|

市場調查報告書

商品編碼

2061493

頭孢菌素類藥物市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測Cephalosporin Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

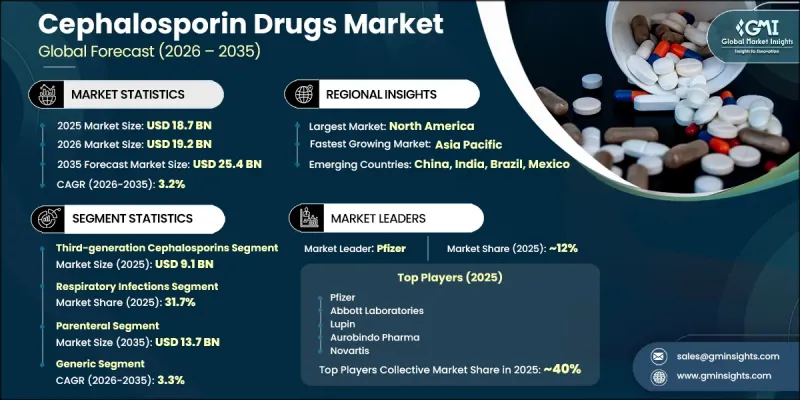

預計到 2025 年,全球頭孢菌素類藥物市場價值將達到 187 億美元,並有望以 3.2% 的複合年成長率成長,到 2035 年達到 254 億美元。

該市場成長的主要促進因素是全球細菌感染疾病率的上升、住院率的增加以及對頻譜抗生素治療的持續需求。頭孢菌素是一類重要的BETA-內醯胺類抗生素,廣泛用於治療多種細菌感染疾病,其作用機轉是透過抑制細菌細胞壁合成來殺死細菌。根據其對革蘭氏陽性菌和革蘭氏陰性菌的抗菌頻譜,這些藥物被分為多代。早期藥物通常用於治療簡單的皮膚和軟組織感染疾病,而新一代藥物常用於治療較嚴重的病例,例如院內感染、腦膜炎、肺炎和多重病菌感染。此類別中常用的藥物包括頭孢曲松、頭孢吡肟、Cefuroxime、頭孢克肟、頭孢Cefazolin和頭孢他啶。日益嚴重的全球抗菌素抗藥性問題持續推動對高效抗生素治療的需求。同時,醫療保健服務的可近性提高和藥品生產能力的擴大進一步加速了開發中國家的市場滲透。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 187億美元 |

| 預測市場規模 | 254億美元 |

| 複合年成長率 | 3.2% |

第三代頭孢菌素市場預計到2025年將達到91億美元。該細分市場憑藉其強大的廣譜抗菌活性、經證實對革蘭氏陰性菌有效的臨床療效以及在醫院感染控制中的廣泛應用,保持著市場主導地位。此類藥物因其組織穿透性高和安全性良好,被廣泛應用於重症監護和住院患者護理。住院率的上升和抗藥性的增加進一步推動了對先進頭孢菌素治療方法的需求,尤其是在重症監護環境中,快速有效的感染控制至關重要。

預計到2025年,呼吸道感染疾病領域將佔全球市場佔有率的31.7%。這一主導地位主要歸因於細菌性呼吸道疾病(包括肺炎、支氣管炎、鼻竇炎和其他需要有效抗菌治療的下呼吸道感染疾病)在全球範圍內的高發生率。呼吸道感染疾病仍然是全球主要的死亡原因之一,尤其是在嬰幼兒和老年人群中,這進一步凸顯了整個醫療保健系統對頭孢菌素類治療方法的持續需求。

預計到2025年,北美頭孢菌素市佔率將達到39.4%。該地區持續保持主導地位,主要得益於其細菌感染疾病的高發生率、先進的醫療基礎設施以及在住院和門診環境中廣泛使用頻譜抗生素。完善的醫院網路和便利的治療服務進一步支撐了該地區的需求。美國擁有龐大的患者群體和完善的臨床治療體系,該體系高度依賴抗生素療法進行感染疾病控制,因此在推動消費方面發揮重要作用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 感染疾病增加

- 手術數量增加

- 擴大使用新一代頭孢菌素

- 產業潛在風險與挑戰

- 抗生素抗藥性增強

- 嚴格的法律規範

- 替代抗生素類別的可用性

- 市場機遇

- 聯合治療的開發

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術展望

- 最新科技趨勢

- 新興技術

- 波特的分析

- PESTLE分析

- 價格分析

- 對過去價格趨勢的分析

- 代際定價策略

- 管線分析和臨床試驗趨勢

- 未來市場趨勢

- 投資與資金籌措分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依世代分類,2022-2035年

- 第一代頭孢菌素

- 第二代頭孢菌素

- 第三代頭孢菌素

- 第四代頭孢菌素

- 第五代頭孢菌素

第6章 市場估計與預測:依適應症分類,2022-2035年

- 呼吸道感染疾病

- 尿道感染(UTI)

- 皮膚和軟組織感染疾病

- 性行為感染感染(STI)

- 胃腸道感染疾病

- 其他改編

第7章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 腸外

- 外用

第8章 市場估算與預測:依藥物類型分類,2022-2035年

- 品牌

- 非專利的

第9章 市場估價與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第11章:公司簡介

- AbbVie

- Abbott Laboratories

- Aurobindo Pharma

- Baxter

- Cipla

- Fresenius Kabi

- GlaxoSmithKline

- Hikma Pharmaceuticals

- Lupin

- Macleods Pharmaceuticals

- Mankind Pharma

- Novartis

- Pfizer

- Shionogi

- Sun Pharmaceutical

- Teva Pharmaceutical Industries

- Zydus Lifesciences

The Global Cephalosporin Drugs Market was valued at USD 18.7 billion in 2025 and is estimated to grow at a CAGR of 3.2% to reach USD 25.4 billion by 2035.

The market growth is primarily supported by the rising incidence of bacterial infections worldwide, increasing hospitalization rates, and sustained demand for broad-spectrum antibiotic therapies. Cephalosporins represent a major class of beta-lactam antibiotics widely used to treat diverse bacterial infections by disrupting bacterial cell wall synthesis, which leads to bacterial cell death. These drugs are structured into multiple generations based on their spectrum of activity against gram-positive and gram-negative organisms. Earlier-generation drugs are commonly prescribed for uncomplicated skin and soft tissue infections, while advanced-generation variants are frequently used in more severe conditions such as hospital-acquired infections, meningitis, pneumonia, and multidrug-resistant bacterial cases. High-usage medications within this category include ceftriaxone, cefepime, cefuroxime, cefixime, cefazolin, and ceftazidime. The expanding global burden of antimicrobial resistance continues to push demand for improved antibiotic therapies, while rising healthcare access and growing pharmaceutical production capacity are further strengthening market penetration across developing and developed regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18.7 Billion |

| Forecast Value | $25.4 Billion |

| CAGR | 3.2% |

The third-generation cephalosporins segment generated USD 9.1 billion in 2025. This segment maintains its dominant position due to its strong broad-spectrum antimicrobial activity, proven clinical effectiveness against gram-negative pathogens, and widespread use in hospital-based infection management. Drugs within this category are extensively utilized in intensive care and inpatient settings due to their strong tissue penetration and favorable safety profile. Increased hospitalization rates and the growing incidence of resistant bacterial strains are further reinforcing demand for advanced cephalosporin-based therapies, particularly in critical care environments where rapid and effective infection control is essential.

The respiratory infections segment accounted for 31.7% share in 2025. This dominance is attributed to the high global burden of bacterial respiratory diseases, including pneumonia, bronchitis, sinus infections, and other lower respiratory tract infections that require effective antimicrobial treatment. Respiratory infections remain a leading cause of mortality globally, particularly among young children and elderly populations, further supporting sustained demand for cephalosporin-based treatment options across healthcare systems.

North America Cephalosporin Drugs Market held a 39.4% share in 2025. The region continues to lead due to a high prevalence of bacterial infections, advanced healthcare infrastructure, and extensive use of broad-spectrum antibiotics across both inpatient and outpatient settings. Strong hospital networks and high treatment accessibility further support regional demand. The United States plays a key role in driving consumption due to the large patient base and well-established clinical treatment frameworks that rely heavily on antibiotic therapies for infection management.

Key companies operating in the Cephalosporin Drugs Industry include AbbVie, Abbott Laboratories, Aurobindo Pharma, Baxter, Cipla, Fresenius Kabi, GlaxoSmithKline, Hikma Pharmaceuticals, Lupin, Macleods Pharmaceuticals, Mankind Pharma, Novartis, Pfizer, Shionogi, Sun Pharmaceutical, Teva Pharmaceutical Industries, and Zydus Lifesciences. Companies operating in the cephalosporin drugs market are focusing on multiple strategic initiatives to strengthen their global presence and enhance competitiveness. Leading players are investing in research and development to introduce improved formulations and combination therapies that address rising antimicrobial resistance. Strategic partnerships, licensing agreements, and manufacturing expansions are helping companies strengthen supply chains and expand geographic reach. Firms are also prioritizing regulatory approvals for new and generic antibiotic products to accelerate market entry and increase accessibility. In addition, expansion of production capabilities in cost-efficient regions is supporting improved profitability and supply stability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Generation trends

- 2.2.3 Indication trends

- 2.2.4 Route of administration trends

- 2.2.5 Drug type trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of infectious diseases

- 3.2.1.2 Growing number of surgical procedures

- 3.2.1.3 Increasing use of advanced-generation cephalosporins

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Rising antimicrobial resistance

- 3.2.2.2 Stringent regulatory oversight

- 3.2.2.3 Availability of alternative antibiotic classes

- 3.2.3 Market opportunities

- 3.2.3.1 Development of combination therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by Primary Research)

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy, by generation

- 3.9 Pipeline analysis and clinical trial landscape

- 3.10 Future market trends (Driven by primary research)

- 3.11 Investment & funding analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Generation, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 First generation cephalosporins

- 5.3 Second generation cephalosporins

- 5.4 Third generation cephalosporins

- 5.5 Fourth generation cephalosporins

- 5.6 Fifth generation cephalosporins

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Respiratory infections

- 6.3 Urinary tract infections (UTIs)

- 6.4 Skin and soft tissue infections

- 6.5 Sexually transmitted infections (STIs)

- 6.6 Gastrointestinal infections

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Parenteral

- 7.4 Topical

Chapter 8 Market Estimates and Forecast, By Drug Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Branded

- 8.3 Generic

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Abbott Laboratories

- 11.3 Aurobindo Pharma

- 11.4 Baxter

- 11.5 Cipla

- 11.6 Fresenius Kabi

- 11.7 GlaxoSmithKline

- 11.8 Hikma Pharmaceuticals

- 11.9 Lupin

- 11.10 Macleods Pharmaceuticals

- 11.11 Mankind Pharma

- 11.12 Novartis

- 11.13 Pfizer

- 11.14 Shionogi

- 11.15 Sun Pharmaceutical

- 11.16 Teva Pharmaceutical Industries

- 11.17 Zydus Lifesciences

頭孢菌素類藥物市場:2026-2032年全球市場預測(依藥物類別、給藥途徑、劑型、應用、最終用戶及通路分類)

頭孢菌素類藥物市場:2026-2032年全球市場預測(依藥物類別、給藥途徑、劑型、應用、最終用戶及通路分類) 頭孢菌素市場規模、佔有率、趨勢和預測:按代、給藥途徑、應用和地區分類(2026-2034 年)

頭孢菌素市場規模、佔有率、趨勢和預測:按代、給藥途徑、應用和地區分類(2026-2034 年) 頭孢菌素類藥物市場:依代、類型、劑型、適應症、通路及地區分類。頭孢菌素C醯化酶市場按產品類型、來源、形式、純度等級、技術、應用和最終用途產業分類-2026-2032年全球預測

頭孢菌素類藥物市場:依代、類型、劑型、適應症、通路及地區分類。頭孢菌素C醯化酶市場按產品類型、來源、形式、純度等級、技術、應用和最終用途產業分類-2026-2032年全球預測 全球頭孢菌素市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考量因素以及未來預測(2026-2034)

全球頭孢菌素市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考量因素以及未來預測(2026-2034) 頭孢菌素藥物市場,按代、按類型、按配方、按適應症、按配銷通路和按地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

頭孢菌素藥物市場,按代、按類型、按配方、按適應症、按配銷通路和按地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測