancements in minimally invasive surgical procedures, all of which require performance-enhanced, safer, and easier-to-use medical devices. Medical coatings are vital for many devices, including catheters, stents, guidewires, orthopedic implants, and surgical instruments, as they offer superior lubricity, biocompatibility, and antimicrobial properties. These coatings reduce friction, minimizing tissue trauma, lower infection risks, and improve device performance and shelf-life. Additionally, the rise in hospital-acquired infections has made antimicrobial and anti-thrombogenic coatings essential for patient safety and meeting strict regulatory standards. Innovations in medical technology, such as imaging systems and precision instruments, have significantly increased the demand for high-performance medical coatings to achieve more accurate and less traumatic surgical outcomes. Therefore, the medical devices segment is expected to continue its growth.

"Based on coating type, active coating will be the fastest in the medical coating market during the forecast period, in terms of value."

Active coatings are the fastest-growing type of coating by value in the medical coating market during the forecast period, due to their specialized therapeutic capabilities compared to passive coatings and the increasing demand for innovative solutions to improve patient safety and clinical outcomes. While passive coatings only provide surface protection during use (such as protection and lubrication), active coatings are engineered to release drugs, antimicrobial agents, or bioactive molecules at the application site. This delivery method is essential for high-risk medical devices (like stents, catheters, and orthopedic implants) where infection, thrombosis, and inflammation threaten successful patient management. The rise in hospital-acquired infections and the worldwide increase in chronic diseases and comorbidities expose chronic patients to higher infection risks, as post-surgical complications-such as PMN-mediated inflammation and infections-lead to extended risks and costs. Therefore, hospitals and healthcare providers are seeking more effective coatings that reduce the risk of hospital-acquired infections and promote faster recovery.

"Based on region, North America accounts for the largest share in the medical coating market, in terms of value."

North America is the largest and fastest-growing region in the medical coating market, with value growth driven by advanced healthcare delivery systems, an increase in procedures performed, and a strong commitment to the continuous development of medical devices. North America, especially the United States, hosts many top medical device manufacturers and research institutions that are innovating the next generation of coatings for applications such as cardiovascular stents, orthopedic implants, catheters, and surgical instruments. Additionally, the rising demand for medical coatings in North America is linked to a growing and aging population with increasing rates of chronic diseases, as well as a heightened focus on infection control and patient safety, which demand sophisticated, biocompatible, and antimicrobial coatings.

During the process of determining and verifying the market size for various segments and subsegments identified through secondary research, extensive primary interviews were conducted. A breakdown of the profiles of the primary interviewees is as follows:

- By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation: Directors- 35%, Managers - 25%, and Others - 40%

- By Region: North America - 22%, Europe - 22%, Asia Pacific - 45%, RoW - 11%

The key players in this market are Hydromer (US), DSM-Firmenich (Netherlands), Surmodics (US), Biocoat Incorporated (US), AST Products Inc (US), Covalon Technologies (Canada), Freudenberg Medical (US), Harland Medical Systems, Inc (US), Merit Medical Systems (US), Applied Medical Coatings (US), PPG Industries, Inc. (US) and The Sherwin-Williams Company (US).

Research Coverage

This report breaks down the medical coating market by coating type, material, substrate, application, and region, and provides estimates for the total market value across different regions. A thorough analysis of major industry players has been carried out to offer insights into their business overviews, products and services, key strategies, new product launches, expansions, and mergers and acquisitions related to the medical coating market.

Key benefits of buying this report

This research report covers different levels of analysis, including industry examination (industry trends), market ranking analysis of leading players, and company profiles. Together, these provide a comprehensive view of the competitive landscape, emerging and high-growth segments of the medical coating market, high-growth regions, and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following:

- Analysis of key drivers (increasing demand for minimally invasive surgical procedures, growing geriatric population and prevalence of chronic diseases), restraints (stringent regulatory requirements, high costs and technical challenges), opportunities (development of smart and multifunctional coatings, expansion in emerging markets) and challenges (technical limitations in coating durability and adhesion, intellectual property and supply chain issues).

- Market Penetration: Comprehensive information on the medical coating market offered by top players in the global medical coating market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the medical coating market

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for medical coating market across regions

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global medical coating market

- Competitive Assessment: In-depth assessment of market share, strategies, products, and manufacturing capabilities of leading players in the medical coating market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS OF STUDY

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 List of primary interview participants-demand and supply sides

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of interviews with experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 FORECAST NUMBER CALCULATION

- 2.4 DATA TRIANGULATION

- 2.5 FACTOR ANALYSIS

- 2.6 ASSUMPTIONS

- 2.7 LIMITATIONS & RISKS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MEDICAL COATING MARKET

- 4.2 MEDICAL COATING MARKET, BY COATING TYPE

- 4.3 MEDICAL COATING MARKET, BY MATERIAL

- 4.4 MEDICAL COATING MARKET, BY SUBSTRATE

- 4.5 MEDICAL COATING MARKET, BY APPLICATION

- 4.6 MEDICAL COATING MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing prevalence of chronic diseases and aging population

- 5.2.1.2 Rise in hospital-acquired infections

- 5.2.1.3 Growth in minimally invasive surgeries and medical device usage

- 5.2.2 RESTRAINTS

- 5.2.2.1 Low shelf life and durability issues

- 5.2.2.2 Raw material price volatility and high costs

- 5.2.2.3 Strict government regulations and compliance challenges

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rise in demand for antimicrobial and drug-eluting coatings

- 5.2.3.2 Technological advancements and nanotechnology

- 5.2.4 CHALLENGES

- 5.2.4.1 Biocompatibility and durability concerns

- 5.2.4.2 Complex application and quality control

- 5.2.1 DRIVERS

6 INDUSTRY TRENDS

- 6.1 VALUE CHAIN ANALYSIS

- 6.1.1 RAW MATERIAL SUPPLIERS

- 6.1.2 MANUFACTURERS

- 6.1.3 DISTRIBUTORS

- 6.1.4 END USERS

- 6.2 ECOSYSTEM ANALYSIS

- 6.3 PORTER'S FIVE FORCES ANALYSIS

- 6.3.1 THREAT OF NEW ENTRANTS

- 6.3.2 THREAT OF SUBSTITUTES

- 6.3.3 BARGAINING POWER OF SUPPLIERS

- 6.3.4 BARGAINING POWER OF BUYERS

- 6.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.4 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.4.2 QUALITY

- 6.4.3 SERVICE

- 6.4.4 BUYING CRITERIA

- 6.5 TRADE ANALYSIS

- 6.5.1 EXPORT SCENARIO (HS CODE 9018)

- 6.5.2 IMPORT SCENARIO (HS CODE 9018)

- 6.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.7 TECHNOLOGY ANALYSIS

- 6.7.1 KEY TECHNOLOGIES

- 6.7.1.1 Plasma spraying

- 6.7.1.2 Chemical vapor deposition

- 6.7.1.3 Microblasting & laser treatments

- 6.7.2 COMPLEMENTARY TECHNOLOGIES

- 6.7.2.1 Nanotechnology integration

- 6.7.2.2 Advanced material formulation

- 6.7.1 KEY TECHNOLOGIES

- 6.8 MACROECONOMIC INDICATORS

- 6.8.1 GDP TRENDS AND FORECASTS

- 6.9 PRICING ANALYSIS

- 6.9.1 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024

- 6.9.2 AVERAGE SELLING PRICE TREND, BY COATING TYPE, 2022-2024

- 6.10 REGULATORY LANDSCAPE

- 6.10.1 NORTH AMERICA

- 6.10.2 ASIA PACIFIC

- 6.10.3 EUROPE

- 6.10.4 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.11 IMPACT OF AI/GEN AI

- 6.12 KEY CONFERENCES AND EVENTS, 2025-2026

- 6.13 CASE STUDY ANALYSIS

- 6.13.1 ANTIMICROBIAL COATING FOR IMPLANTABLE PACEMAKER DEVICE

- 6.13.2 INTRICOAT FOR MEDICAL ROBOTICS PROJECT

- 6.13.3 SLIPS COATING TO PREVENT BIOFILM FORMATION ON MEDICAL IMPLANTS

- 6.14 INVESTMENT AND FUNDING SCENARIO

- 6.15 PATENT ANALYSIS

- 6.15.1 INTRODUCTION

- 6.15.2 LEGAL STATUS OF PATENTS

- 6.15.3 JURISDICTION ANALYSIS

- 6.16 IMPACT OF 2025 US TARIFF - OVERVIEW

- 6.16.1 INTRODUCTION

- 6.17 KEY TARIFF RATES

- 6.18 PRICE IMPACT ANALYSIS

- 6.19 IMPACT ON COUNTRY/REGION

- 6.19.1 US

- 6.19.2 EUROPE

- 6.19.3 ASIA PACIFIC

- 6.20 IMPACT ON END-USE INDUSTRIES

7 MEDICAL COATINGS MARKET, BY COATING TYPE

- 7.1 INTRODUCTION

- 7.2 ACTIVE

- 7.2.1 ANTIMICROBIAL

- 7.2.1.1 Used to prevent microbial infection on medical devices

- 7.2.2 OTHERS

- 7.2.1 ANTIMICROBIAL

- 7.3 PASSIVE

- 7.3.1 HYDROPHILIC/LUBRICIOUS HYDROPHILIC

- 7.3.1.1 Growing awareness of minimally invasive surgical techniques to boost demand

- 7.3.2 HYDROPHOBIC

- 7.3.2.1 High water resistance to drive market growth

- 7.3.1 HYDROPHILIC/LUBRICIOUS HYDROPHILIC

8 MEDICAL COATINGS MARKET, BY MATERIAL TYPE

- 8.1 INTRODUCTION

- 8.2 POLYMERS

- 8.2.1 FLUOROPOLYMERS

- 8.2.1.1 PTFE

- 8.2.1.1.1 Minimal friction and strong resistance to heat and chemicals to boost adoption

- 8.2.1.2 PVDF

- 8.2.1.2.1 Exceptionally robust and resistant to chemicals

- 8.2.1.3 Others

- 8.2.1.1 PTFE

- 8.2.2 PARYLENE

- 8.2.2.1 Frictional coefficient comparable to PTFE - key segment driver

- 8.2.3 SILICONES

- 8.2.3.1 Biocompatibility fuels widespread adoption in medical applications

- 8.2.4 OTHERS

- 8.2.1 FLUOROPOLYMERS

- 8.3 METALS

- 8.3.1 SILVER

- 8.3.1.1 Antimicrobial properties boost application

- 8.3.2 TITANIUM

- 8.3.2.1 Commonly employed in implant applications due to excellent biocompatibility

- 8.3.3 OTHERS

- 8.3.1 SILVER

- 8.4 OTHERS

9 MEDICAL COATINGS MARKET, BY SUBSTRATE

- 9.1 INTRODUCTION

- 9.2 METALS

- 9.2.1 METALS IN IMPLANTED MEDICAL DEVICES: DRIVING BIOCOMPATIBILITY AND MARKET GROWTH

- 9.3 CERAMICS

- 9.3.1 WIDELY USED IN DENTAL IMPLANT APPLICATIONS

- 9.4 POLYMERS

- 9.4.1 FLUOROPOLYMERS

- 9.4.1.1 PTFE's unparalleled lubricity boosts advanced medical device performance

- 9.4.2 SILICONE

- 9.4.2.1 Superior compatibility with human tissue and bodily fluids

- 9.4.3 OTHER POLYMERS

- 9.4.1 FLUOROPOLYMERS

- 9.5 COMPOSITES

- 9.5.1 LIGHT WEIGHT PROPERTY ENHANCES PROSTHETIC MOBILITY

- 9.6 GLASS

- 9.6.1 OFFERS BIOCOMPATIBILITY FOR SAFE AND DURABLE MEDICAL IMPLANTS

10 MEDICAL COATINGS MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 MEDICAL DEVICES

- 10.2.1 INCREASING DEMAND FOR MINIMALLY INVASIVE SURGICAL PROCEDURES TO BOOST MARKET

- 10.3 MEDICAL IMPLANTS

- 10.3.1 ORTHOPEDIC IMPLANTS

- 10.3.1.1 Lubricity and fatigue strength in orthopedic implants

- 10.3.2 DENTAL IMPLANTS

- 10.3.2.1 Use of hydroxyapatite in dental implants to stimulate bone healing

- 10.3.3 CARDIOVASCULAR IMPLANTS

- 10.3.3.1 Nanomaterial coatings used for stents

- 10.3.1 ORTHOPEDIC IMPLANTS

- 10.4 MEDICAL EQUIPMENT & TOOLS

- 10.4.1 SURGICAL EQUIPMENT & TOOLS

- 10.4.1.1 Antimicrobial and other functional properties benefit surgical tools

- 10.4.2 INSTITUTIONAL EQUIPMENT

- 10.4.2.1 Hydrophobic coatings - widely used in institutional equipment

- 10.4.1 SURGICAL EQUIPMENT & TOOLS

- 10.5 PROTECTIVE CLOTHING

- 10.5.1 HELPS ENHANCE HEALTHCARE SAFETY

- 10.6 OTHERS

11 MEDICAL COATING MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Ongoing advancements in medical technology to propel market

- 11.2.2 CANADA

- 11.2.2.1 Rising investments to boost demand for medical coatings

- 11.2.3 MEXICO

- 11.2.3.1 Rising domestic production to drive market

- 11.2.1 US

- 11.3 ASIA PACIFIC

- 11.3.1 CHINA

- 11.3.1.1 World's third-largest market for medical device production

- 11.3.2 JAPAN

- 11.3.2.1 Rising percentage of geriatric population to drive market

- 11.3.3 INDIA

- 11.3.3.1 Government initiatives to fuel demand for medical coatings

- 11.3.4 SOUTH KOREA

- 11.3.4.1 Continuous R&D activities to fuel market

- 11.3.5 AUSTRALIA

- 11.3.5.1 Rising incidence of chronic diseases drive innovation in market

- 11.3.6 REST OF ASIA PACIFIC

- 11.3.1 CHINA

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Innovations in medical technology to drive market

- 11.4.2 UK

- 11.4.2.1 Government initiatives for collaborative developments in medical technology to drive market

- 11.4.3 FRANCE

- 11.4.3.1 Well-established medical device manufacturing industry to boost market

- 11.4.4 ITALY

- 11.4.4.1 Prevalence of chronic diseases to fuel market growth

- 11.4.5 SPAIN

- 11.4.5.1 High demand for implants and catheters to boost market

- 11.4.6 RUSSIA

- 11.4.6.1 Rising demand for minimally invasive procedures to spur market

- 11.4.7 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Government initiatives for healthcare industry to drive market

- 11.5.1.2 UAE

- 11.5.1.2.1 Medical tourism to drive market

- 11.5.1.3 Other GCC countries

- 11.5.1.1 Saudi Arabia

- 11.5.2 SOUTH AFRICA

- 11.5.2.1 Global investments to propel market

- 11.5.3 REST OF MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Market enhanced through local device production

- 11.6.2 ARGENTINA

- 11.6.2.1 Rising prevalence of non-communicable disease to boost market

- 11.6.3 REST OF SOUTH AMERICA

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6 BRAND/PRODUCT COMPARISON ANALYSIS

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Coating type footprint

- 12.7.5.4 Material footprint

- 12.7.5.5 Substrate footprint

- 12.7.5.6 Application footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 EXPANSIONS

- 12.9.3 DEALS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 HYDROMER

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 DSM-FIRMENICH

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Deals

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 SURMODICS, INC.

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 BIOCOAT INCORPORATED

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Deals

- 13.1.4.4 Expansions

- 13.1.4.4.1 Product launches

- 13.1.4.5 MnM view

- 13.1.4.5.1 Key strengths

- 13.1.4.5.2 Strategic choices

- 13.1.4.5.3 Weaknesses and competitive threats

- 13.1.5 AST PRODUCTS INC

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Key strengths

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses and competitive threats

- 13.1.6 COVALON TECHNOLOGIES

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 MnM view

- 13.1.6.3.1 Key strengths

- 13.1.6.3.2 Strategic choices

- 13.1.6.3.3 Weaknesses and competitive threats

- 13.1.7 FREUDENBERG MEDICAL

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Expansions

- 13.1.7.4 MnM view

- 13.1.7.4.1 Key strengths

- 13.1.7.4.2 Strategic choices

- 13.1.7.4.3 Weaknesses and competitive threats

- 13.1.8 HARLAND MEDICAL SYSTEMS, INC.

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Expansions

- 13.1.8.4 MnM view

- 13.1.8.4.1 Key strengths

- 13.1.8.4.2 Strategic choices

- 13.1.8.4.3 Weaknesses and competitive threats

- 13.1.9 MERIT MEDICAL SYSTEMS

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 MnM view

- 13.1.10 APPLIED MEDICAL COATINGS

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 MnM view

- 13.1.11 PPG INDUSTRIES, INC

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Solutions/Services offered

- 13.1.11.3 MnM view

- 13.1.11.3.1 Key strengths

- 13.1.11.3.2 Strategic choices

- 13.1.11.3.3 Weaknesses and competitive threats

- 13.1.12 THE SHERWIN-WILLIAMS COMPANY

- 13.1.12.1 Business overview

- 13.1.12.2 Products/Solutions/Services offered

- 13.1.12.3 MnM view

- 13.1.12.3.1 Key strengths

- 13.1.12.3.2 Strategic choices

- 13.1.12.3.3 Weaknesses and competitive threats

- 13.1.1 HYDROMER

- 13.2 OTHER PLAYERS

- 13.2.1 FORMACOAT

- 13.2.2 TUA SYSTEMS

- 13.2.3 APPLIED MEMBRANE TECHNOLOGIES

- 13.2.4 A&A COATINGS

- 13.2.5 CALICO COATINGS

- 13.2.6 COATINGS2GO

- 13.2.7 CURTISS-WRIGHT CORPORATION

- 13.2.8 ENCAPSON

- 13.2.9 ENDURA COATINGS

- 13.2.10 MEDICOAT AG

- 13.2.11 MILLER-STEPHENSON CHEMICAL COMPANY, INC.

- 13.2.12 PRECISION COATING TECHNOLOGY & MANUFACTURING INC.

- 13.2.13 SPECIALTY COATING SYSTEMS

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 RELATED REPORTS

- 14.4 AUTHOR DETAILS

List of Tables

- TABLE 1 LIST OF KEY SECONDARY SOURCES

- TABLE 2 MEDICAL COATING MARKET: ROLE OF PLAYERS IN ECOSYSTEM

- TABLE 3 MEDICAL COATING MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

- TABLE 5 KEY BUYING CRITERIA FOR TOP APPLICATIONS

- TABLE 6 EXPORT SCENARIO FOR HS CODE 9018-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 7 IMPORT SCENARIO FOR HS CODE 9018-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 8 PROJECTED REAL GDP GROWTH (ANNUAL PERCENTAGE CHANGE) OF KEY COUNTRIES, 2019-2023

- TABLE 9 ANNUAL GDP PERCENTAGE CHANGE AND PROJECTION OF KEY COUNTRIES, 2024-2029

- TABLE 10 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 MEDICAL COATING MARKET: KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 14 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 15 MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (USD MILLION)

- TABLE 16 MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (USD MILLION)

- TABLE 17 MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (KILOTONS)

- TABLE 18 MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (KILOTONS)

- TABLE 19 MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (USD MILLION)

- TABLE 20 MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 21 MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (KILOTONS)

- TABLE 22 MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (KILOTONS)

- TABLE 23 MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (USD MILLION)

- TABLE 24 MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (USD MILLION)

- TABLE 25 MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (KILOTONS)

- TABLE 26 MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (KILOTONS)

- TABLE 27 MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 28 MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 29 MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 30 MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 31 MEDICAL COATING MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 32 MEDICAL COATING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 33 MEDICAL COATING MARKET, BY REGION, 2022-2024 (KILOTONS)

- TABLE 34 MEDICAL COATING MARKET, BY REGION, 2025-2030 (KILOTONS)

- TABLE 35 NORTH AMERICA: MEDICAL COATING MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 36 NORTH AMERICA: MEDICAL COATING MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 37 NORTH AMERICA: MEDICAL COATING MARKET, BY COUNTRY, 2022-2024 (KILOTONS)

- TABLE 38 NORTH AMERICA: MEDICAL COATING MARKET, BY COUNTRY, 2025-2030 (KILOTONS)

- TABLE 39 NORTH AMERICA: MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (USD MILLION)

- TABLE 40 NORTH AMERICA: MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (USD MILLION)

- TABLE 41 NORTH AMERICA: MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (KILOTONS)

- TABLE 42 NORTH AMERICA: MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (KILOTONS)

- TABLE 43 NORTH AMERICA: MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (USD MILLION)

- TABLE 44 NORTH AMERICA: MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 45 NORTH AMERICA: MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (KILOTONS)

- TABLE 46 NORTH AMERICA: MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (KILOTONS)

- TABLE 47 NORTH AMERICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (USD MILLION)

- TABLE 48 NORTH AMERICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (USD MILLION)

- TABLE 49 NORTH AMERICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (KILOTONS)

- TABLE 50 NORTH AMERICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (KILOTONS)

- TABLE 51 NORTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 52 NORTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 53 NORTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 54 NORTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 55 US: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 56 US: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 57 US: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 58 US: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 59 CANADA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 60 CANADA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 61 CANADA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 62 CANADA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 63 MEXICO: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 64 MEXICO: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 65 MEXICO: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 66 MEXICO: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 67 ASIA PACIFIC: MEDICAL COATING MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 68 ASIA PACIFIC: MEDICAL COATING MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 69 ASIA PACIFIC: MEDICAL COATING MARKET, BY COUNTRY, 2022-2024 (KILOTONS)

- TABLE 70 ASIA PACIFIC: MEDICAL COATING MARKET, BY COUNTRY, 2025-2030 (KILOTONS)

- TABLE 71 ASIA PACIFIC: MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (USD MILLION)

- TABLE 72 ASIA PACIFIC: MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (USD MILLION)

- TABLE 73 ASIA PACIFIC: MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (KILOTONS)

- TABLE 74 ASIA PACIFIC: MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (KILOTONS)

- TABLE 75 ASIA PACIFIC: MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (USD MILLION)

- TABLE 76 ASIA PACIFIC: MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 77 ASIA PACIFIC: MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (KILOTONS)

- TABLE 78 ASIA PACIFIC: MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (KILOTONS)

- TABLE 79 ASIA PACIFIC: MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (USD MILLION)

- TABLE 80 ASIA PACIFIC: MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (USD MILLION)

- TABLE 81 ASIA PACIFIC: MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (KILOTONS)

- TABLE 82 ASIA PACIFIC: MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (KILOTONS)

- TABLE 83 ASIA PACIFIC: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 84 ASIA PACIFIC: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 85 ASIA PACIFIC: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 86 ASIA PACIFIC: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 87 CHINA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 88 CHINA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 89 CHINA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 90 CHINA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 91 JAPAN: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 92 JAPAN: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 93 JAPAN: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 94 JAPAN: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 95 INDIA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 96 INDIA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 97 INDIA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 98 INDIA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 99 SOUTH KOREA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 100 SOUTH KOREA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 101 SOUTH KOREA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 102 SOUTH KOREA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 103 AUSTRALIA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 104 AUSTRALIA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 105 AUSTRALIA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 106 AUSTRALIA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 107 REST OF ASIA PACIFIC: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 108 REST OF ASIA PACIFIC: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 109 REST OF ASIA PACIFIC: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 110 REST OF ASIA PACIFIC: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 111 EUROPE: MEDICAL COATING MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 112 EUROPE: MEDICAL COATING MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 113 EUROPE: MEDICAL COATING MARKET, BY COUNTRY, 2022-2024 (KILOTONS)

- TABLE 114 EUROPE: MEDICAL COATING MARKET, BY COUNTRY, 2025-2030 (KILOTONS)

- TABLE 115 EUROPE: MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (USD MILLION)

- TABLE 116 EUROPE: MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (USD MILLION)

- TABLE 117 EUROPE: MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (KILOTONS)

- TABLE 118 EUROPE: MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (KILOTONS)

- TABLE 119 EUROPE: MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (USD MILLION)

- TABLE 120 EUROPE: MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 121 EUROPE: MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (KILOTONS)

- TABLE 122 EUROPE: MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (KILOTONS)

- TABLE 123 EUROPE: MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (USD MILLION)

- TABLE 124 EUROPE: MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (USD MILLION)

- TABLE 125 EUROPE: MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (KILOTONS)

- TABLE 126 EUROPE: MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (KILOTONS)

- TABLE 127 EUROPE: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 128 EUROPE: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 129 EUROPE: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 130 EUROPE: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 131 GERMANY: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 132 GERMANY: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 133 GERMANY: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 134 GERMANY: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 135 UK: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 136 UK: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 137 UK: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 138 UK: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 139 FRANCE: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 140 FRANCE: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 141 FRANCE: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 142 FRANCE: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 143 ITALY: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 144 ITALY: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 145 ITALY: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 146 ITALY: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 147 SPAIN: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 148 SPAIN: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 149 SPAIN: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 150 SPAIN: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 151 RUSSIA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 152 RUSSIA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 153 RUSSIA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 154 RUSSIA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 155 REST OF EUROPE: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 156 REST OF EUROPE: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 157 REST OF EUROPE: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 158 REST OF EUROPE: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 159 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 160 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 161 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY COUNTRY, 2022-2024 (KILOTONS)

- TABLE 162 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY COUNTRY, 2025-2030 (KILOTONS)

- TABLE 163 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (USD MILLION)

- TABLE 164 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (USD MILLION)

- TABLE 165 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (KILOTONS)

- TABLE 166 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (KILOTONS)

- TABLE 167 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (USD MILLION)

- TABLE 168 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 169 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (KILOTONS)

- TABLE 170 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (KILOTONS)

- TABLE 171 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (USD MILLION)

- TABLE 172 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (USD MILLION)

- TABLE 173 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (KILOTONS)

- TABLE 174 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (KILOTONS)

- TABLE 175 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 176 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 177 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 178 MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 179 SAUDI ARABIA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 180 SAUDI ARABIA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 181 SAUDI ARABIA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 182 SAUDI ARABIA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 183 UAE: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 184 UAE: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 185 UAE: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 186 UAE: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 187 OTHER GCC COUNTRIES: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 188 OTHER GCC COUNTRIES: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 189 OTHER GCC COUNTRIES: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 190 OTHER GCC COUNTRIES: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 191 SOUTH AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 192 SOUTH AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 193 SOUTH AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 194 SOUTH AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 195 REST OF MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 196 REST OF MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 197 REST OF MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 198 REST OF MIDDLE EAST & AFRICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 199 SOUTH AMERICA: MEDICAL COATING MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 200 SOUTH AMERICA: MEDICAL COATING MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 201 SOUTH AMERICA: MEDICAL COATING MARKET, BY COUNTRY, 2022-2024 (KILOTONS)

- TABLE 202 SOUTH AMERICA: MEDICAL COATING MARKET, BY COUNTRY, 2025-2030 (KILOTONS)

- TABLE 203 SOUTH AMERICA: MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (USD MILLION)

- TABLE 204 SOUTH AMERICA: MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (USD MILLION)

- TABLE 205 SOUTH AMERICA: MEDICAL COATING MARKET, BY COATING TYPE, 2022-2024 (KILOTONS)

- TABLE 206 SOUTH AMERICA: MEDICAL COATING MARKET, BY COATING TYPE, 2025-2030 (KILOTONS)

- TABLE 207 SOUTH AMERICA: MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (USD MILLION)

- TABLE 208 SOUTH AMERICA: MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 209 SOUTH AMERICA: MEDICAL COATING MARKET, BY MATERIAL, 2022-2024 (KILOTONS)

- TABLE 210 SOUTH AMERICA: MEDICAL COATING MARKET, BY MATERIAL, 2025-2030 (KILOTONS)

- TABLE 211 SOUTH AMERICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (USD MILLION)

- TABLE 212 SOUTH AMERICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (USD MILLION)

- TABLE 213 SOUTH AMERICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2022-2024 (KILOTONS)

- TABLE 214 SOUTH AMERICA: MEDICAL COATING MARKET, BY SUBSTRATE, 2025-2030 (KILOTONS)

- TABLE 215 SOUTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 216 SOUTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 217 SOUTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 218 SOUTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 219 BRAZIL: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 220 BRAZIL: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 221 BRAZIL: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 222 BRAZIL: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 223 ARGENTINA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 224 ARGENTINA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 225 ARGENTINA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 226 ARGENTINA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 227 REST OF SOUTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 228 REST OF SOUTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 229 REST OF SOUTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2022-2024 (KILOTONS)

- TABLE 230 REST OF SOUTH AMERICA: MEDICAL COATING MARKET, BY APPLICATION, 2025-2030 (KILOTONS)

- TABLE 231 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN MEDICAL COATING MARKET BETWEEN JANUARY 2020 AND MAY 2025

- TABLE 232 MEDICAL COATING MARKET: DEGREE OF COMPETITION

- TABLE 233 MEDICAL COATING MARKET: REGION FOOTPRINT

- TABLE 234 MEDICAL COATING MARKET: COATING TYPE FOOTPRINT

- TABLE 235 MEDICAL COATING MARKET: MATERIAL FOOTPRINT

- TABLE 236 MEDICAL COATING MARKET: SUBSTRATE FOOTPRINT

- TABLE 237 MEDICAL COATING MARKET: APPLICATION FOOTPRINT

- TABLE 238 MEDICAL COATING MARKET: KEY STARTUPS/SMES

- TABLE 239 MEDICAL COATING MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/ SMES (1/2)

- TABLE 240 MEDICAL COATING MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/ SMES (2/2)

- TABLE 241 MEDICAL COATING MARKET: PRODUCT LAUNCHES, JANUARY 2020-MAY 2025

- TABLE 242 MEDICAL COATING MARKET: EXPANSIONS, JANUARY 2020-MAY 2025

- TABLE 243 MEDICAL COATING MARKET: DEALS, JANUARY 2020-MAY 2025

- TABLE 244 HYDROMER: COMPANY OVERVIEW

- TABLE 245 HYDROMER: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 246 HYDROMER: PRODUCT LAUNCHES, JANUARY 2020-MAY 2025

- TABLE 247 DSM-FIRMENICH: COMPANY OVERVIEW

- TABLE 248 DSM-FIRMENICH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 249 DSM-FIRMENICH: DEALS, JANUARY 2020-MAY 2025

- TABLE 250 SURMODICS, INC.: COMPANY OVERVIEW

- TABLE 251 SURMODICS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 252 SURMODICS, INC.: PRODUCT LAUNCHES, JANUARY 2020-MAY 2025

- TABLE 253 BIOCOAT INCORPORATED: COMPANY OVERVIEW

- TABLE 254 BIOCOAT INCORPORATED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 255 BIOCOAT INCORPORATED: DEALS, JANUARY 2020-MAY 2025

- TABLE 256 BIOCOAT INCORPORATED: EXPANSIONS, JANUARY 2020-MAY 2025

- TABLE 257 BIOCOAT INCORPORATED: PRODUCT LAUNCHES, JANUARY 2020-MAY 2025

- TABLE 258 AST PRODUCTS INC: COMPANY OVERVIEW

- TABLE 259 AST PRODUCTS INC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 260 COVALON TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 261 COVALON TECHNOLOGIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 262 FREUDENBERG MEDICAL: COMPANY OVERVIEW

- TABLE 263 FREUDENBERG MEDICAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 264 FREUDENBERG MEDICAL: EXPANSIONS, JANUARY 2020-MAY 2025

- TABLE 265 HARLAND MEDICAL SYSTEMS, INC: COMPANY OVERVIEW

- TABLE 266 HARLAND MEDICAL SYSTEMS, INC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 267 HARLAND MEDICAL SYSTEMS, INC: EXPANSIONS, JANUARY 2020-MAY 2025

- TABLE 268 MERIT MEDICAL SYSTEMS: COMPANY OVERVIEW

- TABLE 269 MERIT MEDICAL SYSTEMS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 270 APPLIED MEDICAL COATINGS: COMPANY OVERVIEW

- TABLE 271 APPLIED MEDICAL COATINGS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 272 PPG INDUSTRIES, INC: COMPANY OVERVIEW

- TABLE 273 PPG INDUSTRIES, INC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 274 THE SHERWIN-WILLIAMS COMPANY: COMPANY OVERVIEW

- TABLE 275 THE SHERWIN-WILLIAMS COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 276 FORMACOAT: COMPANY OVERVIEW

- TABLE 277 TUA SYSTEMS: COMPANY OVERVIEW

- TABLE 278 APPLIED MEMBRANE TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 279 A&A COATINGS: COMPANY OVERVIEW

- TABLE 280 CALICO COATINGS: COMPANY OVERVIEW

- TABLE 281 COATINGS2GO: COMPANY OVERVIEW

- TABLE 282 CURTISS-WRIGHT CORPORATION: COMPANY OVERVIEW

- TABLE 283 ENCAPSON: COMPANY OVERVIEW

- TABLE 284 ENDURA COATINGS: COMPANY OVERVIEW

- TABLE 285 MEDICOAT AG: COMPANY OVERVIEW

- TABLE 286 MILLER-STEPHENSON CHEMICAL COMPANY, INC.: COMPANY OVERVIEW

- TABLE 287 PRECISION COATING TECHNOLOGY & MANUFACTURING INC.: COMPANY OVERVIEW

- TABLE 288 SPECIALTY COATING SYSTEMS: COMPANY OVERVIEW

List of Figures

- FIGURE 1 MEDICAL COATING MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 YEARS CONSIDERED

- FIGURE 3 MEDICAL COATING MARKET: RESEARCH DESIGN

- FIGURE 4 MEDICAL COATING MARKET: BOTTOM-UP APPROACH

- FIGURE 5 MEDICAL COATING MARKET: TOP-DOWN APPROACH

- FIGURE 6 MARKET SIZE ESTIMATION: MEDICAL COATING MARKET TOP-DOWN APPROACH

- FIGURE 7 DEMAND-SIDE FORECAST PROJECTIONS

- FIGURE 8 MEDICAL COATING MARKET: DATA TRIANGULATION

- FIGURE 9 PASSIVE COATINGS TO DOMINATE MARKET

- FIGURE 10 POLYMERS TO LEAD MARKET AMONG MATERIALS DURING FORECAST PERIOD

- FIGURE 11 MEDICAL DEVICES TO HAVE HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 12 NORTH AMERICA WAS LARGEST MARKET IN 2024

- FIGURE 13 GROWING DEMAND FROM MEDICAL DEVICES TO DRIVE MARKET

- FIGURE 14 ACTIVE COATING SEGMENT TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 15 POLYMERS SEGMENT TO LEAD MARKET BY VOLUME

- FIGURE 16 POLYMERS TO BE LARGEST SUBSTRATE SEGMENT FOR MEDICAL COATINGS

- FIGURE 17 MEDICAL DEVICES - DOMINANT APPLICATION FOR MEDICAL COATINGS

- FIGURE 18 CHINA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 19 MEDICAL COATING MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 20 MEDICAL COATING MARKET: VALUE CHAIN ANALYSIS

- FIGURE 21 MEDICAL COATING MARKET: ECOSYSTEM

- FIGURE 22 MEDICAL COATING MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 23 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

- FIGURE 24 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- FIGURE 25 EXPORT DATA FOR HS CODE 9018-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- FIGURE 26 IMPORT DATA FOR HS CODE 9018-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- FIGURE 27 MEDICAL COATING MARKET: TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 28 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024 (USD/KG)

- FIGURE 29 AVERAGE SELLING PRICE TREND, BY COATING TYPE, 2022-2024 (USD/KG)

- FIGURE 30 INVESTMENT AND FUNDING SCENARIO, 2021-2024 (USD MILLION)

- FIGURE 31 PATENTS APPLIED AND GRANTED, 2014-2024

- FIGURE 32 LEGAL STATUS OF PATENTS (2014-2024)

- FIGURE 33 MEDICAL COATING PATENTS: TOP JURISDICTIONS

- FIGURE 34 PASSIVE COATINGS TO ACCOUNT FOR LARGER MARKET SHARE

- FIGURE 35 POLYMERS TO ACCOUNT FOR LARGEST MARKET SHARE

- FIGURE 36 METAL SUBSTRATES TO GROW FASTEST DURING FORECAST PERIOD

- FIGURE 37 MEDICAL DEVICES SEGMENT TO DOMINATE MARKET

- FIGURE 38 CHINA TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- FIGURE 39 NORTH AMERICA: MEDICAL COATING MARKET SNAPSHOT

- FIGURE 40 ASIA PACIFIC: MEDICAL COATING MARKET SNAPSHOT

- FIGURE 41 EUROPE: MEDICAL COATING MARKET SNAPSHOT

- FIGURE 42 REVENUE ANALYSIS OF TOP PLAYERS IN MEDICAL COATING MARKET, 2022-2024

- FIGURE 43 MEDICAL COATING MARKET SHARE ANALYSIS, 2024

- FIGURE 44 VALUATION OF LEADING COMPANIES IN MEDICAL COATING MARKET, 2024

- FIGURE 45 FINANCIAL METRICS OF LEADING COMPANIES IN MEDICAL COATING MARKET, 2024

- FIGURE 46 MEDICAL COATING MARKET: BRAND/PRODUCT COMPARISON ANALYSIS

- FIGURE 47 MEDICAL COATING MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 48 MEDICAL COATING MARKET: COMPANY FOOTPRINT

- FIGURE 49 MEDICAL COATING MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 50 DSM-FIRMENICH: COMPANY SNAPSHOT

- FIGURE 51 SURMODICS, INC.: COMPANY SNAPSHOT

- FIGURE 52 COVALON TECHNOLOGIES: COMPANY SNAPSHOT

- FIGURE 53 FREUDENBERG MEDICAL: COMPANY SNAPSHOT

- FIGURE 54 MERIT MEDICAL SYSTEMS: COMPANY SNAPSHOT

- FIGURE 55 PPG INDUSTRIES: COMPANY SNAPSHOT

- FIGURE 56 THE SHERWIN-WILLIAMS COMPANY: COMPANY SNAPSHOT

血液相容性塗層市場規模、佔有率和成長分析:按塗層類型、材料類型、應用領域、最終用戶和地區分類-2026-2033年產業預測

血液相容性塗層市場規模、佔有率和成長分析:按塗層類型、材料類型、應用領域、最終用戶和地區分類-2026-2033年產業預測 2026年全球抗菌整形外科植入市場報告2026年全球醫療設備塗層市場報告

2026年全球抗菌整形外科植入市場報告2026年全球醫療設備塗層市場報告 醫療設備抗菌塗層市場分析及預測(至2035年):類型、產品類型、技術、應用、材料類型、設備、製程、最終用戶、功能、安裝類型2026年全球抗菌醫療設備塗層市場報告2026年全球醫用塗層市場報告

醫療設備抗菌塗層市場分析及預測(至2035年):類型、產品類型、技術、應用、材料類型、設備、製程、最終用戶、功能、安裝類型2026年全球抗菌醫療設備塗層市場報告2026年全球醫用塗層市場報告 全球醫用塗層市場,2026-2030年

全球醫用塗層市場,2026-2030年 生物活性複合材料市場按材料分類、生物活性化合物類型、形態、來源、應用和最終用戶類型分類-2026年至2032年全球預測醫用聚氨酯市場按應用、類型、形式和最終用戶分類-2026年至2032年全球預測

生物活性複合材料市場按材料分類、生物活性化合物類型、形態、來源、應用和最終用戶類型分類-2026年至2032年全球預測醫用聚氨酯市場按應用、類型、形式和最終用戶分類-2026年至2032年全球預測 日本醫療設備塗層市場規模、佔有率、趨勢及預測(按產品、材料、應用和地區分類),2026-2034年

日本醫療設備塗層市場規模、佔有率、趨勢及預測(按產品、材料、應用和地區分類),2026-2034年