|

市場調查報告書

商品編碼

2061454

DNA合成市場機會、成長要素、產業趨勢分析及2026-2035年預測DNA Synthesis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

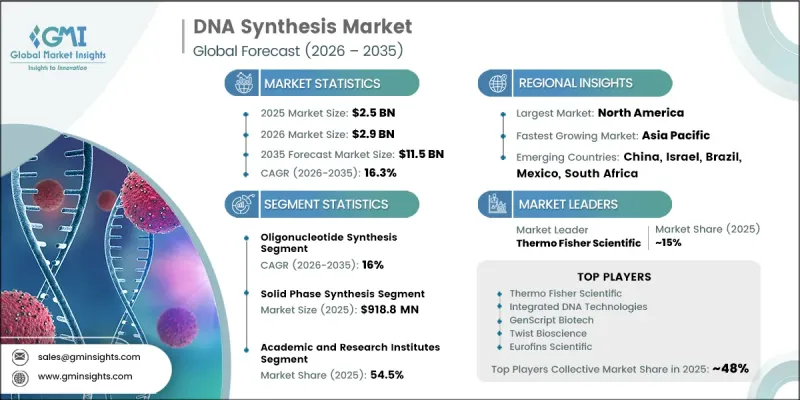

全球DNA合成市場預計到2025年將達到25億美元,並有望以16.3%的複合年成長率成長,到2035年將達到115億美元。

由於分子生物學、合成生物學、基因工程和臨床診斷等領域對合成DNA的需求不斷成長,市場呈現強勁成長動能。遺傳性疾病和慢性病的日益普遍進一步加劇了藥物發現、疫苗研發和個人化醫療領域對先進研究的需求。生物技術投資的增加、高通量合成平台的日益普及以及基因組學技術的持續進步,都進一步推動了產業成長。此外,先進的商業合成服務的普及以及基於DNA的研究工具在生命科學領域的日益整合,也加速了全球的應用。生技公司、製藥公司和致力於開發下一代基因解決方案的研究機構之間加強合作,也為市場發展提供了有利因素。雖然對精準醫療和工程化生物系統的日益關注將進一步推動長期需求,但合成工作流程的自動化和數位化正在提高所有應用的擴充性、速度和準確性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 25億美元 |

| 預測金額 | 115億美元 |

| 複合年成長率 | 16.3% |

DNA合成是指利用化學或酵素方法在實驗室中建構人工DNA序列。該過程能夠精確建構客製化的遺傳物質,廣泛應用於基因編輯、治療方法開發、分子診斷、疫苗研發和合成生物學等領域。它在現代生物技術中也發揮著至關重要的作用,支持著用於商業和科研目的的工程基因、生物路徑和複雜生命系統的設計。這項技術正日益融入先進的生物工程工作流程,加速生命科學產業的實驗和創新。

預計2026年至2035年間,寡核苷酸合成領域將以16%的複合年成長率成長。其市場主導地位主要得益於PCR、qPCR、基因定序、克隆和基因編輯等應用領域的高使用率。這些短DNA片段作為重要的實驗室耗材,廣泛應用於臨床和科研領域,從而創造了穩定且持續的需求。產業相關人員的持續產品創新和策略合作也進一步推動了該領域的成長。

到2025年,學術和研究機構將佔據54.5%的市場。這一主導地位主要得益於合成DNA在基因組研究、分子克隆、功能生物學研究、通路工程以及更廣泛的生命科學研究中的廣泛應用。公營和私營機構對大學、政府實驗室和研究中心的持續資助將維持各科學領域對寡核苷酸和基因合成服務的強勁需求。

預計到2025年,北美DNA合成市佔率將達到38.7%。該地區的領先地位得益於對生物技術和基因組學研究的大量投資,以及許多領先的DNA合成公司和高度發展的研究基礎設施。強而有力的政府支持,以及與產業相關人員和研究機構的合作,正在推動市場的進一步成長。該地區擁有成熟的生物技術生態系統,包括製藥公司、合成生物學開發公司、受託研究機構和學術機構,這些機構正積極利用高通量DNA合成技術進行藥物研發和前沿研究應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 全球疾病盛行率上升

- 合成生物學領域的快速技術進步

- 增加對研發活動的投資

- 產業潛在風險與挑戰

- 嚴格的政府法規和指導方針

- 高成本、潛在的生物安全、生物安保和倫理問題。

- 市場機遇

- 酶促和無細胞DNA合成技術的進展

- 拓展DNA資料儲存商業化的機會

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術展望

- 最新科技趨勢

- 自動化高通量DNA合成平台

- 利用酵素進行DNA合成的進展

- 新興技術

- 與無細胞和有細胞製造系統的整合

- 基於雲端的DNA合成平台與數位實驗室

- 最新科技趨勢

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依服務業分類,2022-2035年

- 寡核苷酸合成

- 標準OCD合成

- 客製化寡核苷酸合成

- 基因合成

- 客製化基因合成

- 基因文庫合成

第6章 市場估計與預測:依方法分類,2022-2035年

- 固相合成

- 利用PCR進行酶合成

- 基於晶片的DNA合成

第7章:DNA合成市場規模及預測:依應用領域分類,2022-2035年

- 研究與開發

- 診斷

- 治療

第8章:DNA合成市場規模及預測:依最終用途分類,2022-2035年

- 學術研究機構

- 受託研究機構

- 生物製藥公司

第9章:DNA合成市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- BIOMATIK

- Bioneer

- Eton Bioscience

- Eurofins Scientific

- GenScript Biotech

- IBA Lifesciences

- Integrated DNA Technologies

- Kaneka Eurogentec

- LGC Biosearch Technologies

- OriGene Technologies

- ProMab Biotechnologies

- ProteoGenix

- Quintara Biosciences

- Shenzhen Shuxin Biotechnology

- Synbio Technologies

- Thermo Fisher Scientific

- Twist Bioscience

The Global DNA Synthesis Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 16.3% to reach USD 11.5 billion by 2035.

The market is experiencing strong momentum due to rising demand for synthetic DNA across molecular biology, synthetic biology, genetic engineering, and clinical diagnostics applications. Increasing prevalence of genetic and chronic diseases is further strengthening the need for advanced research in drug discovery, vaccine development, and personalized medicine. Expanding biotechnology investments, growing adoption of high-throughput synthesis platforms, and continuous technological improvements in genomics are further supporting industry expansion. In addition, the availability of advanced commercial synthesis services and rising integration of DNA-based research tools in life sciences are accelerating global adoption. The market is also benefiting from increasing collaboration between biotechnology firms, pharmaceutical companies, and research institutions focused on developing next-generation genetic solutions. Growing emphasis on precision medicine and engineered biological systems is further reinforcing long-term demand, while automation and digitalization in synthesis workflows are improving scalability, speed, and accuracy across applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 16.3% |

DNA synthesis is defined as the laboratory-based creation of artificial DNA sequences using chemical or enzymatic techniques. This process enables the precise construction of customized genetic material used in a wide range of applications such as gene editing, therapeutic development, molecular diagnostics, vaccine research, and synthetic biology. It plays a foundational role in modern biotechnology by supporting the design of engineered genes, biological pathways, and complex living systems for both commercial and research purposes. The technology is increasingly integrated into advanced biological engineering workflows, enabling faster experimentation and innovation across life sciences industries.

The oligonucleotide synthesis segment is projected to grow at a CAGR of 16% during 2026-2035. Its dominance is mainly supported by strong utilization in PCR, qPCR, gene sequencing, cloning, and gene-editing applications. These short DNA fragments are widely used as essential laboratory consumables in both clinical and research environments, creating steady and recurring demand. Ongoing product innovations and strategic partnerships among industry participants are further strengthening segment growth.

The academic and research institutes segment accounted for a share of 54.5% in 2025. This leadership is driven by extensive use of synthetic DNA in genomics research, molecular cloning, functional biology studies, pathway engineering, and broader life science investigations. Consistent funding support from public and private organizations for universities, government laboratories, and research centers continues to sustain strong demand for oligonucleotide and gene synthesis services across scientific disciplines.

North America DNA Synthesis Market held a 38.7% share in 2025. The region's dominance is supported by significant investments in biotechnology and genomics research, along with the presence of leading DNA synthesis companies and highly advanced research infrastructure. Strong government support, along with collaborations between industry participants and research organizations, is further driving growth. The region benefits from a mature biotechnology ecosystem that includes pharmaceutical companies, synthetic biology developers, contract research organizations, and academic institutions actively utilizing high-throughput DNA synthesis technologies for drug discovery and advanced research applications.

Prominent players operating in the Global DNA synthesis industry include GenScript Biotech, Thermo Fisher Scientific, Eurofins Scientific, Integrated DNA Technologies, Twist Bioscience, BIOMATIK, Bioneer, Eton Bioscience, IBA Lifesciences, Kaneka Eurogentec, LGC Biosearch Technologies, OriGene Technologies, ProMab Biotechnologies, ProteoGenix, Quintara Biosciences, Shenzhen Shuxin Biotechnology, Synbio Technologies, and LGC Biosearch Technologies. Companies operating in the DNA synthesis market are increasingly focusing on technological innovation, automation, and scalability to strengthen their market position. A key strategy includes expanding high-throughput synthesis capabilities to meet rising demand from research and pharmaceutical applications. Market players are heavily investing in next-generation synthesis platforms that improve speed, accuracy, and cost efficiency. Strategic collaborations with biotechnology firms, academic institutes, and pharmaceutical companies are also enhancing product development and application reach. Many companies are strengthening their global distribution networks and expanding service portfolios to include customized DNA design and rapid delivery solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis

- 2.1.1 Regional trends

- 2.1.2 Service trends

- 2.1.3 Method trends

- 2.1.4 Application trends

- 2.1.5 End Use trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of diseases globally

- 3.2.1.2 Rapid technology advancements in the field of synthetic biology

- 3.2.1.3 Rising investments towards research and development(R&D) activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent government regulations and guidelines

- 3.2.2.2 High cost, potential biosafety,biosecurity and ethical issues

- 3.2.3 Market opportunities

- 3.2.3.1 Advancement of enzymatic and cell-free DNA synthesis technologies

- 3.2.3.2 Expansion of DNA data storage commercialization opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Automation and high-throughput DNA synthesis platforms

- 3.5.1.2 Advancements in enzymatic DNA synthesis

- 3.5.2 Emerging technologies

- 3.5.2.1 Integration with cell-free and cell-based manufacturing systems

- 3.5.2.2 Cloud-based DNA synthesis platforms and digital labs

- 3.5.1 Current technological trends

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Impact of AI and Generative AI on the market (Driven by Primary Research)

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Service, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Oligonucleotide synthesis

- 5.2.1 Standard oligonucleotide synthesis

- 5.2.2 Custom oligonucleotide synthesis

- 5.3 Gene Synthesis

- 5.3.1 Custom gene synthesis

- 5.3.2 Gene library synthesis

Chapter 6 Market Estimates and Forecast, By Method, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Solid phase synthesis

- 6.3 PCR-based enzyme synthesis

- 6.4 CHIP-based DNA synthesis

Chapter 7 DNA Synthesis Market Size and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Research and development

- 7.3 Diagnostics

- 7.4 Therapeutics

Chapter 8 DNA Synthesis Market Size and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Academic and research institutes

- 8.3 Contract research organizations

- 8.4 Biopharmaceutical companies

Chapter 9 DNA Synthesis Market Size and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East & Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 BIOMATIK

- 10.2 Bioneer

- 10.3 Eton Bioscience

- 10.4 Eurofins Scientific

- 10.5 GenScript Biotech

- 10.6 IBA Lifesciences

- 10.7 Integrated DNA Technologies

- 10.8 Kaneka Eurogentec

- 10.9 LGC Biosearch Technologies

- 10.10 OriGene Technologies

- 10.11 ProMab Biotechnologies

- 10.12 ProteoGenix

- 10.13 Quintara Biosciences

- 10.14 Shenzhen Shuxin Biotechnology

- 10.15 Synbio Technologies

- 10.16 Thermo Fisher Scientific

- 10.17 Twist Bioscience

全球DNA合成市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球DNA合成市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034)

全球DNA合成市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球DNA合成市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034) DNA合成市場規模、佔有率和成長分析(按產品、類型、方法、應用、最終用戶和地區分類)—產業預測,2026-2033年

DNA合成市場規模、佔有率和成長分析(按產品、類型、方法、應用、最終用戶和地區分類)—產業預測,2026-2033年 美國DNA 合成市場規模、佔有率和趨勢分析報告:按服務類型、應用、最終用途和細分市場預測,2025 年至 2033 年DNA合成市場規模、佔有率、趨勢分析報告:按服務類型、應用、最終用途、地區、細分市場預測,2025-2033年

美國DNA 合成市場規模、佔有率和趨勢分析報告:按服務類型、應用、最終用途和細分市場預測,2025 年至 2033 年DNA合成市場規模、佔有率、趨勢分析報告:按服務類型、應用、最終用途、地區、細分市場預測,2025-2033年