|

市場調查報告書

商品編碼

2071379

水果採摘機器人市場機會、成長要素、產業趨勢分析及2026-2035年預測。Fruit Picking Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

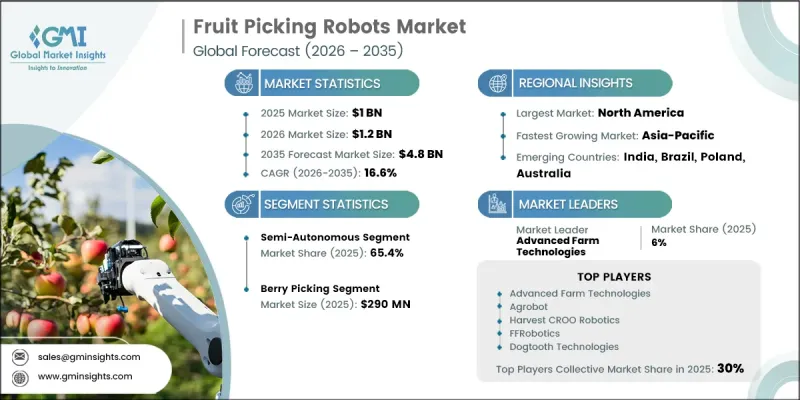

全球水果採摘機器人市場預計到 2025 年將達到 10 億美元,年複合成長率為 16.6%,到 2035 年將達到 48 億美元。

該市場正從實驗和試點階段過渡到商業性擴張的早期階段。特別是漿果和蘋果等高價值水果,由於其勞動密集度高且對採摘時間要求嚴格,使得自動化在經濟上更具可行性。一個關鍵的結構性變化是,在機器人即服務 (RaaS)資金籌措模式和硬體成本持續下降的支持下,機器人採摘的應用範圍正從大型農業企業擴展到中型農場。同時,包括物聯網田間感測器、無人機監測系統、精密農業平台和農場管理軟體在內的數位農業生態系統的整合,正在建構大規模機器人採摘所需的基礎設施。農業系統間數據連接性和互通性的提高進一步增強了機器人採摘的可行性。整體市場走向反映出一種以生產力主導的機械化趨勢,旨在解決勞動力短缺問題、提高採摘均勻度並減少對大規模勞動力的依賴。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 10億美元 |

| 預計金額 | 48億美元 |

| 複合年成長率 | 16.6% |

到2025年,半自動機器人將佔據65.4%的市場。這一主導地位源於當前的技術階段,在品質評估、密集作物環境下的導航協調以及收割物流協調等方面,仍需要人工監督。半自動系統結合了機器人精準的果實偵測和採摘能力,以及人工在關鍵控制點的決策能力,從而在保持可靠性的同時,提高了作業效率,即使在複雜的農業環境中也能如此。這些系統之所以被廣泛採用,是因為它們在自動化優勢和實際應用適應性之間取得了平衡。

預計到2025年,莓果採摘市場規模將達2.9億美元。這個市場主導地位主要源自於莓果採摘對勞動力的高需求,以及生產集中在人事費用高的地區,這使得自動化在經濟上極具吸引力。漿果作物需要精細處理和頻繁採摘,因此非常適合採用機器人技術。該領域持續進行大規模技術研發,旨在提高整個商業農業的採摘精度、速度和作物處理效率。

預計2025年,北美水果採摘機器人市場規模將達3.3億美元。這主要得益於主要水果產區強勁的需求,這些產區勞動密集,且面臨季節性勞動力短缺。此外,該地區先進的農業基礎設施、自動化技術的早期應用以及機器人技術在商業農業中日益廣泛的應用,進一步鞏固了其主導地位。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 前景

- 製造商

- 中斷

- 供應商情況

- 主要新聞和舉措

- 技術與創新展望

- 監理情勢

- 影響因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 2025年價格分析

- 2022-2025年歷史價格趨勢分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 區域價格波動分析

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 生產能力和生產情況

- 設備產能:按地區和主要生產商分類

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依自動化程度分類,2022-2035年

- 全自動機器人

- 半自動自主機器人

第6章 市場估算與預測:依作物類型分類,2022-2035年

- 採摘漿果

- 蘋果採摘

- 葡萄和葡萄園的收穫

- 柑橘採摘

- 核果豐收

- 其他作物(酪梨、奇異果、芒果和新興作物)

第7章 市場估算與預測:依部署環境分類,2022-2035年

- 露天果園

- 溫室和可控制環境農業(CEA)

- 葡萄園

- 研究機構和實驗農場

第8章 市場估算與預測:依導航系統分類,2022-2035年

- 輪式移動機器人

- 鐵路系統

- 多機器人協作系統

- 飛機和無人機支援系統

- 其他(新興和混合導航平台)

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 銷售代理商和經銷商

- 農業機械經銷商

- 區域農業技術經銷商

- 線上銷售

- 製造商的電子商務平台

- 第三方農業機械市場

- 其他(租賃、RaaS模式、與農業技術培養箱合作)

第10章及預測:區域細分,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- UAE

- 沙烏地阿拉伯

- 南非

第11章:公司簡介

- 世界公司

- Dogtooth Technologies

- Harvest CROO Robotics

- Advanced Farm Technologies

- Zimmer Group

- J. Schmalz GmbH

- Zivid

- FFRobotics

- Tevel Aerobotics Technologies

- 當地公司

- Fieldwork Robotics

- Agrobot

- MetoMotion

- Organifarms

- Ripe Robotics

- Robotics Plus

- Suzhou Botian Automation Technology

- 新興企業

- NeuPeak Robotics

- Four Growers

- Nanovel

- Picker Agrobotics

- Gripwiq

- K2 Tech/Qogori

The Global Fruit Picking Robots Market was valued at USD 1 billion in 2025 and is estimated to grow at a CAGR of 16.6% to reach USD 4.8 billion in 2035.

The market is transitioning from experimental and pilot-focused deployments to early commercial scaling, particularly in high-value fruit categories such as berries and apples, where labor intensity and harvest timing sensitivity have strengthened the economic case for automation. A key structural evolution is the expansion of adoption beyond large agribusinesses to mid-sized farming operations, supported by Robotics-as-a-Service financing models and steadily declining hardware costs. At the same time, the integration of digital agriculture ecosystems, including IoT-enabled field sensors, drone-based monitoring systems, precision farming platforms, and farm management software, is establishing the infrastructure required for large-scale robotic harvesting adoption. Improved data connectivity and interoperability across agricultural systems are further enhancing deployment feasibility. The overall market direction reflects a shift toward productivity-driven mechanization aimed at addressing labor shortages, improving harvest consistency, and reducing operational dependence on seasonal workforce availability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 16.6% |

The semi-autonomous segment held a 65.4% share in 2025. This leadership is attributed to the current technological stage, where human oversight remains necessary for quality assessment, navigation adjustments within dense crop environments, and harvest logistics coordination. Semi-autonomous systems combine robotic precision in fruit detection and picking with human decision-making at critical control points, enabling improved operational efficiency while maintaining reliability in complex agricultural settings. These systems are widely adopted due to their balance between automation benefits and practical field adaptability.

The berry picking application segment captured USD 290 million in 2025. This dominance is driven by the high labor requirements associated with berry harvesting and the concentration of production in regions where labor costs are elevated, increasing the financial attractiveness of automation. Berry crops require delicate handling and frequent harvesting cycles, making them well-suited for robotic intervention. The segment continues to attract significant technological development aimed at improving picking accuracy, speed, and crop handling efficiency across commercial farming operations.

North America Fruit Picking Robots Market generated USD 330 million in 2025, supported by strong demand from major fruit-producing states with intensive labor requirements and seasonal workforce constraints. The region's leadership is reinforced by advanced agricultural infrastructure, early adoption of automation technologies, and increasing integration of robotics into commercial farming practices.

Major companies operating in the fruit picking robots market include Robotics Plus, Agrobot, Advanced Farm Technologies, Harvest CROO Robotics, Tevel Aerobotics Technologies, Fieldwork Robotics, Ripe Robotics, FFRobotics, Four Growers, Dogtooth Technologies, Organifarms, Picker Agrobotics, NeuPeak Robotics, MetoMotion, Suzhou Botian Automation Technology, Nanovel, K2 Tech / Qogori, Zimmer Group, Zivid, J. Schmalz GmbH, and Gripwiq. Companies operating in the global fruit picking robots market are adopting several strategic initiatives to strengthen their competitive positioning and accelerate commercialization. A major focus is the development of AI-enabled vision systems that improve fruit detection accuracy and enable more efficient harvesting in complex canopy environments. Firms are increasingly shifting toward Robotics-as-a-Service business models to reduce upfront costs and expand adoption among mid-scale farmers. Strategic partnerships with agricultural cooperatives and farm operators are being used to facilitate real-world deployment and performance validation. Companies are also investing in modular robot designs that can be adapted for multiple crop types, improving asset utilization across seasons.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Automation Level

- 2.2.3 Crop Type

- 2.2.4 Deployment Environment

- 2.2.5 Navigation System

- 2.2.6 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Technology & Innovation Landscape

- 3.5 Regulatory landscape

- 3.6 Impact on forces

- 3.6.1 Growth drivers

- 3.6.2 Industry pitfalls & challenges

- 3.6.3 Opportunities

- 3.7 Pricing analysis, 2025 (driven by primary research)

- 3.7.1 Historical price trend analysis (2022-2025)

- 3.7.2 Pricing strategy by player type (premium/value/cost-plus)

- 3.7.3 Regional price variation analysis

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Trade data analysis (driven by paid database)

- 3.11.1 Import/export volume & value trends (Driven by Primary Research)

- 3.11.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Automation Level, 2022-2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Fully Autonomous Robots

- 5.3 Semi-Autonomous Robots

Chapter 6 Market Estimates & Forecast, By Crop Type, 2022-2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Berry Picking

- 6.3 Apple Picking

- 6.4 Grape & Vineyard Picking

- 6.5 Citrus Picking

- 6.6 Stone Fruit Picking

- 6.7 Others (Avocado, Kiwi, Mango & Emerging)

Chapter 7 Market Estimates & Forecast, By Deployment Environment, 2022-2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Open-Field Orchards

- 7.3 Greenhouses & Controlled Environment Agriculture (CEA)

- 7.4 Vineyards

- 7.5 Research Institutes & Trial Farms

Chapter 8 Market Estimates & Forecast, By Navigation System, 2022-2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Wheeled Mobile Robots

- 8.3 Rail-Based Systems

- 8.4 Multi-Robot Collaborative Systems

- 8.5 Aerial & Drone-Assisted Systems

- 8.6 Others (Emerging & Hybrid Navigation Platforms)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct Sales

- 9.3 Distributors & Dealers

- 9.3.1 Agricultural Equipment Dealers

- 9.3.2 Regional Agri-Tech Distributors

- 9.4 Online Sales

- 9.4.1 Manufacturer E-Commerce Platforms

- 9.4.2 Third-Party Agricultural Equipment Marketplaces

- 9.5 Others (Leasing, RaaS Models & Agri-Tech Incubator Partnerships)

Chapter 10 & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 U.K.

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Global players

- 11.1.1 Dogtooth Technologies

- 11.1.2 Harvest CROO Robotics

- 11.1.3 Advanced Farm Technologies

- 11.1.4 Zimmer Group

- 11.1.5 J. Schmalz GmbH

- 11.1.6 Zivid

- 11.1.7 FFRobotics

- 11.1.8 Tevel Aerobotics Technologies

- 11.2 Regional players

- 11.2.1 Fieldwork Robotics

- 11.2.2 Agrobot

- 11.2.3 MetoMotion

- 11.2.4 Organifarms

- 11.2.5 Ripe Robotics

- 11.2.6 Robotics Plus

- 11.2.7 Suzhou Botian Automation Technology

- 11.3 Emerging players

- 11.3.1 NeuPeak Robotics

- 11.3.2 Four Growers

- 11.3.3 Nanovel

- 11.3.4 Picker Agrobotics

- 11.3.5 Gripwiq

- 11.3.6 K2 Tech / Qogori

2026-2030年全球農作物收割機器人市場

2026-2030年全球農作物收割機器人市場 2026年全球收割機器人市場報告

2026年全球收割機器人市場報告 農業作物收割機器人市場:按運作模式、組件、作物類型、應用和最終用戶分類-2026-2032年全球市場預測2026年全球人工智慧機器人揀選市場報告

農業作物收割機器人市場:按運作模式、組件、作物類型、應用和最終用戶分類-2026-2032年全球市場預測2026年全球人工智慧機器人揀選市場報告 2034年水果採摘機器人市場預測-全球分析(按機器人類型、移動方式、水果類型、部署模式、自主程度、農場規模、技術、最終用戶和地區分類)全球收割機器人市場預測至2034年—按機器人類型、收割方法、作物類型、農業環境、農場類型、組件、應用、最終用戶和地區分類的分析

2034年水果採摘機器人市場預測-全球分析(按機器人類型、移動方式、水果類型、部署模式、自主程度、農場規模、技術、最終用戶和地區分類)全球收割機器人市場預測至2034年—按機器人類型、收割方法、作物類型、農業環境、農場類型、組件、應用、最終用戶和地區分類的分析 收割機器人市場:按類型、機器人型號和地區分類水果採摘機器人市場:按水果類型、部署方式、技術、應用、最終用戶、自主性和產品/服務分類-全球預測,2026-2032年

收割機器人市場:按類型、機器人型號和地區分類水果採摘機器人市場:按水果類型、部署方式、技術、應用、最終用戶、自主性和產品/服務分類-全球預測,2026-2032年 全球收割機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年)水果採摘機器人市場按類型、應用和地區分類

全球收割機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年)水果採摘機器人市場按類型、應用和地區分類