|

市場調查報告書

商品編碼

2071397

無鈷陰極材料市場機會、成長要素、產業趨勢分析及2026-2035年預測。Cobalt-Free Cathode Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

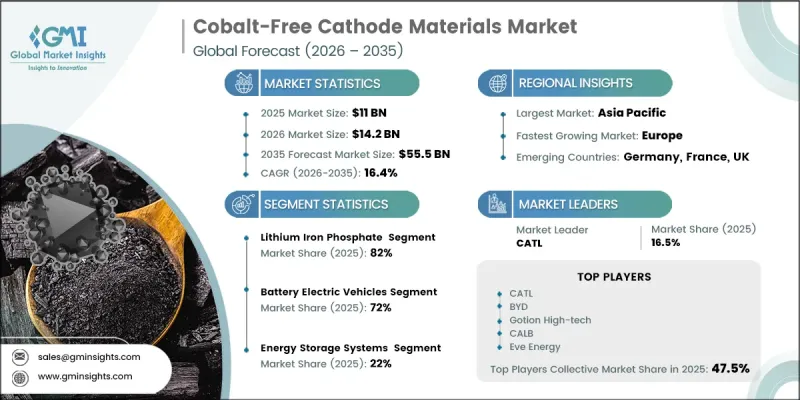

全球無鈷陰極材料市場預計到 2025 年將達到 110 億美元,並以 16.4% 的複合年成長率成長,到 2035 年將達到 555 億美元。

這一成長趨勢主要得益於從高鈷含量化學成分向替代成分的果斷轉變,這些替代成分消除了供應鏈風險並降低了材料成本。監管部門對負責任採購的監管力道不斷加強,加上對整個電池價值鏈的大規模投資,持續加速這些替代成分的普及。同時,材料科學的進步正在縮小鈷基電池和無鈷電池之間的性能差距,使後者實用化應用於更廣泛的領域。成本優勢仍然是關鍵因素,無鈷化學成分在保持高安全性和耐久性的同時,顯著降低了每千瓦時的成本。產業合作的加強、生產效率的提高以及有利的政策支持,都為市場的長期擴張做出了貢獻。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 110億美元 |

| 預測金額 | 555億美元 |

| 複合年成長率 | 16.4% |

市場格局正經歷結構性轉變,從傳統的正極材料成分轉向磷酸鋰鐵和錳增強型替代材料,徹底擺脫了對鈷的依賴。更嚴格的監管要求和持續減少對不穩定原料供應鏈依賴的努力進一步推動了這一轉變。成本競爭力持續提升,磷酸鋰鐵每千瓦時的成本比傳統化學成分降低了約30%。雖然由於製造流程複雜,富錳型正極材料的價格略高,但與含鈷材料相比,它們仍然保持著整體成本優勢。

到2025年,磷酸鋰鐵鋰將佔82%的市場佔有率,這體現了其強大的商業化和規模化優勢。這一優勢得益於其高熱穩定性、優異的安全性能以及基於廣泛可得原料的成熟供應鏈系統。這些特性使其成為大規模部署的理想選擇,尤其適用於那些對安全性、使用壽命和成本效益要求極高的應用領域。

到2025年,電池式電動車(BEV)市場佔有率將達到72%。此細分市場的需求持續變化,標準續航里程電池系統與先進的快速充電解決方案之間的差異日益明顯。材料密度和充電性能的提升,使得電池的應用場景更加廣泛,並提高了系統的整體效率。

2025年,北美無鈷正極材料市場佔有率將達到11%,但由於國內對電池製造和儲能基礎設施的投資不斷增加,其戰略重要性持續提升。美國仍然是主要的需求中心,這得益於大規模能源儲存系統部署的快速擴張和電動車解決方案的日益普及。持續的政策支持和供應鏈在地化措施預計將進一步鞏固該地區的市場地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 專利趨勢

- 貿易統計

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- LATAM

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依材料化學類型分類,2022-2035年

- 磷酸鋰鐵(LFP)

- 磷酸錳鐵鋰(LMFP)

- 鎳錳鋁氧化物(NMA)

- 高鎳層狀氧化物(LNO基)

- 富鋰層狀氧化物(LMR)

- 錳基尖晶石(LMO)

- 其他

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 電池式電動車(BEV)

- 搭乘用純電動車

- 商用純電動車(卡車、巴士)

- 插電式混合動力車(PHEV)

- 固定能源儲存系統(ESS)

- 網格級儲能系統

- 商用和工業用儲能系統

- 住宅儲能系統

- 家用電子產品

- 智慧型手機和平板電腦

- 筆記型電腦和穿戴式裝置

- 其他

第7章 市場估計與預測:依最終用戶分類,2022-2035年

- 汽車原廠設備製造商

- 電池製造商

- 能源儲存系統系統整合商

- 家用電子電器製造商

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- UAE

- 其他中東和非洲國家

第9章:公司簡介

- BTR New Material Group

- BYD Company Limited

- CATL(Contemporary Amperex Technology)

- Dynanonic Ltd.

- Epsilon Advanced Materials

- IBU-tec Advanced Materials AG

- IBUvolt Battery Materials GmbH

- Integrals Power Pte. Ltd.

- Mitra Chem Inc.

- Nano One Materials Corp.

- Redoxion Ltd.

- Sparkz Inc.

- Sumitomo Metal Mining Co., Ltd.

- Targray Technology International

- Umicore NV

- Western CAM Inc.

The Global Cobalt-Free Cathode Materials Market was valued at USD 11 billion in 2025 and is estimated to grow at a CAGR of 16.4% to reach USD 55.5 billion by 2035.

The growth trajectory is driven by a decisive transition away from cobalt-intensive chemistries toward alternatives that eliminate supply chain risk and reduce material costs. Increasing regulatory scrutiny around responsible sourcing, combined with large-scale investments across the battery value chain, continues to accelerate adoption. At the same time, advancements in material engineering have narrowed the performance gap between cobalt-based and cobalt-free solutions, making the latter viable across a wider range of applications. Cost advantages remain a central factor, as cobalt-free chemistries deliver significantly lower cost per kWh while maintaining strong safety and durability characteristics. Growing industrial alignment, improved manufacturing efficiencies, and favorable policy support are collectively reinforcing long-term market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11 Billion |

| Forecast Value | $55.5 Billion |

| CAGR | 16.4% |

The market is shaped by a structural migration away from traditional cathode compositions toward lithium iron phosphate and manganese-enhanced alternatives that completely remove cobalt dependency. This shift is further supported by tightening compliance requirements and ongoing efforts to reduce exposure to volatile raw material supply chains. Cost competitiveness continues to improve, with lithium iron phosphate offering nearly a 30% lower cost-per-kWh compared to conventional chemistries. Manganese-enriched variants, while slightly more expensive due to processing complexity, still maintain an overall cost advantage when compared to cobalt-containing materials.

The lithium iron phosphate segment accounted for 82% share in 2025, reflecting its strong commercialization and scalability advantages. Its dominance is supported by high thermal stability, improved safety performance, and a well-established supply ecosystem based on widely available raw materials. These characteristics have positioned it as the preferred choice for large-scale adoption, particularly in applications where safety, longevity, and cost efficiency are critical considerations.

The battery electric vehicles segment held 72% share in 2025. Demand within this segment continues to evolve, with clear differentiation emerging between standard-range battery systems and advanced fast-charging solutions. Improvements in material density and charging performance are enabling broader use cases and enhancing overall system efficiency.

North America Cobalt-Free Cathode Materials Market held a 11% share in 2025, yet its strategic importance continues to rise due to increasing domestic investments in battery manufacturing and energy storage infrastructure. The United States remains a key demand hub, supported by rapid growth in large-scale energy storage deployments and rising adoption of electric mobility solutions. Continued policy backing and supply chain localization efforts are expected to further strengthen regional market positioning.

Key participants in the Global Cobalt-Free Cathode Materials Market include BTR New Material Group, Dynanonic Ltd., Nano One Materials Corp., Integrals Power Pte. Ltd., IBU-tec Advanced Materials AG, Mitra Chem Inc., Redoxion Ltd., Sparkz Inc., CATL (Contemporary Amperex Technology Co., Ltd.), BYD Company Limited, and Epsilon Advanced Materials. Companies operating in the cobalt-free cathode materials market are focusing on capacity expansion, vertical integration, and advanced material innovation to strengthen their competitive position. Strategic collaborations across the battery value chain are enabling firms to secure raw material supply and enhance production efficiency. Investments in research and development are driving improvements in energy density, cycle life, and fast-charging capabilities, helping companies differentiate their offerings. Many players are also prioritizing regional manufacturing footprints to align with local policy incentives and reduce supply chain risks. In addition, partnerships with automotive and energy storage stakeholders are supporting long-term demand visibility while accelerating the commercialization of next-generation cathode technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material chemistry

- 2.2.3 Application

- 2.2.4 End user industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Chemistry Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Lithium iron phosphate (LFP)

- 5.3 Lithium manganese iron phosphate (LMFP)

- 5.4 Nickel-manganese-aluminum oxide (NMA)

- 5.5 High-nickel layered oxides (LNO-based)

- 5.6 Lithium-rich layered oxides (LMR)

- 5.7 Manganese-based spinels (LMO)

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Battery electric vehicles (BEV)

- 6.2.1 Passenger BEV

- 6.2.2 Commercial BEV (Trucks, Buses)

- 6.3 Plug-in hybrid electric vehicles (PHEV)

- 6.4 Stationary energy storage systems (ESS)

- 6.4.1 Grid-scale ESS

- 6.4.2 Commercial & industrial ESS

- 6.4.3 Residential ESS

- 6.5 Consumer electronics

- 6.5.1 Smartphones & tablets

- 6.5.2 Laptops & wearables

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End User, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive OEMs

- 7.3 Battery cell manufacturers

- 7.4 Energy storage system integrators

- 7.5 Consumer electronics manufacturers

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BTR New Material Group

- 9.2 BYD Company Limited

- 9.3 CATL (Contemporary Amperex Technology)

- 9.4 Dynanonic Ltd.

- 9.5 Epsilon Advanced Materials

- 9.6 IBU-tec Advanced Materials AG

- 9.7 IBUvolt Battery Materials GmbH

- 9.8 Integrals Power Pte. Ltd.

- 9.9 Mitra Chem Inc.

- 9.10 Nano One Materials Corp.

- 9.11 Redoxion Ltd.

- 9.12 Sparkz Inc.

- 9.13 Sumitomo Metal Mining Co., Ltd.

- 9.14 Targray Technology International

- 9.15 Umicore N.V.

- 9.16 Western CAM Inc.

住宅鋰離子電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型和最終用途產業、地區和競爭格局分類,2021-2031年商用鋰離子電池市場:全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用途產業和地區分類),競爭格局(2021-2031 年)工業鋰離子電池市場:全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用途產業和地區分類)、競爭格局(2021-2031 年)船用鋰離子電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、電壓、可充電/不可充電、應用、地區和競爭格局分類,2021-2031年

住宅鋰離子電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型和最終用途產業、地區和競爭格局分類,2021-2031年商用鋰離子電池市場:全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用途產業和地區分類),競爭格局(2021-2031 年)工業鋰離子電池市場:全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用途產業和地區分類)、競爭格局(2021-2031 年)船用鋰離子電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、電壓、可充電/不可充電、應用、地區和競爭格局分類,2021-2031年 2026-2030年全球鋰離子電池市場

2026-2030年全球鋰離子電池市場 鋰離子電池市場:依化學成分、電壓範圍、外形規格及應用分類-2026-2032年全球市場預測

鋰離子電池市場:依化學成分、電壓範圍、外形規格及應用分類-2026-2032年全球市場預測 鋰離子電池市場:按類型、應用和地區分類

鋰離子電池市場:按類型、應用和地區分類 2026-2030年全球鋰離子電池市場圓柱形全極耳電池製造設備市場:按設備類型、電池類型、製造階段、產能、技術類型、最終用途分類,全球預測(2026-2032年)

2026-2030年全球鋰離子電池市場圓柱形全極耳電池製造設備市場:按設備類型、電池類型、製造階段、產能、技術類型、最終用途分類,全球預測(2026-2032年) 鋰離子電池市場規模、佔有率、趨勢和預測:按產品類型、功率容量、應用和地區分類,2026-2034年

鋰離子電池市場規模、佔有率、趨勢和預測:按產品類型、功率容量、應用和地區分類,2026-2034年