|

市場調查報告書

商品編碼

2071191

微生物來源食品色素市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。Microbial Food Colors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

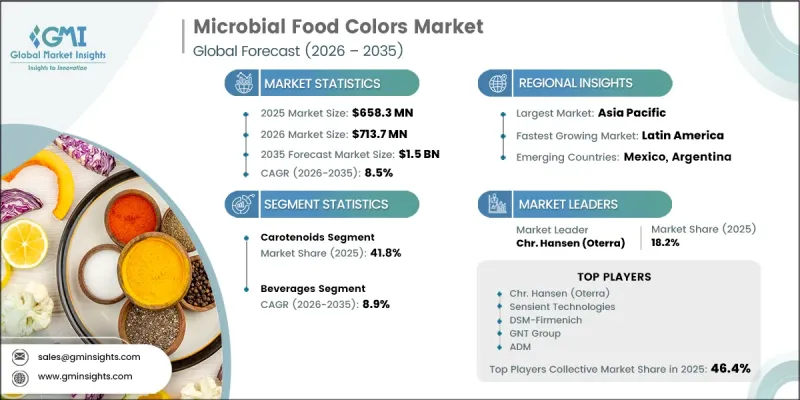

預計到 2025 年,全球微生物衍生食品色素市場價值將達到 6.583 億美元,年複合成長率為 8.5%,到 2035 年將達到 15 億美元。

市場成長的驅動力在於,消費者正加速從合成食用色素轉向透過微生物發酵和生物技術製程生產的天然色素。這一轉變反映了食品飲料行業更廣泛的轉型,製造商越來越重視原料透明度、潔淨標示產品的開發以及天然替代品的採用。微生物色素生產商業性可行性的提高,加上不斷變化的監管要求和消費者對原料成分日益成長的關注,為市場擴張創造了有利環境。在成分標籤對購買決策和品牌差異化起著至關重要作用的產品類型中,市場需求尤其強勁。在各大市場,食品製造商正在最佳化產品配方,以迎合消費者對成分更簡單、加工更少的產品的偏好。隨著「潔淨標示」趨勢從高級產品領域擴展到主流市場,微生物來源的食用色素的應用範圍也日益擴大。監管支援、發酵製程的技術進步以及消費者對天然原料日益成長的需求,預計將有助於市場實現長期持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 6.583億美元 |

| 預測金額 | 15億美元 |

| 複合年成長率 | 8.5% |

預計到2025年,類胡蘿蔔素市佔率將達到41.8%。其市場主導地位得益於微生物生產技術的成熟商業性規模化應用,以及類胡蘿蔔素色素在眾多食品和飲料應用中的廣泛功能。穩定的著色能力、配方柔軟性以及與多種產品類型的兼容性等特性,持續推動著該細分市場的廣泛應用。預計在預測期內,發酵效率和生產最佳化的不斷進步將進一步鞏固該細分市場的市場地位。

預計到2025年,飲料市佔率將達到32.3%,並在2035年之前以8.9%的複合年成長率成長。這一主導地位反映了飲料配方中視覺吸引力和成分透明度的關鍵重要性。隨著消費者越來越關注產品標籤並要求使用天然成分,飲料製造商正在加速向微生物著色解決方案轉型。消費者對潔淨標示飲料的需求不斷成長,以及高級產品定位的不斷擴大,持續為微生物著色劑在該品類中的應用創造了巨大的機會。

預計到2025年,北美微生物衍生食用色素市場佔有率將達到24.8%,並在2035年之前以8.4%的複合年成長率成長。該地區仍然是天然食品配料的重要市場,這得益於消費者較高的認知度、完善的食品生產基礎設施以及對潔淨標示產品日益成長的需求。持續的監管趨勢,以及業界對天然配料解決方案不斷增加的投資,將繼續推動微生物衍生食用色素在各種食品和飲料應用中的廣泛應用。該地區對產品透明度和配料創新的重視預計將在整個預測期內支撐市場的持續成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 成長促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 價格趨勢

- 按地區

- 依顏料類型

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 專利趨勢

- 貿易統計

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依顏料類型分類,2022-2035年

- 類胡蘿蔔素

- 花青素和黃酮類化合物

- 藻膽蛋白

- 核黃素

- 地工合成材料粘土襯墊菌素

- 黑色素和其他

第6章 市場估計與預測:依來源分類,2022-2035年

- 細菌來源

- 真菌來源

- 酵母衍生的

- 源自微藻類

第7章 市場估計與預測:依類型分類,2022-2035年

- 液體

- 粉末

- 凝膠

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 飲料

- 碳酸飲料

- 果汁和水果飲料

- 能量飲料和運動飲料

- 酒精飲料

- 麵包糖果甜點

- 燒製產品

- 冰淇淋和冷凍甜點

- 糖果

- 乳製品

- 優格

- 乳類飲料

- 嬰兒食品

- 起司和奶油

- 加工食品

- 醬汁和調味料

- 調理食品

- 零嘴零食

- 肉類、家禽和水產品

- 肉類色素

- 水產飼料

- 家禽飼料

- 營養補充品

- 營養保健品

- 保健品

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- UAE

- 其他中東和非洲國家

第10章:公司簡介

- Chr. Hansen(Oterra)

- Sensient Technologies

- GNT Group

- DSM-Firmenich

- ADM

- Kerry Group

- Dohler

- Givaudan

- Kalsec

- Roha Dyechem

- Lycored

- Chenguang Biotech

- Allied Biotech

- Synthite Industries

- AVT Natural Products

The Global Microbial Food Colors Market was valued at USD 658.3 million in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 1.5 billion by 2035.

Market growth is driven by the accelerating transition from synthetic food colorants to naturally derived pigments produced through microbial fermentation and biotechnology-based processes. This shift reflects broader changes in the food and beverage industry, where manufacturers are increasingly prioritizing ingredient transparency, clean-label product development, and naturally sourced alternatives. The improving commercial viability of microbial pigment production, combined with evolving regulatory requirements and rising consumer awareness regarding ingredient composition, is creating favorable conditions for market expansion. Demand is particularly strong in product categories where ingredient labeling plays a critical role in purchasing decisions and brand differentiation. Across major markets, food manufacturers are reformulating products to align with consumer preferences for simpler ingredient lists and minimally processed formulations. As clean-label trends continue to move beyond premium product segments and become increasingly mainstream, the adoption of microbial food colors is expanding across a broader range of food and beverage applications. The combination of regulatory support, technological advancements in fermentation processes, and growing consumer demand for naturally sourced ingredients is expected to sustain long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $658.3 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 8.5% |

The carotenoids segment accounted for 41.8% share in 2025. Its dominant position is supported by the established commercial scalability of microbial production technologies and the broad functionality of carotenoid pigments across numerous food and beverage applications. Their ability to provide stable coloration, formulation flexibility, and compatibility with diverse product categories continues to support widespread adoption. Ongoing advancements in fermentation efficiency and production optimization are expected to further strengthen the segment's market position during the forecast period.

The beverages segment held a 32.3% share in 2025 and is expected to grow at a CAGR of 8.9% through 2035. The segment's leadership reflects the critical importance of visual appeal and ingredient transparency within beverage formulations. As consumers increasingly evaluate product labels and seek naturally sourced ingredients, beverage manufacturers are accelerating the transition toward microbial color solutions. Growing demand for clean-label beverages and premium product positioning continues to create significant opportunities for microbial pigment adoption across the category.

North America Microbial Food Colors Market accounted for 24.8% share in 2025 and is projected to grow at a CAGR of 8.4% through 2035. The region remains a key market for naturally derived food ingredients, supported by strong consumer awareness, established food manufacturing infrastructure, and increasing demand for clean-label products. Ongoing regulatory developments, combined with growing industry investment in natural ingredient solutions, continue to encourage the adoption of microbial food colors across a wide range of food and beverage applications. The region's emphasis on product transparency and ingredient innovation is expected to support sustained market growth throughout the forecast period.

Major companies operating in the global microbial food colors market include ADM, Givaudan, Sensient Technologies, Dohler, Kerry Group, DSM-Firmenich, Chr. Hansen (Oterra), GNT Group, Kalsec, Lycored, Roha Dyechem, Chenguang Biotech, Allied Biotech, Synthite Industries, and AVT Natural Products. Companies operating in the microbial food colors market are adopting several strategic initiatives to strengthen their competitive position and expand market presence. Product innovation remains a key focus area, with manufacturers investing in advanced fermentation technologies to improve pigment yield, stability, color intensity, and cost efficiency. Companies are also expanding their portfolios of natural color solutions to meet evolving customer requirements across food, beverage, and nutritional product applications. Strategic collaborations, partnerships, and acquisitions are being utilized to strengthen technological capabilities and broaden geographic reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Pigment type

- 2.2.3 Source

- 2.2.4 Form

- 2.2.5 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By pigment type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Pigment Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Carotenoids

- 5.3 Anthocyanins & flavonoids

- 5.4 Phycobiliproteins

- 5.5 Riboflavin

- 5.6 Prodigiosin & violacein

- 5.7 Melanin & others

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Bacteria-derived

- 6.3 Fungi-derived

- 6.4 Yeast-derived

- 6.5 Microalgae-derived

Chapter 7 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Liquid

- 7.3 Powder

- 7.4 Gel

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Beverages

- 8.2.1 Carbonated drinks

- 8.2.2 Juices & fruit drinks

- 8.2.3 Energy & sports drinks

- 8.2.4 Alcoholic beverages

- 8.3 Bakery & confectionery

- 8.3.1 Baked goods

- 8.3.2 Ice cream & frozen desserts

- 8.3.3 Candies & sweets

- 8.4 Dairy products

- 8.4.1 Yogurt

- 8.4.2 Milk-based drinks

- 8.4.3 Baby foods

- 8.4.4 Cheese & butter

- 8.5 Processed foods

- 8.5.1 Sauces & condiments

- 8.5.2 Ready meals

- 8.5.3 Snack foods

- 8.6 Meat, poultry & seafood

- 8.6.1 Meat colorants

- 8.6.2 Aquaculture feed

- 8.6.3 Poultry feed

- 8.7 Dietary supplements

- 8.7.1 Nutraceuticals

- 8.7.2 Health supplements

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Chr. Hansen (Oterra)

- 10.2 Sensient Technologies

- 10.3 GNT Group

- 10.4 DSM-Firmenich

- 10.5 ADM

- 10.6 Kerry Group

- 10.7 Dohler

- 10.8 Givaudan

- 10.9 Kalsec

- 10.10 Roha Dyechem

- 10.11 Lycored

- 10.12 Chenguang Biotech

- 10.13 Allied Biotech

- 10.14 Synthite Industries

- 10.15 AVT Natural Products