|

市場調查報告書

商品編碼

2061402

2026 年至 2035 年重症監護醫療設備市場的商業機會、成長要素、產業趨勢與預測。Critical Care Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

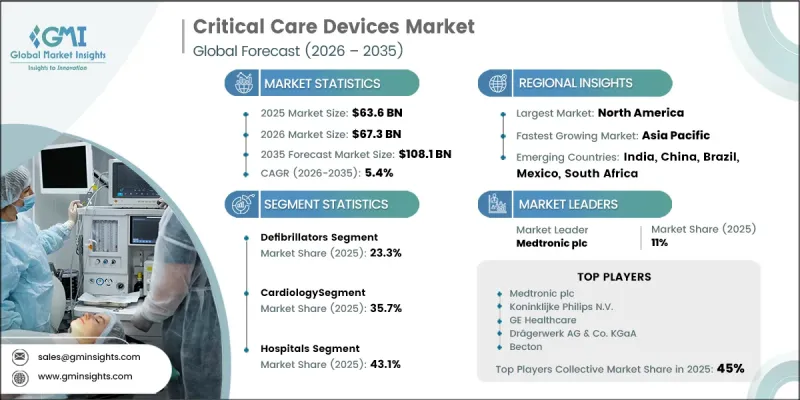

預計到 2025 年,全球重症監護醫療設備市場規模將達到 636 億美元,並預計以 5.4% 的複合年成長率成長,到 2035 年達到 1,081 億美元。

市場擴張的促進因素包括對先進重症監護解決方案日益成長的需求、慢性病盛行率的上升以及重症監護技術的持續進步。全球醫療系統面臨越來越大的壓力,需要更有效地管理重症患者,加速了先進病患監測設備的應用。重症監護醫療設備旨在支持和維持急診和重症監護環境下的生命維持生理功能,使醫護人員能夠提供持續監測和快速醫療干預。人口老化、生活方式的改變以及因醫療需求增加而導致的慢性病發病率上升,都顯著促進了市場成長。需要密切醫療監護和長期重症監護支援的患者數量不斷增加,進一步推高了對技術先進的醫療設備的需求。此外,醫療基礎設施的擴建、對重症監護設施投資的增加以及數位監護技術的整合,正在推動全球醫院和專科醫療中心更廣泛地採用重症監護系統。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 636億美元 |

| 預計金額 | 1081億美元 |

| 複合年成長率 | 5.4% |

重症監護設備是指在重症監護環境中用於支援對嚴重或生命垂危患者進行監測和穩定治療的專用醫療技術。這些系統廣泛用於維持重要器官功能,並在緊急醫療程序中改善病患管理。對持續患者監測和先進治療支援的需求不斷成長,推動了醫療機構對重症監護技術的應用。慢性病和需要即時乾預的急性疾病負擔日益加重,也促進了該行業的擴張。對加護病房(ICU)需求的不斷成長,也推動了整個醫療保健產業對先進監測和生命維持系統的廣泛應用。

截至2025年,去心房顫動市佔率將達到23.3%。由於去心房顫動在嚴重心臟併發症的緊急情況下恢復正常心率方面發揮著至關重要的作用,因此市場需求持續成長。技術的不斷進步提高了設備在急救環境中的便攜性、操作效率和易用性。人們對緊急心臟反應系統的認知不斷提高,以及急救服務的擴展,進一步推動了該領域的成長。技術先進的去心房顫動系統的普及也促進了其在醫院和重症監護室的廣泛應用。

到2025年,循環系統領域將佔據35.7%的市場。全球心血管疾病負擔日益加重,以及對快速心臟介入技術的需求不斷成長,使得循環系統醫學成為重症監護設備應用最廣泛的領域之一。用於心臟病學的重症監護系統使醫護人員能夠持續監測患者,並在出現危及生命的心臟疾病時提供即時治療支持。因心臟併發症而入住ICU的患者數量不斷增加,顯著提升了對先進心臟監測技術和支援設備的需求。即時監測系統和心臟護理技術的持續創新,進一步推動了全球醫療機構中這一領域的擴張。

預計到2025年,北美重症監護設備市佔率將達到37.5%。由於慢性病盛行率上升和對重症監護服務的需求不斷成長,該地區持續保持強勁的市場地位。心血管和呼吸系統疾病盛行率的上升導致住院率和重症監護室(ICU)入院率增加,從而推動了醫療機構對先進重症監護技術的需求。北美也受惠於高度發展的醫療基礎設施、有利的報銷機制以及先進醫療設備的廣泛應用。美國和加拿大的醫院持續大力投資於先進的重症監護系統,從而滿足了全部區域對監護設備、液體管理系統和生命維持技術的持續需求。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 對加護病房的需求不斷成長

- 全球慢性病發生率正在上升。

- 重症監護技術的進步

- 為加強疾病控制,人工呼吸器需求激增。

- 產業潛在風險與挑戰

- 熟練專業人員短缺

- 重症監護設備高成本

- 市場機遇

- 改善緊急醫療服務(EMS)

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術展望

- 最新科技趨勢

- 多參數病患監測系統

- 連續性腎臟替代療法(CRRT)系統

- 新興技術

- 遠端ICU和遠端監控解決方案

- 人工智慧整合重症監護系統

- 最新科技趨勢

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 價格趨勢分析

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 去心房顫動

- 多參數監測設備

- 心電圖(ECG)設備

- 血液透析機

- 點滴幫浦

- 人工呼吸器

- 腸內營養管

- 麻醉監控器

- CRRT裝置

- 其他產品

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 腎臟護理

- 循環系統

- 神經病學

- 其他用途

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 門診手術中心

- 專科診所

- 其他最終用戶

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第9章:公司簡介

- Abbott Laboratories

- Air Liquide Medical Systems India

- Asahi Kasei Corporation

- B. Braun Melsungen

- Baxter

- Becton, Dickinson and Company

- Boston Scientific Corporation

- Cardinal Health

- Dragerwerk

- Fresenius Medical Care

- GE Healthcare

- Getinge

- Hamilton Medical

- ICU Medical

- Koninklijke Philips

- Medtronic

The Global Critical Care Devices Market was valued at USD 63.6 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 108.1 billion by 2035.

Market expansion is driven by the increasing need for advanced intensive care solutions, the rising prevalence of chronic health conditions, and ongoing technological advancements in critical care technologies. Growing pressure on healthcare systems worldwide to manage critically ill patients more effectively is accelerating the adoption of sophisticated life-support and patient monitoring equipment. Critical care devices are designed to support and maintain vital physiological functions in emergency and intensive care environments, enabling healthcare professionals to deliver continuous monitoring and rapid medical intervention. Rising incidences of chronic disorders associated with aging populations, changing lifestyles, and increasing healthcare demands are contributing significantly to market growth. The growing number of patients requiring intensive medical supervision and long-term critical care support is further increasing the demand for technologically advanced medical devices. In addition, expanding healthcare infrastructure, increasing investments in intensive care facilities, and the integration of digital monitoring technologies are supporting broader adoption of critical care systems across hospitals and specialized healthcare centers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $63.6 Billion |

| Forecast Value | $108.1 Billion |

| CAGR | 5.4% |

Critical care devices are specialized medical technologies used within intensive care environments to assist in monitoring and stabilizing patients experiencing severe or life-threatening health conditions. These systems are widely utilized to support essential organ functions and improve patient management during emergency treatment procedures. Rising demand for continuous patient observation and advanced therapeutic support is strengthening the adoption of critical care technologies across healthcare facilities. The increasing burden of chronic illnesses and acute medical conditions requiring immediate intervention is further contributing to industry expansion. Growing demand for intensive care units is also supporting the widespread deployment of advanced monitoring and life-support systems throughout the healthcare sector.

The Defibrillators segment accounted for 23.3% share in 2025. Demand for defibrillators continues to rise due to their critical role in restoring normal cardiac rhythm during emergency situations involving severe cardiac complications. Ongoing technological advancements have improved device portability, operational efficiency, and accessibility across emergency care settings. Increasing awareness regarding emergency cardiac response systems and expanding emergency healthcare services are further contributing to the growth of the segment. The availability of technologically advanced defibrillation systems is also supporting wider adoption across hospitals and critical care facilities.

The cardiology segment held a share of 35.7% in 2025. Cardiology remains one of the largest application areas for critical care devices due to the growing global burden of cardiovascular disorders and increasing demand for rapid cardiac intervention technologies. Critical care systems used in cardiology applications enable healthcare professionals to monitor patients continuously and provide immediate therapeutic support during life-threatening cardiac conditions. Rising ICU admissions related to cardiac complications are significantly increasing the demand for advanced cardiac monitoring technologies and support devices. Continuous innovation in real-time monitoring systems and cardiac care technologies is further strengthening the expansion of this segment across healthcare institutions worldwide.

North America Critical Care Devices Market held a 37.5% share in 2025. The region continues to maintain a strong market position due to increasing rates of chronic illnesses and rising demand for intensive healthcare services. The growing prevalence of cardiovascular and respiratory conditions is contributing to higher hospitalization and ICU admission rates, driving the need for advanced critical care technologies across healthcare facilities. North America also benefits from a highly developed healthcare infrastructure, favorable reimbursement systems, and widespread adoption of technologically advanced medical devices. Hospitals throughout the U.S. and Canada continue to invest heavily in advanced intensive care systems, supporting sustained demand for monitoring equipment, infusion systems, and life-support technologies across the region.

Major companies operating in the Global Critical Care Devices Market include Abbott Laboratories, Air Liquide Medical Systems India, Asahi Kasei Corporation, B. Braun Melsungen, Baxter, Becton, Dickinson and Company, Boston Scientific Corporation, Cardinal Health, Dragerwerk, Fresenius Medical Care, GE Healthcare, Getinge, Hamilton Medical, ICU Medical, Koninklijke Philips, and Medtronic. Companies operating in the critical care devices market are adopting several strategic initiatives to strengthen their market presence and expand their competitive positioning globally. Industry participants are investing heavily in research and development activities to introduce technologically advanced monitoring systems, life-support equipment, and integrated digital healthcare solutions. Strategic mergers, acquisitions, and collaborations are helping companies expand product portfolios and improve geographic reach. Market players are also focusing on incorporating artificial intelligence, remote patient monitoring, and data-driven healthcare technologies into critical care systems to improve clinical efficiency and patient outcomes. Expanding manufacturing capabilities, strengthening distribution networks, and increasing investments in healthcare infrastructure partnerships are further supporting business growth.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy and data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy and data integrity commitment

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for intensive care units

- 3.2.1.2 Growing incidence of chronic diseases throughout the globe

- 3.2.1.3 Technological advancements in critical care

- 3.2.1.4 Surging demand for ventilators for better management of diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals

- 3.2.2.2 High cost of critical care devices

- 3.2.3 Market opportunities

- 3.2.3.1 Improvement in emergency medical services (EMS)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.1.1 Multiparameter patient monitoring systems

- 3.5.1.2 Continuous renal replacement therapy (CRRT) Systems

- 3.5.2 Emerging technologies

- 3.5.2.1 Tele-ICU and remote monitoring solutions

- 3.5.2.2 AI-Integrated critical care systems

- 3.5.1 Current technological trends

- 3.6 Future market trends (Driven by primary research)

- 3.7 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.8 Pricing trend analysis (Driven by primary research)

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Defibrillators

- 5.3 Multiparameter monitoring devices

- 5.4 ECG devices

- 5.5 Hemodialysis machines

- 5.6 Infusion pumps

- 5.7 Ventilators

- 5.8 Feeding tubes

- 5.9 Anesthesia monitors

- 5.10 CRRT machines

- 5.11 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn and Units)

- 6.1 Key trends

- 6.2 Renal care

- 6.3 Cardiology

- 6.4 Neurology

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn and Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Air Liquide Medical Systems India

- 9.3 Asahi Kasei Corporation

- 9.4 B. Braun Melsungen

- 9.5 Baxter

- 9.6 Becton, Dickinson and Company

- 9.7 Boston Scientific Corporation

- 9.8 Cardinal Health

- 9.9 Dragerwerk

- 9.10 Fresenius Medical Care

- 9.11 GE Healthcare

- 9.12 Getinge

- 9.13 Hamilton Medical

- 9.14 ICU Medical

- 9.15 Koninklijke Philips

- 9.16 Medtronic

重症監護醫療設備市場規模、佔有率和成長分析:按產品類型、應用、病患類型、最終用戶和地區分類-2026-2033年產業預測

重症監護醫療設備市場規模、佔有率和成長分析:按產品類型、應用、病患類型、最終用戶和地區分類-2026-2033年產業預測 重症監護診斷市場預測至2034年-按產品類型、檢測類型、最終用戶和地區分類的全球分析

重症監護診斷市場預測至2034年-按產品類型、檢測類型、最終用戶和地區分類的全球分析 新生兒重症監護設備市場:依人工呼吸器、最終用戶和分銷管道分類-2026-2032年全球市場預測急救醫療設備市場:按產品類型、便攜性、分銷管道和最終用戶分類-全球市場預測(2026-2032 年)重症醫學市場:2026-2032年全球市場預測(按產品類型、給藥途徑、患者族群、治療應用和最終用戶分類)重症加護診斷市場:2026-2032年全球市場預測(按產品類型、技術、檢測模式、應用和最終用戶分類)

新生兒重症監護設備市場:依人工呼吸器、最終用戶和分銷管道分類-2026-2032年全球市場預測急救醫療設備市場:按產品類型、便攜性、分銷管道和最終用戶分類-全球市場預測(2026-2032 年)重症醫學市場:2026-2032年全球市場預測(按產品類型、給藥途徑、患者族群、治療應用和最終用戶分類)重症加護診斷市場:2026-2032年全球市場預測(按產品類型、技術、檢測模式、應用和最終用戶分類) 2026年全球重症醫學市場報告2026年全球重症監護設備市場報告

2026年全球重症醫學市場報告2026年全球重症監護設備市場報告 全球新生兒重症監護設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球新生兒重症監護設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 重症監護資訊系統市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、應用、最終用戶、地區和競爭格局分類,2021-2031年

重症監護資訊系統市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、應用、最終用戶、地區和競爭格局分類,2021-2031年