|

市場調查報告書

商品編碼

2071286

2026 年至 2035 年住宅太陽能發電和儲能市場的商業機會、成長要素、產業趨勢和預測。Residential Solar Energy Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

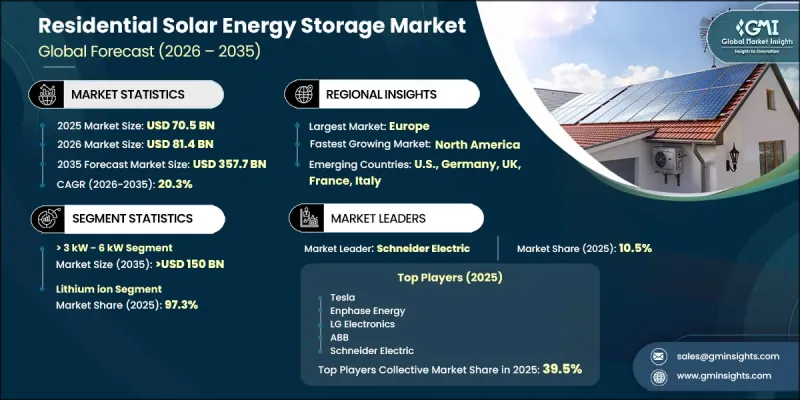

全球住宅太陽能發電和儲能市場預計到 2025 年將達到 705 億美元,並以 20.3% 的複合年成長率成長,到 2035 年將達到 3,577 億美元。

都市區和郊區家庭能源效率意識的提高以及政府對可再生能源推廣的支持,推動了市場擴張。都市化加快與獎勵性太陽能發電計畫和補貼政策的協同作用,進一步加速了住宅儲能系統的需求。此外,人們對電網可靠性和頻繁停電的擔憂日益加劇,也促使家庭採用太陽能發電與儲能結合的解決方案。屋頂太陽能發電系統滲透率的不斷提高也促進了整體應用。住宅太陽能儲能系統旨在儲存太陽能電池板產生的多餘電力以供後續使用,確保夜間、用電尖峰時段或電網故障時的不間斷供電。這些系統主要採用鋰離子電池技術,因為鋰離子電池具有高能量密度和高效率。能源管理系統和智慧監控技術的進步進一步提升了系統效能和使用者控制能力。淨計量計劃、稅收優惠和上網電價補貼等扶持性政策框架持續增強了市場的吸引力。同時,由於大規模生產和技術進步,電池成本下降,使得電池更經濟實惠,並顯著擴大了市場滲透率。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 705億美元 |

| 預測金額 | 3577億美元 |

| 複合年成長率 | 20.3% |

預計到2035年,容量在3千瓦至6千瓦之間的住宅太陽能儲能市場規模將達到1,500億美元。該細分市場成長強勁,因為它兼具成本效益和備用電源能力,即使在停電期間也能為照明和小家電等重要用電設備供電。混合逆變器系統的日益普及和安裝技術的簡化進一步推動了該容量範圍的需求,使其成為尋求可靠且擴充性儲能解決方案的住宅用戶的首選。

預計到2025年,鋰離子電池將佔據97.3%的市場佔有率,並繼續保持其在整個產業的領先地位。這一主導地位源自於其卓越的能量密度、緊湊的設計、快速充放電能力以及整體系統效率。大規模生產和持續的技術改進降低了成本,使其價格更加親民,進一步提升了市場滲透率。因此,鋰離子技術仍然是全球住宅儲能應用的首選。

預計到2025年,美國住宅太陽能儲能市場規模將達到184億美元,主要得益於以脫碳和提高能源效率為重點的強大政策框架。政府鼓勵採用清潔能源的獎勵,以及家庭對永續能源解決方案日益成長的認知,共同推動了市場的穩定成長。住宅太陽能裝置的普及以及相關法規的訂定,正在推動全美範圍內對住宅能源儲存系統的持續需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 原物料供應及採購分析

- 生產能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 監理情勢

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 成本結構分析:住宅太陽能發電與儲能

- 新機會與趨勢

- 數位化和物聯網整合

- 未開發市場和應用領域的成長

- 投資分析及未來展望

- 價格趨勢分析

- 按地區

- 額定功率

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧最佳化生產

- 預測性維護和故障檢測

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 按公司規模進行基準測試

- 排名分類標準與遴選標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場規模及預測:額定功率,2022-2035年

- 3千瓦或以下

- >3 kW~6 kW

- >6 kW

第6章 市場規模及預測:依技術分類,2022-2035年

- 鋰離子

- 鉛酸電池

第7章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 瑞士

- 奧地利

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- UAE

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第8章:公司簡介

- ABB

- Eaton

- EnerSys

- Enphase Energy

- Fluence

- Honeywell

- Huawei

- iNVERGY Ltd.

- Johnson Controls

- Leclanche

- LG Electronics

- Maxwell Energy

- Primus Power

- PURE Energy

- Saft

- SAMSUNG SDI

- Schneider Electric

- SolarEdge Technologies

- Toshiba

- Uniper

The Global Residential Solar Energy Storage Market was valued at USD 70.5 billion in 2025 and is estimated to grow at a CAGR of 20.3% to reach USD 357.7 billion by 2035.

Market expansion is driven by increasing consumer awareness regarding energy efficiency across urban and suburban households, along with supportive government initiatives promoting renewable energy adoption. Expanding urbanization, coupled with incentive-based solar programs and subsidies, is further accelerating demand for residential storage systems. In addition, rising concerns over grid reliability and the growing frequency of power outages are encouraging households to integrate solar-plus-storage solutions. The increasing penetration of rooftop solar installations is also strengthening overall adoption. Residential solar energy storage systems are designed to store surplus electricity generated from solar panels for later use, ensuring uninterrupted power supply during nighttime, peak demand hours, or grid disruptions. These systems primarily rely on lithium-ion battery technology due to its high energy density and efficiency. Advancements in energy management systems and smart monitoring technologies are further improving system performance and user control. Supportive policy frameworks, including net metering mechanisms, tax incentives, and feed-in tariff structures, continue to enhance market attractiveness. At the same time, declining battery costs driven by large-scale manufacturing and technological advancements are significantly improving affordability and expanding market penetration.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.5 Billion |

| Forecast Value | $357.7 Billion |

| CAGR | 20.3% |

The residential solar energy storage market for the > 3 kW - 6 kW capacity range is projected to reach USD 150 billion by 2035. This segment is gaining strong traction as it provides an optimal balance between cost efficiency and power backup capability, enabling households to support essential electrical loads such as lighting and small appliances during outages. Growing adoption of hybrid inverter systems and simplified installation technologies is further enhancing demand within this capacity range, making it a preferred choice among residential users seeking reliable and scalable energy storage solutions.

The lithium-ion battery segment accounted for 97.3% share in 2025, maintaining a dominant position across the industry. Its leadership is attributed to superior energy density, compact design, rapid charging and discharging capabilities, and overall system efficiency. Increasing affordability driven by mass production scale and ongoing technological improvements has further strengthened its market penetration. As a result, lithium-ion technology continues to remain the preferred choice for residential energy storage applications worldwide.

United States Residential Solar Energy Storage Market was valued at USD 18.4 billion in 2025, supported by strong policy frameworks focused on decarbonization and energy efficiency. Government incentives promoting clean energy adoption, combined with increasing household awareness of sustainable energy solutions, are contributing to steady market growth. The expansion of solar installations across residential properties, along with supportive regulatory mechanisms, continues to reinforce demand for residential energy storage systems across the country.

Major companies operating in the global residential solar energy storage industry include Tesla, Enphase Energy, SolarEdge Technologies, Schneider Electric, ABB, LG Electronics, Samsung SDI, Huawei, Eaton, Johnson Controls, Fluence, Toshiba, Saft, EnerSys, Leclanche, Primus Power, Pure Energy, Maxwell Energy, iNVERGY Ltd., Uniper, and Honeywell. Companies in the residential solar energy storage market are focusing on strategic initiatives to strengthen their market presence and enhance competitive positioning. A major focus is on technological innovation, with firms developing high-efficiency battery systems, advanced inverters, and integrated energy management platforms. Cost optimization through large-scale production and supply chain efficiency improvements is also a key strategy to enhance affordability and expand adoption. Companies are increasingly investing in lithium-ion technology advancements to improve battery life, performance, and safety. Expansion of distribution networks and partnerships with solar installers and utility providers is helping improve market reach. Digital integration, including smart monitoring and AI-based energy optimization, is being adopted to enhance user experience and system efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Power rating trends

- 2.1.3 Technology trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of residential solar energy storage

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.9.1 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

- 3.11 Price trend analysis (USD/MW) (Driven by Primary Research)

- 3.11.1 By region (Driven by Primary Research)

- 3.11.2 By power rating (Driven by Primary Research)

- 3.12 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.12.1 AI-Driven production optimization (Driven by Primary Research)

- 3.12.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 3 kW

- 5.3 > 3 kW - 6 kW

- 5.4 > 6 kW

Chapter 6 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 Lithium ion

- 6.3 Lead acid

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Italy

- 7.3.4 Spain

- 7.3.5 UK

- 7.3.6 Switzerland

- 7.3.7 Austria

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Eaton

- 8.3 EnerSys

- 8.4 Enphase Energy

- 8.5 Fluence

- 8.6 Honeywell

- 8.7 Huawei

- 8.8 iNVERGY Ltd.

- 8.9 Johnson Controls

- 8.10 Leclanche

- 8.11 LG Electronics

- 8.12 Maxwell Energy

- 8.13 Primus Power

- 8.14 PURE Energy

- 8.15 Saft

- 8.16 SAMSUNG SDI

- 8.17 Schneider Electric

- 8.18 SolarEdge Technologies

- 8.19 Toshiba

- 8.20 Uniper

太陽能、風能和儲能混合發電廠市場預測至2034年—按組件、技術整合、儲能方法、所有權和營運模式、應用和地區分類的全球分析

太陽能、風能和儲能混合發電廠市場預測至2034年—按組件、技術整合、儲能方法、所有權和營運模式、應用和地區分類的全球分析 太陽能儲能電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、安裝方式、應用、地區和競爭格局分類,2021-2031年

太陽能儲能電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、安裝方式、應用、地區和競爭格局分類,2021-2031年 太陽能儲能市場商機、成長要素、產業趨勢分析及2026-2035年預測。

太陽能儲能市場商機、成長要素、產業趨勢分析及2026-2035年預測。 2026-2030年全球住宅太陽能儲能市場

2026-2030年全球住宅太陽能儲能市場 2026年全球太陽能電池儲能市場報告

2026年全球太陽能電池儲能市場報告 住宅太陽能儲能:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

住宅太陽能儲能:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 全球鋰離子住宅太陽能能源儲存市場全球鋰離子太陽能能源儲存市場

全球鋰離子住宅太陽能能源儲存市場全球鋰離子太陽能能源儲存市場 混合動力發電廠市場分析與預測(至 2034 年):類型、產品、服務、技術、組件、應用、部署、最終用戶、安裝類型、設備

混合動力發電廠市場分析與預測(至 2034 年):類型、產品、服務、技術、組件、應用、部署、最終用戶、安裝類型、設備 美國的分散式太陽能光伏發電和蓄電池的2025年展望

美國的分散式太陽能光伏發電和蓄電池的2025年展望