|

市場調查報告書

商品編碼

2061452

2026 年至 2035 年訂閱盒的市場機會、成長要素、產業趨勢分析與預測。Subscription Box Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

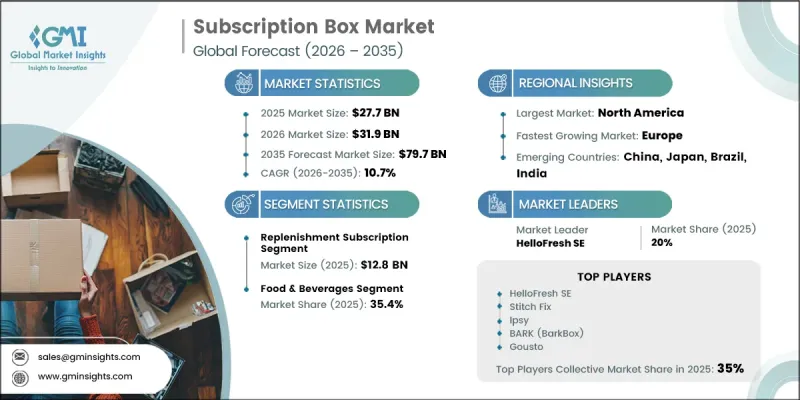

全球訂閱盒市場預計到 2025 年價值 277 億美元,預計到 2035 年將以 10.7% 的複合年成長率成長至 797 億美元。

訂閱零售已成為現代消費者購買行為中不可或缺的一部分,其模式定期提供精心挑選的產品,強調便利性、個人化和新奇體驗。訂閱零售已發展成為一個結構化的生態系統,消費者定期收到個人化產品,形成可預測的消費週期。這種模式強化了消費者的習慣性購買行為,並透過持續互動提升了客戶參與。企業受益於穩定且持續的收入來源和更高的客戶維繫,而消費者則享受便利性和根據自身偏好量身定做的體驗。該行業正日益受到個人化策略的影響,這些策略根據用戶行為、生活方式偏好和過往購買模式選擇商品,從而顯著提升客戶滿意度和品牌忠誠度。數位平台和先進的分析技術使企業能夠進一步最佳化產品和服務,提升用戶體驗。總而言之,隨著消費者越來越重視便利性、個人化和體驗式零售模式,訂閱盒市場持續擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 277億美元 |

| 預計金額 | 797億美元 |

| 複合年成長率 | 10.7% |

預計到2025年,訂閱市場規模將達到128億美元。該市場主要由日常必需品需求驅動,透過定期配送產品確保不間斷使用。訂閱市場專注於便利性消費,涵蓋個人保養用品、營養補充品和家居日用品等。與追求自由裁量權或體驗型產品的消費者相比,訂閱使用者更傾向於選擇穩定性、節省時間和自動化購買流程的產品。

2025年,食品飲料產業佔據35.4%的市場佔有率,並持續保持主導在所有產品類型中的領先地位。該行業受益於強勁的重複消費模式,因為食品類產品天然契合訂閱配送模式。消費者越來越青睞預先搭配好的食品組合帶來的便利,以及探索全新美食選擇的機會。這種便利性、多樣性和新穎性的結合,持續推動全球食品飲料訂閱服務的強勁成長。

美國訂閱盒市場佔85%的佔有率,預計2025年市場規模將達到103億美元。美國市場領先地位的支撐因素包括:早期採用訂閱經營模式、消費者強大的購買力以及先進的物流和履約基礎設施。消費者對便利型服務的循環支付系統的廣泛接受度也進一步推動了市場成長。憑藉其強大的創新生態系統、高效的執行能力以及消費者對訂閱服務的廣泛認可,美國繼續保持區域市場的主導地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 訂閱平台提供者和技術棧

- 履約及物流層

- 支付處理和計費基礎設施

- 客戶獲取和留存行銷

- 每個階段增加的價值

- 按價值鏈層進行利潤率分析

- 影響產業的因素

- 促進因素

- 個性化和精選的魅力

- 電子商務和D2C模式的成長

- 企業經常性收入模式

- 產業潛在風險與挑戰

- 客戶流失率高

- 物流和履約的複雜性

- 機會

- 注重永續性的包裝和產品

- 進入市場區隔

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 技術與創新展望

- 當前技術趨勢(人工智慧內容規劃、預測分析、自動化)

- 新興科技(生成式個人化、區塊鏈忠誠度、物聯網包裝)

- 訂閱管理平台分析(Recharge、Recurly、Chargebee、Bold)

- 履約自動化技術(WMS、機器人揀貨、智慧套件組裝)

- 價格分析

- 2019-2024年歷史價格趨勢分析

- 按業務類型分類的定價策略(高階精選產品與低價補充品)

- 價格彈性和客戶流失敏感性

- 折扣和促銷對顧客終身價值的影響

- 監理框架

- 關於自動續約和取消的法律(州和聯邦法律)

- 消費者保護條例(FTC Rosaka 法案、負面選擇規則)

- 產品特定合規性(食品和化妝品:FDA,酒精:TTB)

- 資料隱私和支付安全(PCI-DSS、GDPR、CCPA)

- 波特的分析

- PESTLE分析

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧驅動的現有經營模式轉型(大規模超個人化)

- Genai按細分市場分類的應用案例和實施藍圖(內容聚合演算法、客戶流失預測、動態定價)

- 風險、限制和監管方面的考量(演算法偏差、隱私問題)

- 目前分銷基礎設施和通路滲透情況

- 區域履約中心網路密度和覆蓋率分析(自營中心和第三方物流中心的人口比率)

- 最後一公里基礎設施差異和不斷變化的管道(當日送達、儲物櫃自提、混合模式)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依訂閱類型分類,2022-2035年

- 補貨訂閱

- 精選訂閱

- 訪問訂閱

第6章 市場估計與預測:依價格區間分類,2022-2035年

- 價格實惠

- 中階

- 高階/豪華

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 美容及個人護理

- 食品/飲料

- 時尚與服裝

- 圖書

- 健身與健康

- 寵物用品

- 科技與小工具

- 兒童和嬰兒用品

- 美術和手工藝品

- 家居用品

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第9章:公司簡介

- 世界公司

- HelloFresh SE

- Ipsy

- Stitch Fix

- BARK(BarkBox)

- Green Chef

- FabFitFun

- Allure Beauty Box

- 該地區的領先企業

- Gousto

- GlossyBox

- Bespoke Post

- Mindful Chef

- Hunt A Killer

- Dollar Shave Club

- Grove Collaborative

- Niche/Specialist Players

- KiwiCo

- Book of the Month

- ButcherBox

- Atlas Coffee Club

- Universal Yums

- Winc

- Carnivore Club

The Global Subscription Box Market was valued at USD 27.7 billion in 2025 and is estimated to grow at a CAGR of 10.7% to reach USD 79.7 billion by 2035.

The market has become an established part of modern consumer purchasing behavior, offering curated and recurring product delivery models that emphasize convenience, personalization, and discovery. Subscription-based retail has evolved into a structured ecosystem where consumers receive tailored product selections at regular intervals, creating predictable consumption cycles. This model strengthens habitual purchasing patterns while enhancing customer engagement through continuous interaction. Businesses benefit from stable recurring revenue streams and improved customer retention, while consumers enjoy convenience and curated experiences aligned with their preferences. The industry is increasingly shaped by personalization strategies, where product selection is guided by user behavior, lifestyle preferences, and past purchasing patterns. This has significantly improved customer satisfaction and brand loyalty. Digital platforms and advanced analytics further enable companies to refine offerings and optimize user experiences. Overall, the subscription box market continues to expand as consumers increasingly value convenience, personalization, and experiential retail formats.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $27.7 Billion |

| Forecast Value | $79.7 Billion |

| CAGR | 10.7% |

The replenishment subscription segment generated USD 12.8 billion in 2025. This segment is primarily driven by routine and essential consumer needs, where products are delivered on a recurring schedule to ensure uninterrupted usage. It focuses on convenience-driven purchases such as personal care items, nutritional products, and household consumables. The segment appeals to consumers who prioritize consistency, time savings, and automated purchasing cycles over discretionary or experience-based offerings.

The food & beverages segment accounted for 35.4% share in 2025, maintaining a leading position across product categories. This segment benefits from strong repeat consumption patterns, as food-related products naturally align with recurring delivery models. Consumers are increasingly attracted to the convenience of pre-selected food assortments along with the opportunity to explore new culinary options. The combination of convenience, variety, and novelty continues to support strong adoption of food and beverage subscription services across global markets.

United States Subscription Box Market held an 85% share, generating USD 10.3 billion in 2025. Market leadership in the country is supported by early adoption of subscription-based business models, high consumer purchasing power, and advanced logistics and fulfillment infrastructure. The strong acceptance of recurring payment systems for convenience-driven services has further supported market expansion. The U.S. continues to dominate the regional landscape due to its strong innovation ecosystem, efficient execution capabilities, and widespread consumer familiarity with subscription-based offerings.

Major companies operating in the Global Subscription Box Market include HelloFresh SE, Ipsy, Stitch Fix, BARK (BarkBox), FabFitFun, Green Chef, Allure Beauty Box, Gousto, GlossyBox, Bespoke Post, Mindful Chef, Hunt A Killer, Dollar Shave Club, Grove Collaborative, KiwiCo, Book of the Month, ButcherBox, Atlas Coffee Club, Universal Yums, Winc, and Carnivore Club. Companies in the subscription box market are focusing heavily on personalization-driven strategies to enhance customer engagement and retention. Many players are leveraging advanced data analytics and AI-based recommendation systems to tailor product selections according to user preferences, purchase history, and lifestyle patterns. Expansion of direct-to-consumer digital platforms is enabling stronger customer relationships and improved retention rates. Firms are also investing in flexible subscription models, including tiered pricing and customizable delivery frequencies, to increase accessibility and reduce churn. Strategic partnerships with logistics providers are improving delivery efficiency and scalability across regions. In addition, brands are strengthening their value proposition through exclusive product offerings, curated experiences, and premium packaging designs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Subscription type

- 2.2.3 Price range

- 2.2.4 Application

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Subscription platform providers & technology stack

- 3.1.3 Fulfillment & logistics layer

- 3.1.4 Payment processing & billing infrastructure

- 3.1.5 Customer acquisition & retention marketing

- 3.1.6 Value addition at each stage

- 3.1.7 Profit margin analysis by value chain layer (driven by primary research)

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Personalization and curation appeal

- 3.2.1.2 Growth of e-commerce and direct-to-consumer models

- 3.2.1.3 Recurring revenue model for businesses

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High customer churn rates

- 3.2.2.2 Logistics and fulfilment complexity

- 3.2.3 Opportunities

- 3.2.3.1 Sustainability-focused packaging and products

- 3.2.3.2 Expansion into niche segments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology & innovation landscape

- 3.5.1 Current technological trends (ai curation, predictive analytics, automation)

- 3.5.2 Emerging technologies (genai personalization, blockchain loyalty, iot packaging)

- 3.5.3 Subscription management platform analysis (recharge, recurly, chargebee, bold)

- 3.5.4 Fulfillment automation technologies (wms, robotic picking, smart kitting)

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (2019-2024) (driven by primary research)

- 3.6.2 Pricing strategy by player type (premium curation vs. budget replenishment) (driven by primary research)

- 3.6.3 Price elasticity & churn sensitivity

- 3.6.4 Discount & promotional impact on ltv

- 3.7 Regulatory framework

- 3.7.1 Auto-renewal & cancellation laws (state-level & federal)

- 3.7.2 Consumer protection regulations (ftc rosaca, negative option rules)

- 3.7.3 Product-specific compliance (fda for food/cosmetics, ttb for alcohol)

- 3.7.4 Data privacy & payment security (pci-dss, gdpr, ccpa)

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Impact of ai & generative ai on the market

- 3.10.1 Ai-driven disruption of existing business models (hyper-personalization at scale)

- 3.10.2 Genai use cases & adoption roadmap by segment (curation algorithms, churn prediction, dynamic pricing)

- 3.10.3 Risks, limitations & regulatory considerations (algorithmic bias, privacy concerns)

- 3.11 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.11.1 Fulfillment center network density & coverage analysis by region (in-house vs. 3pl penetration) (driven by primary research)

- 3.11.2 Last-mile infrastructure gaps & emerging channel shifts (same-day, locker pickup, hybrid models) (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Subscription Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Replenishment subscription

- 5.3 Curation subscription

- 5.4 Access subscription

Chapter 6 Market Estimates and Forecast, By Price Range, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Budget-friendly

- 6.3 Mid-range

- 6.4 Premium/luxury

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Beauty and personal care

- 7.3 Food and beverages

- 7.4 Fashion and apparel

- 7.5 Books

- 7.6 Fitness and wellness

- 7.7 Pet products

- 7.8 Tech and gadgets

- 7.9 Kids and baby products

- 7.10 Arts and crafts

- 7.11 Home goods

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 HelloFresh SE

- 9.1.2 Ipsy

- 9.1.3 Stitch Fix

- 9.1.4 BARK (BarkBox)

- 9.1.5 Green Chef

- 9.1.6 FabFitFun

- 9.1.7 Allure Beauty Box

- 9.2 Regional Champions

- 9.2.1 Gousto

- 9.2.2 GlossyBox

- 9.2.3 Bespoke Post

- 9.2.4 Mindful Chef

- 9.2.5 Hunt A Killer

- 9.2.6 Dollar Shave Club

- 9.2.7 Grove Collaborative

- 9.3 Niche/Specialist Players

- 9.3.1 KiwiCo

- 9.3.2 Book of the Month

- 9.3.3 ButcherBox

- 9.3.4 Atlas Coffee Club

- 9.3.5 Universal Yums

- 9.3.6 Winc

- 9.3.7 Carnivore Club

2026-2030年全球美妝訂閱盒市場

2026-2030年全球美妝訂閱盒市場 全球訂閱盒市場(至 2035 年):依訂閱類型、使用類型、性別、地區、產業趨勢和預測

全球訂閱盒市場(至 2035 年):依訂閱類型、使用類型、性別、地區、產業趨勢和預測 訂閱盒市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類

訂閱盒市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類 訂閱盒市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

訂閱盒市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 圖書定期訂閱盒市場按類型、通路、訂閱頻率和圖書格式分類-2026-2032年全球預測

圖書定期訂閱盒市場按類型、通路、訂閱頻率和圖書格式分類-2026-2032年全球預測 日本訂閱盒市場報告(按類型、性別、應用和地區分類,2026-2034年)

日本訂閱盒市場報告(按類型、性別、應用和地區分類,2026-2034年) 訂閱盒市場規模、佔有率和成長分析(按類型、性別、應用和地區分類)—2026-2033年產業預測

訂閱盒市場規模、佔有率和成長分析(按類型、性別、應用和地區分類)—2026-2033年產業預測 訂閱盒包裝解決方案市場預測至2032年:按材料、包裝類型、分銷管道、應用、最終用戶和地區分類的全球分析

訂閱盒包裝解決方案市場預測至2032年:按材料、包裝類型、分銷管道、應用、最終用戶和地區分類的全球分析 全球美容訂購盒市場2032 年訂閱盒市場預測:按類型、類別、訂閱期、定價模式、分銷管道、最終用戶和地區進行的全球分析

全球美容訂購盒市場2032 年訂閱盒市場預測:按類型、類別、訂閱期、定價模式、分銷管道、最終用戶和地區進行的全球分析