|

市場調查報告書

商品編碼

2071328

廚房水龍頭市場商機、成長要素、產業趨勢分析及2026-2035年預測。Kitchen Faucets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

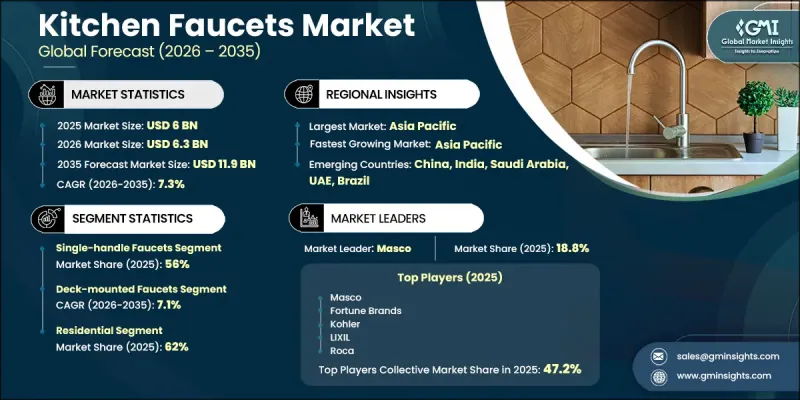

據估計,到 2025 年,全球廚房水龍頭市場價值將達到 60 億美元,到 2035 年將以 7.3% 的複合年成長率成長至 119 億美元。

市場擴張的促進因素包括:成熟經濟體穩定的住宅更換需求、快速都市化地區不斷成長的新安裝需求,以及消費者對價格更高的高階高科技水龍頭設計的明顯偏好。廚房水龍頭通常屬於半必需的裝修類別,其更換往往更受磨損、設計過時或功能下降等因素驅動,而非純粹的經濟因素,這賦予了該行業強大的結構穩定性。即使在宏觀經濟高度不確定性時期,也能確保持續的基本需求。與更具選擇性的住宅裝修領域不同,廚房水龍頭的更換需求往往不受經濟週期的影響,從而支撐了其長期韌性。此外,持續的產品創新,包括智慧功能、節水性能的提升和表面處理的改進,推高了平均售價,確保銷售成長持續超過銷售成長。都市化,尤其是在新興市場,透過新建住宅和初始安裝進一步推動了需求成長。總體而言,該市場既受益於成熟地區的匯兌需求,也受益於開發中國家的主導需求,預計在整個預測期內將保持平衡和永續的成長軌跡。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 60億美元 |

| 預測金額 | 119億美元 |

| 複合年成長率 | 7.3% |

預計到2025年,單把手水龍頭將佔據56%的市場佔有率,並預計在2035年之前以7.8%的複合年成長率成長,成為成長最快的產品類型。該細分市場的需求主要得益於其易用性、安裝簡便以及與現代緊湊型廚房佈局的兼容性。單把手水龍頭採用單一機制即可有效控制水溫和水流,因此在住宅和商用都很受歡迎。觸控操作和動作感測器控制等先進功能的日益普及也進一步提升了其受歡迎程度,因為這些功能與單把手設計相得益彰。由於便利性和空間利用率在現代廚房設計中仍然至關重要,預計該細分市場將在整個預測期內保持強勁的成長勢頭。

到2025年,檯面式水龍頭市佔率將達到84%。這種安裝方式之所以能保持主導地位,是因為它與標準廚房水槽設計相容性強,且在住宅和商業環境中都易於安裝。其靈活的設計應用和涵蓋入門級到高級產品等不同價位的豐富產品線也為其廣受歡迎提供了支援。在消費者認知度不斷提高以及翻新和新建項目需求持續成長的推動下,檯面式水龍頭市場正不斷主導地位。

預計到2025年,北美廚房水龍頭市佔率將達到29%,並在2035年之前以7.2%的複合年成長率成長。美國憑藉其龐大的住宅安裝基礎和持續的廚房翻新活動,仍然是區域需求的主要驅動力。由於基礎設施老化和持續的住宅維修投資,更換需求仍然強勁。完善的分銷網路和成熟的零售通路進一步提高了全部區域的供應量。加拿大也透過持續的住宅開發和主要都市區多用戶住宅的擴張,推動了市場成長,從而滿足了不斷成長的廚房水龍頭安裝需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 價格趨勢

- 對過去價格趨勢的分析

- 定價策略:按業務類型分類

- 監理框架

- 美國法規:WaterSense計畫、無鉛強制令(《安全飲用水法》)

- 歐洲法規:歐盟建築產品法規、REACH(六價鉻)

- 亞太地區的法規:印度 BIS 標準、中國的 GB 標準、日本的 JIS 標準。

- 區域節水標準和認證(WaterSense、WELS、WRAS、歐盟生態標籤)

- 建築規範和管道標準對產品設計的影響(IPC、UPC、EN 817)

- 波特五力分析

- PESTLE分析

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧正在改變傳統的經營模式。

- 按客戶群分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 消費行為分析

- 購買模式

- 偏好分析

- 不同地區的消費行為差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 單把手水龍頭

- 標準型/固定單把手

- 下拉式單把手

- 拉出式單把手

- 單把手旋轉出水嘴

- 雙把手水龍頭

- 中置雙把手

- 寬口雙把手

- 橋式雙把手

第6章 市場估計與預測:依材料分類,2022-2035年

- 不銹鋼

- 黃銅

- 鉻鎳合金

- 青銅/銅

- 塑膠/聚合物

- 其他材料(鋅合金、複合材料等)

第7章 市場估計與預測:依技術分類,2022-2035年

- 手動廚房水龍頭

- 電子和自動廚房水龍頭

- 感應式/紅外線(非接觸式)廚房水龍頭

- 觸控式廚房水龍頭

- 聲控廚房水龍頭

第8章 市場估算與預測:依安裝類型分類,2022-2035年

- 檯面式水龍頭

- 壁掛式水龍頭

第9章 市場估計與預測:依價格區間分類,2022-2035年

- 價格低廉(50 美元以下)

- 中價位(50美元至199美元)

- 價格區間較高(200-499 美元)

- 高級版(超過 500 美元)

第10章 市場估價與預測:依最終用戶分類,2022-2035年

- 住宅

- 商業

- 飯店業

- 衛生保健

- 辦公大樓

- 零售及餐飲服務業

- 教育機構

- 產業

第11章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 公司網站

- 離線

- 超級市場/大賣場

- 專業零售店

- 其他(例如獨立經營零售商店)

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第13章:公司簡介

- 全球主要公司

- Fortune Brands

- Hansgrohe

- Kohler

- LIXIL

- Masco

- Roca Group

- TOTO

- 當地公司

- Arrow Home Group

- Cera Sanitaryware

- FM Mattsson

- Hindware(HSIL Ltd.)

- Huida Sanitary Ware

- Oras Group

- Vitra(Eczacibasi Group)

- 新興企業和專業公司

- Bravat

- Chicago Faucets

- Fantini Rubinetti

- Gessi

- T&S Brass and Bronze Works

- THG Paris

- Zucchetti Rubinetteria

The Global Kitchen Faucets Market was valued at USD 6 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 11.9 billion by 2035.

Market expansion is driven by a combination of steady residential replacement activity in established economies, rising initial installation demand in rapidly urbanizing regions, and a clear shift toward premium and technology-enabled faucet designs that command higher price realization. The industry demonstrates strong structural stability, as kitchen faucets typically fall into a semi-essential renovation category where replacement is triggered more by wear, design obsolescence, or functional decline rather than purely economic sentiment. This creates a consistent baseline demand even during periods of macroeconomic uncertainty. Unlike more discretionary home renovation segments, kitchen faucet replacement tends to remain steady across cycles, supporting long-term resilience. Additionally, ongoing product innovation, including smart functionality, improved water efficiency, and enhanced finishes, is contributing to higher average selling prices, ensuring revenue growth continues to outpace unit expansion. Increasing urbanization, especially in emerging economies, is further reinforcing demand through new housing development and first-time installations. Overall, the market is benefiting from both replacement-driven consumption in mature regions and expansion-led demand in developing economies, creating a balanced and sustainable growth trajectory across the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6 Billion |

| Forecast Value | $11.9 Billion |

| CAGR | 7.3% |

Single-handle faucets accounted for 56% share in 2025 and is projected to grow at a CAGR of 7.8% through 2035, making it the fastest-growing product category. Demand for this segment is supported by ease of use, simplified installation, and compatibility with modern compact kitchen layouts. The design allows efficient temperature and water flow control through a single mechanism, making it widely preferred across residential and commercial applications. Its adoption is also reinforced by increasing integration of advanced features such as touch and motion-based controls, which align well with single-handle configurations. As modern kitchen design continues to prioritize convenience and space efficiency, this segment is expected to maintain strong momentum throughout the forecast period.

The deck-mounted faucets segment held an 84% share in 2025. This installation type continues to lead due to its broad compatibility with standard kitchen sink designs and ease of installation across both residential and commercial environments. Its widespread use is supported by flexible design applications and availability across multiple price points, ranging from entry-level to premium product categories. The segment benefits from established consumer familiarity and consistent demand across renovation and new construction activities, reinforcing its leading position in the market structure.

North America Kitchen Faucets Market accounted for 29% share in 2025 and is expected to grow at a CAGR of 7.2% through 2035. The United States remains the primary contributor to regional demand, supported by a large installed base of residential housing and ongoing kitchen renovation activity. Replacement demand remains steady due to aging infrastructure and continuous home improvement investments. Strong distribution networks and well-established retail channels further support product accessibility across the region. Canada is also contributing to market growth through sustained residential development activity and multi-family housing expansion in major urban centers, supporting incremental demand for kitchen faucet installations.

Key companies operating in the global kitchen faucets market include Masco Corporation, LIXIL Corporation, Fortune Brands Home & Security, Roca Group, and Kohler Co. Companies operating in the kitchen faucets market are focusing on several strategic initiatives to strengthen their competitive position and expand market share. Product innovation remains central, with manufacturers introducing advanced faucet designs that incorporate water efficiency, durable materials, and smart functionality. Investments in design aesthetics and premium finishes are helping brands differentiate their offerings in an increasingly competitive environment. Companies are also expanding their presence across digital retail channels and strengthening partnerships with distributors, contractors, and home improvement retailers to improve market reach. Geographic expansion into high-growth regions is another key focus area, supported by localized product development strategies. In addition, mergers, acquisitions, and portfolio diversification are enabling firms to enhance their technological capabilities and broaden their product offerings, while continuous research and development investments are ensuring long-term competitiveness and sustained brand positioning.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Valve mechanism

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 Price range

- 2.2.7 End users

- 2.2.8 Distribution channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Price trends

- 3.4.1 Historical price trend analysis

- 3.4.2 Pricing strategy by player type

- 3.5 Regulatory framework

- 3.5.1 US Regulations: WaterSense Program, Lead-Free Mandates (Safe Drinking Water Act)

- 3.5.2 European Regulations: EU Construction Products Regulation, REACH (Hexavalent Chromium)

- 3.5.3 Asia Pacific Regulations: BIS (India), China GB Standards, Japan JIS

- 3.5.4 Water Efficiency Standards & Certifications by Region (WaterSense, WELS, WRAS, EU Ecolabel)

- 3.5.5 Building Codes & Plumbing Standards Impact on Product Design (IPC, UPC, EN 817)

- 3.6 Porter's five forces analysis

- 3.7 PESTEL analysis

- 3.8 Trade data analysis (based on paid database) (HS Code: 8481.80)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of traditional business models

- 3.9.2 GenAI use cases & adoption roadmap by customer segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Future market trends

- 3.11 Technology and innovation landscape

- 3.11.1 Current technological trends

- 3.11.2 Emerging technologies

- 3.12 Consumer behavior analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Single-handle faucets

- 5.2.1 Standard/stationary single handle

- 5.2.2 Pull-down single-handle

- 5.2.3 Pull-out single-handle

- 5.2.4 Swivel spout single-handle

- 5.3 Dual-handle faucets

- 5.3.1 Centerset dual handle

- 5.3.2 Widespread dual handle

- 5.3.3 Bridge dual-handle

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Stainless steel

- 6.3 Brass

- 6.4 Chrome/nickel alloy

- 6.5 Bronze/copper

- 6.6 Plastic/polymer

- 6.7 Others (zinc alloys, composite materials etc.)

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Manual kitchen faucets

- 7.3 Electronic/automatic kitchen faucets

- 7.3.1 Sensor/infrared-activated (touchless) kitchen faucets

- 7.3.2 Touch-activated kitchen faucets

- 7.3.3 Voice-activated kitchen faucets

Chapter 8 Market Estimates & Forecast, By Mounting Type, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Deck-mounted faucets

- 8.3 Wall-mounted faucets

Chapter 9 Market Estimates & Forecast, By Price Range, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Low (under US$ 50)

- 9.3 Medium (US$ 50 - US$ 199)

- 9.4 High (US$ 200 - US$ 499)

- 9.5 Premium (US$ 500 and above)

Chapter 10 Market Estimates & Forecast, By End Users, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Residential

- 10.3 Commercial

- 10.3.1 Hospitality

- 10.3.2 Healthcare

- 10.3.3 Office & corporate buildings

- 10.3.4 Retail & food service establishments

- 10.3.5 Educational institutions

- 10.4 Industrial

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 E-commerce

- 11.2.2 Company websites

- 11.3 Offline

- 11.3.1 Supermarkets/hypermarket

- 11.3.2 Specialty retail stores

- 11.3.3 Others (independent retailer etc.)

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Key Players

- 13.1.1 Fortune Brands

- 13.1.2 Hansgrohe

- 13.1.3 Kohler

- 13.1.4 LIXIL

- 13.1.5 Masco

- 13.1.6 Roca Group

- 13.1.7 TOTO

- 13.2 Regional Players

- 13.2.1 Arrow Home Group

- 13.2.2 Cera Sanitaryware

- 13.2.3 FM Mattsson

- 13.2.4 Hindware (HSIL Ltd.)

- 13.2.5 Huida Sanitary Ware

- 13.2.6 Oras Group

- 13.2.7 Vitra (Eczacibasi Group)

- 13.3 Emerging/Niche Specialists

- 13.3.1 Bravat

- 13.3.2 Chicago Faucets

- 13.3.3 Fantini Rubinetti

- 13.3.4 Gessi

- 13.3.5 T&S Brass and Bronze Works

- 13.3.6 THG Paris

- 13.3.7 Zucchetti Rubinetteria

水龍頭市場機會、成長要素、產業趨勢分析及2026-2035年預測。

水龍頭市場機會、成長要素、產業趨勢分析及2026-2035年預測。 電動水龍頭市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、安裝類型、最終用戶、材料類型、分銷管道、地區和競爭格局分類,2021-2031年

電動水龍頭市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、安裝類型、最終用戶、材料類型、分銷管道、地區和競爭格局分類,2021-2031年 2026-2030年全球住宅水龍頭市場

2026-2030年全球住宅水龍頭市場 水龍頭市場規模、佔有率、趨勢和預測:按類型、應用、技術、分銷管道、最終用戶和地區分類(2026-2034 年)

水龍頭市場規模、佔有率、趨勢和預測:按類型、應用、技術、分銷管道、最終用戶和地區分類(2026-2034 年) 水龍頭市場:2026-2032年全球市場預測(依產品類型、把手類型、技術水準、材料、通路、最終用途領域及應用產業分類)

水龍頭市場:2026-2032年全球市場預測(依產品類型、把手類型、技術水準、材料、通路、最終用途領域及應用產業分類) 全球水龍頭市場規模、佔有率、趨勢和成長分析報告(2026-2034年)住宅水龍頭市場:依產品類型、材質、安裝方式、技術、應用和分銷管道分類-2026-2032年全球預測計量水龍頭市場:依產品類型、安裝方式、材料、最終用戶和分銷管道分類,全球預測(2026-2032年)

全球水龍頭市場規模、佔有率、趨勢和成長分析報告(2026-2034年)住宅水龍頭市場:依產品類型、材質、安裝方式、技術、應用和分銷管道分類-2026-2032年全球預測計量水龍頭市場:依產品類型、安裝方式、材料、最終用戶和分銷管道分類,全球預測(2026-2032年) 2035年即熱式水龍頭市場分析及預測:按類型、產品類型、技術、組件、應用、材質、安裝類型、最終用戶和功能分類即熱式水龍頭市場:按產品類型、過濾器類型、安裝類型、溫度輸出、分銷管道、應用領域分類 - 全球預測 2026-2032

2035年即熱式水龍頭市場分析及預測:按類型、產品類型、技術、組件、應用、材質、安裝類型、最終用戶和功能分類即熱式水龍頭市場:按產品類型、過濾器類型、安裝類型、溫度輸出、分銷管道、應用領域分類 - 全球預測 2026-2032