|

市場調查報告書

商品編碼

2061395

孕酮市場商機、成長要素、產業趨勢分析及2026-2035年預測。Progesterone Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

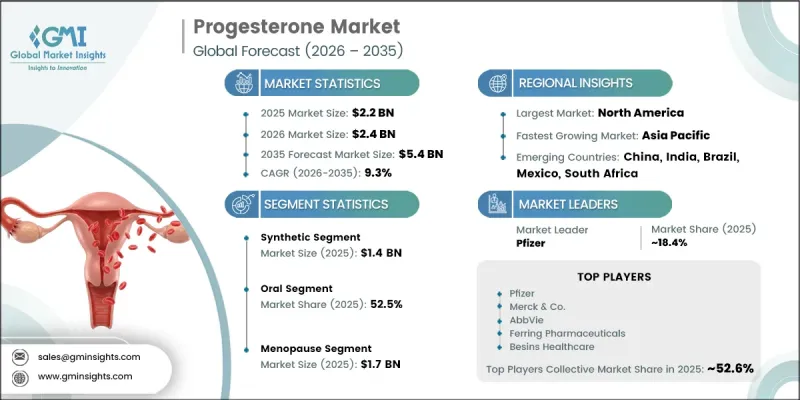

預計到 2025 年,全球孕酮市場價值將達到 22 億美元,並預計以 9.3% 的複合年成長率成長,到 2035 年達到 54 億美元。

市場擴張的促進因素包括:荷爾蒙失衡的日益普遍、荷爾蒙補充療法(HRT)的廣泛應用、全球不孕症發病率的上升以及女性生殖和荷爾蒙健康意識的增強。孕激素在生殖醫學中日益重要的角色也推動了市場需求。黃體素廣泛用於調節月經週期、維持懷孕、降低流產和早產風險、緩解更年期症狀。它仍然廣泛應用於避孕、輔助生殖技術(ART)、不孕症治療和更年期治療,並且是婦科治療方案的核心組成部分。正如全球健康評估所指出的,全球不孕症盛行率的上升影響著數百萬育齡女性,這進一步加劇了對荷爾蒙支持療法的需求。同時,體外受精 (IVF) 和胚胎移植等輔助生殖技術 (ART) 的日益普及,顯著提高了醫療保健機構對黃體素製劑的需求,包括膠囊、凝膠、注射和陰道內給藥系統。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 22億美元 |

| 預測金額 | 54億美元 |

| 複合年成長率 | 9.3% |

預計到2025年,合成荷爾蒙市場規模將達到14億美元,並在2035年之前以9.5%的複合年成長率成長。合成黃體素產品的強勁表現得益於其在口服避孕藥、荷爾蒙補充療法、生育治療方案以及婦科疾病治療中的廣泛應用。這些製劑因其長期的臨床應用記錄、成本效益、高穩定性和長保存期限而備受青睞,使其適用於大規模醫療機構。此外,非專利合成荷爾蒙療法的廣泛普及及其在聯合療法中的應用也進一步推動了市場成長,提高了已開發和新興醫療體系的醫療服務可近性。

到2025年,口服藥物將佔52.5%的市場。口服黃體素療法因其使用方便性、醫生支持力度大以及應用範圍廣泛(包括荷爾蒙補充療法、不孕症治療、月經失調治療和孕期支持護理)而被廣泛採用。患者遵守用藥的提高、給藥的便捷性以及緩釋製劑的日益普及(這些製劑可增強吸收和治療效果)進一步鞏固了其受歡迎程度。接受生物等效荷爾蒙療法的閉經患者對口服黃體素的需求增加,也進一步推動了全球對口服黃體素產品的需求。

預計到2025年,北美孕酮市佔率將達到37.8%。該地區孕酮市場的主導地位主要得益於荷爾蒙補充療法的高普及率、不斷成長的生育治療計畫以及患者和醫護人員對生殖健康意識的提高。尤其在美國,成熟的生育生態系統取得了成功,體外受精(IVF)和胚胎移植手術數量的增加,帶動了黃體期支持使用黃體素的強勁需求。微粒化口服黃體素製劑的持續進步、生物等效荷爾蒙療法的日益普及以及臨床意識的提高,都進一步推動了全部區域孕酮市場的成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 不孕症和荷爾蒙失調症的盛行率增加

- 荷爾蒙補充療法(HRT)的廣泛應用

- 擴大婦女醫療保健基礎設施和生殖醫學。

- 藥物遞送製劑的進展

- 產業潛在風險與挑戰

- 人們對荷爾蒙療法的副作用和安全性有擔憂

- 嚴格的法規和臨床核准要求

- 不孕症替代療法和荷爾蒙療法的可及性

- 市場機遇

- 對生物同源性和個人化荷爾蒙療法的需求日益成長

- 進入新興市場

- 促進因素

- 監理情勢

- 技術展望

- 最新科技趨勢

- 新興技術

- 未來市場趨勢

- 波特的分析

- PESTLE分析

- 價格分析

- 對過去價格趨勢的分析

- 按產品類型分類的定價策略

- 管線分析和臨床試驗趨勢

- 專利趨勢

- 投資與資金籌措分析

- 各國出生率(人均出生人數)

- 差距分析

- 人工智慧和生成式人工智慧對市場的影響

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依配方分類,2022-2035年

- Natural

- 合成

第6章 市場估計與預測:依給藥途徑分類,2022-2035年

- 注射藥物

- 口服

- 經皮

- 其他給藥途徑

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 停經

- 避孕

- 功能性子宮出血

- 增生性前驅病變

- 子宮內膜癌

- 其他用途

第8章 市場估算與預測:依藥物類型分類,2022-2035年

- 品牌

- 非專利的

第9章 市場估計與預測:依類型分類,2022-2035年

- 處方

- OTC

第10章 市場估價與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第12章:公司簡介

- AbbVie

- Alkem Laboratories

- Bayer AG

- Besins Healthcare

- Cipla

- Ferring Pharmaceuticals

- Glenmark Pharmaceuticals

- Gedeon Richter

- Lupin Limited

- Merck &Co.

- Organon

- Pfizer

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

- TherapeuticsMD

- Viatris(Mylan)

- Xiromed

- Zydus Lifesciences

The Global Progesterone Market was valued at USD 2.2 billion in 2025 and is estimated to grow at a CAGR of 9.3% to reach USD 5.4 billion by 2035.

Market expansion is supported by the rising incidence of hormonal imbalances, increasing uptake of hormone replacement therapy (HRT), higher infertility treatment rates worldwide, and growing awareness of women's reproductive and hormonal health. Demand is also being reinforced by the expanding role of progesterone in reproductive medicine, where it is widely used to regulate menstrual cycles, support pregnancy maintenance, reduce risks linked to miscarriage and preterm birth, and manage menopausal symptoms. The hormone continues to be extensively utilized across contraception, assisted reproductive technologies (ART), infertility care, and menopausal therapy, making it a core component of gynecological treatment protocols. Rising global infertility prevalence, affecting millions of individuals of reproductive age as highlighted by global health assessments, is further strengthening the need for hormonal support therapies. In parallel, the increasing adoption of ART procedures such as IVF and embryo transfer is significantly boosting demand for progesterone-based formulations, including capsules, gels, injections, and vaginal delivery systems across healthcare settings.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.2 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 9.3% |

The synthetic segment accounted for USD 1.4 billion in 2025 and is projected to grow at a CAGR of 9.5% through 2035. The strong performance of synthetic progesterone products is driven by their extensive use in oral contraceptives, hormone replacement therapy, infertility treatment protocols, and gynecological disorder management. These formulations are widely preferred due to their long-standing clinical usage, cost efficiency, high stability, and extended shelf life, making them suitable for large-scale healthcare deployment. Market growth is further supported by the broad availability of generic synthetic hormone therapies and their inclusion in combination treatment regimens, which enhances accessibility across both developed and emerging healthcare systems.

The oral segment held a share of 52.5% in 2025. Oral progesterone therapies are widely adopted due to their ease of use, strong physician preference, and broad application across hormone replacement therapy, infertility management, menstrual disorder treatment, and pregnancy support care. Their popularity is reinforced by improved patient adherence, simple administration, and the increasing availability of sustained-release formulations that enhance absorption and therapeutic performance. Growing use among menopausal patients receiving bioidentical hormone therapy has further strengthened demand for oral progesterone products globally.

North America Progesterone Industry held a 37.8% in 2025. The region's leadership is driven by high adoption rates of hormone replacement therapy, increasing fertility treatment procedures, and strong awareness of reproductive health management among patients and healthcare providers. The United States, in particular, benefits from a well-established fertility treatment ecosystem, where rising IVF and embryo transfer procedures continue to support strong demand for progesterone in luteal phase support. Continuous advancements in micronized oral progesterone formulations, increasing acceptance of bioidentical hormone therapies, and strong clinical awareness further reinforce market growth across the region.

Key companies operating in the Global Progesterone Market include AbbVie, Pfizer, Merck & Co., Bayer AG, Organon, Viatris (Mylan), Teva Pharmaceutical Industries, Sun Pharmaceutical Industries, Lupin Limited, Cipla, Ferring Pharmaceuticals, Gedeon Richter, Glenmark Pharmaceuticals, Alkem Laboratories, Zydus Lifesciences, Besins Healthcare, TherapeuticsMD, and Xiromed. Companies in the progesterone market are increasingly focusing on expanding their hormone therapy portfolios through the development of advanced and patient-friendly formulations that improve treatment adherence and therapeutic outcomes. A major strategy involves strengthening research and development efforts to enhance the bioavailability and stability of progesterone-based products, particularly in oral and micronized delivery systems. Firms are also investing in fertility-focused treatment innovations aligned with the rising demand for assisted reproductive technologies such as IVF and embryo transfer procedures. Strategic collaborations with fertility clinics and healthcare providers are being used to expand prescription reach and improve patient access. In addition, companies are leveraging generic product expansion strategies to strengthen market penetration across cost-sensitive regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Formulation trends

- 2.2.3 Route of administration trends

- 2.2.4 Drug type trends

- 2.2.5 Type trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of infertility and hormonal disorders

- 3.2.1.2 Growing adoption of hormone replacement therapy (HRT)

- 3.2.1.3 Expansion of women’s healthcare infrastructure and reproductive medicine

- 3.2.1.4 Advancements in drug delivery formulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Side effects and safety concerns associated with hormone therapy

- 3.2.2.2 Stringent regulatory and clinical approval requirements

- 3.2.2.3 Availability of alternative fertility and hormone therapies

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for bioidentical and personalized hormone therapies

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape (Driven by primary research)

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 MEA

- 3.4 Technology landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Future market trends (Driven by primary research)

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy, by formulation

- 3.9 Pipeline analysis and clinical trial landscape

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Investment & funding analysis

- 3.12 Fertility rates, by country (births per woman)

- 3.13 Gap analysis

- 3.14 Impact of AI & Generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Formulation, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Natural

- 5.3 Synthetic

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Injectable

- 6.3 Oral

- 6.4 Transdermal

- 6.5 Other routes of administration

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Menopause

- 7.3 Contraception

- 7.4 Dysfunctional uterine bleeding

- 7.5 Hyperplastic precursor lesions

- 7.6 Endometrial cancer

- 7.7 Other applications

Chapter 8 Market Estimates and Forecast, By Drug Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Branded

- 8.3 Generic

Chapter 9 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 9.1 Prescription

- 9.2 OTC

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Hospital pharmacy

- 10.3 Retail pharmacy

- 10.4 Online pharmacy

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AbbVie

- 12.2 Alkem Laboratories

- 12.3 Bayer AG

- 12.4 Besins Healthcare

- 12.5 Cipla

- 12.6 Ferring Pharmaceuticals

- 12.7 Glenmark Pharmaceuticals

- 12.8 Gedeon Richter

- 12.9 Lupin Limited

- 12.10 Merck & Co.

- 12.11 Organon

- 12.12 Pfizer

- 12.13 Sun Pharmaceutical Industries

- 12.14 Teva Pharmaceutical Industries

- 12.15 TherapeuticsMD

- 12.16 Viatris (Mylan)

- 12.17 Xiromed

- 12.18 Zydus Lifesciences