|

市場調查報告書

商品編碼

2071340

直流電動車快速充電站市場機會、成長要素、產業趨勢分析及2026-2035年預測DC Fast Electric Vehicle Charging Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

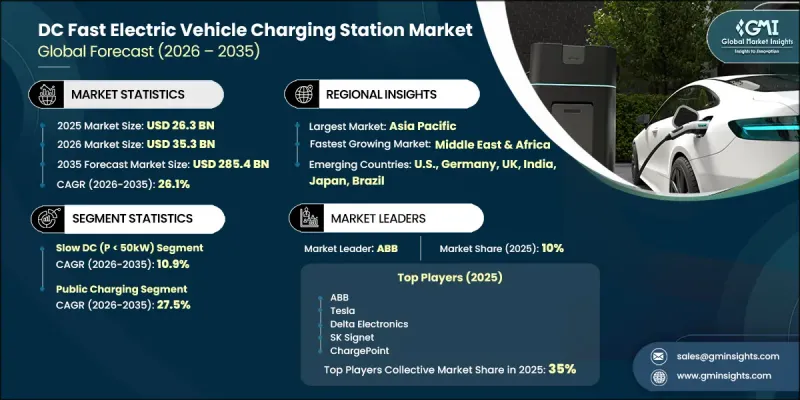

全球直流電動車快速充電站市場預計到 2025 年將達到 263 億美元,到 2035 年將以 26.1% 的複合年成長率成長至 2854 億美元。

市場成長主要受三大因素驅動:對30分鐘以內超快充電週期的需求不斷成長;主要經濟體政府主導的基礎建設義務;以及電力電子技術進步帶來的高功率充電系統成本持續下降。此外,企業淨零排放承諾和國家脫碳目標正將直流快速充電基礎設施視為一項策略性合規投資,從而顯著縮短部署時間。電動車在乘用車、商用車和大眾運輸領域的日益普及,並持續推動高容量充電網路的需求。城際高速公路、物流走廊和人口密集都市區基礎設施缺口的彌補需求,正在推動大規模資本投資。碳化矽(SiC)半導體、新一代電力電子技術和雙向充電系統的技術進步,在提高效率的同時,也降低了單位充電成本。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 263億美元 |

| 預計金額 | 2854億美元 |

| 複合年成長率 | 26.1% |

低速直流充電市場(定義為功率低於 50 kW 的系統)預計到 2025 年將佔據 9.4% 的市佔率。該市場主要服務於老一代電動車平台和低容量電動出行應用,在這些應用中,適中的充電速度足以滿足日常營運需求。在電動車生態系統仍在發展中的地區以及對超快充電功能需求不高的車型類別中,低速直流充電的普及正在逐步推進,從而支撐著該市場穩步但相對緩慢的成長。

預計到2025年,公共充電市場規模將達到174億美元,佔市場佔有率的66.3%,並將在2035年之前以27.5%的複合年成長率成長。該市場主要包括沿高速公路、大都會圈充電樞紐、與公共交通直接相連的設施以及所有電動車用戶均可使用的商業停車場等常用充電站。這一成長主要受越來越多沒有家用充電設施的電動車車主的推動,而共用充電基礎設施對於滿足日常出行需求仍然至關重要,尤其是在人口密集的都市區。

預計到2025年,北美市場佔有率將達到3.4%,隨著聯邦和州級基礎設施發展計畫從規劃階段進入大規模部署階段,預計該市場將快速成長。政府為支持全國充電基礎設施擴張而製定的資金籌措框架,強制要求在主要交通幹線沿線安裝高功率直流快速充電站,從而加強全部區域的長期基礎設施建設。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 原物料供應及採購分析

- 生產能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 價格趨勢分析

- 依輸出類型

- 按地區

- 人工智慧和生成式人工智慧對市場(核心解決方案)的影響

- 利用人工智慧最佳化生產

- 預測性維護和故障檢測

- 新機會和趨勢

- 投資分析及未來展望

- 永續發展措施與工業4.0的融合

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 主要進展

- 重要合作夥伴關係和合作

- 併購主要趨勢

- 產品創新和新產品發布

- 市場擴大策略

- 競爭定位矩陣

第5章 市場規模及預測:以產量計算,2022-2035年

- 低速直流(小於50kW)

- 高速直流(50kW 至 150kW)

- 一級 - 超高速直流(150kW 至 350kW)

- 二級 - 超高速直流(350kW 或以上)

第6章 市場規模與預測:依應用領域分類,2022-2035年

- 民眾

- 半公開

- 個人/車隊

第7章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 挪威

- 德國

- 法國

- 荷蘭

- 英國

- 瑞典

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 新加坡

- 中東和非洲

- 沙烏地阿拉伯

- UAE

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

第8章:公司簡介

- ABB

- Alpitronic

- Blink Charging

- ChargePoint

- Delta Electronics

- Eaton

- EON

- EVBox

- EVgo

- Fortum

- GreenWay Infrastructure

- Kempower

- Leviton Manufacturing

- Schneider Electric

- Siemens

- SK Signet

- Starvo Global Energi

- Tesla

- Tritium

- Volta

- Wallbox

The Global DC Fast Electric Vehicle Charging Station Market was valued at USD 26.3 billion in 2025 and is estimated to grow at a CAGR of 26.1% to reach USD 285.4 billion by 2035.

Market growth is reinforced by three core forces: rising demand for ultra-fast charging cycles under 30 minutes, government-backed infrastructure deployment mandates across major economies, and continuous reductions in high-power charging system costs driven by advancements in power electronics. In addition, corporate net-zero commitments and national decarbonization targets are accelerating the positioning of DC fast charging infrastructure as a strategic compliance-driven investment, significantly shortening deployment timelines. Expanding EV penetration across passenger vehicles, commercial fleets, and public transportation is generating sustained demand for high-capacity charging networks. The need to bridge infrastructure gaps across intercity highways, logistics corridors, and dense urban regions is encouraging large-scale capital investment. Technological progress in silicon carbide (SiC) semiconductors, next-generation power electronics, and bidirectional charging systems is further enhancing efficiency while reducing per-unit charging costs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26.3 Billion |

| Forecast Value | $285.4 Billion |

| CAGR | 26.1% |

The slow DC charging segment, defined by systems below 50 kW, accounted for 9.4% share in 2025. This segment mainly supports earlier-generation EV platforms and lower-capacity electric mobility applications, where moderate charging speeds remain operationally sufficient. Its adoption continues in regions with evolving EV ecosystems and in vehicle categories that do not require ultra-fast charging capabilities, supporting steady but comparatively slower growth.

The public DC fast charging segment held a 66.3% share, representing USD 17.4 billion in 2025, and is projected to grow at a CAGR of 27.5% through 2035. This segment includes high-traffic charging installations located along highways, in metropolitan charging hubs, at transit-oriented facilities, and within commercial parking environments accessible to all EV users. Growth is strongly supported by the increasing number of EV owners who lack private home charging access, particularly in densely populated urban settings where shared charging infrastructure remains essential for daily mobility needs.

North America DC Fast Electric Vehicle Charging Station Market accounted for 3.4% share in 2025 and is expected to witness strong future acceleration as federal and state-level infrastructure initiatives shift from planning stages to large-scale deployment. Government funding frameworks supporting nationwide charging expansion are mandating high-power DC fast charging installations along key transportation routes, reinforcing long-term infrastructure buildout across the region.

Major players operating in the Global DC Fast Electric Vehicle Charging Station Market include ABB, ChargePoint, Tesla, Alpitronic, SK Signet, Delta Electronics, Blink Charging, Eaton, EVBox, Leviton Manufacturing, and Siemens. Companies in the DC Fast Electric Vehicle Charging Station Market are prioritizing large-scale expansion of high-power charging networks through strategic public-private partnerships to secure site access and accelerate deployment timelines. Many players are investing heavily in next-generation ultra-fast charging technologies supported by silicon carbide (SiC) semiconductors to improve efficiency and reduce charging duration. Firms are also focusing on interoperability and roaming agreements to ensure seamless cross-network charging experiences for EV users. Geographic expansion strategies into high-growth emerging EV markets are being supported by localized manufacturing and regional partnerships. Additionally, companies are strengthening long-term competitiveness through vertical integration of software platforms for energy management, predictive maintenance, and real-time load balancing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Power output trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Price trend analysis (USD/Unit) (Driven by primary research)

- 3.7.1 By power output

- 3.7.2 By Region

- 3.8 Impact of AI & Generative AI on the market (Core Solution)

- 3.8.1 AI-Driven production optimization

- 3.8.2 Predictive maintenance & fault detection

- 3.9 Emerging opportunities & trends

- 3.10 Investment analysis & future prospects

- 3.11 Sustainability initiatives & industry 4.0 integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Key developments

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive positioning matrix

Chapter 5 Market Size and Forecast, By power output, 2022 - 2035 (Units & USD Million)

- 5.1 Key trends

- 5.2 Slow DC (P < 50kW)

- 5.3 Fast DC (50kW ≤ P < 150kW)

- 5.4 Level 1 - Ultra-fast DC(150kW ≤ P < 350kW)

- 5.5 Level 2 - Ultra-fast DC (P ≥ 350kW)

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (Units & USD Million)

- 6.1 Key trends

- 6.2 Public

- 6.3 Semi-public charging

- 6.4 Private/fleet

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (Units & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Norway

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Netherlands

- 7.3.5 UK

- 7.3.6 Sweden

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Singapore

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Alpitronic

- 8.3 Blink Charging

- 8.4 ChargePoint

- 8.5 Delta Electronics

- 8.6 Eaton

- 8.7 EON

- 8.8 EVBox

- 8.9 EVgo

- 8.10 Fortum

- 8.11 GreenWay Infrastructure

- 8.12 Kempower

- 8.13 Leviton Manufacturing

- 8.14 Schneider Electric

- 8.15 Siemens

- 8.16 SK Signet

- 8.17 Starvo Global Energi

- 8.18 Tesla

- 8.19 Tritium

- 8.20 Volta

- 8.21 Wallbox

電動車充電站和直流快速充電器市場預測至2034年-全球分析(按充電類型、應用、組件、冷卻方式、並聯型連接、所有權模式、最終用戶和地區分類)

電動車充電站和直流快速充電器市場預測至2034年-全球分析(按充電類型、應用、組件、冷卻方式、並聯型連接、所有權模式、最終用戶和地區分類) 直流快速充電市場:市場規模、佔有率和趨勢分析(按連接器、充電基礎設施、額定輸出、應用和地區分類),細分市場預測(2026-2033 年)

直流快速充電市場:市場規模、佔有率和趨勢分析(按連接器、充電基礎設施、額定輸出、應用和地區分類),細分市場預測(2026-2033 年) 直流快速充電站市場規模、佔有率及成長分析(按充電基礎設施、充電方式、最終用戶和地區分類)-2026-2033年產業預測

直流快速充電站市場規模、佔有率及成長分析(按充電基礎設施、充電方式、最終用戶和地區分類)-2026-2033年產業預測 全球直流電動車快速充電站市場

全球直流電動車快速充電站市場 直流快速充電站市場,按類型、安裝類型、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

直流快速充電站市場,按類型、安裝類型、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測