|

市場調查報告書

商品編碼

2061414

太陽能電池封裝市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。Solar Encapsulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

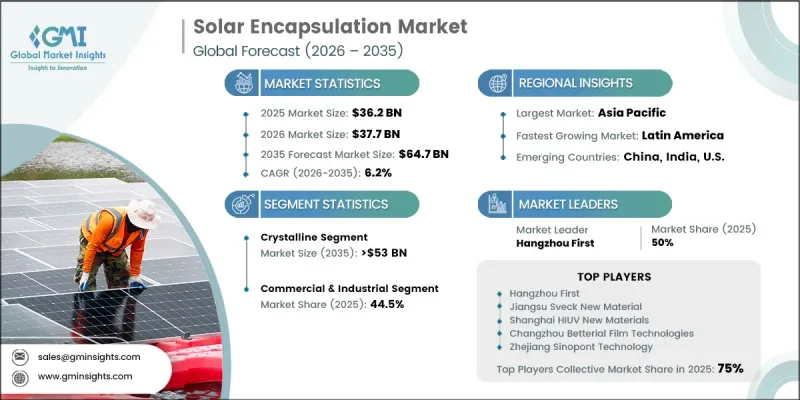

全球太陽能電池封裝市場預計到 2025 年將價值 362 億美元,預計到 2035 年將以 6.2% 的複合年成長率成長至 647 億美元。

太陽能電池封裝產業的整體成長主要得益於太陽能製造在地化進程的加速以及對提升國內太陽能發電能力的投資不斷增加。已開發國家和開發中國家的政府都在積極推動光學模組製造的自給自足,從而在全部區域供應鏈中創造了對高性能封裝的巨大需求。隨著全球光學模組產能的持續擴張,封裝的消耗量預計將穩定成長。減少對進口太陽能組件依賴的努力正在推動對本地製造生態系統的投資,進而提升對關鍵太陽能材料的需求。垂直整合型太陽能製造商的崛起也導致了封裝產品的大規模採購,進一步推動了市場成長。此外,太陽能發電工程投資的增加也為能夠提升組件耐久性和運作效率的高品質封裝創造了機會。長期太陽能部署策略以及對整個太陽能價值鏈成本最佳化的日益重視,都進一步強化了市場需求。此外,太陽能技術的進步和組件設計的演變,增加了對能夠提供卓越性能、可靠性和長期保護的專用封裝解決方案的需求,從而增強了全球太陽能電池封裝市場的積極前景。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 362億美元 |

| 預測金額 | 647億美元 |

| 複合年成長率 | 6.2% |

高效能太陽能電池組件的日益普及進一步推動了太陽能電池封裝市場的創新。業界對能夠適應不斷發展的太陽能電池結構,同時提升光學性能、機械強度和電絕緣性能的先進封裝的需求日益成長。隨著太陽能電池製造商不斷致力於最大化能量輸出和延長組件壽命,對技術先進的封裝解決方案的需求變得愈發迫切。持續的材料創新有望在支持下一代光電系統和維持市場長期擴張方面發揮至關重要的作用。

預計到2035年,晶體矽太陽能電池市場規模將達到530億美元,主要得益於其在經濟高效的太陽能電池組件生產中的廣泛應用。該領域使用的封裝因其能夠提供可靠的熱穩定性、紫外線防護和長期的組件耐久性,同時保持價格合理而備受青睞。晶體矽電池技術相對簡單的結構需求,持續推動成熟封裝解決方案的應用,從而支撐著該領域的持續成長。晶體矽光學模組在全球的普及,仍是推動封裝需求成長的關鍵因素。

預計到2035年,住宅應用市場規模將達到178億美元。市場成長的主要驅動力是越來越多的住宅安裝屋頂太陽能發電系統,以尋求可靠且持久的可再生能源解決方案。住宅光學模組需要封裝,以確保其在長期運作中保持光學透明度、耐候性和結構完整性。消費者對美觀的太陽能裝置日益成長的需求,以及太陽光電技術在住宅建築中的持續應用,進一步推動了該領域對高品質封裝的需求成長。

預計到2025年,美國太陽能電池封裝市場規模將達98億美元。該地區市場擴張的驅動力在於加大投資,旨在增強國內太陽能製造能力並提高供應鏈韌性。提高太陽能材料在地化生產能力並減少對外部資源的依賴,為封裝製造商創造了有利的市場環境。持續的政策支持和不斷擴大的太陽能普及活動預計將在預測期內進一步推動北美市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系統

- 原物料供應商

- 封裝膜製造商

- 太陽能電池組件OEM製造商和層壓設備製造商

- IPC承包商和下游安裝公司

- 終端需求者和獨立發電商(IPP)

- 監理情勢

- 太陽能發電封裝材料的IEC標準

- 歐盟 REACH 和 RoHS 法規合規性對封裝劑化學性質的影響

- 反傾銷措施與貿易政策

- 各國可再生能源強制政策及其對封裝材料需求的影響。

- 環境與回收法規

- 影響產業的因素

- 成長促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTLE分析

- 技術與創新展望

- EVA技術的發展與局限性

- POE和非EVA封裝的進展

- 下一代封裝材料技術

- 鈣鈦礦和串聯組件的封裝要求

- 智慧安裝媒體和功能整合

- 價格分析

- 按材料分析歷史價格趨勢

- 定價策略:按業務類型分類

- 原料成本對封裝劑價格的影響

- 貿易數據分析

- 按黏合劑類型分類的進出口量和進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧的影響

- 人工智慧驅動的封裝設計和配方製程變革。

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 人工智慧在太陽能發電製造中的風險、限制和監管考量。

- 生產能力和生產情況

- 各地區及主要生產商的產能

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 按公司規模進行基準測試

- 排名分類標準與遴選標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場規模及預測:依面板類型分類,2022-2035年

- 晶體系統

- 薄膜

- 其他

第6章 市場規模及預測:依材料類型分類,2022-2035年

- EVA

- 透明的

- 白色的

- POE

- EPE

第7章 市場規模及預測:依應用領域分類,2022-2035年

- 住宅

- 商業和工業用途

- 公用事業

第8章 市場規模及預測:依最終用途分類,2022-2035年

- 建造

- 電子設備

- 其他

第9章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 奧地利

- 丹麥

- 芬蘭

- 法國

- 德國

- 義大利

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 新加坡

- 中東和非洲

- 以色列

- 沙烏地阿拉伯

- UAE

- 約旦

- 阿曼

- 拉丁美洲

- 巴西

- 智利

- 阿根廷

- 秘魯

第10章:公司簡介

- 3M

- Alishan Green Energy

- Al Technology

- Changzhou Betterial Film Technologies

- Crown Advanced Materials

- Cybrid Technologies

- Dow Corning

- DuPont

- Eastman

- Endurans Solar

- Enrich Encap Pvt Ltd.

- First Solar

- Hangzhou First PV Material

- Jiangsu Sveck New Material

- Jolywood(Suzhou)Sunwatt

- Momentive

- Mitsubishi Chemicals

- RenewSys India

- SATINAL SpA

- Shanghai HIUV New Materials

- Sunlink Photovoltaic

- Zhejiang Sinopont Technology

The Global Solar Encapsulation Market was valued at USD 36.2 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 64.7 billion by 2035.

Growth across the solar encapsulation industry is supported by the accelerating transition toward localized solar manufacturing and increasing investments aimed at strengthening domestic photovoltaic production capabilities. Governments across both developed and developing economies are actively promoting self-sufficiency in solar module manufacturing, creating substantial demand for high-performance encapsulation materials throughout regional supply chains. As solar module production capacity continues to expand globally, consumption of encapsulation materials is expected to rise steadily. Efforts to reduce reliance on imported solar components are encouraging greater investment in local manufacturing ecosystems, which is increasing demand for critical photovoltaic materials. The emergence of vertically integrated solar manufacturers is also contributing to large-scale procurement of encapsulation products, further supporting market growth. In addition, growing investments in solar power generation projects are creating favorable opportunities for premium encapsulation materials that enhance module durability and operational efficiency. Long-term solar deployment strategies and increasing focus on cost optimization throughout the solar value chain continue to strengthen demand. Furthermore, advancements in photovoltaic technologies and evolving module designs are increasing the need for specialized encapsulation solutions capable of delivering superior performance, reliability, and long-term protection, reinforcing the positive outlook for the global solar encapsulation market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $36.2 Billion |

| Forecast Value | $64.7 Billion |

| CAGR | 6.2% |

Increasing adoption of high-efficiency solar modules is further driving innovation within the solar encapsulation market. The industry is witnessing rising demand for advanced encapsulation materials that can support evolving photovoltaic cell architectures while delivering improved optical performance, mechanical strength, and electrical insulation characteristics. As solar manufacturers continue to focus on maximizing energy output and module lifespan, the need for technologically advanced encapsulation solutions is becoming increasingly important. Continuous material innovation is expected to play a critical role in supporting the next generation of solar energy systems and sustaining long-term market expansion.

The crystalline segment is projected to reach USD 53 billion by 2035, supported by its widespread utilization in cost-effective solar module production. Encapsulation materials used within this segment are valued for their ability to provide dependable thermal stability, ultraviolet protection, and long-term module durability while maintaining affordability. The relatively straightforward structural requirements associated with crystalline technologies continue to encourage the use of established encapsulation solutions, supporting ongoing growth across the segment. Strong adoption of crystalline solar modules worldwide remains a key factor contributing to increasing demand for encapsulation materials.

The residential application segment is expected to reach USD 17.8 billion by 2035. Market growth is being driven by the increasing installation of rooftop solar systems among homeowners seeking reliable and long-lasting renewable energy solutions. Residential solar modules require encapsulation materials capable of maintaining optical transparency, weather resistance, and structural integrity over extended operating periods. Growing consumer interest in aesthetically appealing solar installations and the continued integration of solar technologies into residential structures are further contributing to rising demand for premium encapsulation products within this segment.

U.S. Solar Encapsulation Market was valued at USD 9.8 billion in 2025.Market expansion across the region is being supported by increasing investments aimed at strengthening domestic solar manufacturing capabilities and improving supply chain resilience. Efforts to enhance regional production of photovoltaic materials and reduce external supply dependencies are creating favorable conditions for encapsulation material manufacturers. Continued policy support and growing solar deployment activities are expected to further stimulate market growth throughout North America over the forecast period.

Major companies operating in the Global Solar Encapsulation Industry include 3M, Alishan Green Energy, Al Technology, Changzhou Betterial Film Technologies, Crown Advanced Materials, Cybrid Technologies, Dow Corning, DuPont, Eastman, Endurans Solar, Enrich Encap Pvt Ltd., First Solar, Hangzhou First PV Material, Jiangsu Sveck New Material, Jolywood (Suzhou) Sunwatt, Momentive, Mitsubishi Chemicals, RenewSys India, SATINAL SpA, Shanghai HIUV New Materials, Sunlink Photovoltaic, and Zhejiang Sinopont Technology. Companies participating in the solar encapsulation market are implementing a range of strategic initiatives to strengthen their market position and expand their competitive advantage. Significant investments in research and development are focused on enhancing material durability, optical performance, weather resistance, and compatibility with advanced photovoltaic technologies. Manufacturers are also expanding production capacities to meet growing global demand and improve supply chain reliability. Strategic partnerships with solar module producers and long-term supply agreements are helping companies secure stable revenue streams and strengthen customer relationships. Many industry participants are pursuing geographic expansion strategies to increase their presence in high-growth solar markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Panel type trends

- 2.4 Material type trends

- 2.5 Application trends

- 2.6 End use trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw Material Suppliers

- 3.1.2 Encapsulant Film Manufacturers

- 3.1.3 Solar Module OEMs & Lamination Equipment Providers

- 3.1.4 EPC Contractors & Downstream Installers

- 3.1.5 End-Use Buyers & Independent Power Producers (IPPs)

- 3.2 Regulatory landscape

- 3.2.1 IEC Standards for PV Encapsulants

- 3.2.2 EU REACH & RoHS Compliance Impact on Encapsulant Chemistry

- 3.2.3 Anti-Dumping Measures & Trade Policies

- 3.2.4 National Renewable Energy Mandates & Their Encapsulant Demand Implications

- 3.2.5 Environmental & Recycling Regulations

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Technology & innovation landscape

- 3.7.1 EVA Technology Evolution & Limitations

- 3.7.2 POE & Non-EVA Encapsulant Advancements

- 3.7.3 Next-Generation Encapsulant Technologies

- 3.7.4 Encapsulant Requirements for Perovskite & Tandem Modules

- 3.7.5 Smart Encapsulants & Functional Integration

- 3.8 Pricing Analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis by Material Type

- 3.8.2 Pricing Strategy by Player Type

- 3.8.3 Impact of Raw Material Costs on Encapsulant Pricing

- 3.9 Trade Data Analysis (Driven by Primary Research)

- 3.9.1 Import/Export Volume & Value Trends by Encapsulant Type

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Impact of AI & Generative AI (Solution Core)

- 3.10.1 AI-Driven Disruption of Encapsulant Design & Formulation Processes

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, Limitations & Regulatory Considerations for AI in PV Manufacturing

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Installed Production Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipeline

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Panel Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Crystalline

- 5.3 Thin Film

- 5.4 Others

Chapter 6 Market Size and Forecast, By Material Type, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 EVA

- 6.2.1 Transparent

- 6.2.2 White

- 6.3 POE

- 6.4 EPE

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial & industrial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By End Use, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Construction

- 8.3 Electronics

- 8.4 Others

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Austria

- 9.3.2 Denmark

- 9.3.3 Finland

- 9.3.4 France

- 9.3.5 Germany

- 9.3.6 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.5 Middle East and Africa

- 9.5.1 Israel

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

- 9.5.4 Jordan

- 9.5.5 Oman

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Chile

- 9.6.3 Argentina

- 9.6.4 Peru

Chapter 10 Company Profiles

- 10.1 3M

- 10.2 Alishan Green Energy

- 10.3 Al Technology

- 10.4 Changzhou Betterial Film Technologies

- 10.5 Crown Advanced Materials

- 10.6 Cybrid Technologies

- 10.7 Dow Corning

- 10.8 DuPont

- 10.9 Eastman

- 10.10 Endurans Solar

- 10.11 Enrich Encap Pvt Ltd.

- 10.12 First Solar

- 10.13 Hangzhou First PV Material

- 10.14 Jiangsu Sveck New Material

- 10.15 Jolywood (Suzhou) Sunwatt

- 10.16 Momentive

- 10.17 Mitsubishi Chemicals

- 10.18 RenewSys India

- 10.19 SATINAL SpA

- 10.20 Shanghai HIUV New Materials

- 10.21 Sunlink Photovoltaic

- 10.22 Zhejiang Sinopont Technology

太陽能纖維素封裝市場規模、佔有率、趨勢和預測:按材料、技術、應用和地區分類,2026-2034年

太陽能纖維素封裝市場規模、佔有率、趨勢和預測:按材料、技術、應用和地區分類,2026-2034年 太陽能纖維素封裝市場:按材料、技術、安裝類型、透明度、封裝方法、應用和最終用戶分類-2026-2032年全球市場預測太陽能電池封裝市場:按材料類型、技術、最終用途和應用分類-2026-2032年全球市場預測建築用太陽能封裝市場:依材料類型、製程、最終用途、應用類型和分銷管道分類-全球預測,2026-2032年

太陽能纖維素封裝市場:按材料、技術、安裝類型、透明度、封裝方法、應用和最終用戶分類-2026-2032年全球市場預測太陽能電池封裝市場:按材料類型、技術、最終用途和應用分類-2026-2032年全球市場預測建築用太陽能封裝市場:依材料類型、製程、最終用途、應用類型和分銷管道分類-全球預測,2026-2032年 2026年全球太陽能封裝市場報告

2026年全球太陽能封裝市場報告 太陽能電池封裝市場規模、佔有率和成長分析(按材料、技術、應用和地區分類)—2026-2033年產業預測

太陽能電池封裝市場規模、佔有率和成長分析(按材料、技術、應用和地區分類)—2026-2033年產業預測 太陽能電池封裝:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

太陽能電池封裝:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 美國光伏封裝封裝市場規模、佔有率及趨勢分析報告:2025-2033年材料、技術、應用及細分市場預測太陽能電池封裝市場規模、佔有率及趨勢分析報告:依材料、技術、應用、地區及細分市場預測,2025-2033年

美國光伏封裝封裝市場規模、佔有率及趨勢分析報告:2025-2033年材料、技術、應用及細分市場預測太陽能電池封裝市場規模、佔有率及趨勢分析報告:依材料、技術、應用、地區及細分市場預測,2025-2033年 太陽能電池封裝材的全球市場的評估:類別,面板類別,各用途,各地區,機會,預測(2018年~2032年)

太陽能電池封裝材的全球市場的評估:類別,面板類別,各用途,各地區,機會,預測(2018年~2032年)