|

市場調查報告書

商品編碼

2061424

泛自閉症障礙治療市場機會、成長促進因素、產業趨勢分析及2026-2035年預測Autism Spectrum Disorder Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

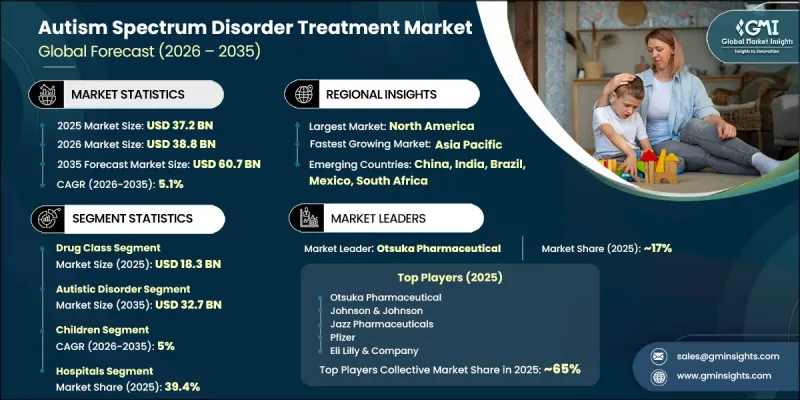

2025 年全球泛自閉症障礙治療市場規模預計為 372 億美元,預計到 2035 年將以 5.1% 的複合年成長率成長至 607 億美元。

由於全球泛自閉症障礙(ASD) 盛行率不斷上升、人們對早期診斷的認知不斷提高以及對神經發育障礙的臨床理解不斷加深,該市場正穩步擴張。篩檢系統的完善和發育健康評估的廣泛應用,促使許多地區的診斷率不斷提高。基因研究、神經影像技術和標準化診斷框架的持續進步,使得ASD的識別更加早期、準確,從而直接推動了對介入和護理服務的需求。越來越多的證據表明,早期療育計畫在改善長期認知功能、行為和社會結果方面發揮著重要作用,這提升了其在醫療保健系統中的優先順序。此外,整合行為療法、教育支持和醫療管理的多學科照護模式的普及,正在改變治療方案的選擇模式。對個人化照護計畫和長期發展支援的日益重視,以及對自閉症專用醫療保健基礎設施和專業照護服務的投入不斷增加,進一步加速了全球市場的成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 372億美元 |

| 預測金額 | 607億美元 |

| 複合年成長率 | 5.1% |

泛自閉症障礙(ASD)是一種複雜的神經發展障礙,其特徵是持續存在溝通、社交互動、行為控制和感覺處理方面的挑戰。治療策略通常包括行為療法、語言療法、職業療法、教育支持系統和藥物治療的綜合運用,旨在控制症狀並改善功能能力。全球對ASD的認知不斷提高,導致診斷率顯著上升,對系統性治療方案和長期支援服務的需求也日益成長。診斷工具和臨床篩檢技術的進步進一步提高了早期發現ASD的能力,從而能夠及時治療性介入。早期發現被廣泛認為是改善ASD患者發展軌跡、溝通能力、行為結果和整體生活品質的關鍵因素。

2025年,醫藥市場規模預計將達183億美元。該市場涵蓋多種治療類別,例如抗精神病藥物、興奮劑、選擇性血清素再回收抑制劑(SSRIs)以及其他相關藥物。藥物治療被廣泛用於控制相關症狀,例如易怒、焦慮、過動、情緒障礙、行為問題和溝通障礙。雖然目前尚無治癒泛自閉症障礙的治療方法方法,但藥物治療在改善症狀控制和維持日常生活功能方面發揮著至關重要的作用,尤其是在與行為療法和其他治療性介入相結合時。

預計到2035年,自閉症譜系障礙市場規模將達到327億美元,佔據整體市場相當大的佔有率。該市場的成長主要得益於嚴重泛自閉症障礙患者複雜的護理需求。這類患者通常需要全面且持續的支持,包括行為療法、結構化教育計畫、臨床介入和長期照護服務。對以促進發展、提升溝通技巧和增強功能獨立性為重點的綜合治療方法的需求不斷成長,也推動了該市場的持續擴張。

到2025年,北美泛自閉症障礙治療市佔率將達到48.1%。該地區市場實力強勁,得益於完善的保險覆蓋、先進的醫療基礎設施以及廣泛的專業自閉症護理和復健服務。該地區持續受益於較高的診斷意識、積極實施的早期療育計畫以及先進治療方法的日益普及。數位健康解決方案、遠距治療平台和混合式醫療服務模式的整合,進一步提升了全部區域的醫療服務可近性和治療效率。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 成長促進因素

- 自閉症的盛行率

- 診斷工具的進步

- 治療方法創新

- 數位醫療和遠端醫療模式整合的進展

- 產業潛在風險與挑戰

- 高昂的醫療費用

- 治療效果的差異

- 市場機遇

- 精準醫療和基於生物標記的治療方法的擴展

- 對成人自閉症護理生態系統的需求日益成長

- 成長促進因素

- 成長潛力分析

- 監理情勢

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 管道分析

- 人工智慧和生成式人工智慧對市場的影響

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依治療類型分類,2022-2035年

- 藥物類別

- 抗精神病藥物

- 選擇性血清素再回收抑制劑

- 興奮劑

- 其他藥物類別

- 治療方法

- 行為和溝通療法

- 螯合療法

- 其他治療方法

- 支援應用

第6章 市場估計與預測:依疾病分類,2022-2035年

- 自閉症譜系障礙

- 亞斯伯格症候群

- 廣泛性發展障礙(PDD)

- 其他疾病

第7章 市場估計與預測:依年齡層別分類,2022-2035年

- 孩子們

- 成人

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 醫院

- 居家醫療

- 復健中心

- 其他最終用戶

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- 服務提供者

- Autism Research Institute

- Child Mind Institute

- Cleveland Clinic

- Mayo Foundation for Medical Education and Research(MFMER).

- The General Hospital

- 製藥公司

- Jazz Pharmaceuticals

- Bristol Myers Squibb

- Pfizer

- Novartis

- AbbVie

- Viatris

- Eli Lilly &Company

- Neurim Pharmaceuticals

The Global Autism Spectrum Disorder Treatment Market was valued at USD 37.2 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 60.7 billion by 2035.

The market is expanding steadily due to the increasing global prevalence of autism spectrum disorder, rising awareness around early-stage diagnosis, and improved clinical understanding of neurodevelopmental conditions. Strengthened screening practices and broader acceptance of developmental health assessments are contributing to higher diagnosis rates across multiple regions. Continuous improvements in genetic research, neuroimaging techniques, and standardized diagnostic frameworks are enabling earlier and more accurate identification of ASD, which is directly supporting demand for intervention and care services. Healthcare systems are increasingly prioritizing early intervention programs as evidence continues to highlight their role in improving long-term cognitive, behavioral, and social outcomes. In addition, expanding access to multidisciplinary care models that integrate behavioral therapy, educational support, and medical management is shaping treatment adoption patterns. Growing emphasis on individualized care planning and long-term developmental support is further strengthening market expansion globally, along with rising investments in autism-focused healthcare infrastructure and specialized care services.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $37.2 Billion |

| Forecast Value | $60.7 Billion |

| CAGR | 5.1% |

Autism spectrum disorder is defined as a complex neurodevelopmental condition marked by persistent challenges in communication, social interaction, behavior regulation, and sensory processing. Treatment strategies typically combine behavioral therapies, speech and occupational interventions, educational support systems, and medication-based approaches designed to manage symptoms and enhance functional abilities. The rising global awareness of ASD has significantly increased diagnostic rates, leading to higher demand for structured treatment programs and long-term support services. Advances in diagnostic tools and clinical screening methods have further improved early detection capabilities, enabling timely therapeutic intervention. Early identification is widely recognized as a key factor in improving developmental progress, communication skills, behavioral outcomes, and overall quality of life for individuals affected by ASD.

The drug class segment generated USD 18.3 billion in 2025. This segment includes multiple therapeutic categories such as antipsychotic medications, stimulants, selective serotonin reuptake inhibitors, and other related drug classes. Pharmacological interventions are widely used to manage associated symptoms, including irritability, anxiety, hyperactivity, mood disturbances, behavioral dysregulation, and communication difficulties. While autism spectrum disorder does not have a definitive cure, medication-based treatments play a critical role in improving symptom control and supporting daily functioning, particularly when combined with behavioral and therapeutic interventions.

The autistic disorder segment is projected to reach USD 32.7 billion by 2035, representing a significant share of the overall market. Growth in this segment is driven by the complex care requirements associated with more severe manifestations of autism spectrum disorder. Individuals within this category often require comprehensive and continuous support involving behavioral therapies, structured educational programs, clinical interventions, and long-term care services. The increasing demand for integrated treatment approaches focused on developmental improvement, communication enhancement, and functional independence is supporting sustained expansion within this segment.

North America Autism Spectrum Disorder Treatment Market accounted for 48.1% share in 2025. Market strength in the region is supported by well-established insurance coverage systems, advanced healthcare infrastructure, and widespread availability of specialized autism care and rehabilitation services. The region continues to benefit from high diagnostic awareness, strong adoption of early intervention programs, and increasing use of advanced therapeutic approaches. The integration of digital health solutions, remote therapy platforms, and hybrid care delivery models is further enhancing accessibility and treatment efficiency across the region.

Major companies operating in the Global Autism Spectrum Disorder Treatment Market include Mayo Foundation for Medical Education and Research (MFMER), Cleveland Clinic, Child Mind Institute, Autism Research Institute, The General Hospital, Jazz Pharmaceuticals, Pfizer, Novartis, Bristol Myers Squibb, AbbVie, Eli Lilly & Company, Viatris, Neurim Pharmaceuticals. Companies operating in the autism spectrum disorder treatment market are focusing on multiple strategic initiatives to strengthen their competitive position and expand long-term market reach. Leading organizations are increasing investments in clinical research, neurodevelopmental studies, and innovative therapeutic development to improve treatment effectiveness and patient outcomes. Strategic collaborations between pharmaceutical manufacturers, healthcare institutions, and research organizations are enhancing the development of advanced intervention models and expanding access to care. Companies are also prioritizing digital health integration, including telehealth-based therapy platforms and remote monitoring solutions, to improve accessibility and continuity of care. In addition, expanding early diagnosis programs, strengthening behavioral therapy networks, and enhancing patient support ecosystems are key priorities. The growing focus on personalized treatment approaches, combined therapeutic models, and data-driven care planning continues to drive innovation and competitive differentiation across the autism spectrum disorder treatment market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type trends

- 2.2.3 Disease trends

- 2.2.4 Age group trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of autism

- 3.2.1.2 Advancements in diagnostic tools

- 3.2.1.3 Innovation in therapeutics

- 3.2.1.4 Growing integration of digital & remote therapy models

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Variability in treatment efficacy

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of precision-based and biomarker-driven therapies

- 3.2.3.2 Growing demand for adult autism care ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Future market trends

- 3.6 Technological and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies (Driven by Primary Research)

- 3.7 Pipeline analysis (Driven by Primary Research)

- 3.8 Impact of AI and generative AI on the market (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Drug class

- 5.2.1 Antipsychotic drugs

- 5.2.2 Selective serotonin reuptake inhibitors

- 5.2.3 Stimulants

- 5.2.4 Other drug classes

- 5.3 Therapy

- 5.3.1 Behavior and communication therapies

- 5.3.2 Chelation therapy

- 5.3.3 Other therapies

- 5.4 Assistive apps

Chapter 6 Market Estimates and Forecast, By Disease, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Autistic disorder

- 6.3 Asperger syndrome

- 6.4 Pervasive developmental disorder (PDD)

- 6.5 Other diseases

Chapter 7 Market Estimates and Forecast, By Age Group, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Children

- 7.3 Adult

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Homecare settings

- 8.4 Rehabilitation centers

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Service Provider

- 10.1.1 Autism Research Institute

- 10.1.2 Child Mind Institute

- 10.1.3 Cleveland Clinic

- 10.1.4 Mayo Foundation for Medical Education and Research (MFMER).

- 10.1.5 The General Hospital

- 10.2 Medication Manufacturer

- 10.2.1 Jazz Pharmaceuticals

- 10.2.2 Bristol Myers Squibb

- 10.2.3 Pfizer

- 10.2.4 Novartis

- 10.2.5 AbbVie

- 10.2.6 Viatris

- 10.2.7 Eli Lilly & Company

- 10.2.8 Neurim Pharmaceuticals

自閉症篩檢和診斷工具市場預測——按工具類型、經營模式、交付方式、最終用戶和地區分類的全球分析——2034年

自閉症篩檢和診斷工具市場預測——按工具類型、經營模式、交付方式、最終用戶和地區分類的全球分析——2034年 泛自閉症障礙市場:依年齡層、治療方法、嚴重程度、最終用戶和通路分類-2026-2032年全球市場預測

泛自閉症障礙市場:依年齡層、治療方法、嚴重程度、最終用戶和通路分類-2026-2032年全球市場預測 2026-2034年全球泛自閉症障礙治療市場規模、佔有率、趨勢和成長分析報告2026-2034年全球泛自閉症障礙治療市場規模、佔有率、趨勢和成長分析報告全球泛自閉症障礙診斷市場規模、佔有率、趨勢和成長分析報告(2026-2034)

2026-2034年全球泛自閉症障礙治療市場規模、佔有率、趨勢和成長分析報告2026-2034年全球泛自閉症障礙治療市場規模、佔有率、趨勢和成長分析報告全球泛自閉症障礙診斷市場規模、佔有率、趨勢和成長分析報告(2026-2034) 日本泛自閉症障礙市場規模、佔有率、趨勢和預測:按自閉症類型、治療方法和地區分類,2026-2034年

日本泛自閉症障礙市場規模、佔有率、趨勢和預測:按自閉症類型、治療方法和地區分類,2026-2034年 泛自閉症障礙治療藥物市場:依藥物類型、年齡層、通路和地區分類

泛自閉症障礙治療藥物市場:依藥物類型、年齡層、通路和地區分類 泛自閉症障礙(ASD):新興療法、未滿足的需求和TPP洞察報告,2026年自閉症譜系障礙治療市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,以及2025年至2034年的預測自閉症譜系障礙(ASD)治療市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2025-2034)

泛自閉症障礙(ASD):新興療法、未滿足的需求和TPP洞察報告,2026年自閉症譜系障礙治療市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,以及2025年至2034年的預測自閉症譜系障礙(ASD)治療市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2025-2034)