|

市場調查報告書

商品編碼

2071249

永續船用燃料市場機會、成長要素、產業趨勢分析及2026-2035年預測Sustainable Marine Fuels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

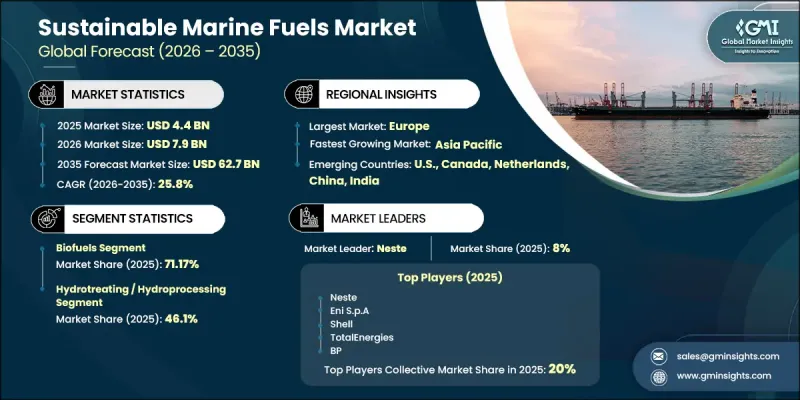

預計到 2025 年,全球永續船用燃料市場價值將達到 44 億美元,並將以 25.8% 的複合年成長率成長,到 2035 年達到 627 億美元。

永續船用燃料產業的整體成長受到全球更嚴格的排放法規、強制性溫室氣體排放強度降低目標以及碳定價機制擴展的推動,這些因素正在重塑整個航運業的營運和籌資策略。隨著供應鏈排放排放納入企業的淨零排放框架,托運人的脫碳努力進一步提振了需求。這種轉變促進了長期燃料採購合約的簽訂,從而穩定需求並支持基礎設施投資。因此,托運人正日益與產業夥伴合作,以確保低排放燃料的穩定供應,同時加強對不斷變化的環境標準的遵守。向永續船用燃料的轉型也得益於航運價值鏈上各環節合作的加強,燃料生產商、物流供應商和相關人員攜手合作,共同支持低碳燃料生態系統的發展。預計這些結構性促進因素將在預測期內顯著改變船用燃料的採購模式。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 44億美元 |

| 預測金額 | 627億美元 |

| 複合年成長率 | 25.8% |

生物基船用燃料市佔率高達71.17%,銷售額達31.3億美元,年複合成長率達16.3%。該細分市場佔據主導地位的主要原因是其與現有船用引擎系統和燃料供應基礎設施的高度兼容性,無需對船舶進行重大改造即可部署。這種營運柔軟性使得生物基燃料成為全球船隊實現航運脫碳最切實可行的短期途徑之一。

預計到2025年,氫氣加工和氫氣純化技術領域將佔據46.1%的市場佔有率,市場規模達20.3億美元。這些製程透過基於氫氣的純化方法,將脂質原料轉化為低碳船用燃料,並支持可再生柴油的生產。它們能夠有效地將各種原料轉化為標準化燃料產品,這推動了它們在大規模永續燃料生產系統中的日益普及。

預計2025年,北美永續船用燃料市場規模將達到9.9億美元,市佔率為22.45%,並將在2035年之前以23.2%的複合年成長率成長。美國是該地區成長的主要驅動力,這得益於其製定的旨在加速向低排放量航運轉型的政策框架。對無污染燃料基礎設施投資的增加以及在商業航運和國防相關海事活動中的日益普及,進一步推動了該地區的市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 原物料供應及採購分析

- 供應鏈韌性與風險因素

- 配電網路分析

- 中斷

- 監理情勢

- 國際海事組織的溫室氣體戰略和歐盟的航運燃料法規

- 區域監管要求(歐盟排放交易體系、美國環保署、國際原子能系統協會)

- 符合碳強度指數 (CII) 和 EEXI 標準

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 新機會和趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

- 技術與創新展望

- 人工智慧正在改變加油、物流和車隊管理。

- GenAI按燃料細分市場的應用案例和部署藍圖

- 風險、限制和監管考量

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧最佳化生產

- 預測性維護和故障檢測

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 市場集中度分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 按公司規模進行基準測試

- 排名分類標準與遴選標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場規模及預測:依燃料類型分類,2022-2035年

- 生質燃料

- 生質柴油

- HVO/可再生柴油

- 生質油

- 生物原油

- 綠色甲醇

- 綠色氨氣

- 綠氫能

- 生物液化天然氣/再生天然氣

- 其他

第6章 市場規模與預測:依轉型過程分類,2022-2035年

- 酯交換反應

- 電解合成

- 費托合成(FTS)

- 氫處理/氫化處理

- 厭氧消化

- 其他

第7章 市場規模及預測:依應用領域分類,2022-2035年

- 商船

- 貨船

- 油船

- 客船

- 作業船

- 防禦艦艇

- 海軍水面艦艇

- 兩棲攻擊艦和支援艦

- 其他

第8章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 挪威

- 德國

- 法國

- 荷蘭

- 英國

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 新加坡

- 中東和非洲

- 沙烏地阿拉伯

- UAE

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第9章:公司簡介

- Argent Energy

- BP

- Bunker Holding

- Cargill

- Chevron Corporation

- Eni SpA

- Evergent Technologies

- Exxon Mobil Corporation

- FincoEnergies

- Gevo

- GoodFuels

- Kvasir Technologies

- Moeve

- Neste Corporation

- Shell plc

- Steeper Energy

- Sunpine AB

- Repsol

- TotalEnergies

- World Energy

The Global Sustainable Marine Fuels Market was valued at USD 4.4 billion in 2025 and is estimated to grow at a CAGR of 25.8% to reach USD 62.7 billion by 2035.

Growth across the sustainable marine fuels industry is influenced by tightening global emissions regulations, mandatory greenhouse gas intensity reduction targets, and increasing carbon pricing mechanisms that are reshaping operational and procurement strategies across the shipping sector. Decarbonization commitments from cargo owners are further reinforcing demand, as supply chain emissions are increasingly incorporated into corporate net-zero frameworks. This shift is encouraging long-term fuel procurement agreements that help stabilize demand and support infrastructure investment. As a result, shipping operators are increasingly aligning with industrial partners to secure reliable access to low-emission fuel supplies while improving compliance with evolving environmental standards. The transition toward sustainable marine fuels is also being reinforced by growing collaboration across the maritime value chain, where fuel producers, logistics operators, and cargo stakeholders are jointly supporting the scale-up of low-carbon fuel ecosystems. These combined structural drivers are expected to significantly reshape marine fuel sourcing patterns over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.4 Billion |

| Forecast Value | $62.7 Billion |

| CAGR | 25.8% |

The bio-based marine fuels segment held a 71.17% share, generating USD 3.13 billion, while expanding at a CAGR of 16.3%. Their leadership position is largely attributed to their compatibility with existing marine engine systems and fuel distribution infrastructure, enabling adoption without requiring major vessel modifications. This operational flexibility has made bio-based fuels one of the most practical short-term pathways for maritime decarbonization across global shipping fleets.

The hydrotreatment and hydroprocessing technologies segment held a 46.1% share in 2025, generating USD 2.03 billion. These processes convert lipid-based raw materials into low-carbon marine fuels through hydrogen-based refining methods, supporting the production of renewable diesel-type fuels. Their ability to efficiently transform diverse feedstocks into standardized fuel products has strengthened their adoption within large-scale sustainable fuel production systems.

North America Sustainable Marine Fuels Market held 22.45% share in 2025, valued at USD 0.99 billion, and is projected to grow at a CAGR of 23.2% through 2035. The United States serves as the key growth engine in the region, supported by policy frameworks designed to accelerate the transition toward low-emission maritime operations. Increasing investments in clean fuel infrastructure and expanding adoption across commercial shipping and defense-related maritime activities are further reinforcing regional market growth.

Key companies operating in the global sustainable marine fuels market include Shell, BP, Exxon Mobil Corporation, Chevron Corporation, TotalEnergies, Repsol, Eni S.p.A, Neste Corporation, World Energy, Cargill, Bunker Holding, FincoEnergies, Gevo, GoodFuels, Argent Energy, Moeve, Evergent Technologies, Kvasir Technologies, Steeper Energy, and Sunpine AB. Companies operating in the sustainable marine fuels market are focusing on strengthening their competitive positioning through large-scale investments in production capacity, long-term supply agreements, and strategic partnerships across the maritime value chain. Many market participants are prioritizing the expansion of biofuel and synthetic fuel production facilities to meet rising demand from shipping operators transitioning toward low-carbon operations. Collaboration with cargo owners and logistics providers is becoming increasingly important to secure offtake agreements and stabilize revenue streams. Firms are also investing heavily in research and development to improve fuel efficiency, feedstock flexibility, and production scalability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Fuel type trends

- 2.1.3 Conversion process trends

- 2.1.4 Application trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Feedstock availability & sourcing analysis

- 3.1.2 Supply chain resilience & risk factors

- 3.1.3 Distribution network analysis

- 3.1.4 Disruptions

- 3.2 Regulatory landscape

- 3.2.1 IMO GHG Strategy & fuel EU maritime regulation

- 3.2.2 Regional Regulatory mandates (EU ETS, US EPA, IACS)

- 3.2.3 Carbon Intensity Indicator (CII) & EEXI compliance

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.8 Digitalization & IoT integration

- 3.9 Investment analysis & future prospects

- 3.10 Technology & innovation landscape

- 3.10.1 AI-Driven Disruption of bunkering, logistics & fleet management

- 3.10.2 GenAI use cases & adoption roadmap by fuel segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Impact of AI & Generative AI on the market (Solution Core)

- 3.11.1 AI-driven production optimization

- 3.11.2 Predictive maintenance & fault detection

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East & Africa

- 4.2.1.5 Latin America

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 key developments

- 4.5.1 Merger & acquisition

- 4.5.2 Partnership & collaboration

- 4.5.3 New product launched

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Fuel type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Biofuel

- 5.2.1 Biodiesel

- 5.2.2 HVO /Renewable Diesel

- 5.2.3 Bio-Oil

- 5.2.4 Biocrude

- 5.3 Green Methanol

- 5.4 Green Ammonia

- 5.5 Green Hydrogen

- 5.6 Bio-LNG / RNG

- 5.7 Others

Chapter 6 Market Size and Forecast, By Conversion process, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Transesterification

- 6.3 Electrolysis-based synthesis

- 6.4 Fischer-tropsch synthesis (FTS)

- 6.5 Hydrotreating / hydroprocessing

- 6.6 Anaerobic digestion

- 6.7 Others

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Commercial Vessels

- 7.2.1 Cargo vessels

- 7.2.2 Tankers

- 7.2.3 Passenger vessels

- 7.2.4 Working vessels

- 7.3 Defense vessels

- 7.3.1 Naval surface ships

- 7.3.2 Amphibious & support vessels

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Norway

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Netherlands

- 8.3.5 UK

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Singapore

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Argent Energy

- 9.2 BP

- 9.3 Bunker Holding

- 9.4 Cargill

- 9.5 Chevron Corporation

- 9.6 Eni S.p.A

- 9.7 Evergent Technologies

- 9.8 Exxon Mobil Corporation

- 9.9 FincoEnergies

- 9.10 Gevo

- 9.11 GoodFuels

- 9.12 Kvasir Technologies

- 9.13 Moeve

- 9.14 Neste Corporation

- 9.15 Shell plc

- 9.16 Steeper Energy

- 9.17 Sunpine AB

- 9.18 Repsol

- 9.19 TotalEnergies

- 9.20 World Energy

船舶燃料管理市場:按組件、船舶類型、安裝類型、部署類型、應用、分銷管道和最終用戶分類-2026-2032年全球市場預測

船舶燃料管理市場:按組件、船舶類型、安裝類型、部署類型、應用、分銷管道和最終用戶分類-2026-2032年全球市場預測 船舶燃料最佳化市場:規模、佔有率、成長、全球產業分析、區域趨勢及2026-2034年預測

船舶燃料最佳化市場:規模、佔有率、成長、全球產業分析、區域趨勢及2026-2034年預測 2026年全球船舶燃料最佳化市場報告2026-2034年全球永續船用燃料市場規模、佔有率、趨勢和成長分析報告

2026年全球船舶燃料最佳化市場報告2026-2034年全球永續船用燃料市場規模、佔有率、趨勢和成長分析報告 永續船用燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年生物來源船用燃料市場(按燃料類型、船舶類型、引擎類型、應用和分銷管道分類)-全球預測,2026-2032年

永續船用燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年生物來源船用燃料市場(按燃料類型、船舶類型、引擎類型、應用和分銷管道分類)-全球預測,2026-2032年 船舶燃料最佳化市場規模、佔有率和成長分析(按解決方案/組件、最佳化技術、部署類型、最終用戶和地區分類)-2026-2033年產業預測

船舶燃料最佳化市場規模、佔有率和成長分析(按解決方案/組件、最佳化技術、部署類型、最終用戶和地區分類)-2026-2033年產業預測 船用替代燃料技術市場:到 2033 年的市場分析和預測 - 按產品、按服務、按技術、按組件、按應用、按部署、按最終用戶、按安裝類型、按解決方案

船用替代燃料技術市場:到 2033 年的市場分析和預測 - 按產品、按服務、按技術、按組件、按應用、按部署、按最終用戶、按安裝類型、按解決方案