|

市場調查報告書

商品編碼

2071388

床墊及床墊組件市場機會、成長促進因素、產業趨勢分析及2026-2035年預測Mattress and Mattress Component Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

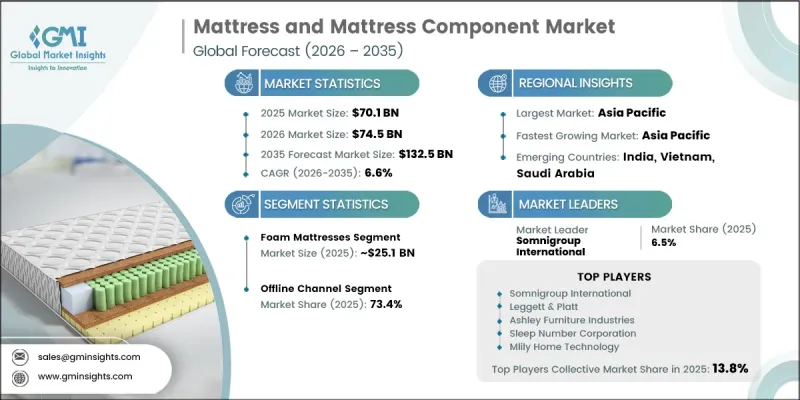

全球床墊及床墊組件市場預計到 2025 年將達到 701 億美元,年複合成長率為 6.6%,到 2035 年將達到 1,325 億美元。

市場擴張的促進因素包括:人口結構變化促使人們定期更換床墊;開發中國家的快速都市化;以及消費者對睡眠品質作為健康核心要素的日益重視。住宅建設活動的復甦進一步推動了成熟市場和新興市場對床墊的更換需求。消費者對睡眠不足的認知不斷提高,這源自於人們越來越意識到睡眠不足是一個重要的公共衛生問題,促使各個收入階層的消費者增加對睡眠改善產品的支出。雖然高階和超高階床墊市場在北美和歐洲等已開發地區迅速擴張,但在亞洲和中東,隨著中產階級的壯大,高品質床墊系統的普及速度也正在加速。家庭支出模式數據顯示,在一些主要經濟體,睡眠相關產品的支出成長速度超過了耐用消費品整體的成長速度。同時,從實體店向線上銷售管道的轉變正在重塑定價結構、品牌互動和客戶獲取策略,使擁有強大直銷(D2C)能力的製造商能夠鞏固其長期市場地位。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 701億美元 |

| 預測金額 | 1325億美元 |

| 複合年成長率 | 6.6% |

發泡材床墊市場目前佔35.8%的市場佔有率,預計到2025年銷售額將達到251億美元。由於消費者擴大轉向混合型床墊系統,以及泡沫製造關鍵原料成本的上漲,泡沫床墊市場的成長速度正在放緩。成本壓力對多個已開發市場的製造商造成了顯著影響,導致生產成本增加。在這一品類中,對基礎泡棉產品的需求正在放緩,而具有更佳散熱性、透氣性和抗菌性能的高性能產品則獲得了更強的市場支持,並超越了傳統產品。

預計到2025年,線下銷售管道將佔據73.4%的市場佔有率,市場規模將達到515億美元。該通路持續保持其主導地位,因為消費者傾向於親自體驗產品,尤其是在購買高價商品時,舒適度評估至關重要。然而,隨著線上購物的日益普及,線下通路的市佔率正逐漸被數位平台蠶食。在線下零售業內部,整合趨勢日益明顯:大規模連鎖零售商透過拓展產品線和提升客戶體驗策略來鞏固市場地位,而小規模獨立零售商則因消費者購買行為的改變而面臨日益激烈的競爭壓力。

預計到2025年,北美床墊及床墊配件市場規模將達2,14億美元,市佔率將達30.5%。北美市場需求旺盛,得益於穩定的更換週期、消費者對睡眠健康的高認知、完善的零售體系。該地區的消費者產品偏好也在轉變,對高階睡眠系統和高科技床墊解決方案的需求日益成長。流通結構的轉型以及對直銷模式(DTT)的日益重視,正在重塑市場競爭格局,並對產業的長期發展產生影響。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 住宅市場的復甦提振了新房購買和更換的需求。

- 人們睡眠健康的意識日益增強,以及消費者對高階產品的偏好趨勢。

- DTC和電子商務管道的激增

- 來自飯店、醫療保健和機構部門的需求不斷成長。

- 產業潛在風險與挑戰

- 中型企業正面臨市場飽和和產業重組帶來的壓力。

- 亞洲產零件會受到關稅不確定性和供應鏈成本波動的影響。

- 機會

- 智慧床墊與睡眠技術的融合正在推動高階市場的發展。

- 永續性驅動了對有機、可回收和生態認證材料的需求。

- 促進因素

- 成長潛力分析

- 監理框架

- 標準和合規要求

- 區域監理框架

- 認證標準

- 關鍵市場趨勢與顛覆性因素

- 技術與創新展望

- 當前趨勢

- 新進展

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 未來市場趨勢

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 波特的分析

- PESTLE分析

- 目前分銷基礎設施和通路滲透情況

- 按地區與業態(現代零售與傳統零售)分類的通路覆蓋率

- 最後一公里基礎設施差異和不斷變化的管道(DTC、社交電商、快閃店)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 泡棉床墊

- 記憶海綿

- 凝膠泡沫

- 聚氨酯泡棉

- 混合床墊

- 彈簧床墊

- 邦內爾線圈

- 口袋線圈

- 連續線圈

- 偏置線圈

- 乳膠床墊

- 其他(水床、氣墊床等)

第6章 市場估計與預測:依組件類型分類,2022-2035年

- 支撐層

- 形式

- 內彈簧

- 乳膠

- 混合

- 舒適層

- 絕緣墊

- 被子層

- 中級軟墊家具

- 其他

第7章 市場規模估算與預測(2022-2035年)

- 均碼

- 雙人床

- 全尺寸或雙人尺寸

- 特大號

- 其他

第8章 市場估算與預測:依價格區間分類,2022-2035年

- 低的

- 中等的

- 高的

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 住宅

- 商業

- 飯店業

- 衛生保健

- 對機構而言

- 其他

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 超級市場和大賣場

- 專賣店

- 其他(個體店、百貨公司等)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- UAE

- 沙烏地阿拉伯

- 南非

第12章:公司簡介

- 世界公司

- Ashley Furniture Industries

- Business Overview

- Financial Data

- Product Landscape

- Strategic Outlook

- SWOT Analysis

- DeRUCCI

- Hilding Anders

- Leggett &Platt

- Mlily Home Technology

- Sleep Number Corporation

- Somnigroup International

- Ashley Furniture Industries

- 當地公司

- Duroflex

- Hastens

- King Koil International

- Magniflex

- Pikolin

- Relyon

- Silentnight Group

- 新興企業

- Avocado Green Mattress

- Eight Sleep

- Emma Sleep

- Helix Sleep(3Z Brands)

- Saatva

- Wakefit

- Zinus

The Global Mattress and Mattress Component Market was valued at USD 70.1 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 132.5 billion by 2035.

Market expansion is driven by demographic shifts that support consistent replacement cycles, rapid urbanization across developing economies, and a growing consumer emphasis on sleep quality as a core component of overall health and wellness. Recovery in residential construction activity is further reinforcing demand for mattress replacements across both mature and emerging markets. Recognition of sleep deprivation as a significant public health issue has increased consumer awareness, encouraging higher spending on improved sleep products across diverse income groups. Premium and ultra-premium mattress categories are expanding at a faster pace in developed regions such as North America and Europe, while rising middle-class populations in Asia and the Middle East are accelerating adoption of higher-quality mattress systems. Data on household consumption patterns shows that spending on sleep-related products is increasing faster than broader durable goods categories in several leading economies. At the same time, the transition from physical retail to digital sales channels is reshaping pricing structures, brand engagement, and customer acquisition strategies, enabling manufacturers with strong direct-to-consumer capabilities to strengthen long-term market positioning.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.1 Billion |

| Forecast Value | $132.5 Billion |

| CAGR | 6.6% |

The foam-based mattresses segment accounted for 35.8% share, generating USD 25.1 billion in 2025. Growth is moderated by increasing consumer migration toward hybrid mattress systems and rising input costs associated with key raw materials used in foam production. Cost pressures have notably impacted manufacturers in several developed markets, leading to higher production expenses. Within this category, basic foam products are experiencing slower demand, while enhanced variants with improved cooling, airflow, and antimicrobial properties are gaining stronger traction and outperforming traditional formats.

The offline distribution channel segment held a 73.4% share in 2025, amounting to USD 51.5 billion. Its continued dominance is linked to consumer preference for physical product testing, particularly for high-value purchases where comfort evaluation plays a critical role. However, the channel is gradually losing share to digital platforms as online purchasing adoption increases. Within offline retail, consolidation trends are becoming more visible, with larger organized retailers strengthening their market position through expanded product offerings and improved customer experience strategies, while smaller independent retailers are facing increasing competitive pressure due to shifting consumer buying behavior.

North America Mattress and Mattress Component Market accounted for 30.5% share in 2025, representing USD 21.4 billion. Demand in North America is supported by stable replacement cycles, high consumer awareness of sleep health, and a well-developed retail ecosystem. The region is also experiencing changes in product preference, with increased demand for premium sleep systems and technologically advanced mattress solutions. Evolving distribution dynamics and growing emphasis on direct-to-consumer models are reshaping market competitiveness and influencing long-term industry structure.

Major companies operating in the Global Mattress and Mattress Component Market include Ashley Furniture Industries, Avocado Green Mattress, DeRUCCI, Duroflex, Eight Sleep, Emma Sleep, Hastens, Helix Sleep (3Z Brands), Hilding Anders, King Koil International, Leggett & Platt, Magniflex, Mlily Home Technology Co., Ltd, Pikolin, Relyon, Saatva, Silentnight Group, Sleep Number Corporation, Somnigroup International, Wakefit, and Zinus. Companies in the mattress and mattress component market are focusing on innovation-led growth strategies to strengthen their competitive position. Product development efforts are increasingly centered on hybrid construction, enhanced pressure relief systems, and advanced temperature regulation technologies to improve sleep quality. Manufacturers are also investing in direct-to-consumer business models and digital retail platforms to improve customer engagement and strengthen brand loyalty. Expansion of product portfolios across multiple price segments is helping companies address both value-driven and premium consumer groups. Strategic partnerships with material suppliers and sleep technology firms are supporting continuous product enhancement and differentiation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.2.1 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Region

- 2.2.2 Product Type

- 2.2.3 Component Type

- 2.2.4 Size

- 2.2.5 Price Range

- 2.2.6 End Use

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Housing market recovery fuels demand for new purchases and replacements

- 3.2.1.2 Growing awareness of sleep health & trend of consumer premiumization

- 3.2.1.3 Surge in DTC & e-commerce channels

- 3.2.1.4 Rising demand from hospitality, healthcare & institutional sectors

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Mid-tier players face pressure from market saturation & consolidation

- 3.2.2.2 Asian-sourced components hit by tariff uncertainty & supply chain cost fluctuations

- 3.2.3 Opportunities

- 3.2.3.1 Integration of smart mattresses & sleep technology boosts premium segment

- 3.2.3.2 Demand for organic, recycled, & eco-certified materials driven by sustainability

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 Standards & compliance requirements

- 3.4.2 Regional regulatory frameworks

- 3.4.3 Certification standards

- 3.5 Major market trends and disruptions

- 3.6 Technology/innovation landscape

- 3.6.1 Current trends

- 3.6.2 Emerging trends

- 3.7 Pricing Analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.8 Future market trends

- 3.9 Trade data analysis (driven by paid database) (HS Code- 9404)

- 3.9.1 Import/export volume & value trends (driven by primary research)

- 3.9.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 Gen-AI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.13.1 Channel coverage by region & format (modern vs. Traditional trade) (driven by primary research)

- 3.13.2 Last-mile infrastructure gaps & emerging channel shifts (DTC, social commerce, pop-up retail) (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Foam mattress

- 5.2.1 Memory Foam

- 5.2.2 Gel-Infused Foam

- 5.2.3 Polyurethane Foam

- 5.3 Hybrid mattress

- 5.4 Innerspring mattress

- 5.4.1 Bonnell Coil

- 5.4.2 Pocket Coil

- 5.4.3 Continuous Coil

- 5.4.4 Offset Coil

- 5.5 Latex mattress

- 5.6 Others (waterbed, airbed, etc.)

Chapter 6 Market Estimates and Forecast, By Component Type, 2022 - 2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Support Layer

- 6.2.1 Foam

- 6.2.2 Innerspring

- 6.2.3 Latex

- 6.2.4 hybrid

- 6.3 Comfort Layer

- 6.3.1 Insulator Pad

- 6.3.2 Quilt Layer

- 6.3.3 Middle Upholstery

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Size, 2022 - 2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Single size

- 7.3 Twin size

- 7.4 Full or double size

- 7.5 King size

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Price Range, 2022 - 2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.3.1 Hospitality

- 9.3.2 Healthcare

- 9.3.3 Institutional

- 9.3.4 Others

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-Commerce

- 10.2.2 Company website

- 10.3 Offline

- 10.3.1 Supermarkets/hypermarkets

- 10.3.2 Specialty stores

- 10.3.3 Others (individual stores, departmental stores, etc.)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 U.K.

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Global Companies

- 12.1.1 Ashley Furniture Industries

- 12.1.1.1 Business Overview

- 12.1.1.2 Financial Data

- 12.1.1.3 Product Landscape

- 12.1.1.4 Strategic Outlook

- 12.1.1.5 SWOT Analysis

- 12.1.2 DeRUCCI

- 12.1.3 Hilding Anders

- 12.1.4 Leggett & Platt

- 12.1.5 Mlily Home Technology

- 12.1.6 Sleep Number Corporation

- 12.1.7 Somnigroup International

- 12.1.1 Ashley Furniture Industries

- 12.2 Regional Companies

- 12.2.1 Duroflex

- 12.2.2 Hastens

- 12.2.3 King Koil International

- 12.2.4 Magniflex

- 12.2.5 Pikolin

- 12.2.6 Relyon

- 12.2.7 Silentnight Group

- 12.3 Emerging Companies

- 12.3.1 Avocado Green Mattress

- 12.3.2 Eight Sleep

- 12.3.3 Emma Sleep

- 12.3.4 Helix Sleep (3Z Brands)

- 12.3.5 Saatva

- 12.3.6 Wakefit

- 12.3.7 Zinus

豪華床墊市場機會、成長要素、產業趨勢分析及2026-2035年預測。

豪華床墊市場機會、成長要素、產業趨勢分析及2026-2035年預測。 寢具和床墊市場:未來預測(至2034年)-按產品類型、材料、床墊尺寸、價格範圍、技術、最終用戶和地區分類的全球分析

寢具和床墊市場:未來預測(至2034年)-按產品類型、材料、床墊尺寸、價格範圍、技術、最終用戶和地區分類的全球分析 記憶海綿床墊市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、分銷管道、地區和競爭格局分類,2021-2031年

記憶海綿床墊市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、分銷管道、地區和競爭格局分類,2021-2031年 床墊市場規模、佔有率和成長分析:按產品類型、尺寸、價格範圍、銷售管道、最終用戶和地區分類-2026-2033年產業預測床墊市場商機、成長要素、產業趨勢分析及2026-2035年預測。嬰幼兒床墊市場:商機、成長要素、產業趨勢分析及2026-2035年預測

床墊市場規模、佔有率和成長分析:按產品類型、尺寸、價格範圍、銷售管道、最終用戶和地區分類-2026-2033年產業預測床墊市場商機、成長要素、產業趨勢分析及2026-2035年預測。嬰幼兒床墊市場:商機、成長要素、產業趨勢分析及2026-2035年預測 床墊市場:依原料、尺寸、技術、結構設計、通路和應用分類-2026-2030年全球市場預測

床墊市場:依原料、尺寸、技術、結構設計、通路和應用分類-2026-2030年全球市場預測 單人床墊市場規模、佔有率和成長分析:按材質、尺寸、最終用戶、價格範圍、分銷管道和地區分類-2026-2033年產業預測床墊墊層市場機會、成長要素、產業趨勢分析及2026-2035年預測。牛墊市場:2026-2032年全球市場預測(依最終用戶、材料、應用、銷售管道、農場規模和安裝類型分類)

單人床墊市場規模、佔有率和成長分析:按材質、尺寸、最終用戶、價格範圍、分銷管道和地區分類-2026-2033年產業預測床墊墊層市場機會、成長要素、產業趨勢分析及2026-2035年預測。牛墊市場:2026-2032年全球市場預測(依最終用戶、材料、應用、銷售管道、農場規模和安裝類型分類)