|

市場調查報告書

商品編碼

2061479

燃料電池無人機市場機會、成長要素、產業趨勢分析及2026-2035年預測Fuel Cell UAV Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

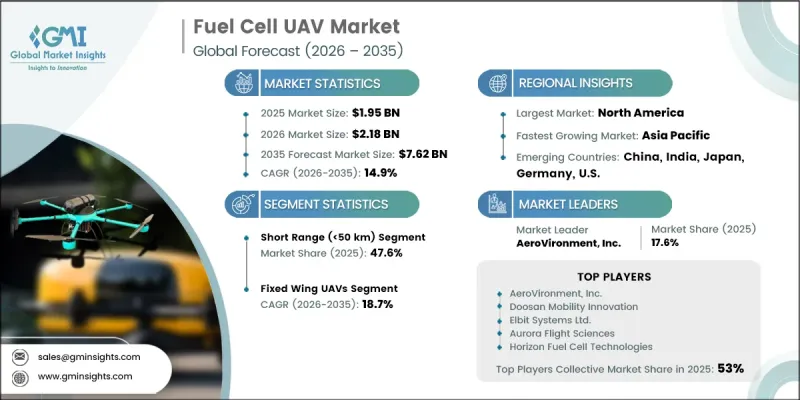

2025 年全球燃料電池無人機市場價值為 19.5 億美元,預計到 2035 年將以 14.9% 的複合年成長率成長,達到 76.2 億美元。

推動市場成長的因素包括:對長航時無人駕駛航空器系統的需求不斷成長、主要經濟體國防費用增加、氫燃料電池技術的持續進步以及商用無人機應用範圍的不斷擴大。與傳統的電池動力系統相比,燃料電池無人機的飛行時間顯著延長,使其在監測、測量、檢查、偵察和後勤保障等任務中極具吸引力。減少停機時間和提高任務效率的需求也推動了向更有效率、更永續的空中平台轉型。此外,各國政府和國防機構正在加大對下一代無人系統的投資,以增強情境察覺、邊境監控和情報收集能力。氫氣儲存、能量密度提升和輕量化系統整合的持續創新進一步促進了其應用。無人機與工業工作流程的日益融合,以及對高性能、永續運作的空中系統日益成長的需求,正在加速全球市場的擴張。這些因素共同促成了燃料電池無人機在不斷發展的無人機生態系統中的關鍵技術地位。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 19.5億美元 |

| 預測金額 | 76.2億美元 |

| 複合年成長率 | 14.9% |

燃料電池無人機市場也呈現強勁成長勢頭,主要得益於氫動力系統卓越的航程、運作效率和能源優勢。與電池充電相比,燃料電池無人機平台能夠更快地完成燃料加註,從而顯著減少停機時間,提高任務連續性和作戰準備狀態。隨著各組織機構日益重視遠程、長途飛行航空能力,燃料電池無人機正成為國防和商業應用領域的首選解決方案。系統整合和能源最佳化方面的持續改進進一步提升了效能和可靠性,增強了其在各個領域長期部署的前景。

預計到2025年,短程(50公里以下)無人機市佔率將達到47.6%。這主要得益於無人機在巡檢、農業監測、基礎設施評估和局部監測任務中的廣泛應用。這些無人機因其成本效益高、操作簡便且適用於短途任務而備受青睞。此外,無人機在商業和工業領域的應用不斷擴展,也持續推動該細分市場需求的穩定成長。

固定翼無人機市佔率高達48.6%,預計2026年至2035年將以18.7%的複合年成長率成長。這一市場主導地位主要得益於長時間空中作業(包括監測、偵察、測繪和保全監控等活動)日益成長的需求。與其他類型的無人機相比,固定翼平台具有更長的飛行時間、更高的能源效率和更廣泛的覆蓋範圍。國防領域的現代化建設不斷推進以及無人機在工業活動中的日益普及,也進一步推動了該細分市場的成長。

預計到2025年,北美燃料電池無人機市佔率將達到35%。該地區市場擴張的驅動力包括國防現代化項目投資的增加、各工業領域對先進無人駕駛航空器系統的日益普及,以及對遠程飛行能力無人機的強勁需求。此外,成熟的航太生態系統、持續的技術創新以及自主無人機解決方案的快速整合,也進一步推動了區域市場的成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 工業生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 長時間無人機作業的需求日益成長

- 加大國防和軍事對先進無人機技術的投資

- 氫燃料電池系統的技術進步

- 擴大永續和零排放航空解決方案的應用

- 拓展商用無人機在跨產業的應用

- 產業潛在風險與挑戰

- 高昂的基礎設施和氫氣儲存成本

- 引入氫動力無人機的技術與法規挑戰

- 市場機遇

- 擴大無人機在物流和貨物運輸的應用

- 擴大氫能經濟規模並投資清潔能源

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 技術與創新展望

- 最新科技趨勢

- 新技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- R&D

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基參與企業

- 戰略展望矩陣

- 併購

- 夥伴關係和聯盟

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 財務績效比較

- 新興企業競爭公司和新創企業的發展趨勢

第5章 市場估價與預測:依無人機類型分類,2022-2035年

- 固定翼無人機

- 微型UAV(負載容量5公斤或以下)

- 小型無人機(負載容量5-25公斤)

- 中型無人機(負載容量25-150公斤)

- 旋翼無人機

- 四旋翼/多旋翼飛行器(負載容量15公斤或以下)

- 單轉子(負載容量15-50kg)

- 大型(負載容量50公斤或以上)

- 混合動力垂直起降無人機

- 輕型垂直起降飛機(負載容量10公斤或以下)

- 大型垂直起降飛機(負載容量超過10公斤)

第6章 市場估計與預測:依範圍分類,2022-2035年

- 短距離(小於50公里)

- 中等距離(50-200公里)

- 長途(超過200公里)

第7章 市場估算與預測:依電力系統類型分類,2022-2035年

- 氫燃料電池系統

- PEM燃料電池

- SOFC

- 混合動力(燃料電池+電池)

- 電池供電系統

- 鋰離子電池(Li-ion)

- 鋰聚合物(LiPo)

- 其他

第8章 市場估算與預測:依最終用戶產業分類,2022-2035年

- 軍事/國防

- 情報與監視偵察(ISR)

- 訓練和射擊練習

- 電子戰和通訊中繼

- 搜救行動

- 其他

- 商業和工業

- 安全和周邊監控

- 關鍵基礎設施安全

- 工業設施邊界監測

- 活動人群監測

- 其他

- 航空測量/測繪

- 地形/地籍測量

- 礦山和採石場測繪

- 都市規劃與智慧城市應用

- 其他

- 資產檢查和維護

- 石油和天然氣基礎設施

- 可再生能源資產

- 通訊基礎設施

- 其他

- 配送/物流

- 藥物輸送

- 電子商務最後一公里配送

- 工業零件和工具的交付

- 其他

- 農業用途

- 農藥和化肥的施用

- 作物健康監測和病害檢測

- 精密農業和土壤分析

- 其他

- 環境監測

- 空氣品質和污染監測

- 災害應變和損失評估

- 其他

- 其他

- 安全和周邊監控

- 私人/政府

- 公共安全和緊急應變

- 交通監控管理

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球主要公司

- AeroVironment, Inc.

- Doosan Mobility Innovation

- Elbit Systems Ltd.

- Aurora Flight Sciences

- Horizon Fuel Cell Technologies

- 該地區的主要公司

- 北美洲

- Lockheed Martin Corporation

- The Boeing Company

- Northrop Grumman Corporation

- Textron Inc.

- 亞太地區

- Doosan Mobility Innovation

- H3 Dynamics Holdings Pte. Ltd.

- Horizon Fuel Cell Technologies

- 歐洲

- ISS Aerospace

- Elbit Systems Ltd.

- 北美洲

- 小眾參與企業和顛覆者

- Plug Power Inc.

- Ballard Power Systems Inc.

The Global Fuel Cell UAV Market was valued at USD 1.95 billion in 2025 and is estimated to grow at a CAGR of 14.9% to reach USD 7.62 billion by 2035.

Growth in this market is driven by rising demand for long-endurance unmanned aerial systems, increasing defense spending across major economies, continuous advancements in hydrogen fuel cell technologies, and the widening scope of commercial UAV applications. Fuel cell powered drones are gaining strong traction across surveillance, mapping, inspection, reconnaissance, and logistics-related missions due to their ability to deliver significantly longer flight durations compared to conventional battery powered systems. The shift toward more efficient and persistent aerial platforms is also being reinforced by the need for reduced operational downtime and improved mission efficiency. In addition, governments and defense organizations are increasingly investing in next-generation unmanned systems to enhance situational awareness, border monitoring, and intelligence capabilities. Ongoing technological innovation in hydrogen storage, energy density improvement, and lightweight system integration is further strengthening adoption. The growing integration of UAVs into industrial workflows, combined with the demand for high-performance aerial systems capable of sustained operations, continues to accelerate market expansion globally. These combined factors are positioning fuel cell UAVs as a critical technology within the evolving unmanned aerial ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.95 Billion |

| Forecast Value | $7.62 Billion |

| CAGR | 14.9% |

The fuel cell UAV market is also witnessing strong momentum due to the superior endurance, operational efficiency, and energy advantages offered by hydrogen-based propulsion systems. These platforms significantly reduce downtime by enabling faster refueling compared to battery charging cycles, which improves mission continuity and operational readiness. As organizations increasingly prioritize long-range, high-persistence aerial capabilities, fuel cell UAVs are becoming a preferred solution for both defense and commercial applications. Continuous improvements in system integration and energy optimization are further enhancing performance and reliability, strengthening long-term adoption prospects across multiple sectors.

The short-range (below 50 km) segment accounted for 47.6% share in 2025, driven by strong utilization across inspection activities, agricultural monitoring, infrastructure assessment, and localized surveillance missions. These UAVs are widely preferred due to their cost efficiency, simplified operational requirements, and suitability for short-distance missions. Their expanding use across commercial and industrial applications continues to support steady demand growth within this segment.

The fixed wing UAV segment held a 48.6% share and is projected to grow at a CAGR of 18.7% during 2026-2035. This dominance is supported by increasing demand for long-duration aerial operations, including surveillance, reconnaissance, mapping, and security monitoring activities. Fixed-wing platforms offer extended flight endurance, enhanced energy efficiency, and broader coverage capabilities compared to other UAV types. Growing defense modernization initiatives and the expanding use of UAVs in industrial operations are further reinforcing segment growth.

North America Fuel Cell UAV Market held a 35% share in 2025. Market expansion in the region is driven by rising investments in defense modernization programs, increased adoption of advanced unmanned aerial systems across industrial sectors, and strong demand for long-endurance drone capabilities. The presence of a well-established aerospace ecosystem, combined with continuous technological innovation and rapid integration of autonomous UAV solutions, is further supporting regional market growth.

Key companies operating in the Global Fuel Cell UAV Industry include AeroVironment, Inc., Doosan Mobility Innovation, Elbit Systems Ltd., Aurora Flight Sciences, Horizon Fuel Cell Technologies, ISS Aerospace, Israel Aerospace Industries (IAI), Lockheed Martin Corporation, The Boeing Company, Northrop Grumman Corporation, Textron Inc., General Dynamics Corporation, Plug Power Inc., Ballard Power Systems Inc., and H3 Dynamics Holdings Pte. Ltd. Companies operating in the fuel cell UAV market are adopting several strategic initiatives to strengthen their market position and expand their technological capabilities. A major focus is placed on research and development to improve hydrogen fuel efficiency, extend flight endurance, and enhance payload capacity. Firms are also investing in lightweight materials and advanced propulsion systems to improve overall UAV performance. Strategic collaborations with defense agencies, aerospace manufacturers, and energy technology providers are helping accelerate commercialization and expand application areas. Many players are also scaling production capabilities and strengthening supply chains to support growing demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Range trends

- 2.2.2 UAV type trends

- 2.2.3 Power System Type trends

- 2.2.4 End-user industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for long-endurance UAV operations

- 3.2.1.2 Rising defense and military investments in advanced UAV technologies

- 3.2.1.3 Technological advancements in hydrogen fuel cell systems

- 3.2.1.4 Growing adoption of sustainable and zero-emission aviation solutions

- 3.2.1.5 Expansion of commercial UAV applications across industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure and hydrogen storage costs

- 3.2.2.2 Technical and regulatory challenges in hydrogen-powered UAV deployment

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of UAVs in logistics and cargo delivery

- 3.2.3.2 Expansion of hydrogen economy and clean energy investments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By UAV Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Fixed Wing UAVs

- 5.2.1 Micro UAVs (<5 kg payload)

- 5.2.2 Small UAVs (5-25 kg payload)

- 5.2.3 Medium UAVs (25-150 kg payload)

- 5.3 Rotary Wing UAVs

- 5.3.1 Quadcopter/Multirotor (<15 kg payload)

- 5.3.2 Single Rotor (15-50 kg payload)

- 5.3.3 Heavy Lift (>50 kg payload)

- 5.4 Hybrid VTOL UAVs

- 5.4.1 Light VTOL (<10 kg payload)

- 5.4.2 Heavy VTOL (>10 kg payload)

Chapter 6 Market Estimates and Forecast, By Range, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Short Range (<50 km)

- 6.3 Medium Range (50-200 km)

- 6.4 Long Range (>200 km)

Chapter 7 Market Estimates and Forecast, By Power System Type, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Hydrogen Fuel Cell Systems

- 7.2.1 PEM Fuel Cell

- 7.2.2 SOFC

- 7.2.3 Hybrid (Fuel Cell + Battery)

- 7.3 Battery-Electric Systems

- 7.3.1 Lithium-Ion (Li-ion)

- 7.3.2 Lithium-Polymer (LiPo)

- 7.3.3 Others

Chapter 8 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Military & Defense

- 8.2.1 Intelligence, Surveillance & Reconnaissance (ISR)

- 8.2.2 Training & Target Practice

- 8.2.3 Electronic Warfare & Communications Relay

- 8.2.4 Search & Rescue (SAR) Operations

- 8.2.5 Others

- 8.3 Commercial & Industrial

- 8.3.1 Security & Perimeter Surveillance

- 8.3.1.1 Critical Infrastructure Security

- 8.3.1.2 Industrial Site Perimeter Monitoring

- 8.3.1.3 Event & Crowd Surveillance

- 8.3.1.4 Others

- 8.3.2 Aerial Mapping & Surveying

- 8.3.2.1 Topographic & Cadastral Mapping

- 8.3.2.2 Mining & Quarrying Site Mapping

- 8.3.2.3 Urban Planning & Smart City Applications

- 8.3.2.4 Others

- 8.3.3 Asset Inspection & Maintenance

- 8.3.3.1 Oil & Gas Infrastructure

- 8.3.3.2 Renewable Energy Assets

- 8.3.3.3 Telecom Infrastructure

- 8.3.3.4 Others

- 8.3.4 Delivery & Logistics

- 8.3.4.1 Medical & Pharmaceutical Delivery

- 8.3.4.2 E-commerce Last-Mile Delivery

- 8.3.4.3 Industrial Parts & Tools Delivery

- 8.3.4.4 Others

- 8.3.5 Agricultural Applications

- 8.3.5.1 Pesticide & Fertilizer Spraying

- 8.3.5.2 Crop Health Monitoring & Disease Detection

- 8.3.5.3 Precision Agriculture & Soil Analysis

- 8.3.5.4 Others

- 8.3.6 Environmental Monitoring

- 8.3.6.1 Air Quality & Pollution Monitoring

- 8.3.6.2 Disaster Response & Damage Assessment

- 8.3.6.3 Others

- 8.3.7 Others

- 8.3.1 Security & Perimeter Surveillance

- 8.4 Civil/Government

- 8.4.1 Public Safety & Emergency Response

- 8.4.2 Traffic Monitoring & Management

- 8.4.3 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 AeroVironment, Inc.

- 10.1.2 Doosan Mobility Innovation

- 10.1.3 Elbit Systems Ltd.

- 10.1.4 Aurora Flight Sciences

- 10.1.5 Horizon Fuel Cell Technologies

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Lockheed Martin Corporation

- 10.2.1.2 The Boeing Company

- 10.2.1.3 Northrop Grumman Corporation

- 10.2.1.4 Textron Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Doosan Mobility Innovation

- 10.2.2.2 H3 Dynamics Holdings Pte. Ltd.

- 10.2.2.3 Horizon Fuel Cell Technologies

- 10.2.3 Europe

- 10.2.3.1 ISS Aerospace

- 10.2.3.2 Elbit Systems Ltd.

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Plug Power Inc.

- 10.3.2 Ballard Power Systems Inc.

燃料電池無人機(UAV)全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

燃料電池無人機(UAV)全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 燃料電池無人機市場分析及預測(至2035年):類型、產品、技術、組件、應用、最終用戶、功能、安裝方式、解決方案

燃料電池無人機市場分析及預測(至2035年):類型、產品、技術、組件、應用、最終用戶、功能、安裝方式、解決方案 2026-2030年全球軍用無人機燃料電池市場

2026-2030年全球軍用無人機燃料電池市場 2026年全球氫能無人機集群動力市場報告

2026年全球氫能無人機集群動力市場報告 燃料電池動力無人機市場:2026-2032年全球市場預測(按燃料電池類型、無人機類型、功率、應用和最終用戶分類)

燃料電池動力無人機市場:2026-2032年全球市場預測(按燃料電池類型、無人機類型、功率、應用和最終用戶分類) 燃料電池無人機市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年

燃料電池無人機市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年 氫燃料電池無人機的全球市場:2030年為止的預測

氫燃料電池無人機的全球市場:2030年為止的預測