|

市場調查報告書

商品編碼

2061486

獸醫自體免疫疾病治療市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測Veterinary Autoimmune Disease Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

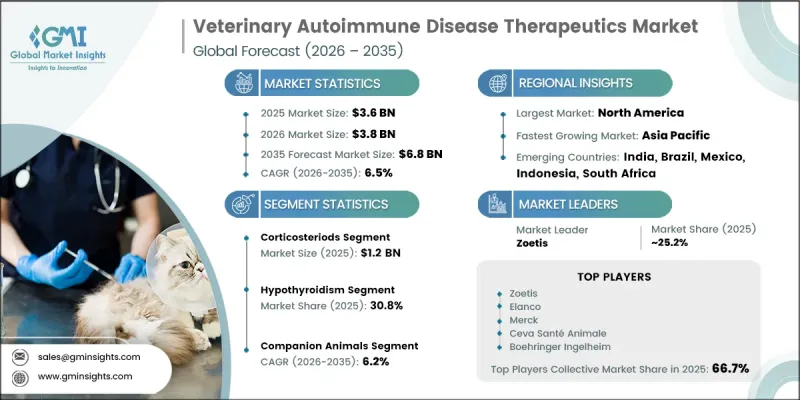

2025 年全球獸醫自體免疫疾病治療市場價值為 36 億美元,預計到 2035 年將以 6.5% 的複合年成長率成長至 68 億美元。

全球寵物飼養量的成長以及動物自體自體免疫疾病發生率的上升推動了市場成長。獸醫自體免疫疾病治療的重點在於控制免疫系統錯誤攻擊健康組織的疾病,這類疾病需要長期醫療介入。治療方法主要包括免疫抑制劑、皮質類固醇和生物製藥,旨在控制免疫介導性貧血、紅斑性狼瘡和天皰瘡等疾病。隨著寵物「人性化」趨勢的加劇,對先進和專業獸醫醫療解決方案的需求顯著成長。同時,製藥公司和研究機構正加強合作,以擴大創新治療方法的可近性並改善治療效果。標靶生物製劑和單株抗體研究的進展進一步加速了該領域治療方法的創新。此外,由於人們越來越傾向於更環保、更安全的配方,市場正逐漸轉向天然和永續的替代治療方法。法規結構的加強和研發投入的增加正在縮短產品開發週期。此外,對品種和疾病特異性治療方法的需求不斷成長,推動了全球市場更個人化的獸醫方法的發展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 36億美元 |

| 預計金額 | 68億美元 |

| 複合年成長率 | 6.5% |

預計到2025年,皮質類固醇市場規模將達到12億美元,到2035年將達到22億美元,年複合成長率(CAGR)為6.4%。此細分市場的主導地位得益於其快速的治療效果、成本效益以及對多種動物自體免疫疾病的廣泛適用性。由於皮質類固醇治療方法能夠快速抑制過度免疫反應並減輕炎症,因此仍然是獸醫學中的基礎治療選擇。這些治療方法廣泛用於治療免疫介導性關節炎、自體免疫貧血和內分泌相關免疫功能障礙等疾病,在這些疾病的治療中,免疫調節至關重要。

預計到2025年,甲狀腺機能低下症症將佔所有病例的30.8%,成為伴侶動物中最常見的自體免疫疾病之一。這種疾病在犬類中特別常見,其原因是免疫功能異常,導致甲狀腺功能失調,進而造成荷爾蒙分泌減少。患病動物常出現疲勞、體重增加和皮膚問題等症狀。鑑於該疾病的高發生率,目前正在研發針對性治療方法,旨在恢復荷爾蒙平衡,改善寵物的長期健康狀況。

預計到2025年,北美獸醫自體免疫疾病治療市場佔有率將達42.3%。該地區的領先地位得益於其較高的寵物擁有率、完善的醫療保健體係以及人們對動物自體免疫疾病日益成長的認知。龐大的伴侶動物數量,尤其是犬貓,推動了狼瘡和免疫介導性溶血性貧血等疾病的高診斷率。全部區域的先進獸醫醫院和診所網路能夠實現疾病的早期發現和有效管理。此外,寵物保險的日益普及和個人化獸醫診療方法的日益廣泛應用也進一步推動了市場的擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 通用感染疾病在人與人之間傳播的風險增加

- 牲畜自體免疫疾病發生率增加

- 提高對自體免疫疾病的認知與診斷

- 寵物數量增加

- 動物醫療保健支出增加

- 產業潛在風險與挑戰

- 獸醫自體免疫療法高成本

- 自體免疫藥物會增加感染風險

- 市場機遇

- 對品種特異性和個人化治療的需求日益成長

- 遠端醫療和遠距獸醫診斷的發展

- 促進因素

- 成長潛力分析

- 技術展望

- 目前技術

- 新興技術

- 價格分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

第5章 市場估計與預測:依治療類型分類,2022-2035年

- 皮質類固醇

- Azathioprine

- Cyclosporine

- 黴酚酸

- 來氟米德

- Cyclophosphamide

- 左甲狀腺素

- 葉酸

- 羥氯喹

- Chloroquine

第6章 市場估計與預測:依疾病分類,2022-2035年

- 甲狀腺機能低下症

- 天皰瘡

- 犬類狼瘡

- 自體免疫溶血性貧血

- 水痘天皰瘡

- 盤狀紅斑狼瘡(DLE)

- 免疫相關性關節炎

- 其他疾病

第7章 市場估計與預測:依動物類型分類,2022-2035年

- 伴侶動物

- 狗

- 貓

- 馬

- 其他伴侶動物

- 家畜

- 牛

- 豬

- 家禽

- 羊

- 其他牲畜

- 其他動物

第8章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 注射藥物

- 外用

第9章 市場估價與預測:依通路分類,2022-2035年

- 動物醫院

- 動物診所

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第11章:公司簡介

- Animalcare group

- Bimeda

- Boehringer Ingelheim

- Ceva Sante Animal

- Dechra Pharmaceuticals

- Dopharma

- Elanco

- Merck Animal Health

- Norbrook

- Vetoquinol

- Virbac

- Zoetis

The Global Veterinary Autoimmune Disease Therapeutics Market was valued at USD 3.6 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 6.8 billion by 2035.

Market growth is driven by the rising incidence of autoimmune conditions in animals alongside increasing global adoption of companion pets. Veterinary autoimmune disease therapeutics focus on managing disorders in which the immune system mistakenly attacks healthy tissues, requiring long-term medical intervention. Treatment options primarily include immunosuppressive agents, corticosteroid-based therapies, and biologics designed to control conditions such as immune-mediated anemia, lupus, and pemphigus. Growing pet humanization trends are significantly increasing demand for advanced and specialized veterinary care solutions. At the same time, pharmaceutical companies and research organizations are increasingly collaborating to expand access to innovative therapies and improve treatment outcomes. Advancements in targeted biologics and monoclonal antibody research are further accelerating therapeutic innovation in this space. The market is also experiencing a gradual shift toward natural and sustainable treatment alternatives, driven by rising preference for eco-conscious and safer formulations. Strengthened regulatory frameworks and higher research investments are supporting faster product development cycles. Additionally, increasing demand for breed-specific and condition-specific therapies is encouraging the development of more personalized veterinary treatment approaches across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.6 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 6.5% |

The corticosteroids segment reached USD 1.2 billion in 2025 and is expected to reach USD 2.2 billion by 2035, growing at a CAGR of 6.4%. This segment's dominance is supported by its rapid therapeutic action, cost-effectiveness, and broad applicability across multiple autoimmune conditions in animals. Corticosteroid-based treatments remain a foundational option in veterinary care due to their ability to quickly suppress immune overactivity and reduce inflammation. These therapies are widely used in managing disorders such as immune-mediated arthritis, autoimmune anemia, and endocrine-related immune dysfunctions, where immune modulation is critical for disease control.

The hypothyroidism segment accounted for 30.8% share in 2025, making it one of the most prevalent autoimmune conditions treated in companion animals. This disorder is especially common in dogs and occurs when immune dysfunction disrupts normal thyroid activity, leading to reduced hormone production. Symptoms such as fatigue, weight gain, and dermatological complications are frequently observed in affected animals. The high occurrence rate has encouraged the development of targeted therapeutic approaches aimed at restoring hormonal balance and improving long-term health outcomes in pets.

North America Veterinary Autoimmune Disease Therapeutics Market held a 42.3% share in 2025. The region's dominance is supported by high pet ownership rates, a well-developed veterinary healthcare system, and increasing awareness of autoimmune disorders in animals. The large population of companion animals, particularly dogs and cats, contributes to higher diagnosis rates for conditions such as lupus and immune-mediated hemolytic anemia. Advanced veterinary clinics and hospitals across the region enable early detection and effective disease management. In addition, the growing penetration of pet insurance and the rising adoption of personalized veterinary care approaches are further supporting market expansion.

Key companies operating in the Global Veterinary Autoimmune Disease Therapeutics Market include Zoetis, Elanco, Merck Animal Health, Boehringer Ingelheim, Virbac, Dechra Pharmaceuticals, Vetoquinol, Ceva Sante Animale, Animalcare Group, Norbrook, Bimeda, and Dopharma. Companies in the veterinary autoimmune disease therapeutics market are focusing on expanding their product portfolios through the development of advanced immunomodulatory therapies that offer improved safety and efficacy profiles. A key strategy involves strengthening research and development capabilities to accelerate the introduction of targeted biologics and next-generation monoclonal antibody treatments. Firms are also pursuing strategic collaborations with veterinary research institutes and academic organizations to enhance clinical innovation and improve disease understanding. Geographic expansion into emerging pet care markets is being prioritized to capture rising demand for specialized veterinary services. Companies are further investing in sustainable and natural formulation development to align with changing consumer preferences for eco-friendly products. Strengthening distribution networks and expanding partnerships with veterinary clinics and hospitals are also central to improving product accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Therapy type trends

- 2.2.3 Disease trends

- 2.2.4 Animal type trends

- 2.2.5 Route of administration trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing threat of transfer of zoonotic diseases among humans

- 3.2.1.2 Rising incidence of autoimmune diseases in livestock animals

- 3.2.1.3 Increasing awareness and diagnosis of autoimmune diseases

- 3.2.1.4 Growing companion animal ownership

- 3.2.1.5 Increasing expenditure on animal healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of veterinary autoimmune therapies

- 3.2.2.2 Increase risk of infection due to autoimmune drugs

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for breed-specific and personalized treatments

- 3.2.3.2 Growth in telemedicine and remote veterinary diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technology

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.6 Regulatory landscape (Driven by primary research)

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends (Driven by primary research)

- 3.10 Impact of AI and generative AI on the market (Driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Therapy Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Corticosteroids

- 5.3 Azathioprine

- 5.4 Cyclosporine

- 5.5 Mycophenolate

- 5.6 Leflunomide

- 5.7 Cyclophosphamide

- 5.8 Levothyroxine

- 5.9 Folic acid

- 5.10 Hydroxychloroquine

- 5.11 Chloroquine

Chapter 6 Market Estimates and Forecast, By Disease, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hypothyroidism

- 6.3 Pemphigus disease

- 6.4 Canine lupus

- 6.5 Autoimmune haemolytic anaemia

- 6.6 Bullous pemphigoid

- 6.7 Discoid lupus erythematosus (DLE)

- 6.8 Immune-related arthritis

- 6.9 Other diseases

Chapter 7 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Companion animals

- 7.2.1 Dogs

- 7.2.2 Cats

- 7.2.3 Horses

- 7.2.4 Other companion animals

- 7.3 Livestock animals

- 7.3.1 Cattle

- 7.3.2 Swine

- 7.3.3 Poultry

- 7.3.4 Sheep

- 7.3.5 Other livestock animals

- 7.4 Other animals

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Injectable

- 8.4 Topical

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospitals

- 9.3 Veterinary clinics

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Animalcare group

- 11.2 Bimeda

- 11.3 Boehringer Ingelheim

- 11.4 Ceva Sante Animal

- 11.5 Dechra Pharmaceuticals

- 11.6 Dopharma

- 11.7 Elanco

- 11.8 Merck Animal Health

- 11.9 Norbrook

- 11.10 Vetoquinol

- 11.11 Virbac

- 11.12 Zoetis

寵物健康與營養快速消費品市場預測至2034年-按產品類型、寵物品種、原料類型、分銷管道和最終用戶分類的全球分析

寵物健康與營養快速消費品市場預測至2034年-按產品類型、寵物品種、原料類型、分銷管道和最終用戶分類的全球分析 獸醫保健市場規模、佔有率和成長分析:按動物類型、服務類型、產品類型、應用、最終用戶和地區分類-2026-2033年產業預測寵物健康資料平台市場預測至2034年-全球分析(按平台類型、組件、資料類型、目標動物、整合生態系統、經營模式、應用、最終用戶和地區分類)寵物心理健康市場預測至2034年-按產品類型、適應症、動物種類、通路和地區分類的全球分析多通道動物麻醉設備市場預測至 2034 年—按類型、目標動物、應用和地區進行全球分析。

獸醫保健市場規模、佔有率和成長分析:按動物類型、服務類型、產品類型、應用、最終用戶和地區分類-2026-2033年產業預測寵物健康資料平台市場預測至2034年-全球分析(按平台類型、組件、資料類型、目標動物、整合生態系統、經營模式、應用、最終用戶和地區分類)寵物心理健康市場預測至2034年-按產品類型、適應症、動物種類、通路和地區分類的全球分析多通道動物麻醉設備市場預測至 2034 年—按類型、目標動物、應用和地區進行全球分析。 動物用藥品活性成分市場:依動物種類、產品類型、化合物類型、原料、應用及最終用戶分類-2026-2032年全球市場預測

動物用藥品活性成分市場:依動物種類、產品類型、化合物類型、原料、應用及最終用戶分類-2026-2032年全球市場預測 獸醫保健市場規模、佔有率、趨勢和預測:按產品類型、動物種類、最終用戶和地區分類(2026-2034 年)

獸醫保健市場規模、佔有率、趨勢和預測:按產品類型、動物種類、最終用戶和地區分類(2026-2034 年) 動物血液製品市場:依產品類型、最終用戶、供血動物、通路和地區分類全球禽流感市場:依病毒類型、檢測類型、治療類型、動物類型和地區分類獸醫護理市場:按動物類型、服務類型、執業模式、最終用戶和通路類型分類-2026-2032年全球市場預測

動物血液製品市場:依產品類型、最終用戶、供血動物、通路和地區分類全球禽流感市場:依病毒類型、檢測類型、治療類型、動物類型和地區分類獸醫護理市場:按動物類型、服務類型、執業模式、最終用戶和通路類型分類-2026-2032年全球市場預測