|

市場調查報告書

商品編碼

2071278

動畫市場機會、成長要素、產業趨勢分析及2026-2035年預測Anime Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

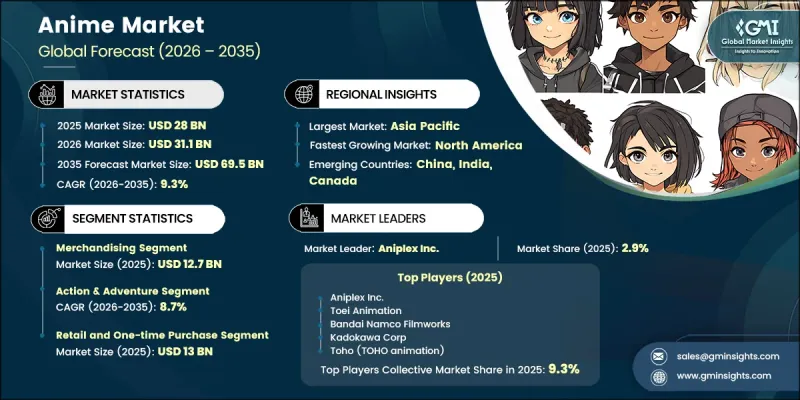

據估計,到 2025 年,全球動畫市場價值將達到 280 億美元,年複合成長率為 9.3%,到 2035 年將達到 695 億美元。

全球對動畫娛樂內容的需求不斷成長,加上串流媒體服務的普及,持續推動市場擴張。動畫市場受益於更廣泛的國際受眾、更豐富的內容資源以及知識產權商業化在多個收入管道的推進。數位平台透過提升內容獲取的便利性並降低全球觀眾的進入門檻,改變了內容消費模式。同時,透過授權協議、消費品和跨媒體開發等方式實現特許經營智慧財產權的商業化,也增強了整個產業的成長機會。對內容創作的持續投入、拓展國際發行策略以及消費者對動畫相關娛樂內容參與度的不斷提高,也為市場成長提供了支撐。隨著數位生態系統的不斷發展和全球需求的持續強勁,預計動畫市場將在預測期內保持強勁的成長勢頭。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 280億美元 |

| 預測金額 | 695億美元 |

| 複合年成長率 | 9.3% |

訂閱式影片串流服務已成為動畫市場最具影響力的成長要素之一。串流平台不斷擴充動畫庫,擴大全球覆蓋範圍,並顯著提升了國際市場的內容可近性。同時,業界也在向平台主導的原創內容製作模式轉型,使發行商能夠在獲取製作資金和加速內容分發方面發揮更積極的作用。這種不斷演進的經營模式強化了串流媒體服務商對動畫節目的長期投入,同時也促進了製作能力和受眾群體的拓展。同時,隨著實體媒體消費的持續下滑,數位平台正成為全球動畫內容的主要發行管道。此外,互動娛樂與動畫IP的融合日益加深,提升了動漫IP的價值,並透過整合的內容生態系統,為觀眾互動和品牌長期發展創造了新的機會。

累計到2025年,商品行銷部門的銷售額將達到127億美元,市佔率高達45.4%。這一主導地位反映了動畫IP強大的商業性實力,為眾多消費品類別的授權銷售提供了堅實的基礎。無論內容發佈計畫為何,周邊商品銷售都能持續帶來可觀的收入。此外,隨著全球對動畫內容的認知度透過數位管道不斷提升,消費者對授權商品的接受度也隨之提高,從而延長了動漫品牌的商業性壽命。

累計到2025年,動作冒險類電影的收入將達到98億美元,市佔率將達到35%。此類型電影預計到2035年將以8.7%的複合年成長率成長。其市場主導地位得益於其對多個消費群廣泛的吸引力,以及在串流媒體和院線發行管道中的強大影響力。此外,這類型電影也受益於豐富的商業化機會,例如授權協議、消費品、數位娛樂、現場體驗以及其他互補的收入來源,這些都提升了系列電影的長期價值。

預計到2025年,亞太地區動畫市場規模將達到161.6億美元,佔全球市佔率的57.7%。其中,日本的貢獻預計為125.8億美元,體現了其作為動畫內容主要製作中心和全球最大單一動畫消費市場的獨特地位。該地區持續受益於許多因素,例如高度發展的製作生態系統、強勁的消費需求、完善的發行網路以及與動漫娛樂深厚的文化淵源,所有這些因素都支撐著市場的持續成長和行業領先地位。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 前景

- 製造商

- 中斷

- 供應商情況

- 主要新聞和舉措

- 技術與創新展望

- 監理情勢

- 影響因素

- 促進因素

- 串流平台的擴張使得人們更容易獲得來自世界各地的動畫內容。

- 動漫在年輕觀眾群中越來越受歡迎,從而推動了動畫的消費。

- 拓展與遊戲領域的合作關係將提高動畫系列的知名度。

- 產業潛在風險與挑戰

- 高昂的製作成本正在給動畫工作室的利潤率帶來壓力。

- 盜版問題對合法動畫收入的創造產生了負面影響。

- 機會

- 人工智慧動畫技術顯著提高了製作效率。

- 拓展國際授權業務將創造全球商機。

- 促進因素

- 波特的分析

- PESTLE分析

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧驅動的現有經營模式轉型(降低生產成本,緩解工作室整合風險)

- 針對特定領域的生成式人工智慧(中間繪圖、背景藝術、語音合成、字幕創建)的應用案例和實施藍圖

- 風險、限制和監管的考量(藝術真實性、人工智慧生成作品的智慧財產權所有權、動畫師工作的替代)

- 基礎架構和部署狀態

- 按地區和購買群體分類的採用率(亞太地區、北美和歐洲的 SVOD/AVOD動畫平台覆蓋範圍)

- 可擴展性限制和基礎設施投資趨勢(CDN 容量、在地化基礎設施、同時交付瓶頸)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依服務類型分類,2022-2035年

- TV

- 電影

- 影片

- 網路散佈

- 商品行銷

- 音樂

- 柏青哥

- 現場娛樂

第6章 市場估計與預測:依類型分類,2022-2035年

- 動作冒險

- 科幻、奇幻、異世界

- 愛情劇

- 生活片段/喜劇

- 運動的

- 恐怖驚悚片

- 其他

第7章 市場估計與預測:依支付模式分類,2022-2035年

- 零售/一次性購買

- B2B 許可

- 訂閱(SVOD)

- 交易型(TVOD)

- 其他

第8章及預測:區域細分,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- UAE

- 沙烏地阿拉伯

- 南非

第9章:公司簡介

- 世界公司

- Toei Animation Co., Ltd.

- Bandai Namco Filmworks Inc.(Sunrise)

- Aniplex Inc.

- Toho Co., Ltd.(TOHO animation)

- TMS Entertainment Co., Ltd.

- OLM, Inc.

- Bones Inc.

- 當地公司

- Kyoto Animation Co., Ltd.

- Production IG, Inc.

- MADHOUSE Inc.

- Pierrot Co., Ltd.

- Studio Ghibli Inc.

- Kadokawa Corporation

- JCStaff Co., Ltd.

- 新興企業

- MAPPA Co., Ltd.

- Ufotable Co., Ltd.

- WIT Studio Co., Ltd.

- Studio Trigger Inc.

- Science SARU Inc.

- David Production Inc.

- CloverWorks Inc.

The Global Anime Market was valued at USD 28 billion in 2025 and is estimated to grow at a CAGR of 9.3% to reach USD 69.5 billion by 2035.

Strong global demand for animated entertainment content, combined with increasing accessibility through streaming services, continues to drive market expansion. The Anime Market is benefiting from a broader international audience base, greater content availability, and the increasing commercialization of intellectual property across multiple revenue channels. Digital platforms have transformed content consumption patterns by improving accessibility and reducing barriers to entry for viewers worldwide. At the same time, the growing monetization of franchise-based intellectual property through licensing agreements, consumer products, and cross-media initiatives is strengthening revenue generation opportunities across the industry. Market growth is also being supported by ongoing investments in content production, expanding international distribution strategies, and rising consumer engagement with anime-related entertainment. As digital ecosystems continue to evolve and global demand remains strong, the Anime Market is expected to maintain robust growth momentum throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $28 Billion |

| Forecast Value | $69.5 Billion |

| CAGR | 9.3% |

Subscription-based video streaming services have emerged as one of the most influential growth drivers within the Anime Market. Streaming platforms continue to expand their anime offerings, enabling broader global access and significantly improving content availability across international markets. The industry is also witnessing a shift toward platform-supported original content development, allowing distributors to play a more active role in financing productions and accelerating content releases. This evolving business model has strengthened the long-term commitment of streaming providers to anime programming while enhancing production capacity and audience reach. At the same time, the continued decline of physical media consumption has further reinforced digital platforms as the primary distribution channel for anime content worldwide. In addition, the growing convergence between interactive entertainment and animated intellectual property is enhancing franchise value, creating new opportunities for audience engagement and long-term brand expansion through integrated content ecosystems.

The merchandising segment generated USD 12.7 billion in 2025, accounting for 45.4% share. Its leadership position reflects the enduring commercial strength of anime intellectual property, which supports licensing opportunities across numerous consumer product categories. Merchandise sales continue to generate substantial revenue streams regardless of content release schedules, while the increasing global visibility of anime content through digital channels is accelerating consumer adoption of licensed products and expanding the commercial lifespan of franchise brands.

The Action & Adventure segment generated USD 9.8 billion in 2025 holding 35% share. The segment is expected to grow at a CAGR of 8.7% through 2035. Its market dominance is driven by broad audience appeal across multiple demographic groups and its strong presence across both streaming and theatrical distribution channels. The genre also benefits from extensive monetization opportunities through licensing agreements, consumer products, digital entertainment, live experiences, and other complementary revenue streams that enhance long-term franchise value.

Asia Pacific Anime Market reached USD 16.16 billion in 2025, holding 57.7% share. Japan contributed an estimated USD 12.58 billion, reflecting its unique position as both the leading production center for anime content and the largest individual national market for anime consumption. The region continues to benefit from a highly developed production ecosystem, strong consumer demand, established distribution networks, and deep cultural engagement with animated entertainment, all of which support sustained market growth and industry leadership.

Key companies operating in the Global Anime Market include Aniplex Inc., Toei Animation Co. Ltd., Bandai Namco Filmworks Inc., Kadokawa Corporation, and Toho Co. Ltd. Companies operating in the Anime Market are strengthening their competitive position through content expansion, intellectual property development, strategic partnerships, and global distribution initiatives. Leading organizations are increasing investments in original productions and franchise development to build long-term revenue streams across multiple platforms. Collaboration with streaming providers, licensing partners, and international distributors is helping companies broaden audience reach and accelerate market penetration. Businesses are also focusing on expanding merchandise portfolios, enhancing brand visibility, and creating integrated entertainment ecosystems that support sustained consumer engagement.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service type

- 2.2.3 Genre

- 2.2.4 Payment model

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Technology & Innovation Landscape

- 3.5 Regulatory landscape

- 3.6 Impact on forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing streaming platforms increase global anime content accessibility

- 3.6.1.2 Rising popularity among younger audiences boosts anime consumption

- 3.6.1.3 Expanding gaming collaborations strengthen anime franchise visibility

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs pressure anime studio profit margins

- 3.6.2.2 Piracy issues negatively affect legitimate anime revenue generation

- 3.6.3 Opportunities

- 3.6.3.1 AI-assisted animation technologies improve production efficiency significantly

- 3.6.3.2 Expanding international licensing creates global revenue opportunities

- 3.6.1 Growth drivers

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.8.1 Pricing analysis (driven by primary research)

- 3.8.2 Historical price trend analysis licensing fees, streaming rights & merchandise retail pricing (driven by primary research)

- 3.8.3 Pricing strategy by player type (premium studio / mid-tier / independent / platform-native) (driven by primary research)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models (production cost reduction, studio consolidation risk)

- 3.9.2 GenAI use cases & adoption roadmap by segment (in-betweening, background art, voice synthesis, subtitling)

- 3.9.3 Risks, limitations & regulatory considerations (artistic authenticity, IP ownership of AI output, animator displacement)

- 3.10 Infrastructure & deployment landscape (driven by primary research)

- 3.10.1 Deployment penetration by region & buyer segment (SVOD/AVOD anime platform reach across Asia Pacific, North America & Europe) (driven by primary research)

- 3.10.2 Scalability constraints & infrastructure investment trends (CDN capacity, localization infrastructure, simulcast delivery bottlenecks) (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Service Type, 2022-2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 T.V.

- 5.3 Movie

- 5.4 Video

- 5.5 Internet distribution

- 5.6 Merchandising

- 5.7 Music

- 5.8 Pachinko

- 5.9 Live entertainment

Chapter 6 Market Estimates & Forecast, By Genre, 2022-2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Action & adventure

- 6.3 Sci-Fi, fantasy & Isekai

- 6.4 Romance & drama

- 6.5 Slice of life & comedy

- 6.6 Sports

- 6.7 Horror & thriller

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Payment Model, 2022-2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Retail / One-time purchase

- 7.3 B2B licensing

- 7.4 Subscription (SVOD)

- 7.5 Transactional (TVOD)

- 7.6 Others

Chapter 8 & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 U.K.

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Global players

- 9.1.1 Toei Animation Co., Ltd.

- 9.1.2 Bandai Namco Filmworks Inc. (Sunrise)

- 9.1.3 Aniplex Inc.

- 9.1.4 Toho Co., Ltd. (TOHO animation)

- 9.1.5 TMS Entertainment Co., Ltd.

- 9.1.6 OLM, Inc.

- 9.1.7 Bones Inc.

- 9.2 Regional players

- 9.2.1 Kyoto Animation Co., Ltd.

- 9.2.2 Production I.G, Inc.

- 9.2.3 MADHOUSE Inc.

- 9.2.4 Pierrot Co., Ltd.

- 9.2.5 Studio Ghibli Inc.

- 9.2.6 Kadokawa Corporation

- 9.2.7 J.C.Staff Co., Ltd.

- 9.3 Emerging players

- 9.3.1 MAPPA Co., Ltd.

- 9.3.2 Ufotable Co., Ltd.

- 9.3.3 WIT Studio Co., Ltd.

- 9.3.4 Studio Trigger Inc.

- 9.3.5 Science SARU Inc.

- 9.3.6 David Production Inc.

- 9.3.7 CloverWorks Inc.

動畫市場:按類型和地區分類 -

動畫市場:按類型和地區分類 - 動畫和遊戲市場:2026-2032年全球市場預測(按交付方式、遊戲平台、年齡層、內容類型、最終用戶和分銷管道分類)動畫市場:2026-2032年全球市場預測(依格式、類型、目標受眾和收入來源分類)動畫製作市場:按動畫類型、應用程式和地區分類

動畫和遊戲市場:2026-2032年全球市場預測(按交付方式、遊戲平台、年齡層、內容類型、最終用戶和分銷管道分類)動畫市場:2026-2032年全球市場預測(依格式、類型、目標受眾和收入來源分類)動畫製作市場:按動畫類型、應用程式和地區分類 動畫市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、最終使用者、模式及階段分類動畫電影和電視節目市場分析及預測(至2035年):按類型、產品類型、服務、技術、應用、最終用戶、部署類型、解決方案和模式分類

動畫市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、最終使用者、模式及階段分類動畫電影和電視節目市場分析及預測(至2035年):按類型、產品類型、服務、技術、應用、最終用戶、部署類型、解決方案和模式分類 全球動畫市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球動畫市場規模、佔有率、趨勢和成長分析報告(2026-2034) 日本動畫市場規模、佔有率、趨勢和預測:按收入來源和地區分類,2026-2034年

日本動畫市場規模、佔有率、趨勢和預測:按收入來源和地區分類,2026-2034年 動畫市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、主題、地區和競爭格局分類,2021-2031年AI動畫影片製作市場:按組件、類型、經營模式、輸出格式、部署模式、組織規模和最終用途分類,全球預測(2026-2032年)

動畫市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、主題、地區和競爭格局分類,2021-2031年AI動畫影片製作市場:按組件、類型、經營模式、輸出格式、部署模式、組織規模和最終用途分類,全球預測(2026-2032年)