|

市場調查報告書

商品編碼

2061439

特殊檢測市場機會、成長要素、產業趨勢分析及2026-2035年預測Esoteric Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

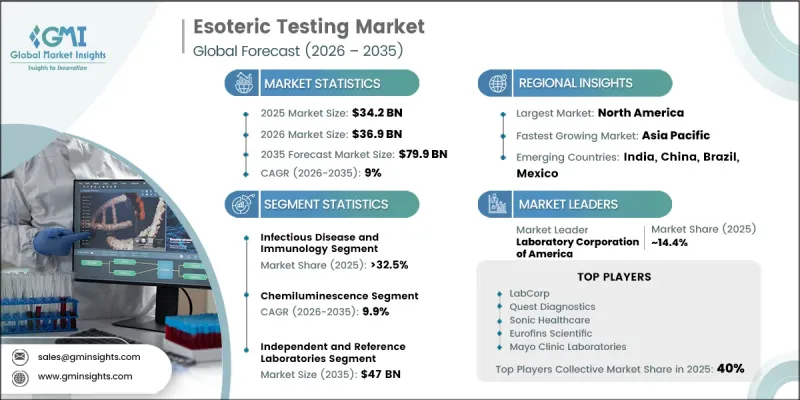

2025 年全球神秘測試市場價值 342 億美元,預計到 2035 年將以 9% 的複合年成長率成長至 799 億美元。

由於慢性病盛行率上升、罕見遺傳疾病發生率增加以及精準醫療在全球的普及,市場正經歷顯著擴張。隨著專業檢測支持超越傳統臨床檢測的高度專業化診斷程序,特異檢測在現代醫學中的重要性日益凸顯。對精準疾病識別、早期診斷和個人化治療方案的需求不斷成長,推動了對先進分子和基因檢測解決方案的需求。此外,醫療機構正擴大利用專業診斷技術來更準確地對疾病進行分類、監測疾病進展並輔助確定標靶治療。分子診斷、基因組學和檢測技術的進步也透過提高檢測的速度、準確性和效率,促進了市場成長。診斷技術的持續創新正在擴大醫療機構和實驗室獲得高靈敏度檢測方法的途徑。此外,預防醫學意識的提高和疾病篩檢力度的加大,正在加速特異檢測服務的普及,並強化先進診斷實驗室在全球醫療系統中管理複雜疾病的作用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 342億美元 |

| 預測市場規模 | 799億美元 |

| 複合年成長率 | 9% |

分子診斷和基因組學領域的技術進步在加速高階檢測市場成長方面發揮著重要作用。先進的檢測技術提高了遺傳物質分析的準確性,並縮短了檢測結果的報告時間。這些創新有助於疾病的早期發現、遺傳健康風險的識別以及治療反應的更有效監測。檢測的可擴展性、靈敏度和經濟性的提升也使得先進的分子檢測解決方案更容易被醫療專業人員和檢測實驗室所採用。因此,先進的基因組學和分子診斷正日益成為現代醫學和專科疾病管理的重要組成部分。

預計到2025年,感染疾病和免疫學領域將佔據32.5%的市場。該領域涵蓋高度專業化的診斷程序,旨在檢測複雜的感染疾病和免疫相關疾病。此類高階檢測解決方案可支援病原體的分子鑑定、免疫系統分析和高級血清學評估。全球對感染疾病和免疫系統疾病日益成長的關注,顯著提升了對高精度、高靈敏度診斷技術的需求。此外,這些檢測解決方案擴大用於監測治療效果和評估免疫反應,進一步推動了該領域的成長。

預計到2025年,化學冷光市場規模將達到89億美元,並在2026年至2035年間以9.9%的複合年成長率成長。由於其高靈敏度、高特異性和快速處理能力,化學冷光診斷檢測在專業檢測產業中持續廣泛應用。此技術廣泛應用於需要高效測量分析物和高通量實驗室處理的複雜診斷應用。與自動化檢測系統的兼容性進一步提高了檢測的一致性、工作流程效率和營運效率,使其成為處理大量檢測的先進診斷實驗室的理想選擇。

美國特殊檢測市場預計到2025年將達到118億美元,並在2026年至2035年間以7.7%的複合年成長率成長。北美憑藉其完善的醫療保健基礎設施、強勁的醫療費用支出以及對創新診斷技術的早期應用,仍然是特殊檢測領域最先進的區域市場之一。該地區受益於眾多領先的診斷服務供應商和先進的參考實驗室,這些機構提供廣泛的專業檢測解決方案。慢性病、癌症和遺傳性疾病發生率的不斷上升,持續推動該地區醫療保健產業對先進診斷能力的需求。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 工業生態系分析

- 影響產業的因素

- 促進因素

- 慢性病和罕見病患疾病率增加

- 個人化醫療與精準醫療的發展

- 分子診斷和基因組學的進展

- 對早期準確疾病診斷的需求日益成長。

- 產業潛在風險與挑戰

- 專業檢測程序高成本

- 特殊檢查的保險覆蓋範圍限制

- 市場機遇

- 遠端醫療和遠距離診斷。

- 人工智慧和數據分析在診斷領域的應用

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術展望

- 最新科技趨勢

- 新技術

- 未來市場趨勢

- 波特的分析

- PESTLE分析

- 價格趨勢分析

- 人工智慧和生成式人工智慧對市場的影響

- 投資與資金籌措分析

- 差距分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依測試類型分類,2022-2035年

- 內分泌學

- 感染疾病與免疫學

- 腫瘤學

- 毒理學

- 神經病學

- 基因組學

- 其他

第6章 市場估計與預測:依技術分類,2022-2035年

- 質譜分析

- 流式細胞技術

- ELISA

- 免疫測量

- 化學冷光

- RT-PCR

- 其他

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院檢驗實驗室

- 獨立和參考測試機構

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- ACM Global Laboratories

- American Esoteric Laboratories(AEL)

- Arup Laboratories

- bioMONTR Labs

- Eurofins Scientific

- Fulgent Genetics

- Genomic Health

- Laboratory Corporation of America

- Mayo Clinic Laboratories

- Myriad Genetics

- Nordic Laboratories

- OPKO Health

- Quest Diagnostics

- Sonic Healthcare

The Global Esoteric Testing Market was valued at USD 34.2 billion in 2025 and is estimated to grow at a CAGR of 9% to reach USD 79.9 billion by 2035.

The market is witnessing significant expansion due to the rising prevalence of chronic illnesses, increasing incidence of rare genetic disorders, and growing adoption of precision medicine worldwide. Esoteric testing has become increasingly important in modern healthcare as it supports highly specialized diagnostic procedures beyond conventional laboratory testing. The growing need for accurate disease identification, early-stage diagnosis, and personalized treatment planning is driving demand for advanced molecular and genetic testing solutions. In addition, healthcare providers are increasingly utilizing specialized diagnostic techniques to classify diseases more precisely, monitor disease progression, and support targeted therapy decisions. Advancements in molecular diagnostics, genomics, and laboratory technologies are also contributing to market growth by improving testing speed, accuracy, and efficiency. Continuous innovation in diagnostic technologies is expanding access to highly sensitive testing methods for healthcare institutions and laboratories. Furthermore, rising awareness regarding preventive healthcare and increasing disease screening initiatives are encouraging wider adoption of esoteric testing services, strengthening the role of advanced diagnostic laboratories in the management of complex medical conditions across global healthcare systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $34.2 Billion |

| Forecast Value | $79.9 Billion |

| CAGR | 9% |

Technological advancements in molecular diagnostics and genomics are playing a major role in accelerating the growth of the esoteric testing market. Advanced testing technologies are improving the ability to analyze genetic material with enhanced precision and faster turnaround times. These innovations are supporting earlier disease detection, identification of inherited health risks, and more effective monitoring of treatment responses. Improvements in test scalability, sensitivity, and affordability are also increasing the accessibility of sophisticated molecular testing solutions for healthcare providers and laboratories. As a result, advanced genomic and molecular diagnostics continue to emerge as essential components of modern healthcare and specialized disease management.

The infectious disease and immunology segment accounted for 32.5% share in 2025. This segment includes highly specialized diagnostic procedures designed to detect complex infections and immune-related disorders. Esoteric testing solutions within this category support molecular pathogen identification, immune system analysis, and advanced serological evaluations. Growing global concerns related to infectious diseases and immune system disorders are significantly increasing demand for highly accurate and sensitive diagnostic technologies. In addition, these testing solutions are increasingly utilized for treatment monitoring and evaluation of immune responses, further supporting segment growth.

The chemiluminescence segment generated USD 8.9 billion in 2025 and is projected to witness a CAGR of 9.9% during 2026-2035. Chemiluminescence-based diagnostic assays continue to gain strong adoption within the esoteric testing industry due to their high sensitivity, specificity, and rapid processing capabilities. This technology is widely utilized for complex diagnostic applications requiring efficient analyte measurement and high-throughput laboratory processing. Its compatibility with automated laboratory systems further improves testing consistency, workflow efficiency, and operational productivity, making it highly suitable for advanced diagnostic laboratories handling large testing volumes.

U.S. Esoteric Testing Market was valued at USD 11.8 billion in 2025 and is projected to grow at a CAGR of 7.7% between 2026 and 2035. North America continues to represent one of the most advanced regional markets for esoteric testing due to its well-established healthcare infrastructure, strong healthcare spending, and early adoption of innovative diagnostic technologies. The region benefits from the presence of major diagnostic service providers and advanced reference laboratories offering a broad range of specialized testing solutions. The rising incidence of chronic diseases, cancer, and genetic conditions continues to drive demand for sophisticated diagnostic capabilities across the regional healthcare sector.

Major companies operating in the Global Esoteric Testing Market include ACM Global Laboratories, American Esoteric Laboratories (AEL), Arup Laboratories, bioMONTR Labs, Eurofins Scientific, Fulgent Genetics, Genomic Health, Laboratory Corporation of America, Mayo Clinic Laboratories, Myriad Genetics, Nordic Laboratories, OPKO Health, Quest Diagnostics, and Sonic Healthcare. Companies operating in the esoteric testing industry are implementing multiple strategic initiatives to strengthen their market presence and expand service capabilities. Leading organizations are investing heavily in advanced molecular diagnostics, genomics platforms, and automation technologies to improve testing accuracy, efficiency, and turnaround times. Many companies are also focusing on expanding specialized testing portfolios to address the increasing demand for precision medicine and personalized healthcare solutions. Strategic collaborations with healthcare providers, pharmaceutical companies, and research institutions are helping market participants improve innovation capabilities and broaden customer reach. In addition, companies are expanding laboratory networks and digital healthcare integration to enhance accessibility and streamline diagnostic workflows.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Test type trends

- 2.2.3 Technology trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic and rare diseases

- 3.2.1.2 Growth in personalized and precision medicine

- 3.2.1.3 Advancements in molecular diagnostics and genomics

- 3.2.1.4 Rising demand for early and accurate disease diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of esoteric testing procedures

- 3.2.2.2 Limited reimbursement coverage for specialized tests

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of telehealth and remote diagnostics

- 3.2.3.2 Integration of AI and data analytics in diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by primary research)

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing trend analysis (Driven by primary research)

- 3.10 Impact of AI & Generative AI on the market

- 3.11 Investment & funding analysis

- 3.12 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Test Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Endocrinology

- 5.3 Infectious disease and immunology

- 5.4 Oncology

- 5.5 Toxicology

- 5.6 Neurology

- 5.7 Genomics

- 5.8 Other test types

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Mass spectrometry

- 6.3 Flow cytometry

- 6.4 ELISA

- 6.5 Radioimmunoassay

- 6.6 Chemiluminescence

- 6.7 RT-PCR

- 6.8 Other technologies

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital-based laboratories

- 7.3 Independent and reference laboratories

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ACM Global Laboratories

- 9.2 American Esoteric Laboratories (AEL)

- 9.3 Arup Laboratories

- 9.4 bioMONTR Labs

- 9.5 Eurofins Scientific

- 9.6 Fulgent Genetics

- 9.7 Genomic Health

- 9.8 Laboratory Corporation of America

- 9.9 Mayo Clinic Laboratories

- 9.10 Myriad Genetics

- 9.11 Nordic Laboratories

- 9.12 OPKO Health

- 9.13 Quest Diagnostics

- 9.14 Sonic Healthcare

特殊檢測市場:按類型、技術、服務供應商和地區分類

特殊檢測市場:按類型、技術、服務供應商和地區分類 特殊檢測市場:全球市場按產品類型、應用、最終用戶和分銷管道分類的預測 - 2026-2032 年

特殊檢測市場:全球市場按產品類型、應用、最終用戶和分銷管道分類的預測 - 2026-2032 年 全球特殊檢測市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球特殊檢測市場規模、佔有率、趨勢和成長分析報告(2026-2034) 特殊檢測市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、技術、樣本、最終用戶、地區和競爭格局分類),2021-2031年全球特殊檢測市場:市場規模、市場佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034 年)

特殊檢測市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、技術、樣本、最終用戶、地區和競爭格局分類),2021-2031年全球特殊檢測市場:市場規模、市場佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034 年) 特殊檢測市場規模、佔有率和成長分析(按類型、技術、最終用戶和地區分類)-2026-2033年產業預測

特殊檢測市場規模、佔有率和成長分析(按類型、技術、最終用戶和地區分類)-2026-2033年產業預測 深奧的測試市場

深奧的測試市場 2025年全球深奧測試市場報告

2025年全球深奧測試市場報告 深奧測試市場規模、佔有率和趨勢分析報告:按類型、技術、最終用途、地區和細分市場預測,2025 年至 2030 年

深奧測試市場規模、佔有率和趨勢分析報告:按類型、技術、最終用途、地區和細分市場預測,2025 年至 2030 年 深層檢測市場,規模,佔有率,趨勢,產業分析報告:類別,各技術,各最終用途,各地區,2025年~2034年的市場預測

深層檢測市場,規模,佔有率,趨勢,產業分析報告:類別,各技術,各最終用途,各地區,2025年~2034年的市場預測