|

市場調查報告書

商品編碼

1775085

全球暖通空調隔熱材料材料市場(按材料類型、產品類型、最終用途行業和地區分類)- 2030 年預測HVAC Insulation Market by Product Type (Pipes, Ducts), Material Type (Mineral Wool (Glass Wool, Stone Wool)), Plastic Foam (Phenolic, Elastomeric Foam), End-use Industry (Commercial, Residential, Industrial), and Region - Global Forecast to 2030 |

||||||

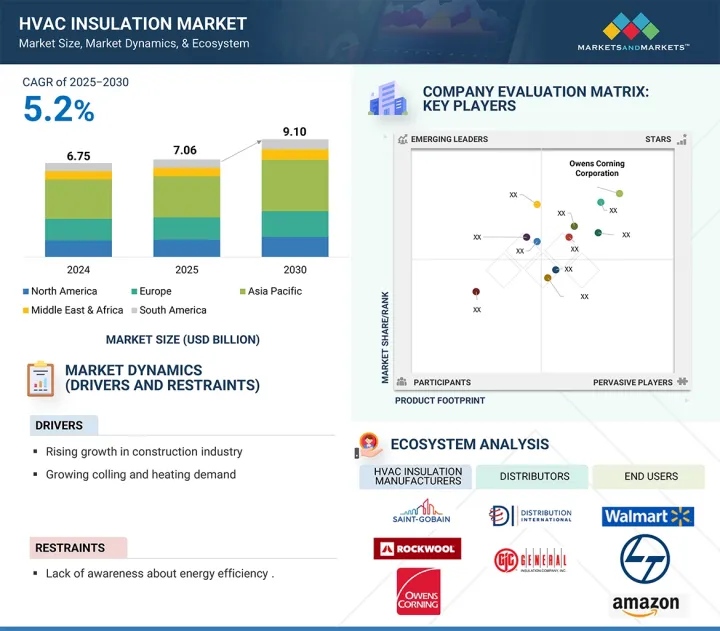

預計 HVAC隔熱材料市場規模將從 2025 年的 70.6 億美元成長到 2030 年的 91 億美元,預測期內的複合年成長率為 5.2%。

全球暖通空調 (HVAC)隔熱材料市場正經歷強勁成長,這主要得益於基礎設施建設、工業擴張以及新興經濟體的蓬勃發展。隨著各國大力投資基礎設施現代化,無論是住宅、商業或公共設施,對高效供暖、通風和空調 (HVAC) 系統的需求也持續成長。隔熱材料在提高這些系統的能源效率方面發揮關鍵作用,它能夠最大限度地減少熱損失和熱增益,提高熱性能,並降低營運成本。這使得隔熱材料成為永續建築實踐的重要組成部分,目前已在各個地區廣泛採用。工業擴張進一步促進了這一成長,尤其是在製造業、製藥業、食品加工和冷藏倉庫等溫度調節至關重要的領域。這些行業需要大型暖通空調系統,並且必須可靠且有效率地運作,而這只有透過適當的隔熱材料才能實現。隨著各行各業都致力於滿足嚴格的能源法規並減少對環境的影響,先進隔熱材料的應用正變得越來越廣泛。都市化、收入成長和人口成長正在推動亞太地區、拉丁美洲和中東地區新興經濟體的建築業繁榮。這些地區基礎設施的快速發展以及對節能和綠色建築的日益重視,推動了暖通空調隔熱材料需求的激增。這些因素共同推動了全球暖通空調隔熱材料市場的持續成長。

| 研究範圍 | |

|---|---|

| 調查年份 | 2022-2030 |

| 基準年 | 2024 |

| 預測期 | 2025-2030 |

| 對價單位 | 金額(百萬美元)、數量(千噸) |

| 部分 | 依材料類型、依產品類型、依最終用途產業、按地區 |

| 目標區域 | 北美、歐洲、亞太地區、南美、中東和非洲 |

塑膠發泡體是暖通空調 (HVAC)隔熱材料市場中重要的材料類型,以其卓越的隔熱性能、輕盈和多功能性而聞名。常用的泡沫塑膠類型包括聚氨酯 (PU)、聚異氰酸酯(PIR) 和發泡聚苯乙烯 (EPS),每種材料根據應用場合都具有各自的優勢。這些材料因其低導熱性、防潮性以及長期保持穩定性能而廣受青睞。塑膠發泡體在減少暖通空調 (HVAC) 系統中的熱傳遞、提高能源效率和降低營運成本方面尤其有效。其閉孔結構具有很強的抗吸水性,非常適合在潮濕環境和濕度控制至關重要的場合使用。此外,發泡塑膠易於安裝,可模製成各種形狀和尺寸,並具有很高的機械強度,使其成為商業和住宅建築中管道、管路和暖通空調 (HVAC) 裝置隔熱的理想選擇。

發泡塑膠隔熱材料的應用範圍涵蓋工業設施、辦公大樓、醫院、零售空間、住宅建築以及其他注重溫度控制和提高能源效率的領域。隨著對高性能、具成本效益隔熱材料的需求日益成長,尤其是在注重節能的建築領域,發泡塑膠領域在全球暖通空調隔熱材料市場中持續佔據主導地位。

工業領域作為暖通空調 (HVAC)隔熱材料市場的終端用戶,在市場中扮演關鍵角色,這主要得益於大型設施對高效能溫度調節、節能和降低營運成本的需求。製造業、製藥業、食品飲料加工、石化業以及低溫運輸物流等產業都高度依賴強大的暖通空調系統,以確保設備和人員處於受控的環境中。這些系統的隔熱對於最大限度地減少能量損失、維持穩定的室內溫度以及確保供暖和冷氣運行的效率至關重要。

工業環境中的暖通空調 (HVAC) 隔熱有助於防止熱波動,從而避免影響生產品質、安全標準或設備性能。例如,在製藥和食品行業,嚴格的溫度控制對於產品穩定性和法規合規性至關重要。適當的隔熱還能減輕暖通空調 (HVAC) 系統的負擔,延長其使用壽命並降低維護成本。

此外,工業設施通常在極端環境條件下運作(極熱或極冷),因此需要先進的隔熱材料。隨著對能源效率、永續性和遵守環境法規的日益重視,各行各業擴大採用高性能隔熱解決方案,以滿足綠色認證標準並減少碳排放。隨著全球工業基礎設施的擴張,尤其是在新興經濟體,預計該領域對暖通空調隔熱材料的需求將穩定成長。

歐洲暖通空調 (HVAC)隔熱材料市場正在穩步成長,這得益於嚴格的能源效率法規、綠色建築的普及以及對永續基礎設施日益成長的需求。該地區致力於減少碳排放並提高建築的能源性能,而暖通空調隔熱材料是實現這些目標的關鍵要素。

歐盟《建築能效指令》(EPBD)和《歐洲綠色交易》等主要法規結構要求各成員國進行節能建築和維修。這些政策提倡在暖通空調系統中使用高品質的隔熱材料,以減少住宅和商業建築的能耗和溫室氣體排放。此外,德國、法國和英國等國家也推出了多項國家級舉措,為節能維修提供誘因和補貼,進一步加速市場應用。

採用現代隔熱解決方案維修老舊建築的舉措,以及該地區致力於在2050年實現氣候中和的承諾,正在推動對先進暖通空調隔熱材料的強勁需求。歐洲成熟的建設產業,加上消費者和企業的高度環保意識,持續支撐市場。隨著持續的技術創新和嚴格的監管執行,歐洲暖通空調隔熱材料市場預計將繼續成為全球成長的主要貢獻者,尤其是在需要高性能、耐用性和環保合規性的應用領域。

本報告研究了全球暖通空調隔熱材料市場,材料類型、產品類型、最終用途行業、區域趨勢和參與市場的公司概況對其進行細分。

目錄

第1章 引言

第2章調查方法

第3章執行摘要

第4章重要考察

第5章市場概述

- 介紹

- 市場動態

- 專利分析

- 波特五力分析

- 生態系測繪

- 價值鏈分析

- 定價分析

- 貿易分析

- 總體經濟指標

- 影響客戶業務的趨勢/中斷

- 2025-2026 年重要會議與活動

- 投資金籌措場景

- 主要相關人員和採購標準

- 影響購買決策的關鍵因素

- 技術分析

- 監管狀況

- 人工智慧/生成式人工智慧對暖通空調隔熱材料市場的影響

- 案例研究分析

6.暖通空調隔熱材料市場(依材料類型)

- 介紹

- 礦棉

- 泡沫塑膠

第7章 HVAC隔熱材料市場(依產品類型)

- 介紹

- 管道

- 管

8. 暖通空調隔熱材料市場(依最終用途產業)

- 介紹

- 住房

- 商業

- 工業

9. 暖通空調隔熱材料市場(按地區)

- 介紹

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 其他

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他

- 中東和非洲

- 海灣合作理事會國家

- 南非

- 其他

第10章 競爭格局

- 介紹

- 主要參與企業的策略/優勢

- 收益分析

- 市場佔有率分析

- 估值和財務指標

- 品牌/產品比較分析

- 競賽評估矩陣:2024 年主要參與企業

- 競爭力評估矩陣:Start-Ups/中小型企業(SMES),2024年

- 競爭場景

第11章 公司簡介

- 主要參與企業

- SAINT-GOBAIN

- OWENS CORNING

- ROCKWOOL INTERNATIONAL

- ARMACELL INTERNATIONAL SA

- KNAUF GROUP

- KINGSPAN GROUP PLC

- JOHNS MANVILLE CORPORATION

- GLASSROCK INSULATION CO SAE

- L'ISOLANTE K-FLEX SPA

- URSA INSULATION SA

- 其他公司

- ARABIAN FIBREGLASS INSULATION CO. LTD.(AFICO)

- FLETCHER INSULATION

- COVESTRO AG

- PPG

- HUNTSMAN INTERNATIONAL LLC

- TROCELLEN

- LINDNER SE

- BRADFORD INSULATION PTY LIMITED

- SAGER AG

- UNION FOAM SPA

- SEKISUI FOAM AUSTRALIA

- GILSULATE INTERNATIONAL, INC.

- PROMAT INTERNATIONAL

- WINCELL INSULATION CO. LTD.

- VISIONARY INDUSTRIAL INSULATION

第12章 附錄

The HVAC insulation market is projected to reach USD 9.10 billion by 2030 from USD 7.06 billion in 2025, at a CAGR of 5.2% during the forecast period. The HVAC insulation market is experiencing robust growth globally, significantly fueled by infrastructure development, industrial expansion, and the rising momentum of emerging economies. As nations invest heavily in modernizing their infrastructure-be it residential, commercial, or public facilities-the demand for efficient heating, ventilation, and air conditioning (HVAC) systems continues to grow. HVAC insulation plays a crucial role in enhancing the energy efficiency of these systems by minimizing heat loss or gain, improving thermal performance, and reducing operational costs. This makes insulation an integral component of sustainable construction practices, which are now being widely adopted across various regions. Industrial expansion further contributes to this growth, especially in sectors like manufacturing, pharmaceuticals, food processing, and cold storage, where temperature regulation is essential. These industries require large-scale HVAC systems that must operate reliably and efficiently, which is only possible with proper insulation. As industries aim to meet stringent energy regulations and lower their environmental impact, the adoption of advanced insulation materials is becoming more widespread. Emerging economies in the Asia Pacific, Latin America, and the Middle East are witnessing a construction boom driven by urbanization, rising incomes, and population growth. These regions are rapidly upgrading their infrastructure, and with a growing focus on energy conservation and green buildings, the demand for HVAC insulation is rising sharply. Collectively, these factors are propelling sustained growth in the global HVAC insulation market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million), Volume (Kilotons) |

| Segments | Material Type, Product Type, End-use Industry, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and Middle East & Africa |

"Plastic foam segment is expected to be the second fastest-growing segment in the HVAC insulation market during the forecast period."

The plastic foam segment is a prominent material type in the HVAC insulation market, known for its excellent thermal insulation properties, lightweight nature, and versatility. Common types of plastic foams used include polyurethane (PU), polyisocyanurate (PIR), and expanded polystyrene (EPS), each offering specific advantages depending on the application. These materials are widely valued for their low thermal conductivity, moisture resistance, and ability to maintain consistent performance over time. Plastic foams are particularly effective in minimizing heat transfer in HVAC systems, which enhances energy efficiency and reduces operational costs. Their closed-cell structure provides strong resistance to water absorption, making them ideal for use in humid environments or where moisture control is critical. Additionally, plastic foams are easy to install, can be molded into various shapes and sizes, and offer good mechanical strength, making them suitable for insulating ducts, pipes, and HVAC units in both commercial and residential buildings.

Applications of plastic foam insulation span sectors such as industrial facilities, office buildings, hospitals, retail spaces, and homes, where controlling temperature and improving energy efficiency are priorities. As the demand for high-performance, cost-effective insulation materials grows-especially in energy-conscious construction-the plastic foam segment continues to gain traction in the HVAC insulation market globally.

"Industrial segment to be the second fastest-growing end-use industry in the HVAC insulation market during the forecast period"

The industrial segment plays a vital role as an end-use industry in the HVAC insulation market, driven by the need for efficient temperature regulation, energy conservation, and operational cost reduction in large-scale facilities. Industries such as manufacturing, pharmaceuticals, food and beverage processing, petrochemicals, and cold chain logistics heavily rely on robust HVAC systems to maintain controlled environments for both equipment and personnel. Insulation in these systems is crucial to minimizing energy loss, maintaining consistent indoor conditions, and ensuring the efficiency of heating and cooling operations.

HVAC insulation in industrial settings helps prevent thermal fluctuations that could compromise production quality, safety standards, or equipment performance. For instance, in the pharmaceutical and food industries, strict temperature control is essential for product stability and regulatory compliance. Proper insulation also reduces the strain on HVAC systems, thereby extending their lifespan and lowering maintenance costs.

Moreover, industrial facilities often operate in extreme environmental conditions-either very hot or very cold-making advanced insulation materials a necessity. With growing emphasis on energy efficiency, sustainability, and adherence to environmental regulations, industries are increasingly adopting high-performance insulation solutions to meet green certification standards and reduce their carbon footprint. As industrial infrastructure expands globally, especially in emerging economies, the demand for HVAC insulation in this segment is expected to grow steadily.

"Europe is projected to be the second-largest market for HVAC insulation during the forecast period"

The Europe HVAC insulation market is witnessing steady growth, driven by stringent energy efficiency regulations, increasing adoption of green building practices, and rising demand for sustainable infrastructure. The region places a strong emphasis on reducing carbon emissions and improving building energy performance, making HVAC insulation a critical component in achieving these goals.

Key regulatory frameworks such as the EU Energy Performance of Buildings Directive (EPBD) and the European Green Deal mandate energy-efficient construction and renovation across member states. These policies promote the use of high-quality insulation materials in HVAC systems to reduce energy consumption and greenhouse gas emissions in both residential and commercial buildings. Additionally, various national initiatives across countries like Germany, France, and the UK provide incentives and subsidies for energy-efficient upgrades, further accelerating market adoption.

The push for retrofitting older buildings with modern insulation solutions and the region's commitment to climate neutrality by 2050 are creating strong demand for advanced HVAC insulation materials. Europe's well-established construction industry, coupled with a high level of environmental awareness among consumers and businesses, continues to support the market. With ongoing innovation and strict regulatory enforcement, the European HVAC insulation market is expected to remain a key contributor to global growth, particularly in applications that require high performance, durability, and environmental compliance.

.

.

Extensive interviews were conducted with experts to determine and verify the market size for several segments and subsegments and the information gathered through secondary research.

The break-up of interviews with experts is given below:

- By Department: Tier 1: 40%, Tier 2: 25%, and Tier 3: 35%

- By Designation: C Level: 35%, Director Level: 30%, and Executives: 35%

- By Region: North America: 25%, Europe: 35%, Asia Pacific: 30%, South America: 5%, Middle East & Africa 5%

Owens Corning Corporation (US), Saint-Gobain SA (France), Knauf Group (US), Kingspan Group PLC (Ireland), Rockwool Group (Denmark), Armacell International SA (Germany), Johns Manville (US), Ursa Insulation S.A. (Spain), Huntsman Corporation (US), Covestro (Germany), L'ISOLANTE K-FLEX SPA (Italy), Union Foam SPA (Italy), Arabian Fiberglass Insulation Company Ltd. (Saudi Arabia), Glassrock Insulation Company (Egypt), and Visionary Industrial Insulation (US), among others are some of the key players in the HVAC insulation market.

The study includes an in-depth competitive analysis of these key players in the HVAC insulation market, with their company profiles, recent developments, and key market strategies.

Research Coverage

The market study covers the HVAC insulation market across various segments. It aims to estimate the market size and the growth potential of this market across different segments based on material type, product type, end-use industry, and region. The study also includes an in-depth competitive analysis of key players in the market, their company profiles, key observations related to their products and business offerings, recent developments undertaken by them, and key growth strategies adopted by them to improve their positions in the HVAC insulation market.

Key Benefits of Buying the Report

The report is expected to help the market leaders/new entrants in this market share the closest approximations of the revenue numbers of the overall HVAC insulation market and its segments and subsegments. This report is projected to help stakeholders understand the competitive landscape of the market, gain insights to improve the positions of their businesses, and plan suitable go-to-market strategies. The report also aims to help stakeholders understand the pulse of the market and provides them with information on the key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Rising growth in construction industry, Rising cooling and heating demand), restraints (Lack of awareness of energy efficiency ), opportunities (Innovation in eco-friendly insulation materials, Technological advancements in HVAC), challenges (Fire safety & toxicity concerns, Requirements of skilled workforce to hinder market growth)

- Market Development: Comprehensive information about lucrative markets - the report analyzes the HVAC insulation market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the HVAC insulation market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product and service offerings of leading players like Owens Corning Corporation (US), Saint-Gobain SA (France), Knauf Group (US), Kingspan Group PLC (Ireland), Rockwool Group (Denmark), Armacell International SA (Germany), Johns Manville (US), Ursa Insulation S.A. (Spain), Huntsman Corporation (US), Covestro (Germany), L'ISOLANTE K-FLEX SPA (Italy), Union Foam SPA (Italy), Arabian Fiberglass Insulation Company Ltd. (Saudi Arabia), Glassrock Insulation Company (Egypt), and Visionary Industrial Insulation (US), among others, are the top manufacturers covered in the HVAC insulation market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Primary interviews - demand and supply sides

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 TOP-DOWN APPROACH

- 2.2.2 BOTTOM-UP APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HVAC INSULATION MARKET

- 4.2 HVAC INSULATION MARKET, BY PRODUCT TYPE

- 4.3 HVAC INSULATION MARKET, BY MATERIAL TYPE

- 4.4 HVAC INSULATION MARKET, BY END-USE INDUSTRY

- 4.5 HVAC INSULATION MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Expanding construction industry

- 5.2.1.2 Stringent energy efficiency regulations and government support

- 5.2.1.3 Rising demand for cooling and heating systems

- 5.2.2 RESTRAINTS

- 5.2.2.1 Lack of awareness regarding energy savings and cost benefits associated with HVAC insulation

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Innovations in eco-friendly insulation materials

- 5.2.3.2 Technological advancements in HVAC systems

- 5.2.4 CHALLENGES

- 5.2.4.1 Fire safety and toxicity concerns

- 5.2.4.2 Requirement for skilled workforce

- 5.2.1 DRIVERS

- 5.3 PATENT ANALYSIS

- 5.3.1 METHODOLOGY

- 5.3.2 DOCUMENT TYPE

- 5.3.3 PUBLICATION TRENDS

- 5.3.4 INSIGHTS

- 5.3.5 JURISDICTION ANALYSIS

- 5.3.6 TOP 10 COMPANIES/APPLICANTS

- 5.4 PORTER'S FIVE FORCES ANALYSIS

- 5.4.1 THREAT OF SUBSTITUTES

- 5.4.2 BARGAINING POWER OF SUPPLIERS

- 5.4.3 THREAT OF NEW ENTRANTS

- 5.4.4 BARGAINING POWER OF BUYERS

- 5.4.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.5 ECOSYSTEM MAPPING

- 5.6 VALUE CHAIN ANALYSIS

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2030

- 5.7.2 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY, 2024

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO (HS CODE 680610)

- 5.8.2 EXPORT SCENARIO (HS CODE 680610)

- 5.9 MACROECONOMIC INDICATORS

- 5.9.1 GDP TRENDS AND FORECASTS

- 5.10 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.11 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.12 INVESTMENT AND FUNDING SCENARIO

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.14 KEY FACTORS IMPACTING BUYING DECISIONS

- 5.14.1 QUALITY

- 5.14.2 SERVICE

- 5.15 TECHNOLOGY ANALYSIS

- 5.15.1 KEY TECHNOLOGIES

- 5.15.1.1 ECOSE technology

- 5.15.2 COMPLEMENTARY TECHNOLOGIES

- 5.15.2.1 Smart thermostats and temperature control

- 5.15.2.2 Internet of Things (IoT) integration

- 5.15.1 KEY TECHNOLOGIES

- 5.16 REGULATORY LANDSCAPE

- 5.16.1 ASTM C1696-20

- 5.16.2 ASTM C547

- 5.16.3 ISO 13787:2003(E)

- 5.16.4 US

- 5.16.5 EUROPE

- 5.16.6 OTHERS

- 5.16.7 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.17 IMPACT OF AI/GEN AI ON HVAC INSULATION MARKET

- 5.18 CASE STUDY ANALYSIS

- 5.18.1 FLETCHER INSULATION

- 5.18.2 H.D. GAJRA BROS.

- 5.18.3 ROCKWOOL

6 HVAC INSULATION MARKET, BY MATERIAL TYPE

- 6.1 INTRODUCTION

- 6.2 MINERAL WOOL

- 6.2.1 GLASS WOOL

- 6.2.1.1 Superior thermal and acoustic insulation properties to drive demand

- 6.2.2 STONE WOOL

- 6.2.2.1 Abundant and easy availability of raw materials to drive market

- 6.2.1 GLASS WOOL

- 6.3 PLASTIC FOAM

- 6.3.1 PHENOLIC FOAM, PIR, & PUR

- 6.3.1.1 Excellent thermal properties, lightweight structure, and adaptability to drive market

- 6.3.2 ELASTOMERIC FOAM

- 6.3.2.1 Excellent fire-resistance properties to propel market

- 6.3.3 POLYETHYLENE

- 6.3.3.1 Lightweight and cost-effectiveness to increase adoption

- 6.3.3.2 XLPE (Cross-linked PE)

- 6.3.1 PHENOLIC FOAM, PIR, & PUR

7 HVAC INSULATION MARKET, BY PRODUCT TYPE

- 7.1 INTRODUCTION

- 7.2 PIPES

- 7.2.1 GROWING EMPHASIS ON ENERGY EFFICIENCY TO DRIVE MARKET

- 7.3 DUCTS

- 7.3.1 STRINGENT REGULATORY COMPLIANCE TO DRIVE MARKET

8 HVAC INSULATION MARKET, BY END-USE INDUSTRY

- 8.1 INTRODUCTION

- 8.2 RESIDENTIAL

- 8.2.1 STRONG GROWTH IN RESIDENTIAL SEGMENT TO DRIVE MARKET

- 8.3 COMMERCIAL

- 8.3.1 RAPID URBANIZATION TO DRIVE MARKET GROWTH

- 8.4 INDUSTRIAL

- 8.4.1 HIGH ENERGY EFFICIENCY OFFERED BY HVAC INSULATION TO DRIVE MARKET

9 HVAC INSULATION MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 ASIA PACIFIC

- 9.2.1 CHINA

- 9.2.1.1 Growth of construction industry to drive market

- 9.2.2 INDIA

- 9.2.2.1 Government-led initiatives aimed at developing infrastructure to drive demand

- 9.2.3 JAPAN

- 9.2.3.1 Strong focus on energy efficiency and energy conservation to drive market

- 9.2.4 SOUTH KOREA

- 9.2.4.1 Favorable business environment and government policies to drive market

- 9.2.5 REST OF ASIA PACIFIC

- 9.2.1 CHINA

- 9.3 EUROPE

- 9.3.1 GERMANY

- 9.3.1.1 Favorable business environments and industrial growth to drive market

- 9.3.2 FRANCE

- 9.3.2.1 Stringent regulations to drive market

- 9.3.3 UK

- 9.3.3.1 Continuous innovations and technological advancements to support market growth

- 9.3.4 ITALY

- 9.3.4.1 Increasing number of infrastructure projects to propel market

- 9.3.5 REST OF EUROPE

- 9.3.1 GERMANY

- 9.4 NORTH AMERICA

- 9.4.1 US

- 9.4.1.1 Stringent government regulations and rising consumer awareness for energy efficiency to propel market

- 9.4.2 CANADA

- 9.4.2.1 Booming construction industry to support market growth

- 9.4.3 MEXICO

- 9.4.3.1 High investments in construction industry to boost demand

- 9.4.1 US

- 9.5 SOUTH AMERICA

- 9.5.1 BRAZIL

- 9.5.1.1 Rising commercial construction activities to fuel demand

- 9.5.2 ARGENTINA

- 9.5.2.1 Government and private sector investments in construction industry to boost demand

- 9.5.3 REST OF SOUTH AMERICA

- 9.5.1 BRAZIL

- 9.6 MIDDLE EAST & AFRICA

- 9.6.1 GCC COUNTRIES

- 9.6.1.1 Saudi Arabia

- 9.6.1.1.1 Government-led projects related to construction industry to drive market

- 9.6.1.2 UAE

- 9.6.1.2.1 Robust growth of construction sector with government-led investments to boost demand

- 9.6.1.3 Rest of GCC countries

- 9.6.1.1 Saudi Arabia

- 9.6.2 SOUTH AFRICA

- 9.6.2.1 Stringent regulations for building insulation to propel market growth

- 9.6.3 REST OF MIDDLE EAST & AFRICA

- 9.6.1 GCC COUNTRIES

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 10.3 REVENUE ANALYSIS

- 10.4 MARKET SHARE ANALYSIS

- 10.5 COMPANY VALUATION AND FINANCIAL METRICS

- 10.6 BRAND/PRODUCT COMPARISON ANALYSIS

- 10.7 COMPETITIVE EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- 10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.7.5.1 Company footprint

- 10.7.5.2 Product type footprint

- 10.7.5.3 End-use industry footprint

- 10.7.5.4 Material type footprint

- 10.7.5.5 Region footprint

- 10.8 COMPETITIVE EVALUATION MATRIX: STARTUPS/SMALL AND MEDIUM-SIZED ENTERPRISES (SMES), 2024

- 10.8.1 RESPONSIVE COMPANIES

- 10.8.2 PROGRESSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- 10.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.8.5.1 Detailed list of key startups/SMEs

- 10.8.5.2 Competitive benchmarking of key startups/SMEs

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 DEALS

- 10.9.3 EXPANSIONS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 SAINT-GOBAIN

- 11.1.1.1 Business overview

- 11.1.1.2 Products offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Product launches

- 11.1.1.3.2 Deals

- 11.1.1.3.3 Expansions

- 11.1.1.4 MnM view

- 11.1.1.4.1 Key strengths/Right to win

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses/Competitive threats

- 11.1.2 OWENS CORNING

- 11.1.2.1 Business overview

- 11.1.2.2 Products offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Product launches

- 11.1.2.3.2 Deals

- 11.1.2.3.3 Expansions

- 11.1.2.4 MnM view

- 11.1.2.4.1 Key strengths/Right to win

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses/Competitive threats

- 11.1.3 ROCKWOOL INTERNATIONAL

- 11.1.3.1 Business overview

- 11.1.3.2 Products offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Product launches

- 11.1.3.3.2 Deals

- 11.1.3.3.3 Expansions

- 11.1.3.4 MnM view

- 11.1.3.4.1 Key strengths/Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses/Competitive threats

- 11.1.4 ARMACELL INTERNATIONAL SA

- 11.1.4.1 Business overview

- 11.1.4.2 Products offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Product launches

- 11.1.4.3.2 Deals

- 11.1.4.3.3 Expansions

- 11.1.4.4 MnM view

- 11.1.4.4.1 Key strengths/Right to win

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses/Competitive threats

- 11.1.5 KNAUF GROUP

- 11.1.5.1 Business overview

- 11.1.5.2 Products offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Product launches

- 11.1.5.3.2 Deals

- 11.1.5.3.3 Expansions

- 11.1.5.4 MnM view

- 11.1.5.4.1 Key strengths/Right to win

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses/Competitive threats

- 11.1.6 KINGSPAN GROUP PLC

- 11.1.6.1 Business overview

- 11.1.6.2 Products offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Product launches

- 11.1.6.3.2 Deals

- 11.1.6.4 MnM view

- 11.1.7 JOHNS MANVILLE CORPORATION

- 11.1.7.1 Business overview

- 11.1.7.2 Products offered

- 11.1.7.3 Recent developments

- 11.1.7.3.1 Product launches

- 11.1.7.3.2 Deals

- 11.1.7.3.3 Expansions

- 11.1.7.4 MnM view

- 11.1.8 GLASSROCK INSULATION CO S.A.E.

- 11.1.8.1 Business overview

- 11.1.8.2 Products offered

- 11.1.8.3 MnM view

- 11.1.9 L'ISOLANTE K-FLEX S.P.A.

- 11.1.9.1 Business overview

- 11.1.9.2 Products offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Expansions

- 11.1.9.4 MnM view

- 11.1.10 URSA INSULATION S.A.

- 11.1.10.1 Business overview

- 11.1.10.2 Products offered

- 11.1.10.3 MnM view

- 11.1.1 SAINT-GOBAIN

- 11.2 OTHER PLAYERS

- 11.2.1 ARABIAN FIBREGLASS INSULATION CO. LTD. (AFICO)

- 11.2.2 FLETCHER INSULATION

- 11.2.3 COVESTRO AG

- 11.2.4 PPG

- 11.2.5 HUNTSMAN INTERNATIONAL LLC

- 11.2.6 TROCELLEN

- 11.2.7 LINDNER SE

- 11.2.8 BRADFORD INSULATION PTY LIMITED

- 11.2.9 SAGER AG

- 11.2.10 UNION FOAM S.P.A.

- 11.2.11 SEKISUI FOAM AUSTRALIA

- 11.2.12 GILSULATE INTERNATIONAL, INC.

- 11.2.13 PROMAT INTERNATIONAL

- 11.2.14 WINCELL INSULATION CO. LTD.

- 11.2.15 VISIONARY INDUSTRIAL INSULATION

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS

List of Tables

- TABLE 1 HVAC INSULATION MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 TOP 10 PATENT OWNERS, 2015-2024

- TABLE 3 HVAC INSULATION: PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 ROLES OF COMPANIES IN HVAC INSULATION ECOSYSTEM

- TABLE 5 INDICATIVE PRICING ANALYSIS OF HVAC INSULATION MATERIALS OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY, 2024 (USD/KG)

- TABLE 6 IMPORT DATA FOR HS CODE 680610 -COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 7 EXPORT DATA FOR HS CODE 680610-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 8 PROJECTED REAL GDP GROWTH (ANNUAL PERCENTAGE CHANGE), BY KEY COUNTRY, 2019-2023 (%)

- TABLE 9 ANNUAL GDP PERCENTAGE CHANGE AND PROJECTION, BY KEY COUNTRY, 2024-2029 (%)

- TABLE 10 HVAC INSULATION MARKET: DETAILED LIST OF KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 11 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END-USE INDUSTRIES

- TABLE 12 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (USD MILLION)

- TABLE 16 HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 17 HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (KILOTON)

- TABLE 18 HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (KILOTON)

- TABLE 19 HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 20 HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 21 HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 22 HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 23 HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 24 HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 25 HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 26 HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 27 HVAC INSULATION MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 28 HVAC INSULATION MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 29 HVAC INSULATION MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 30 HVAC INSULATION MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 31 ASIA PACIFIC: HVAC INSULATION MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 32 ASIA PACIFIC: HVAC INSULATION MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 33 ASIA PACIFIC: HVAC INSULATION MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 34 ASIA PACIFIC: HVAC INSULATION MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 35 ASIA PACIFIC: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (USD MILLION)

- TABLE 36 ASIA PACIFIC: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 37 ASIA PACIFIC: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (KILOTON)

- TABLE 38 ASIA PACIFIC: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (KILOTON)

- TABLE 39 ASIA PACIFIC: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 40 ASIA PACIFIC: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 41 ASIA PACIFIC: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 42 ASIA PACIFIC: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 43 ASIA PACIFIC: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 44 ASIA PACIFIC: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 45 ASIA PACIFIC: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 46 ASIA PACIFIC: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 47 CHINA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 48 CHINA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 49 CHINA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 50 CHINA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 KILOTON)

- TABLE 51 INDIA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 52 INDIA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 53 INDIA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 54 INDIA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 55 JAPAN: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 56 JAPAN: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 57 JAPAN: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 58 JAPAN: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 59 SOUTH KOREA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 60 SOUTH KOREA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 61 SOUTH KOREA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 62 SOUTH KOREA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 63 REST OF ASIA PACIFIC: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 64 REST OF ASIA PACIFIC: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 65 REST OF ASIA PACIFIC: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 66 REST OF ASIA PACIFIC: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 67 EUROPE: HVAC INSULATION MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 68 EUROPE: HVAC INSULATION MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 69 EUROPE: HVAC INSULATION MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 70 EUROPE: HVAC INSULATION MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 71 EUROPE: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (USD MILLION)

- TABLE 72 EUROPE: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 73 EUROPE: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (KILOTON)

- TABLE 74 EUROPE: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (KILOTON)

- TABLE 75 EUROPE: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 76 EUROPE: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 77 EUROPE: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 78 EUROPE: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 79 EUROPE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 80 EUROPE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 81 EUROPE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 82 EUROPE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 83 GERMANY: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 84 GERMANY: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 85 GERMANY: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 86 GERMANY: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 87 FRANCE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 88 FRANCE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 89 FRANCE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 90 FRANCE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 91 UK: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 92 UK: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 93 UK: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 94 UK: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 95 ITALY: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 96 ITALY: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 97 ITALY: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 98 ITALY: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 99 REST OF EUROPE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 100 REST OF EUROPE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 101 REST OF EUROPE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 102 REST OF EUROPE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 103 NORTH AMERICA: HVAC INSULATION MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 104 NORTH AMERICA: HVAC INSULATION MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 105 NORTH AMERICA: HVAC INSULATION MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 106 NORTH AMERICA: HVAC INSULATION MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 107 NORTH AMERICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (USD MILLION)

- TABLE 108 NORTH AMERICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 109 NORTH AMERICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (KILOTON)

- TABLE 110 NORTH AMERICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (KILOTON)

- TABLE 111 NORTH AMERICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 112 NORTH AMERICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 113 NORTH AMERICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 114 NORTH AMERICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 115 NORTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 116 NORTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 117 NORTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 118 NORTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 119 US: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 120 US: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 121 US: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 122 US: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 123 CANADA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 124 CANADA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 125 CANADA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 126 CANADA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 127 MEXICO: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 128 MEXICO: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 129 MEXICO: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 130 MEXICO: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 131 SOUTH AMERICA: HVAC INSULATION MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 132 SOUTH AMERICA: HVAC INSULATION MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 133 SOUTH AMERICA: HVAC INSULATION MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 134 SOUTH AMERICA: HVAC INSULATION MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 135 SOUTH AMERICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (USD MILLION)

- TABLE 136 SOUTH AMERICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 137 SOUTH AMERICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (KILOTON)

- TABLE 138 SOUTH AMERICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (KILOTON)

- TABLE 139 SOUTH AMERICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 140 SOUTH AMERICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 141 SOUTH AMERICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 142 SOUTH AMERICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 143 SOUTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 144 SOUTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 145 SOUTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 KILOTON)

- TABLE 146 SOUTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 147 BRAZIL: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 148 BRAZIL: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 149 BRAZIL: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 150 BRAZIL: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 151 ARGENTINA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 152 ARGENTINA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 153 ARGENTINA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 154 ARGENTINA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 155 REST OF SOUTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 156 REST OF SOUTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 157 REST OF SOUTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 158 REST OF SOUTH AMERICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 159 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 160 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 161 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 162 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 163 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (USD MILLION)

- TABLE 164 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 165 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2022-2024 (KILOTON)

- TABLE 166 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY MATERIAL TYPE, 2025-2030 (KILOTON)

- TABLE 167 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (USD MILLION)

- TABLE 168 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 169 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2022-2024 (KILOTON)

- TABLE 170 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 171 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 172 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 173 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 174 MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 175 SAUDI ARABIA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 176 SAUDI ARABIA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 177 SAUDI ARABIA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 178 SAUDI ARABIA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 179 UAE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 180 UAE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 181 UAE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 182 UAE: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 183 REST OF GCC COUNTRIES: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 184 REST OF GCC COUNTRIES: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 185 REST OF GCC COUNTRIES: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 186 REST OF GCC COUNTRIES: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 187 SOUTH AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 188 SOUTH AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 189 SOUTH AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 190 SOUTH AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 191 REST OF MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 192 REST OF MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 193 REST OF MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 194 REST OF MIDDLE EAST & AFRICA: HVAC INSULATION MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 195 HVAC INSULATION MARKET: OVERVIEW OF MAJOR STRATEGIES ADOPTED BY KEY PLAYERS BETWEEN 2020 AND 2025

- TABLE 196 HVAC INSULATION MARKET: DEGREE OF COMPETITION, 2024

- TABLE 197 HVAC INSULATION MARKET: PRODUCT TYPE FOOTPRINT

- TABLE 198 HVAC INSULATION MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 199 HVAC INSULATION MARKET: MATERIAL TYPE FOOTPRINT

- TABLE 200 HVAC INSULATION MARKET: REGION FOOTPRINT

- TABLE 201 HVAC INSULATION MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 202 HVAC INSULATION MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 203 HVAC INSULATION MARKET: PRODUCT LAUNCHES, JANUARY 2020-MAY 2025

- TABLE 204 HVAC INSULATION MARKET: DEALS, JANUARY 2020-MAY 2025

- TABLE 205 HVAC INSULATION MARKET: EXPANSIONS, JANUARY 2020-MAY 2025

- TABLE 206 SAINT-GOBAIN: COMPANY OVERVIEW

- TABLE 207 SAINT-GOBAIN: PRODUCT OFFERINGS

- TABLE 208 SAINT-GOBAIN: PRODUCT LAUNCHES

- TABLE 209 SAINT-GOBAIN: DEALS

- TABLE 210 SAINT-GOBAIN: EXPANSIONS

- TABLE 211 OWENS CORNING: COMPANY OVERVIEW

- TABLE 212 OWENS CORNING: PRODUCT OFFERINGS

- TABLE 213 OWENS CORNING: PRODUCT LAUNCHES

- TABLE 214 OWENS CORNING: DEALS

- TABLE 215 OWENS CORNING: EXPANSIONS

- TABLE 216 ROCKWOOL INTERNATIONAL: COMPANY OVERVIEW

- TABLE 217 ROCKWOOL INTERNATIONAL: PRODUCT OFFERINGS

- TABLE 218 ROCKWOOL INTERNATIONAL: PRODUCT LAUNCHES

- TABLE 219 ROCKWOOL INTERNATIONAL: DEALS

- TABLE 220 ROCKWOOL INTERNATIONAL: EXPANSIONS

- TABLE 221 ARMACELL INTERNATIONAL SA: COMPANY OVERVIEW

- TABLE 222 ARMACELL INTERNATIONAL SA: PRODUCT OFFERINGS

- TABLE 223 ARMACELL INTERNATIONAL SA: PRODUCT LAUNCHES

- TABLE 224 ARMACELL INTERNATIONAL SA: DEALS

- TABLE 225 ARMACELL INTERNATIONAL SA: EXPANSIONS

- TABLE 226 KNAUF GROUP: COMPANY OVERVIEW

- TABLE 227 KNAUF GROUP: PRODUCT OFFERINGS

- TABLE 228 KNAUF GROUP: PRODUCT LAUNCHES

- TABLE 229 KNAUF GROUP: DEALS

- TABLE 230 KNAUF GROUP: EXPANSIONS

- TABLE 231 KINGSPAN GROUP PLC: COMPANY OVERVIEW

- TABLE 232 KINGSPAN GROUP PLC: PRODUCT OFFERINGS

- TABLE 233 KINGSPAN GROUP PLC: PRODUCT LAUNCHES

- TABLE 234 KINGSPAN GROUP PLC: DEALS

- TABLE 235 JOHNS MANVILLE CORPORATION: COMPANY OVERVIEW

- TABLE 236 JOHNS MANVILLE CORPORATION: PRODUCT OFFERINGS

- TABLE 237 JOHNS MANVILLE CORPORATION: PRODUCT LAUNCHES

- TABLE 238 JOHNS MANVILLE CORPORATION: DEALS

- TABLE 239 JOHNS MANVILLE CORPORATION: EXPANSIONS

- TABLE 240 GLASSROCK INSULATION CO S.A.E.: COMPANY OVERVIEW

- TABLE 241 GLASSROCK INSULATION CO S.A.E.: PRODUCT OFFERINGS

- TABLE 242 L'ISOLANTE K-FLEX S.P.A.: COMPANY OVERVIEW

- TABLE 243 L'ISOLANTE K-FLEX S.P.A.: PRODUCT OFFERINGS

- TABLE 244 L'ISOLANTE K-FLEX S.P.A.: EXPANSIONS

- TABLE 245 URSA INSULATION S.A.: COMPANY OVERVIEW

- TABLE 246 URSA INSULATION S.A.: PRODUCT OFFERINGS

List of Figures

- FIGURE 1 HVAC INSULATION MARKET: SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 HVAC INSULATION MARKET: RESEARCH DESIGN

- FIGURE 3 TOP-DOWN APPROACH

- FIGURE 4 BOTTOM-UP APPROACH

- FIGURE 5 HVAC INSULATION MARKET: DATA TRIANGULATION

- FIGURE 6 DUCTS SEGMENT TO HOLD LARGER MARKET SHARE IN 2030

- FIGURE 7 PLASTIC FOAM SEGMENT TO HOLD LARGER MARKET SHARE IN 2030

- FIGURE 8 COMMERCIAL SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 9 ASIA PACIFIC ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 10 RISING DEMAND FROM CONSTRUCTION INDUSTRY TO CREATE LUCRATIVE OPPORTUNITIES FOR MARKET PLAYERS

- FIGURE 11 PIPES TO BE FAST-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 12 MINERAL WOOL TO BE FAST-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 13 RESIDENTIAL TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 14 INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 15 HVAC INSULATION MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 16 GRANTED PATENTS ACCOUNTED FOR MAJOR SHARE FROM 2015 TO 2024

- FIGURE 17 TOTAL NUMBER OF PATENTS PER YEAR, 2015-2024

- FIGURE 18 TOP JURISDICTIONS FOR HVAC INSULATION PATENTS, 2015-2024

- FIGURE 19 TOP 10 COMPANIES/APPLICANTS WITH HIGHEST PERCENTAGE OF PATENTS, 2015-2024

- FIGURE 20 HVAC INSULATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 21 HVAC INSULATION ECOSYSTEM MAPPING

- FIGURE 22 HVAC INSULATION MARKET: VALUE CHAIN ANALYSIS

- FIGURE 23 AVERAGE SELLING PRICE TREND OF HVAC INSULATION MATERIALS, BY REGION, 2022-2030 (USD/KG)

- FIGURE 24 AVERAGE SELLING PRICE TREND OF HVAC INSULATION MATERIALS OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY, 2024 (USD/KG)

- FIGURE 25 IMPORT DATA RELATED TO HS CODE 680610 -COMPLIANT PRODUCTS, BY KEY COUNTRY, 2020-2024 (USD THOUSAND)

- FIGURE 26 EXPORT DATA RELATED TO HS CODE 680610-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2020-2024 (USD THOUSAND)

- FIGURE 27 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 28 HVAC INSULATION MARKET: INVESTMENT AND FUNDING SCENARIO (USD MILLION)

- FIGURE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END-USE INDUSTRIES

- FIGURE 30 SUPPLIER SELECTION CRITERIA

- FIGURE 31 PLASTIC FOAM SEGMENT TO BE LARGER MATERIAL TYPE DURING FORECAST PERIOD

- FIGURE 32 PIPES SEGMENT TO REGISTER HIGHER GROWTH DURING FORECAST PERIOD

- FIGURE 33 COMMERCIAL SEGMENT TO DOMINATE MARKET IN 2025

- FIGURE 34 HVAC INSULATION MARKET IN INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 35 ASIA PACIFIC: HVAC INSULATION MARKET SNAPSHOT

- FIGURE 36 EUROPE: HVAC INSULATION MARKET SNAPSHOT

- FIGURE 37 HVAC INSULATION MARKET: REVENUE ANALYSIS OF KEY COMPANIES, 2022-2024 (USD BILLION)

- FIGURE 38 HVAC INSULATION MARKET SHARE ANALYSIS, 2024

- FIGURE 39 HVAC INSULATION MARKET: COMPANY VALUATION OF LEADING COMPANIES, 2024 (USD BILLION)

- FIGURE 40 HVAC INSULATION MARKET: FINANCIAL METRICS OF LEADING COMPANIES, 2024

- FIGURE 41 HVAC INSULATION MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 42 HVAC INSULATION MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 43 HVAC INSULATION MARKET: COMPANY FOOTPRINT

- FIGURE 44 HVAC INSULATION MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 45 SAINT-GOBAIN: COMPANY SNAPSHOT

- FIGURE 46 OWENS CORNING: COMPANY SNAPSHOT

- FIGURE 47 ROCKWOOL INTERNATIONAL: COMPANY SNAPSHOT

- FIGURE 48 ARMACELL INTERNATIONAL SA: COMPANY SNAPSHOT

- FIGURE 49 KINGSPAN GROUP PLC: COMPANY SNAPSHOT

暖通空調隔熱材料市場:全球市場預測,2026-2032年

暖通空調隔熱材料市場:全球市場預測,2026-2032年 暖通空調隔熱材料市場報告:趨勢、預測及競爭分析(至2035年)HVAC隔熱材料市場:全球產業分析、市場規模、市佔率及2026年至2033年預測,依產品類型、應用、通路、材料類型、最終用戶、國家及地區分類。

暖通空調隔熱材料市場報告:趨勢、預測及競爭分析(至2035年)HVAC隔熱材料市場:全球產業分析、市場規模、市佔率及2026年至2033年預測,依產品類型、應用、通路、材料類型、最終用戶、國家及地區分類。 HVAC隔熱材料市場規模、佔有率和趨勢分析報告:按產品、材料、應用、分銷管道、最終用途、地區和細分市場預測(2026-2033年)

HVAC隔熱材料市場規模、佔有率和趨勢分析報告:按產品、材料、應用、分銷管道、最終用途、地區和細分市場預測(2026-2033年) 暖通空調隔熱材料市場報告:按材料、產品類型、應用和地區分類(2026-2034 年)

暖通空調隔熱材料市場報告:按材料、產品類型、應用和地區分類(2026-2034 年) 暖通空調隔熱材料市場規模、佔有率及成長分析(依製程、材料類型、組件、應用、最終用戶及地區分類)-2026-2033年產業預測

暖通空調隔熱材料市場規模、佔有率及成長分析(依製程、材料類型、組件、應用、最終用戶及地區分類)-2026-2033年產業預測 暖通空調隔熱材料市場 - 2025 年至 2030 年預測美國暖通空調隔熱材料市場規模、佔有率、趨勢分析報告:按產品、材料、分銷管道、應用、最終用途、細分市場預測,2025-2030 年

暖通空調隔熱材料市場 - 2025 年至 2030 年預測美國暖通空調隔熱材料市場規模、佔有率、趨勢分析報告:按產品、材料、分銷管道、應用、最終用途、細分市場預測,2025-2030 年 暖通空調隔熱材料市場:全球產業分析、規模、佔有率、成長、趨勢與預測,2025-2032年

暖通空調隔熱材料市場:全球產業分析、規模、佔有率、成長、趨勢與預測,2025-2032年 暖通空調隔熱材料市場(按材料類型、化學性質、應用和地區分類)

暖通空調隔熱材料市場(按材料類型、化學性質、應用和地區分類)