|

市場調查報告書

商品編碼

2071348

心臟人工器官市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Cardiac Prosthetic Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

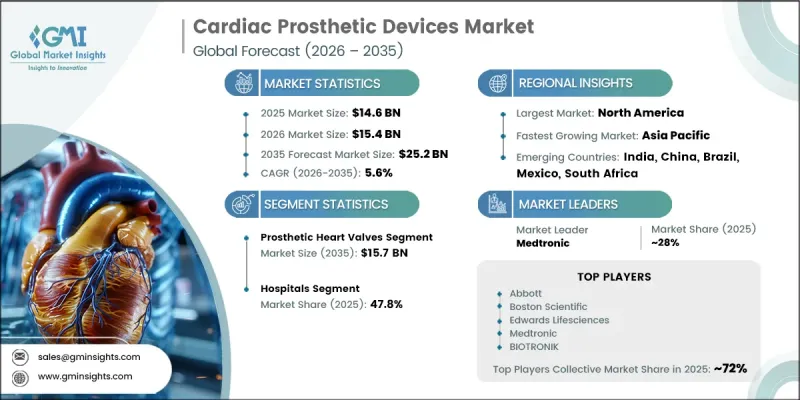

預計到 2025 年,全球心臟假體市場價值將達到 146 億美元,並預計以 5.6% 的複合年成長率成長,到 2035 年達到 252 億美元。

市場擴張的促進因素包括心血管疾病盛行率上升、微創心血管手術的日益普及、器械技術的不斷進步以及全球人口老化。其他成長要素還包括最新人工心臟解決方案帶來的臨床療效改善,以及能夠處理複雜心臟介入手術的醫療基礎設施的擴建。臨床上對植入式心臟輔助裝置的依賴性日益增強,進一步推高了全球醫療系統的需求。醫療設備材料、耐用性和血液動力學性能的技術進步也促進了其應用率的提高。此外,人們對早期診斷和治療心臟疾病重要性的認知不斷提高,也持續推動醫院和專科心臟中心進行相關手術,從而在整個預測期內保持市場穩定成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 146億美元 |

| 預測金額 | 252億美元 |

| 複合年成長率 | 5.6% |

心臟假體是一種可植入式醫療醫療設備,旨在當心臟出現結構或電生理異常時,恢復或取代正常的心臟功能。這些裝置主要包括心臟節律管理系統,例如人工心臟瓣膜和心律調節器,並廣泛用於治療瓣膜性心臟病、心律不整和心臟衰竭等疾病。微創手術(包括經導管手術)的普及顯著改變了現代循環系統的治療方法。器械工程、生物相容性材料和手術技術的持續創新進一步改善了病患的治療效果和手術安全性。此外,診斷能力的提升和介入性心臟病學基礎設施的完善也促進了心臟假體在臨床實踐中的更廣泛應用。尤其是在高齡化社會中,全球心血管疾病負擔的日益加重,推動了對先進植入式治療方案的需求,以治療瓣膜功能障礙和心律不整等疾病,而這種需求將持續成長。

預計到2035年,心臟瓣膜市場規模將達到157億美元,2026年至2035年的複合年成長率(CAGR)為6.1%。此細分市場的成長主要受瓣膜性心臟病(包括主動脈瓣狹窄和二尖瓣逆流)盛行率上升的驅動。這些疾病與老化密切相關,通常需要進行外科手術或經導管瓣膜置換術。臨床上對先進人工瓣膜解決方案的日益青睞也推動了該細分市場的持續成長。

到2025年,醫院市佔率將達到47.8%。由於醫院擁有先進的基礎設施、導管檢查室和專業的醫療團隊,它們仍然是心臟假體植入手術的主要治療場所。這些設施對於進行瓣膜置換術和心律調節器植入等複雜手術至關重要。除了龐大的患者數量外,醫院還憑藉其先進的影像和外科技術,繼續保持心血管疾病診療中心的地位。

預計到2025年,北美將佔據心臟假體市場43.1%的佔有率。這一主導地位主要得益於心血管疾病(如冠狀動脈疾病、心臟衰竭、心律不整和瓣膜性心臟病)的高發生率。肥胖、高血壓、不良飲食和缺乏運動等生活方式相關的風險因素持續加劇這些疾病的盛行率。完善的醫療保健基礎設施和先進的心臟護理體系進一步促進了全部區域心臟假體的應用。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 全球心血管疾病盛行率正在上升。

- 微創手術正變得越來越普及。

- 心臟人工器官的技術進步

- 老年人口增加及其相關的心臟病

- 產業潛在風險與挑戰

- 醫療設備和手術高成本

- 熟練醫護人員短缺

- 市場機遇

- 無引線空間製造器和裝置小型化技術的進步

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術展望

- 最新科技趨勢

- 新興技術

- 價格趨勢分析

- 未來市場趨勢

- 波特的分析

- PESTLE分析

- 人工智慧和生成式人工智慧對市場的影響

- 專利分析

- 價值鏈分析

- 差距分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 人工心臟瓣膜

- 機械心臟瓣膜

- 生物來源的心臟瓣膜

- 經導管心臟瓣膜置換術(TAVR/TMVR)

- 心律調節器

- 植入式心臟節律器

- 單腔心律調節器

- 雙腔心律調節器

- 雙心室型/CRT心律調節器

- 體外心律調節器

- 植入式心臟節律器

第6章 市場估算與預測:依最終用途分類,2022-2035年

- 醫院

- 專業心臟病中心

- 門診手術中心

- 其他最終用戶

第7章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第8章:公司簡介

- Abbott

- Artivion

- BIOTRONIK

- Boston Scientific

- Colibri Heart Valve

- CORCYM

- Edwards Lifesciences

- Labcor Laboratorios

- Lepu Medical

- Medtronic

- Meril Life Sciences

- MicroPort

- Pacetronix

- Venus Medtech

The Global Cardiac Prosthetic Devices Market was valued at USD 14.6 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 25.2 billion by 2035.

Market expansion is driven by the rising prevalence of cardiovascular diseases, increasing adoption of minimally invasive cardiac procedures, continuous advancements in device technologies, and a growing geriatric population worldwide. Additional growth factors include improved clinical outcomes associated with modern prosthetic solutions and expanding healthcare infrastructure capable of supporting complex cardiac interventions. The increasing clinical reliance on implantable cardiac support devices is further strengthening demand across global healthcare systems. Technological progress in device materials, durability, and hemodynamic performance is also enhancing adoption rates. Furthermore, rising awareness of early diagnosis and treatment of cardiac conditions continues to support procedural volumes across hospitals and specialized cardiac centers, reinforcing steady market growth over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.6 Billion |

| Forecast Value | $25.2 Billion |

| CAGR | 5.6% |

Cardiac prosthetic devices are implantable medical technologies designed to restore or replace normal cardiac function when structural or electrical heart abnormalities occur. These devices primarily include prosthetic heart valves and cardiac rhythm management systems such as pacemakers, which are widely used in treating conditions like heart valve disorders, arrhythmias, and heart failure. Growing adoption of minimally invasive procedures, including transcatheter interventions, has significantly reshaped treatment approaches in modern cardiology. Continuous innovation in device engineering, biocompatible materials, and surgical techniques has further improved patient outcomes and procedural safety. In addition, expanding diagnostic capabilities and interventional cardiology infrastructure have supported wider clinical adoption. The rising global burden of cardiovascular diseases, particularly among aging populations, continues to drive sustained demand, as conditions such as valve dysfunction and rhythm disorders increasingly require advanced implantable therapeutic solutions.

The heart valves segment is expected to reach USD 15.7 billion by 2035, advancing at a CAGR of 6.1% during 2026-2035. Growth in this segment is primarily supported by the increasing incidence of valvular heart diseases, including aortic stenosis and mitral regurgitation. These conditions are strongly associated with aging populations and often require surgical or transcatheter valve replacement procedures. Rising clinical preference for advanced prosthetic valve solutions continues to support sustained segment expansion.

The hospitals segment accounted for a share of 47.8% in 2025. Hospitals remain the primary care setting for cardiac prosthetic device procedures due to the availability of advanced infrastructure, catheterization laboratories, and specialized cardiac teams. These facilities are essential for performing complex interventions such as valve replacement and pacemaker implantation. High patient inflow, coupled with access to advanced imaging and surgical technologies, continues to position hospitals as the central hub for cardiovascular treatment.

North America Cardiac Prosthetic Devices Market held a 43.1% share in 2025. The region's dominance is supported by the high burden of cardiovascular diseases, including coronary artery disease, heart failure, arrhythmia, and valvular disorders. Lifestyle-related risk factors such as obesity, hypertension, poor dietary habits, and sedentary behavior continue to contribute to disease prevalence. Strong healthcare infrastructure and advanced cardiac care capabilities further support the adoption of prosthetic cardiac devices across the region.

Prominent players operating in the global cardiac prosthetic devices industry include Abbott, Artivion, BIOTRONIK, Boston Scientific, Colibri Heart Valve, CORCYM, Edwards Lifesciences, Labcor Laboratorios, Lepu Medical, Medtronic, Meril Life Sciences, MicroPort, Pacetronix, and Venus Medtech. Companies in the cardiac prosthetic devices market are strengthening their position through continuous innovation in minimally invasive technologies and next-generation implantable solutions. A major focus remains on improving the durability, biocompatibility, and long-term clinical performance of prosthetic valves and rhythm management devices. Firms are actively investing in research and development to introduce advanced transcatheter systems and patient-specific solutions. Strategic partnerships with hospitals and cardiac centers are expanding clinical adoption and procedural training programs. Manufacturers are also enhancing global distribution networks and regulatory compliance capabilities to accelerate market entry.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiovascular diseases globally

- 3.2.1.2 Growing adoption of minimally invasive procedures

- 3.2.1.3 Technological advancements in cardiac prosthetic devices

- 3.2.1.4 Increasing geriatric population and associated cardiac disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and procedures

- 3.2.2.2 Shortage of skilled healthcare professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Advancement in leadless pacemakers and miniaturized device technology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing trend analysis (Driven by primary research)

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.11 Patent analysis (Driven by primary research)

- 3.12 Value chain analysis (Driven by primary research)

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Prosthetic heart valves

- 5.2.1 Mechanical heart valves

- 5.2.2 Tissue heart valves

- 5.2.3 Transcatheter heart valves (TAVR/TMVR)

- 5.3 Pacemakers

- 5.3.1 Implantable pacemakers

- 5.3.1.1 Single-chamber pacemakers

- 5.3.1.2 Dual-chamber pacemakers

- 5.3.1.3 Biventricular/CRT pacemakers

- 5.3.2 External pacemakers

- 5.3.1 Implantable pacemakers

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Specialty cardiac centers

- 6.4 Ambulatory surgical centers

- 6.5 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott

- 8.2 Artivion

- 8.3 BIOTRONIK

- 8.4 Boston Scientific

- 8.5 Colibri Heart Valve

- 8.6 CORCYM

- 8.7 Edwards Lifesciences

- 8.8 Labcor Laboratorios

- 8.9 Lepu Medical

- 8.10 Medtronic

- 8.11 Meril Life Sciences

- 8.12 MicroPort

- 8.13 Pacetronix

- 8.14 Venus Medtech

心臟假體設備市場報告:按產品類型、最終用戶和地區分類(2026-2034 年)

心臟假體設備市場報告:按產品類型、最終用戶和地區分類(2026-2034 年) 全球心臟假體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球心臟假體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 心臟假體市場:2026年至2032年全球市場預測(依產品類型、手術、材料類型、適應症和最終用戶分類)

心臟假體市場:2026年至2032年全球市場預測(依產品類型、手術、材料類型、適應症和最終用戶分類) 心臟人工器官市場:依產品類型分類

心臟人工器官市場:依產品類型分類 2026年全球人工心臟設備市場報告

2026年全球人工心臟設備市場報告 心臟假體設備市場規模、佔有率和成長分析(按產品類型、材質類型、最終用途和地區分類)-2026-2033年產業預測

心臟假體設備市場規模、佔有率和成長分析(按產品類型、材質類型、最終用途和地區分類)-2026-2033年產業預測 心臟假體設備市場(依產品、國家及地區)-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測

心臟假體設備市場(依產品、國家及地區)-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測