|

市場調查報告書

商品編碼

2071311

雜交種子市場機會、成長要素、產業趨勢分析及2025-2036年預測Hybrid Seed Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2036 |

||||||

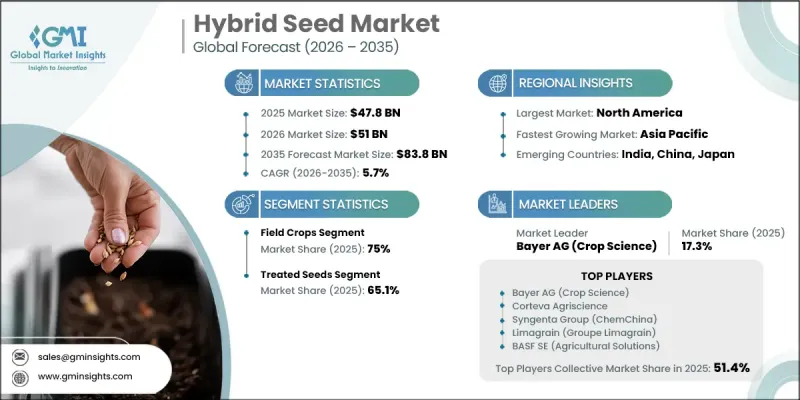

全球雜交種子市場預計到 2025 年將達到 478 億美元,年複合成長率為 5.7%,到 2035 年將達到 838 億美元。

人口成長導致全球糧食需求增加,精密農業工具的廣泛應用,以及亞洲、非洲和中東各國主導加強對糧食安全的投入,共同推動了這項擴張。在公私合營,小規模農戶農業系統的改進,使得認證雜交品種的獲取管道擴展到了傳統商業農業區之外。透過控制雜交以提取雜種優勢而生產的雜交種子,能夠持續提供更高的產量、更優異的均勻性、更強的抗病性和更強的環境壓力耐受性。機械化程度的提高、精準灌溉技術的引入以及數位農業解決方案的進步,進一步擴大了雜交種子在以往投入較低的農業系統中的滲透率。

到2025年,田間作物領域將佔市場佔有率的75%,成為該行業的主要收入來源。預計到2035年,該領域將以4.9%的複合年成長率成長,這主要得益於全球對玉米、飼料、小麥、向日葵、高粱和菜籽等關鍵作物的持續需求,這些作物仍然是世界糧食、飼料和工業供應體系的核心。

預計到2025年,處理種子市佔率將達到65.1%,並在2035年之前以6.9%的複合年成長率成長。這一成長主要得益於生產者日益認知到,在氣候變遷日益嚴峻的背景下,種子層面的保護是一種經濟有效的風險緩解策略。由於處理成本相對較低,而作物生長初期可避免的潛在經濟損失卻相對較小,因此其成本效益結構依然十分有利,這也促使處理種子在不同的農業系統和地區得到廣泛應用。

預計到2025年,北美雜交種子市佔率將達到27%,並在2035年之前以4%的複合年成長率成長。美國在該地區市場佔據主導地位,這得益於玉米帶和北部平原等主要農業區大規模種植玉米、大豆和菜籽。市場結構已高度成熟,主要作物的雜交種子普及率已超過99%,因此競爭重點正從擴大普及率轉向性狀創新、產量最佳化以及數位化農業的融合。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 高產作物的需求增加

- 引進先進的農業方法

- 世界人口不斷成長,糧食需求也不斷擴大。

- 產業潛在風險與挑戰

- 混合子高成本

- 受季節和氣候條件的影響

- 市場機遇

- 新興農業經濟體的業務擴張

- 培育抗氣候變遷的雜交品種

- 特種作物種子需求不斷成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTLE分析

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按作物類型

- 未來市場趨勢

- 專利趨勢

- 貿易統計

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- LATAM

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依作物類型分類,2022-2035年

- 大田作物

- 穀類

- 玉米(Maine)

- 米

- 粟

- 高粱

- 油籽

- 向日葵

- 油菜籽(菜籽)

- 紅花

- 纖維作物

- 棉布

- 豆子

- 鴿子 P

- 鷹嘴豆

- 其他(飼料作物、特種穀物)

- 穀類

- 水果和蔬菜作物

- 茄科蔬菜

- 番茄

- 辣椒(胡椒)

- 茄子(Brinjal)

- 葫蘆科植物

- 黃瓜

- 西瓜

- 葫蘆科植物(葫蘆、苦瓜)

- 南瓜

- 十字花科作物

- 高麗菜

- 花椰菜

- 綠色花椰菜

- 其他物品(秋葵、綠葉蔬菜、甜瓜)

- 茄科蔬菜

第6章 市場估計與預測:依種子處理法分類,2022-2035年

- 加工種子

- 已消毒

- 經殺蟲劑處理

- 多重防護(複合加工)

- 生物衍生治療劑

- 未經處理的種子

第7章 市場估計與預測:依時期分類,2022-2035年

- 短期(一年生作物,不到一年)

- 中期(1-5年)

- 長期(多年生作物,超過5年)

第8章 市場估算與預測:依通路分類,2022-2035年

- 直銷

- 批發商和零售商

- 線上平台

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- UAE

- 其他中東和非洲國家

第10章:公司簡介

- Bayer AG(Crop Science)

- Corteva Agriscience

- Syngenta Group(ChemChina)

- Limagrain(Groupe Limagrain)

- BASF SE(Agricultural Solutions)

- KWS SAAT SE &Co. KGaA

- Sakata Seed Corporation

- Takii &Co., Ltd.

- Enza Zaden

- Rallis India Limited(Tata Group)

- Rijk Zwaan

- Seed Co Limited

- Advanta Seeds(UPL Group)

- Nuziveedu Seeds

- East-West Seed

The Global Hybrid Seed Market was valued at USD 47.8 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 83.8 billion by 2035.

The expansion is driven by rising global food demand linked to population growth, stronger adoption of precision agriculture tools, and increasing government-led food security investments across Asia, Africa, and the Middle East. Improvements in smallholder farming systems supported by public-private seed distribution frameworks and digital agricultural extension platforms are broadening access to certified hybrid varieties beyond conventional commercial farming regions. Hybrid seeds, produced through controlled cross-pollination to express heterosis, consistently deliver higher yields, better uniformity, stronger disease resistance, and improved tolerance to environmental stress. Growing mechanization, precision irrigation adoption, and digital farming solutions are further expanding hybrid seed penetration into previously low-input agricultural systems.

The field crops segment held a 75% share in 2025, forming the core revenue base of the industry. This segment is projected to grow at a CAGR of 4.9% through 2035, supported by sustained global demand for key crops including maize, rice, wheat, sunflower, sorghum, and canola, which remain central to global food, feed, and industrial supply systems.

The treated seeds segment held a 65.1% share in 2025 and is projected to grow at a CAGR of 6.9% through 2035. This growth is driven by increasing recognition among growers that seed-level protection provides a cost-efficient risk mitigation strategy under fluctuating climatic conditions. The cost-benefit structure remains favorable, as treatment expenses are relatively low compared to the potential financial losses avoided during early crop establishment stages, making treated seeds widely adopted across diverse farming systems and geographies.

North America Hybrid Seed Market accounted for 27% share in 2025 and is expected to grow at a CAGR of 4% through 2035. The United States dominates the regional landscape, supported by large-scale cultivation of maize, soybean, and canola across major agricultural belts such as the Corn Belt and Northern Plains. Market structure is highly mature, with hybrid seed penetration already exceeding 99% in major crops, shifting competitive focus toward trait innovation, yield optimization, and digital agriculture integration rather than expansion of adoption volume.

Key players involved in the hybrid seed market include Enza Zaden, Rijk Zwaan, East-West Seed, Advanta Seeds (UPL Group), Nuziveedu Seeds, Rallis India Limited (Tata Group), and Seed Co Limited. Key strategies adopted by hybrid seed companies focus on strengthening R&D investments in trait development, disease resistance, and climate-resilient genetics. Firms are expanding digital agriculture ecosystems to integrate farm analytics, decision support tools, and precision agronomy with seed offerings. Strategic acquisitions and global breeding collaborations are enhancing germplasm diversity and accelerating product pipelines. Companies are also localizing breeding programs to adapt hybrids to regional agro-climatic conditions and consumer preferences. Integrated seed-treatment combinations are being developed to improve early-stage crop performance and risk management. In addition, partnerships with governments and agricultural institutions are expanding market access through certified seed distribution networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Crop type

- 2.2.2 Seed treatment

- 2.2.3 Duration

- 2.2.4 Distribution Channel

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for high-yield crops

- 3.2.1.2 Adoption of advanced agricultural practices

- 3.2.1.3 Rising global population and food demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with hybrid seeds

- 3.2.2.2 Dependence on seasonal and climatic conditions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging agricultural economies

- 3.2.3.2 Development of climate-resilient hybrid varieties

- 3.2.3.3 Growing demand for specialty crop seeds

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By Crop type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Crop Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Field Crops

- 5.2.1 Cereals

- 5.2.1.1 Corn (Maize)

- 5.2.1.2 Rice

- 5.2.1.3 Millet

- 5.2.1.4 Sorghum

- 5.2.2 Oilseeds

- 5.2.2.1 Sunflower

- 5.2.2.2 Rapeseed (Canola)

- 5.2.2.3 Safflower

- 5.2.3 Fiber Crops

- 5.2.3.1 Cotton

- 5.2.4 Pulses

- 5.2.4.1 Pigeon Pea

- 5.2.4.2 Chickpea

- 5.2.4.3 Others (Fodder Crops, Specialty Grains)

- 5.2.1 Cereals

- 5.3 Fruits & Vegetable Crops

- 5.3.1 Solanaceous Vegetables

- 5.3.1.1 Tomato

- 5.3.1.2 Chilli (Pepper)

- 5.3.1.3 Eggplant (Brinjal)

- 5.3.2 Cucurbits

- 5.3.2.1 Cucumber

- 5.3.2.2 Watermelon

- 5.3.2.3 Gourds (Bottle Gourd, Bitter Gourd)

- 5.3.2.4 Pumpkin & Squash

- 5.3.3 Brassicas

- 5.3.3.1 Cabbage

- 5.3.3.2 Cauliflower

- 5.3.3.3 Broccoli

- 5.3.4 Others (Okra, Leafy Vegetables, Melons)

- 5.3.1 Solanaceous Vegetables

Chapter 6 Market Estimates and Forecast, By Seed Treatment, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Treated seeds

- 6.2.1 Fungicide-treated

- 6.2.2 Insecticide-treated

- 6.2.3 Multi-protection (combined treatment)

- 6.2.4 Bio-based treatments

- 6.3 Untreated seeds

Chapter 7 Market Estimates and Forecast, By Duration, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Short-term (Annual Crops, <1 Year)

- 7.3 Medium-term (1-5 Years)

- 7.4 Long-term (Perennial Crops, ≥5 Years)

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Distributors & retailers

- 8.4 Online platforms

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Bayer AG (Crop Science)

- 10.2 Corteva Agriscience

- 10.3 Syngenta Group (ChemChina)

- 10.4 Limagrain (Groupe Limagrain)

- 10.5 BASF SE (Agricultural Solutions)

- 10.6 KWS SAAT SE & Co. KGaA

- 10.7 Sakata Seed Corporation

- 10.8 Takii & Co., Ltd.

- 10.9 Enza Zaden

- 10.10 Rallis India Limited (Tata Group)

- 10.11 Rijk Zwaan

- 10.12 Seed Co Limited

- 10.13 Advanta Seeds (UPL Group)

- 10.14 Nuziveedu Seeds

- 10.15 East-West Seed