|

市場調查報告書

商品編碼

2061481

慢燉鍋市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。Slow Cooker Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

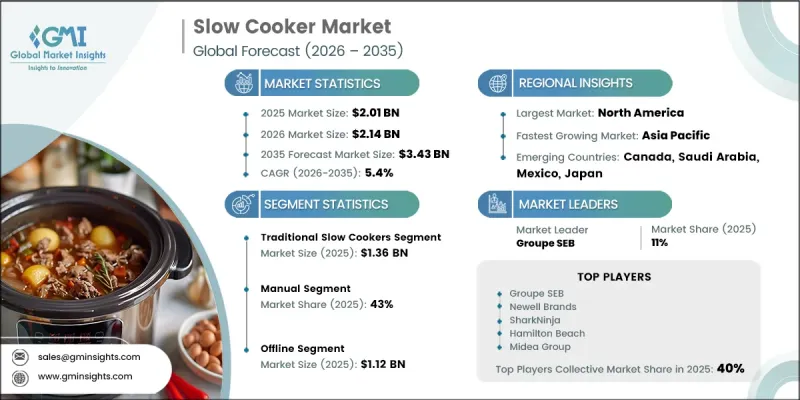

預計到 2025 年,全球慢燉鍋市場價值將達到 20.1 億美元,年複合成長率為 5.4%,到 2035 年將達到 34.3 億美元。

消費者對便利型廚房電器的日益偏好是推動市場擴張的主要動力,尤其是在繁忙的都市區中。消費者越來越傾向於選擇能夠簡化備餐流程、減少烹飪過程中持續監控需求的電器。慢燉鍋因其食材預先準備好後即可自動長時間烹飪,且只需極少人工干預而廣受歡迎。這項功能對上班族、雙薪家庭以及尋求省時省力實用烹飪方案的消費者極具吸引力。此外,大量烹飪和膳食計劃等烹飪習慣的改變也促進了市場成長。消費者擴大一次烹飪大量食物,以減少烹飪次數,更有效地安排每週的膳食。這些生活方式和飲食習慣的改變持續推動著慢燉鍋在全球住宅的普及。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 20.1億美元 |

| 預計金額 | 34.3億美元 |

| 複合年成長率 | 5.4% |

預計到2025年,傳統慢燉鍋市場規模將達到13.6億美元。由於其價格實惠、性能可靠且功能簡單,這一細分市場仍然是慢燉鍋行業的基石。傳統型號通常具備「低溫」、「高溫」和「保溫」等基本加熱設置,無需複雜的數位控制或編程功能即可進行長時間烹飪。其簡潔易用的特點持續吸引著那些喜歡使用簡單廚房電器進行日常烹飪的消費者。

2025年,手動操作型慢燉鍋市佔率達43%。由於其經典的設計和便利的操作,手動慢燉鍋仍保持著強勁的市場需求。這類產品通常配備旋轉撥盤或簡單的開關,方便使用者快速輕鬆地選擇預設溫度。對於偏好傳統烹飪方式且不需要高級數位介面或可程式設計系統的消費者而言,其簡潔的功能仍然極具吸引力。

美國慢燉鍋市佔率高達87.8%,預計2025年市場規模將達7.6億美元。美國市場成長的主要驅動力是產品更換、產品升級以及尖端技術與傳統廚房電器的融合。美國消費者對多功能、便利的廚房產品持續表現出濃厚的興趣,這推動了智慧慢燉鍋和混合型廚房電器需求的成長。此外,人們對居家烹飪、健康飲食習慣和計劃性膳食準備的日益重視,也促進了這些產品在家庭中的穩定普及。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 簡單省時的烹調方法

- 智慧廚房電器的日益普及

- 轉向家庭烹飪

- 產業潛在風險與挑戰

- 長時間烹調的限制

- 對能源消耗的擔憂

- 機會

- 與智慧家庭生態系統整合

- 永續性和節能模式

- 促進因素

- 成長潛力分析

- 監理框架

- 能源效率標準和認證

- 產品安全法規(UL、CE、FDA)

- 環境合規性與RoHS指令

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 區域價格波動

- 貿易資料分析(8516.79)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 區域貿易流量模式

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 目前分銷基礎設施和通路滲透情況

- 按地區與業態(現代零售與傳統零售)分類的通路覆蓋率

- 缺乏最後一公里基礎設施和不斷變化的管道

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 傳統慢燉鍋

- 慢燉鍋用於褐變

第6章 市場估計與預測:按控制方法,2022-2035年

- 手動的

- 數位的

- 聰明的

第7章 市場估計與預測:依產能分類,2022-2035年

- 小號(1-3誇脫)

- 中等大小(4-6誇脫)

- 大容量(7誇脫或以上)

第8章 市場估算與預測:依價格區間分類,2022-2035年

- 預算/經濟型(50 美元以下)

- 中階(50-150美元)

- 高級/高階(超過 150 美元)

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 住宅/房屋

- 商業

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 超級市場

- 專賣店

- 其他(例如,個體商店)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第12章:公司簡介

- 世界公司

- Newell Brands

- Hamilton Beach

- Groupe SEB

- KitchenAid

- Breville Group

- SharkNinja

- Midea Group

- 當地公司

- Bajaj Electricals

- De'Longhi Group

- Sunbeam Products

- Cuisinart

- Lakeland

- Galanz

- NESCO

- 新興企業

- Sub-Zero Group(Wolf Gourmet)

- Chefman

- Elite Gourmet

- Gourmia

- West Bend

- Oster

- Bella

The Global Slow Cooker Market was valued at USD 2.01 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 3.43 billion by 2035.

Rising consumer preference for convenience-oriented kitchen appliances is one of the major factors supporting market expansion, particularly among urban households with fast-paced lifestyles. Consumers increasingly favor appliances that simplify meal preparation and reduce the need for continuous supervision during cooking. Slow cookers have gained strong popularity because they allow users to prepare ingredients in advance and let the appliance complete the cooking process automatically over extended periods with minimal monitoring. This functionality strongly appeals to working professionals, dual-income households, and consumers seeking practical cooking solutions that save time and effort. In addition, evolving food preparation habits such as batch cooking and planned meal management are further contributing to market growth. Consumers are increasingly preparing meals in larger portions to reduce cooking frequency and better organize weekly meal schedules. These changing lifestyle and dietary patterns continue to strengthen the adoption of slow cookers across residential kitchens worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.01 Billion |

| Forecast Value | $3.43 Billion |

| CAGR | 5.4% |

Traditional slow cookers accounted for USD 1.36 billion in 2025. This segment remains the foundation of the slow cooker industry due to its affordability, reliability, and straightforward functionality. Traditional models are commonly equipped with basic heat settings such as low, high, and warm, allowing consumers to cook meals over long periods without requiring advanced digital controls or programming features. Their simplicity and ease of use continue to attract consumers who prefer uncomplicated kitchen appliances for everyday meal preparation.

The manual segment held a 43% share in 2025. Manual-control slow cookers continue to maintain strong market demand due to their classic design and user-friendly operation. These appliances generally feature rotary dials or simple switches that enable users to select preset temperature levels quickly and easily. Their uncomplicated functionality remains highly appealing among consumers who prefer traditional cooking methods and do not require advanced digital interfaces or programmable systems.

U.S. Slow Cooker Market held an 87.8% share, generating USD 0.76 billion in 2025. Market growth in the country is largely driven by replacement purchases, product upgrades, and increasing integration of modern technologies into conventional cooking appliances. Consumers in the U.S. continue to show strong interest in multifunctional and convenience-focused kitchen products, supporting rising demand for smart-enabled slow cookers and hybrid cooking appliances. Furthermore, growing interest in home cooking, healthier eating habits, and organized meal preparation practices continues to support steady product adoption across households.

Major players operating in the Global Slow Cooker Market include Hamilton Beach, Groupe SEB, Newell Brands, SharkNinja, KitchenAid, Breville Group, Midea Group, De'Longhi Group, Cuisinart, Sunbeam Products, Lakeland, Bajaj Electricals, NESCO, Galanz, West Bend, Bella, Gourmia, Elite Gourmet, Oster, Chefman, and Sub-Zero Group (Wolf Gourmet). Companies operating in the Slow Cooker Market are focusing on integrating smart technologies and multifunctional capabilities to enhance product appeal and improve user convenience. Manufacturers are introducing connected appliances with app-based controls, programmable cooking modes, and compatibility with smart home ecosystems. Product innovation centered on energy efficiency, compact designs, and versatile cooking functions is helping brands attract modern consumers with limited kitchen space and busy lifestyles. Companies are also expanding premium product portfolios featuring advanced safety systems, digital displays, and hybrid cooking technologies. Strategic partnerships with retail chains and e-commerce platforms are strengthening market visibility and distribution reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Control type

- 2.2.4 Capacity

- 2.2.5 Price range

- 2.2.6 End user

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Convenience & time-saving cooking

- 3.2.1.2 Rising popularity of smart kitchen appliances

- 3.2.1.3 Shift toward home cooking

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Long cooking time limitation

- 3.2.2.2 Energy consumption concerns

- 3.2.3 Opportunities

- 3.2.3.1 Integration with smart home ecosystems

- 3.2.3.2 Sustainability & energy-efficient models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 Energy efficiency standards & certifications

- 3.4.2 Product safety regulations (UL, CE, FDA)

- 3.4.3 Environmental compliance & RoHS directives

- 3.5 Pricing analysis

- 3.5.1 Historical price trend analysis (driven by primary research)

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.5.3 Regional price variations

- 3.6 Trade data analysis (driven by paid database) (8516.79)

- 3.6.1 Import/export volume & value trends

- 3.6.2 Key trade corridors & tariff impact

- 3.6.3 Regional trade flow patterns

- 3.7 Impact of AI & generative AI on the market

- 3.7.1 AI-driven disruption of existing business models

- 3.7.2 GenAI use cases & adoption roadmap by segment

- 3.7.3 Risks, limitations & regulatory considerations

- 3.8 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.8.1 Channel coverage by region & format (modern vs. traditional trade)

- 3.8.2 Last-mile infrastructure gaps & emerging channel shifts

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Traditional slow cookers

- 5.3 Searing slow cookers

Chapter 6 Market Estimates and Forecast, By Control Type, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Digital

- 6.4 Smart

Chapter 7 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Small (1-3 Quarts)

- 7.3 Medium (4-6 Quarts)

- 7.4 Large (7+ Quarts)

Chapter 8 Market Estimates and Forecast, By Price Range, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Budget/Economy (Under $50)

- 8.3 Mid-Range ($50-$150)

- 8.4 Premium/High-End (Above $150)

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Residential/Household

- 9.3 Commercial

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce

- 10.2.2 Company websites

- 10.3 Offline

- 10.3.1 Supermarkets

- 10.3.2 Specialty stores

- 10.3.3 Others (individual stores, etc.)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Newell Brands

- 12.1.2 Hamilton Beach

- 12.1.3 Groupe SEB

- 12.1.4 KitchenAid

- 12.1.5 Breville Group

- 12.1.6 SharkNinja

- 12.1.7 Midea Group

- 12.2 Regional players

- 12.2.1 Bajaj Electricals

- 12.2.2 De'Longhi Group

- 12.2.3 Sunbeam Products

- 12.2.4 Cuisinart

- 12.2.5 Lakeland

- 12.2.6 Galanz

- 12.2.7 NESCO

- 12.3 Emerging players

- 12.3.1 Sub-Zero Group (Wolf Gourmet)

- 12.3.2 Chefman

- 12.3.3 Elite Gourmet

- 12.3.4 Gourmia

- 12.3.5 West Bend

- 12.3.6 Oster

- 12.3.7 Bella