|

市場調查報告書

商品編碼

2061443

生物相似藥市場機會、成長要素、產業趨勢分析及2026-2035年預測。Biosimilars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025年全球生物相似藥市場價值為387億美元,預計到2035年將以16.6%的複合年成長率成長至1852億美元。

生物製劑市場的強勁成長主要得益於對價格合理的生物製藥日益成長的需求,以及全球慢性複雜疾病盛行率的上升。需要生物製藥治療的長期疾病發生率不斷增加,顯著加速了生物相似藥在整個醫療保健系統中的應用。生物相似藥是指在安全性、有效性和品質方面與已通過核准的參考生物製藥高度相似的生物製劑,能夠提供更具成本生物製藥的治療選擇。這些治療方法在使生物製藥,需要進行廣泛的臨床評估、分析研究和監管評估。醫療專業人員和患者對生物相似藥的認知不斷提高、有利的報銷機制、產品核可的增加以及生物相似藥在多個治療領域的廣泛接受,都將進一步推動預測期內市場的快速擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 387億美元 |

| 預測金額 | 1852億美元 |

| 複合年成長率 | 16.6% |

預計到2025年,重組糖基化蛋白市場規模將達262億美元。該市場持續佔據行業重要佔有率,主要得益於對用於治療慢性病和嚴重的先進生物製藥的需求不斷成長。重組糖基化蛋白採用先進的重組DNA技術生產,能達到精準的蛋白質開發與必要的分子修飾,確保治療效果。這些生物製藥在各種疾病管理領域的應用日益廣泛,也推動了該市場的持續成長。此外,生物製藥研發投入的增加以及對經濟有效的替代療法的需求不斷成長,也是推動該領域成長的重要因素。

預計到2025年,血液學領域將佔據29.8%的市場。血液學領域的市場成長主要受血液相關疾病盛行率上升和對價格合理的生物治療方案需求不斷成長的驅動。由於人們對生物相似藥的臨床療效、安全性和治療效果越來越有信心,生物相似藥在血液疾病治療的應用日益廣泛。醫療專業人員對生物相似藥療法的經濟和臨床優勢的認知不斷提高,進一步促進了其在血液學實踐中的應用。此外,生物製劑替代療法的可近性不斷提高,也推動了該領域市場的持續成長。

預計到2025年,北美生物相似藥市佔率將達到29.9%,並在2026年至2035年間以16.5%的複合年成長率成長。在醫療保健支出不斷成長、消費者對低成本生物製藥療法的偏好日益增強以及關鍵生物製藥專利到期的推動下,生物類似藥在該地區的應用仍然強勁。北美擁有完善的法規環境,支持高效的核准流程,並增強了醫療專業人員和患者對生物相似藥的信心。醫療保健系統面臨的降低治療成本的壓力日益增大,加上有利的報銷政策和處方藥目錄最佳化策略,正在加速生物相似藥在全部區域多個治療領域的應用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 慢性疾病負擔日益加重

- 專利到期增加

- 提高醫護人員和病患的接受度

- 產業潛在風險與挑戰

- 部分地區市場滲透率較低

- 高昂的研發和製造成本

- 市場機遇

- 人工智慧驅動的生物製程的進步

- 引入簡化的監管流程

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術展望

- 目前技術

- 新興技術

- 目前還款狀態

- 美國

- 加拿大

- 歐洲

- 澳洲

- 紐西蘭

- 生物相似藥訴訟現狀

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 生物相似藥的因素分析

- 使用權

- 規章制度

- 支付方的評估和准入

- 醫生的接受

- 患者接受度

- 生物相似藥產品研發管線分析

- 生物相似藥核准趨勢(2022-2025)

- 生物製藥專利到期情景

- 關於生物相似藥使用的國際政策

- 相容性、切換和替代方案

- 供給面政策

- 處方獎勵

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 重組非糖基化蛋白

- 人體生長荷爾蒙

- 顆粒細胞增生因子(Filgrastim)

- 胰島素

- 干擾素

- 阿爾法

- 測試版

- 重組糖基化蛋白

- 單株抗體

- Infliximab

- Rituximab

- Adalimumab

- 曲妥珠單抗

- Bevacizumab

- 促紅血球生成素

- 阿爾法

- 測試版

- 促濾泡素

- 阿爾法

- 測試版

- 融合蛋白

- 單株抗體

- 其他產品

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 血液學

- 嗜中性白血球低下症

- 貧血

- 其他血液學應用

- 腫瘤學

- 肺癌

- 腦腫瘤

- 乳癌

- 子宮頸癌

- 結腸癌

- 白血病

- 其他腫瘤學應用

- 自體免疫疾病

- 關節炎

- 類風濕性關節炎

- 乾癬性關節炎

- 幼年型關節炎

- 僵直性脊椎炎

- 其他關節炎

- 發炎性腸道疾病(IBD)

- 潰瘍性大腸炎

- 克隆氏症

- 其他發炎性腸道疾病

- 銀屑病

- 其他自體免疫疾病

- 關節炎

- 眼科

- 生長激素缺乏症

- 糖尿病

- 其他用途

第7章 市場估價與預測:依製造類型分類,2022-2035年

- 合約研究和製造服務

- 內部

第8章 市場估計與預測:依技術分類,2022-2035年

- 重組DNA技術

- 哺乳動物細胞培養系統

- 其他技術

第9章 市場估價與預測:依通路分類,2022-2035年

- 醫院藥房

- 專科藥房

- 其他分銷管道

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第11章:公司簡介

- Biocon

- Sandoz

- Bio-Thera Solutions

- Pfizer

- Dr. Reddy's Laboratories

- Amgen

- Teva Pharmaceuticals

- Fresenius Kabi

- Coherus Biosciences

- Apobiologix

- Biocad

- Intas Pharma

- Celltrion

- Zydus Cadila

- Samsung Bioepis

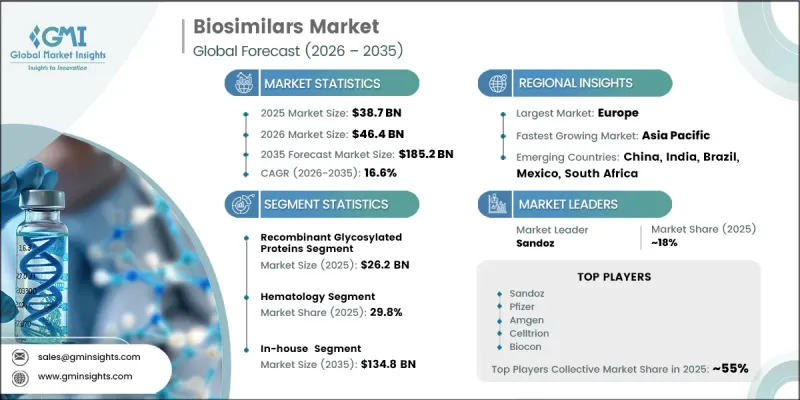

The Global Biosimilars Market was valued at USD 38.7 billion in 2025 and is estimated to grow at a CAGR of 16.6% to reach USD 185.2 billion by 2035.

Strong market growth is driven by the rising demand for affordable biologic therapies and the increasing prevalence of chronic and complex medical conditions worldwide. The growing incidence of long-term diseases requiring biologic treatment solutions is significantly accelerating biosimilar adoption across healthcare systems. Biosimilars are biologic medicines developed to closely match approved reference biologics in terms of safety, effectiveness, and quality while offering more cost-efficient treatment alternatives. These therapies are playing an increasingly important role in improving patient access to advanced biologic treatments and reducing the financial burden associated with long-term disease management. Extensive clinical assessments, analytical studies, and regulatory evaluations are required to establish therapeutic equivalence and biosimilarity with originator biologics. Expanding awareness among healthcare professionals and patients, favorable reimbursement frameworks, increasing product approvals, and broader acceptance of biosimilar therapies across multiple therapeutic areas are further contributing to rapid market expansion throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $38.7 Billion |

| Forecast Value | $185.2 Billion |

| CAGR | 16.6% |

The Recombinant Glycosylated Proteins segment reached USD 26.2 billion in 2025. This segment continues to hold a substantial share of the industry due to increasing demand for advanced biologic therapies utilized in the treatment of chronic and severe medical conditions. Recombinant glycosylated proteins are manufactured using advanced recombinant DNA technologies that enable accurate protein development and essential molecular modifications required for therapeutic effectiveness. Growing adoption of these biologic therapies across various disease management applications is supporting continued segment expansion. Increasing investments in biologic drug development and rising demand for cost-effective therapeutic alternatives are also strengthening growth within this category.

The hematology segment accounted for a share of 29.8% in 2025. Market growth within hematology applications is primarily driven by the increasing prevalence of blood-related disorders and rising demand for affordable biologic treatment solutions. Biosimilars are being increasingly adopted for the management of hematologic conditions due to growing confidence in their clinical performance, safety standards, and therapeutic effectiveness. Rising awareness among healthcare providers regarding the economic and clinical benefits associated with biosimilar therapies is further supporting broader utilization across hematology treatment settings. Expanding access to biologic treatment alternatives is also contributing to the segment's sustained market growth.

North America Biosimilars Market held 29.9% share in 2025 and is expected to grow at a CAGR of 16.5% during 2026-2035. The region continues to experience strong biosimilar adoption supported by increasing healthcare expenditures, growing preference for lower-cost biologic treatment options, and ongoing patent expirations for several major biologic products. North America benefits from a highly structured regulatory environment that supports efficient approval pathways and strengthens confidence in biosimilar utilization among healthcare professionals and patients. Growing pressure on healthcare systems to reduce treatment costs, along with favorable reimbursement policies and formulary optimization strategies, is accelerating biosimilar adoption across multiple therapeutic applications throughout the region.

Key companies operating in the Global Biosimilars Market include Biocon, Sandoz, Bio-Thera Solutions, Pfizer, Dr. Reddy's Laboratories, Amgen, Teva Pharmaceuticals, Fresenius Kabi, Coherus Biosciences, Apobiologix, Biocad, Intas Pharma, Celltrion, Zydus Cadila, and Samsung Bioepis. Companies operating in the biosimilars market are adopting multiple strategic initiatives to strengthen their competitive position and expand global market presence. Leading industry participants are investing heavily in research and development activities to accelerate biosimilar product launches and improve manufacturing capabilities. Strategic partnerships, licensing agreements, and collaborations with biotechnology firms are enabling companies to expand product portfolios and enhance market reach across various therapeutic areas. Organizations are also focusing on strengthening regulatory compliance and obtaining approvals across international markets to improve commercialization opportunities. Increasing investments in advanced manufacturing technologies, supply chain optimization, and biologics production facilities are further supporting long-term growth strategies. In addition, companies are prioritizing physician education programs, patient awareness initiatives, and competitive pricing strategies to increase biosimilar acceptance and strengthen their foothold within the global biosimilars industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 Manufacturing type trends

- 2.2.5 Technology trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising chronic disease burden

- 3.2.1.2 Increasing biologics patent expirations

- 3.2.1.3 Higher clinician and patient acceptance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited market penetration in some regions

- 3.2.2.2 High development and manufacturing costs

- 3.2.3 Market opportunities

- 3.2.3.1 Advancement in AI-driven bioprocessing

- 3.2.3.2 Adoption of streamlined regulatory pathways

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technology

- 3.5.2 Emerging technologies

- 3.6 Reimbursement landscape

- 3.6.1 U.S.

- 3.6.2 Canada

- 3.6.3 Europe

- 3.6.4 Australia

- 3.6.5 New Zealand

- 3.7 Biosimilar Litigation landscape

- 3.8 Future market trends (Driven by primary research)

- 3.9 Impact of AI and generative AI on the market (Driven by primary research)

- 3.10 Biosimilars factor analysis

- 3.10.1 Access

- 3.10.2 Regulations

- 3.10.3 Payer assessment and access

- 3.10.4 Physician acceptance

- 3.10.5 Patient acceptance

- 3.11 Biosimilar product pipeline analysis

- 3.12 Biosimilars approval scenario, 2022 - 2025

- 3.13 Biologics patent expiry scenario

- 3.14 International policies on use of biosimilar drugs

- 3.14.1 Interchangeability, switching and subsitution

- 3.14.2 Supply side policies

- 3.14.3 Prescribing incentives

- 3.15 Porter's analysis

- 3.16 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 ($ Mn)

- 5.1 Key trends

- 5.2 Recombinant non-glycosylated proteins

- 5.2.1 Human growth hormone

- 5.2.2 Granulocyte colony-stimulating factor (filgrastim)

- 5.2.3 Insulin

- 5.2.4 Interferon

- 5.2.4.1 Alfa

- 5.2.4.2 Beta

- 5.3 Recombinant glycosylated proteins

- 5.3.1 Monoclonal antibodies

- 5.3.1.1 Infliximab

- 5.3.1.2 Rituximab

- 5.3.1.3 Adalimumab

- 5.3.1.4 Trastuzumab

- 5.3.1.5 Bevacizumab

- 5.3.2 Erythropoietin

- 5.3.2.1 Alfa

- 5.3.2.2 Beta

- 5.3.3 Follitropin

- 5.3.3.1 Alfa

- 5.3.3.2 Beta

- 5.3.4 Fusion proteins

- 5.3.1 Monoclonal antibodies

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hematology

- 6.2.1 Neutropenia

- 6.2.2 Anemia

- 6.2.3 Other hematology applications

- 6.3 Oncology

- 6.3.1 Lung cancer

- 6.3.2 Brain cancer

- 6.3.3 Breast cancer

- 6.3.4 Cervical cancer

- 6.3.5 Colorectal cancer

- 6.3.6 Leukemia

- 6.3.7 Other Oncology applications

- 6.4 Autoimmune disease

- 6.4.1 Arthritis

- 6.4.1.1 Rheumatoid arthritis

- 6.4.1.2 Psoriatic arthritis

- 6.4.1.3 Juvenile arthritis

- 6.4.1.4 Ankylosing spondylitis

- 6.4.1.5 Other arthritis

- 6.4.2 Inflammatory bowel disease (IBD)

- 6.4.2.1 Ulcerative colitis

- 6.4.2.2 Crohn's disease

- 6.4.2.3 Other IBD

- 6.4.3 Psoriasis

- 6.4.4 Other autoimmune diseases

- 6.4.1 Arthritis

- 6.5 Ophthalmology

- 6.6 Growth hormone deficiency

- 6.7 Diabetes

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By Manufacturing Type, 2022-2035 ($ Mn)

- 7.1 Key trends

- 7.2 Contract research and manufacturing services

- 7.3 In-house

Chapter 8 Market Estimates and Forecast, By Technology, 2022-2035 ($ Mn)

- 8.1 Key trends

- 8.2 Recombinant DNA technology

- 8.3 Mammalian cell culture systems

- 8.4 Other technologies

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Specialty pharmacies

- 9.4 Other distribution channels

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Biocon

- 11.2 Sandoz

- 11.3 Bio-Thera Solutions

- 11.4 Pfizer

- 11.5 Dr. Reddy’s Laboratories

- 11.6 Amgen

- 11.7 Teva Pharmaceuticals

- 11.8 Fresenius Kabi

- 11.9 Coherus Biosciences

- 11.10 Apobiologix

- 11.11 Biocad

- 11.12 Intas Pharma

- 11.13 Celltrion

- 11.14 Zydus Cadila

- 11.15 Samsung Bioepis

Pegfilgrastim生物相似藥市場規模、佔有率和成長分析:按產品、給藥途徑、應用、通路和地區分類-2026-2033年產業預測

Pegfilgrastim生物相似藥市場規模、佔有率和成長分析:按產品、給藥途徑、應用、通路和地區分類-2026-2033年產業預測 生物相似藥市場:2026-2032年全球市場預測(依產品類型、治療領域、給藥途徑、研發階段、生產技術、最終用戶和分銷管道分類)

生物相似藥市場:2026-2032年全球市場預測(依產品類型、治療領域、給藥途徑、研發階段、生產技術、最終用戶和分銷管道分類) 生物相似白細胞介素市場規模、佔有率和成長分析:按分子類型、適應症、給藥途徑、最終用戶、患者類型、分銷管道和地區分類-2026-2033年產業預測

生物相似白細胞介素市場規模、佔有率和成長分析:按分子類型、適應症、給藥途徑、最終用戶、患者類型、分銷管道和地區分類-2026-2033年產業預測 全球Remicade生物相似藥市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年)

全球Remicade生物相似藥市場:市場規模、佔有率、趨勢和成長分析(2026-2034 年) 生物相似藥測試和開發服務市場-全球產業規模、佔有率、趨勢、機會和預測:按服務類型、分子類型、治療領域、最終用戶、地區和競爭格局分類,2021-2031年

生物相似藥測試和開發服務市場-全球產業規模、佔有率、趨勢、機會和預測:按服務類型、分子類型、治療領域、最終用戶、地區和競爭格局分類,2021-2031年 生物相似藥市場預測至2034年-按產品類型、給藥途徑、應用、通路和地區分類的全球分析

生物相似藥市場預測至2034年-按產品類型、給藥途徑、應用、通路和地區分類的全球分析 類克生物相似藥市場:依產品類型、最終用戶、適應症和地區RemicadeHerceptin生物相似藥市場:依適應症、通路和地區分類生物相似藥市場:依藥物類別、治療方法、通路和地區分類修美樂生物相似藥市場:依產品類型、適應症、銷售管道、病患年齡及地區分類

類克生物相似藥市場:依產品類型、最終用戶、適應症和地區RemicadeHerceptin生物相似藥市場:依適應症、通路和地區分類生物相似藥市場:依藥物類別、治療方法、通路和地區分類修美樂生物相似藥市場:依產品類型、適應症、銷售管道、病患年齡及地區分類