|

市場調查報告書

商品編碼

2071245

航太數位訊號處理器市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Aerospace Digital Signal Processors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

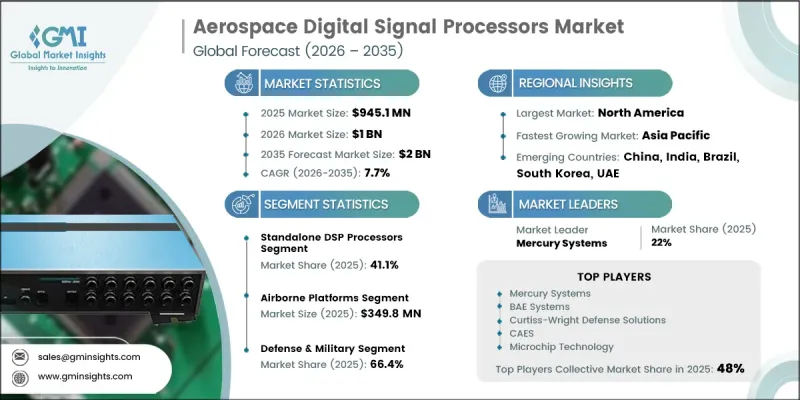

預計到 2025 年,全球航太數位訊號處理器市場規模將達到 9.451 億美元,年複合成長率為 7.7%,到 2035 年將達到 20 億美元。

航太數位訊號處理器市場的成長主要得益於先進航空電子技術的日益普及以及現代航太系統對高速資料處理需求的不斷成長。隨著航太平台日趨複雜,能夠以卓越的速度、精度和可靠性處理複雜運算工作負載的處理器需求持續攀升。先進感測技術、關鍵任務處理能力以及增強型通訊系統在航太和國防領域的整體整合也推動了市場成長。對航太連接基礎設施的持續投資為支援安全高效數據傳輸的數位訊號處理解決方案創造了更多機會。小型化電子裝置和高耐久性半導體元件的技術進步也促進了市場擴張。此外,航太應用整體自主功能和人工智慧的日益普及,也推動了對先進處理架構的需求,這些架構能夠在惡劣環境下提供即時運算效能並保持運作可靠性。所有這些因素共同為全球航太數位訊號處理器市場帶來了強勁的長期發展前景。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 9.451億美元 |

| 預測金額 | 20億美元 |

| 複合年成長率 | 7.7% |

航太數位訊號處理器市場正經歷顯著成長,這主要得益於先進航空電子平台和高效能資料處理技術的日益普及。現代航太系統需要能夠以最小延遲處理海量資訊並支援在日益複雜的環境中高效運行的處理器。航太通訊網路和衛星連接系統的擴展進一步加速了對先進數位訊號處理技術的需求。在任務關鍵型航太環境中,對安全資料傳輸和保護的日益重視推動了支援強大加密和安全通訊框架的先進處理解決方案的應用。這些趨勢有助於提高航太和國防應用領域的系統可靠性、運作連續性和整體性能。

到2025年,獨立式DSP處理器市佔率將達到41.1%,成為業界最大的細分市場。其主導地位主要歸功於其在眾多航太處理應用中的廣泛應用,在這些應用中,設計柔軟性、系統相容性和供應商多樣性仍然是關鍵考慮因素。與成熟的航太架構和現有航空電子生態系統的強大相容性也持續支撐著市場對獨立式DSP解決方案的需求。此外,持續的現代化改造項目和對先進航太平台開發的持續投入也進一步推動了市場成長,這些都需要可靠且適應性強的訊號處理技術。

預計到2025年,飛機平台業務部門的銷售額將達到3.498億美元。該板塊的成長主要得益於全球部署的飛機平台機隊,這些平台在其整個營運生命週期內需要持續的技術升級和系統增強。整合到飛機系統中的數位訊號處理器能夠滿足各種關鍵任務的處理需求,並在維持營運效率方面發揮至關重要的作用。由於原始設備製造商 (OEM) 和售後服務管道持續進行的設備升級、現代化改造和長期維護活動,市場需求保持穩定。

預計到2025年,北美航太數位訊號處理器市佔率將達到40.6%。該地區受益於高度發展的航太和國防生態系統,擁有強大的製造能力、先進的技術研發、研究機構和專業的零件供應商。對航太現代化舉措和長期採購項目的持續投資,推動了對高性能數位訊號處理技術的強勁需求。成熟的航太基礎設施和先進航太系統的持續發展,進一步鞏固了該地區在全球市場中的地位。預計對創新、安全和下一代航太技術的持續關注,將支撐北美地區對航太數位訊號處理器的穩定需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 擴大先進航空電子設備和即時數據處理系統的部署

- 國防飛機上雷達、電子戰和ISR系統的整合進展。

- 擴展衛星通訊和航太連接基礎設施

- 小型化和抗輻射電子設備的技術進步

- 對自主和人工智慧驅動的航太系統的需求日益成長

- 產業潛在風險與挑戰

- 開發航太級DSP的複雜性和高成本。

- 嚴格的認證流程和較長的認證週期

- 市場機遇

- 航太系統中邊緣運算的日益普及

- 對太空探勘和衛星星系的需求日益成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- R&D

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興企業和新創企業領域競爭公司的趨勢

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 獨立式DSP處理器

- 單核心DSP處理器

- 多核心DSP處理器

- 整合DSP系統

第6章 市場估算與預測:依環境階層分類,2022-2035年

- 矽(Si)

- 碳化矽(SiC)

- 氮化鎵(GaN)

- 商用航太級

- 堅固級

- 輻射耐受等級

- 抗輻射硬化級

第7章 市場估計與預測:依平台分類,2022-2035年

- 飛機平台

- 空間平台

- 防禦系統

- 其他

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 國防/軍事

- 商業/民用航太

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- 全球主要公司

- Mercury Systems

- BAE Systems

- Curtiss-Wright Defense Solutions

- CAES

- Microchip Technology

- 該地區的主要公司

- 北美洲

- AMD

- Intel

- Texas Instruments

- Analog Devices

- onsemi

- 亞太地區

- Renesas Electronics

- 歐洲

- STMicroelectronics

- Infineon Technologies

- NXP Semiconductors

- Cobham Gaisler

- 北美洲

- 小眾玩家/顛覆者

- VORAGO Technologies

- NanoXplore

- Teledyne e2v

The Global Aerospace Digital Signal Processors Market was valued at USD 945.1 million in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 2 billion by 2035.

Growth across the aerospace digital signal processors market is fueled by the increasing deployment of sophisticated avionics technologies and the growing requirement for high-speed data processing within modern aerospace systems. As aerospace platforms become more advanced, demand continues to rise for processors capable of managing complex computing workloads with exceptional speed, accuracy, and reliability. The market is also benefiting from the expanding integration of advanced sensing technologies, mission-critical processing capabilities, and enhanced communication systems throughout aerospace and defense operations. Continuous investments in aerospace connectivity infrastructure are creating additional opportunities for digital signal processing solutions that support secure and efficient data transmission. Technological progress in miniaturized electronics and highly durable semiconductor components is further contributing to market expansion. In addition, the growing implementation of autonomous capabilities and artificial intelligence across aerospace applications is increasing the need for advanced processing architectures that can deliver real-time computational performance while maintaining operational reliability in demanding environments. These factors collectively continue to strengthen the long-term outlook for the global aerospace digital signal processors market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $945.1 Million |

| Forecast Value | $2 Billion |

| CAGR | 7.7% |

The aerospace digital signal processors market is experiencing substantial momentum due to the increasing adoption of advanced avionics platforms and high-performance data processing technologies. Modern aerospace systems require processors capable of handling significant volumes of information with minimal delay, supporting efficient operation across increasingly sophisticated environments. The expansion of aerospace communication networks and satellite-based connectivity systems is further accelerating demand for advanced digital signal processing technologies. Growing emphasis on secure data transmission and protection within mission-critical aerospace environments is encouraging the adoption of enhanced processing solutions that support robust encryption capabilities and secure communication frameworks. These developments are helping improve system reliability, operational continuity, and overall performance across aerospace and defense applications.

The standalone DSP processors segment accounted for 41.1% share in 2025, making it the largest segment within the industry. Its leadership position is attributed to widespread adoption across numerous aerospace processing applications where design flexibility, system compatibility, and supplier diversification remain important considerations. Strong compatibility with established aerospace architectures and existing avionics ecosystems continues to support demand for standalone DSP solutions. Market growth is further reinforced by ongoing modernization programs and continued investment in advanced aerospace platform development, which require dependable and adaptable signal processing technologies.

The airborne platforms segment generated USD 349.8 million in 2025. Segment growth is supported by the extensive global fleet of aerospace platforms that require continuous technology upgrades and system enhancements throughout their operational lifecycles. Digital signal processors integrated within airborne systems support a broad range of mission-critical processing requirements and play an essential role in maintaining operational effectiveness. Demand remains consistent due to ongoing equipment upgrades, modernization initiatives, and long-term maintenance activities across both original equipment manufacturing and aftermarket service channels.

North America Aerospace Digital Signal Processors Market accounted for 40.6% share in 2025. The region benefits from a highly developed aerospace and defense ecosystem supported by extensive manufacturing capabilities, advanced technology development, research institutions, and specialized component suppliers. Sustained investments in aerospace modernization initiatives and long-term procurement programs continue to generate strong demand for high-performance digital signal processing technologies. The presence of a mature aerospace infrastructure and ongoing development of advanced aerospace systems further strengthens the region's position within the global market. Continuous focus on innovation, security, and next-generation aerospace technologies is expected to support steady demand for aerospace digital signal processors across North America.

Key companies operating in the Global Aerospace Digital Signal Processors Market include AMD, Microchip Technology, BAE Systems, Intel, Texas Instruments, Analog Devices, VORAGO Technologies, NanoXplore, Teledyne e2v, CAES, NXP Semiconductors, onsemi, Renesas Electronics, STMicroelectronics, Infineon Technologies, Cobham Gaisler, Mercury Systems, and Curtiss-Wright Defense Solutions. Companies participating in the aerospace digital signal processors market are implementing a variety of strategic initiatives to strengthen their market presence and enhance competitive positioning. Product innovation remains a primary focus, with manufacturers investing heavily in the development of high-performance, radiation-tolerant, and power-efficient processing solutions designed for demanding aerospace environments. Strategic collaborations with aerospace manufacturers, defense contractors, and government organizations are helping companies secure long-term supply agreements and expand market opportunities. Businesses are also increasing investments in research and development to accelerate technological advancements in artificial intelligence, autonomous systems, and real-time signal processing capabilities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Environmental grade trends

- 2.2.3 Platform trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of advanced avionics and real-time data processing systems

- 3.2.1.2 Increasing integration of radar, electronic warfare, and ISR systems in defense aircraft

- 3.2.1.3 Expansion of satellite communication and aerospace connectivity infrastructure

- 3.2.1.4 Technological advancements in miniaturized and radiation hardened electronics

- 3.2.1.5 Growing demand for autonomous and AI enabled aerospace systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development complexity and cost of aerospace-grade DSPs

- 3.2.2.2 Stringent certification and long qualification cycles

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of edge computing in aerospace systems

- 3.2.3.2 Increasing demand for space exploration and satellite constellations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Standalone DSP processors

- 5.2.1 Single-core DSP processors

- 5.2.2 Multi-core DSP processors

- 5.3 Integrated DSP systems

Chapter 6 Market Estimates and Forecast, By Environmental Grade, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Silicon (Si)

- 6.3 Silicon carbide (SiC)

- 6.4 Gallium nitride (GaN)

- 6.5 Commercial aerospace grade

- 6.6 Ruggedized grade

- 6.7 Radiation-tolerant grade

- 6.8 Radiation-hardened grade

Chapter 7 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Airborne platforms

- 7.3 Space platforms

- 7.4 Defense systems

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Defense & military

- 8.3 Commercial & civil aerospace

- 8.4 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Mercury Systems

- 10.1.2 BAE Systems

- 10.1.3 Curtiss-Wright Defense Solutions

- 10.1.4 CAES

- 10.1.5 Microchip Technology

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 AMD

- 10.2.1.2 Intel

- 10.2.1.3 Texas Instruments

- 10.2.1.4 Analog Devices

- 10.2.1.5 onsemi

- 10.2.2 Asia Pacific

- 10.2.2.1 Renesas Electronics

- 10.2.3 Europe

- 10.2.3.1 STMicroelectronics

- 10.2.3.2 Infineon Technologies

- 10.2.3.3 NXP Semiconductors

- 10.2.3.4 Cobham Gaisler

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 VORAGO Technologies

- 10.3.2 NanoXplore

- 10.3.3 Teledyne e2v

2034年交通運輸業數位雙胞胎市場預測-全球分析(依孿生類型、交通途徑、技術、部署模式、應用、最終用戶和地區分類)數位雙胞胎市場預測(自動化領域)至 2034 年-全球分析(按組件、部署模式、產業、應用、最終用戶和地區分類)數位雙胞胎系統市場預測至2034年-按類型、技術、應用、最終用戶和地區分類的全球分析認知數位雙胞胎智慧市場預測至2034年:按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析

2034年交通運輸業數位雙胞胎市場預測-全球分析(依孿生類型、交通途徑、技術、部署模式、應用、最終用戶和地區分類)數位雙胞胎市場預測(自動化領域)至 2034 年-全球分析(按組件、部署模式、產業、應用、最終用戶和地區分類)數位雙胞胎系統市場預測至2034年-按類型、技術、應用、最終用戶和地區分類的全球分析認知數位雙胞胎智慧市場預測至2034年:按組件、部署模式、技術、應用、最終用戶和地區分類的全球分析 面向工業4.0的全球數位雙胞胎市場報告(2026年)2034年航太市場數位雙胞胎市場預測:按組件、技術、應用、平台類型、最終用戶和地區分類的全球分析工業數位雙胞胎市場預測至2034年-按類型、產品、技術、應用、最終用戶和地區分類的全球分析

面向工業4.0的全球數位雙胞胎市場報告(2026年)2034年航太市場數位雙胞胎市場預測:按組件、技術、應用、平台類型、最終用戶和地區分類的全球分析工業數位雙胞胎市場預測至2034年-按類型、產品、技術、應用、最終用戶和地區分類的全球分析 海事領域數位雙胞胎市場規模、佔有率和趨勢分析報告:按交付方式、部署方式、應用、最終用戶、地區和細分市場預測(2026-2033 年)

海事領域數位雙胞胎市場規模、佔有率和趨勢分析報告:按交付方式、部署方式、應用、最終用戶、地區和細分市場預測(2026-2033 年) 2026-2030年全球物流領域數位雙胞胎市場

2026-2030年全球物流領域數位雙胞胎市場 2026-2030年全球重工業數位雙胞胎市場

2026-2030年全球重工業數位雙胞胎市場