|

市場調查報告書

商品編碼

2071243

能源電力市場中的數位雙胞胎:市場機會、成長要素、產業趨勢分析及2026-2035年預測Digital Twin in Energy and Power Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

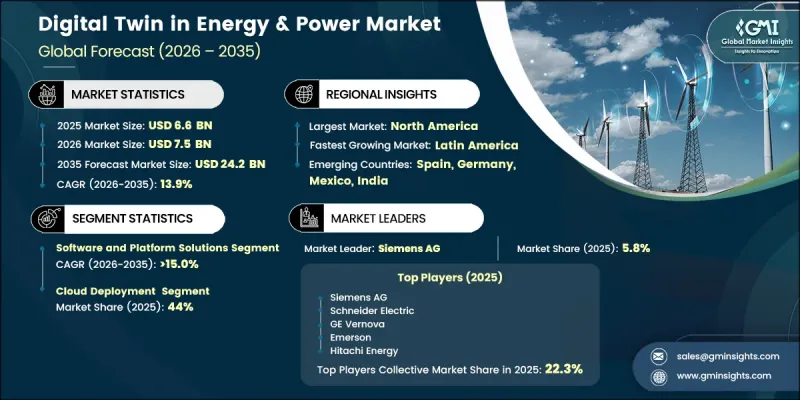

2025年,全球能源電力產業的數位雙胞胎市場價值為66億美元,預計2035年將以13.9%的複合年成長率成長至242億美元。

隨著電力公司、電網營運商和能源資產管理公司越來越依賴先進的模擬和即時監控工具來提高營運效率,市場正在迅速擴張。這一成長主要得益於全球向可再生能源發電主導電力系統的轉型,間歇性的風能和太陽能發電正在取代傳統的可調電源。因此,電網營運商優先考慮能夠最佳化現有基礎設施的智慧系統,而不是僅依賴實體擴容。數位雙胞胎解決方案能夠對電網行為進行持續建模,使營運商能夠模擬故障、評估負載狀況並即時改善擁塞管理。物聯網設備在輸電、配電和發電資產中的日益普及,顯著提高了資料的可用性和模型精度。智慧感測器、邊緣運算設備、同步法佐系統和智慧計量基礎設施等技術正在為高解析度數位雙胞胎平台奠定堅實的基礎。然而,電力公司大規模部署這些技術是一個分階段的過程,因為它需要在硬體部署、整合系統、軟體平台和員工技能發展方面進行大量投資。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 66億美元 |

| 預測金額 | 242億美元 |

| 複合年成長率 | 13.9% |

預計到2025年,軟體和平台服務領域將佔據56%的市場佔有率,並在2035年之前以15%的複合年成長率成長。這一主導地位歸功於軟體解決方案的可擴充性,它能夠在不相應增加基礎設施成本的情況下提升附加價值。隨著感測器網路和連接框架的建立,公共產業將加大投資,透過軟體升級和平台增強來擴展分析和模擬能力。

預計到2025年,基於雲端的部署模式將佔據44%的市場。這一成長主要得益於雲端基礎設施成本的降低、能源專用雲端服務的可用性提高,以及管理和處理分散式能源網路中大規模即時數據的能力。雲端平台還具備滿足現代能源系統運作需求的柔軟性和擴充性。

預計到2025年,數位雙胞胎孿生技術將佔北美能源電力市場38%的佔有率,到2035年將以12.6%的複合年成長率成長。該地區的成長主要得益於大規模的基礎設施現代化改造、公用事業公司不斷擴大的數位化舉措以及成熟技術供應商的積極參與。對電網現代化和韌性提升計畫的持續投資,進一步推動了先進數位雙胞胎技術在整個能源網路中的普及應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系統

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 人工智慧和生成式人工智慧對市場的影響

- 預測性維護和故障檢測

- 電網最佳化和負載預測

- 利用數位雙胞胎進行模擬和測試

- 風險、限制和監管考量

- 新機會與趨勢

- 數位化和物聯網整合

- 進入新興市場

- 整體投資情勢與未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 按公司規模進行基準測試

- 排名分類標準與遴選標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場規模及預測:依組件分類,2022-2035年

- 軟體和平台

- 硬體

- 服務

第6章 市場規模及預測:依部署方式分類,2022-2035年

- 現場

- 雲

- 混合

第7章 市場規模及預測:依雙胞胎類型分類,2022-2035年

- 資產孿生

- 流程/系統孿生體

- 工廠/設施雙體

- 網格/網路孿生

- 企業/系統孿生

- 其他

第8章 市場規模及預測:依應用領域分類,2022-2035年

- 資產績效管理

- 預測性保護

- 電網最佳化和監控

- 流程最佳化

- 能源管理

- 遠端監測和診斷

- 模擬與情境規劃

- 安全、風險和合規管理

- 其他

第9章 市場規模及預測:依最終用戶分類,2022-2035年

- 石油和天然氣

- 發電

- 公共產業及電網營運商

- 可再生能源

- 其他

第10章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 挪威

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- UAE

- 卡達

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

第11章:公司簡介

- ABB Ltd.

- Accenture

- ANSYS Inc.

- Bentley Systems

- Cognite AS

- Dassault Systemes

- Emerson

- ETAP

- GE Vernova

- Hexagon AB

- Hitachi Energy

- Honeywell International

- IBM Corporation

- Kongsberg Digital

- Microsoft

- PTC Inc.

- Schneider Electric

- Siemens AG

- Siemens Energy

- Yokogawa Electric

The Global Digital Twin in Energy & Power Market was valued at USD 6.6 billion in 2025 and is estimated to grow at a CAGR of 13.9% to reach USD 24.2 billion by 2035.

The market is expanding rapidly as utilities, grid operators, and energy asset managers increasingly rely on advanced simulation and real-time monitoring tools to improve operational efficiency. This growth is strongly influenced by the global transition toward renewable-dominant power systems, where intermittent energy generation from wind and solar is replacing conventional dispatchable sources. As a result, grid operators are prioritizing intelligent systems capable of optimizing existing infrastructure rather than relying solely on physical expansion. Digital twin solutions enable continuous modeling of grid behavior, allowing operators to simulate faults, assess load conditions, and improve congestion management in real time. The rising deployment of IoT-enabled devices across transmission, distribution, and generation assets is significantly improving data availability and model accuracy. Technologies such as smart sensors, edge computing devices, synchrophasor systems, and intelligent metering infrastructure are strengthening the foundation for high-resolution digital twin platforms. However, implementation requires considerable investment in hardware deployment, integration systems, software platforms, and workforce upskilling, making large-scale adoption a phased process across utilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.6 Billion |

| Forecast Value | $24.2 Billion |

| CAGR | 13.9% |

The software and platform-based offerings segment held a 56% share in 2025 and is expected to grow at a CAGR of 15% through 2035. This leadership is attributed to the scalable nature of software solutions, where incremental value can be added without proportional increases in infrastructure costs. Once sensor networks and connectivity frameworks are established, utilities increasingly invest in expanding analytical and simulation capabilities through software upgrades and platform enhancements.

The cloud-based deployment models segment held 44% share in 2025. Their growth is supported by improved affordability of cloud infrastructure, increased availability of energy-focused cloud services, and the ability to manage and process large-scale real-time data across distributed energy networks. Cloud platforms also offer flexibility and scalability that align with the operational requirements of modern energy systems.

North America Digital Twin in Energy & Power Market accounted for 38% share in 2025 and is projected to grow at a CAGR of 12.6% through 2035. The region's growth is supported by large-scale infrastructure modernization efforts, increasing utility digitalization initiatives, and strong participation from established technology vendors. Continued investments in grid modernization and resilience programs are further strengthening regional adoption of advanced digital twin technologies across energy networks.

Key companies operating in the Global Digital Twin In Energy & Power Market include Siemens Energy, Schneider Electric, ABB Ltd., GE Vernova, Honeywell International, IBM Corporation, Microsoft, Accenture, Dassault Systemes, Emerson, Hitachi Energy, Bentley Systems, PTC Inc., ANSYS Inc., ETAP, Hexagon AB, Cognite AS, Yokogawa Electric, Kongsberg Digital, and Siemens AG. Market participants are actively strengthening their competitive position by investing in advanced analytics capabilities, AI-driven modeling tools, and cloud-native digital twin platforms. Strategic partnerships with utilities and grid operators are helping companies integrate solutions directly into operational workflows. Many firms are focusing on expanding their software ecosystems to offer end-to-end simulation, monitoring, and predictive maintenance capabilities. Continuous product innovation, particularly in real-time data processing and asset performance optimization, is enhancing solution value. Companies are also prioritizing global expansion strategies and sector-specific customization to address varying regulatory and infrastructure needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Components trends

- 2.4 Deployment trends

- 2.5 Twin type trends

- 2.6 Application trends

- 2.7 End user trends

- 2.8 Region trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.2.1 North America

- 3.2.2 Europe

- 3.2.3 Asia Pacific

- 3.2.4 Middle East & Africa

- 3.2.5 Latin America

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Impact of AI & generative AI on the market

- 3.7.1 Predictive maintenance & fault detection

- 3.7.2 Grid optimization & load forecasting

- 3.7.3 Digital twin simulation & testing

- 3.7.4 Risks, limitations & regulatory considerations

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Overall investment scenario and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Component, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Software & platforms

- 5.3 Hardware

- 5.4 Services

Chapter 6 Market Size and Forecast, By Deployment, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

- 6.4 Hybrid

Chapter 7 Market Size and Forecast, By Twin type, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Asset twin

- 7.3 Process/system twin

- 7.4 Plant/facility twin

- 7.5 Grid/network twin

- 7.6 Enterprise/system-of-systems twin

- 7.7 Others

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Asset performance management

- 8.3 Predictive maintenance

- 8.4 Grid optimization & monitoring

- 8.5 Process optimization

- 8.6 Energy management

- 8.7 Remote monitoring & diagnostics

- 8.8 Simulation & scenario planning

- 8.9 Safety, risk & compliance management

- 8.10 Others

Chapter 9 Market Size and Forecast, By End user, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Oil & gas

- 9.3 Power generation

- 9.4 Utilities & grid operators

- 9.5 Renewable energy

- 9.6 Others

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Norway

- 10.3.5 Italy

- 10.3.6 Spain

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Qatar

- 10.5.4 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Mexico

Chapter 11 Company Profiles

- 11.1 ABB Ltd.

- 11.2 Accenture

- 11.3 ANSYS Inc.

- 11.4 Bentley Systems

- 11.5 Cognite AS

- 11.6 Dassault Systemes

- 11.7 Emerson

- 11.8 ETAP

- 11.9 GE Vernova

- 11.10 Hexagon AB

- 11.11 Hitachi Energy

- 11.12 Honeywell International

- 11.13 IBM Corporation

- 11.14 Kongsberg Digital

- 11.15 Microsoft

- 11.16 PTC Inc.

- 11.17 Schneider Electric

- 11.18 Siemens AG

- 11.19 Siemens Energy

- 11.20 Yokogawa Electric

2026年全球電動車數位雙胞胎市場報告

2026年全球電動車數位雙胞胎市場報告 電動數位雙胞胎市場:按數位雙胞胎類型、類別、組件、資產類型、部署模式、應用領域、最終用戶和用途分類-2026-2032年全球市場預測

電動數位雙胞胎市場:按數位雙胞胎類型、類別、組件、資產類型、部署模式、應用領域、最終用戶和用途分類-2026-2032年全球市場預測 電氣數位雙胞胎市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、最終用戶、地區和競爭格局分類,2021-2031年)按組件、組織規模、應用、最終用戶產業和部署類型分類的電氣數位雙胞胎系統市場 - 全球預測 2026-2032

電氣數位雙胞胎市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、最終用戶、地區和競爭格局分類,2021-2031年)按組件、組織規模、應用、最終用戶產業和部署類型分類的電氣數位雙胞胎系統市場 - 全球預測 2026-2032 電氣數位雙胞胎市場規模、佔有率和成長分析(按孿生類型、用途類型、部署類型、應用、最終用戶和地區分類)—2026-2033年產業預測

電氣數位雙胞胎市場規模、佔有率和成長分析(按孿生類型、用途類型、部署類型、應用、最終用戶和地區分類)—2026-2033年產業預測 全球電氣數位孿生市場規模研究與預測,依孿生類型、使用類型、部署類型、最終用戶、應用程式和區域預測 2025-2035

全球電氣數位孿生市場規模研究與預測,依孿生類型、使用類型、部署類型、最終用戶、應用程式和區域預測 2025-2035