|

市場調查報告書

商品編碼

2061394

運動鞋市場機會、成長要素、產業趨勢分析及2026-2035年預測。Athletic Footwear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

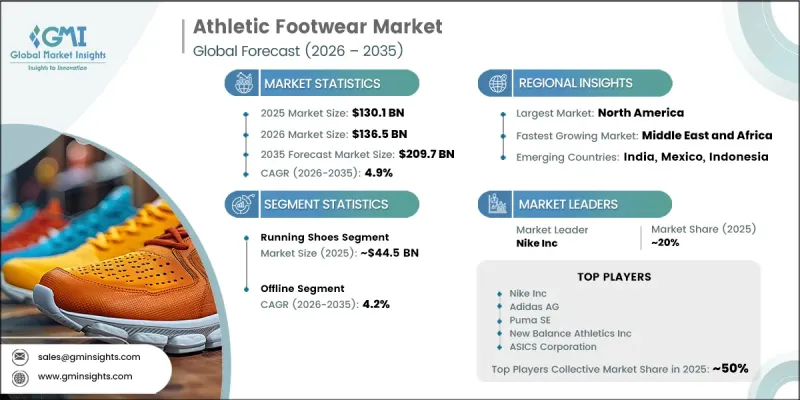

預計到 2025 年,全球運動鞋市場價值將達到 1,301 億美元,並以 4.9% 的複合年成長率成長,到 2035 年將達到 2,097 億美元。

市場成長主要得益於人們參與體育健身活動的增加,這持續擴大了高性能和休閒鞋履的全球消費群。跑步和慢跑是該品類需求的最大驅動力,光在美國就有數千萬活躍的參與者。在成熟經濟體中,即使在經濟波動期間,人們在身體健康方面的支出也保持穩定;而在新興經濟體中,隨著都市區擴大將運動作為一種休閒方式,市場呈現快速成長的態勢。同時,高性能材料和鞋類工程技術的不斷進步正在重塑消費者對跑步、訓練和戶外鞋履的期望。創新動能顯著增強,材料科學與設計的融合正在直接影響消費者的購買行為,尤其是在高性能跑鞋領域。中底技術的突破性進步,例如全球領導品牌率先採用的碳纖維板技術,已展現出可衡量的性能提升,促使消費者願意支付更高的價格。學術研究和運動表現研究也表明,先進的跑鞋設計能夠提高跑步效率,從而增強其在高階市場的價值提案。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1301億美元 |

| 預測金額 | 2097億美元 |

| 複合年成長率 | 4.9% |

預計到2025年,跑鞋市場規模將達到445億美元,並在2035年之前以5.1%的複合年成長率成長。跑鞋在競技運動和日常生活中扮演著重要角色,這使其成為整體市場中最具多功能性的類別之一,也正是推動市場擴張的主要因素。全球知名品牌的領先產品系列憑藉其可靠的性能和時尚的設計,持續保持高銷售量。

預計到2025年,線下零售市佔率將達到61.8%,並在2035年之前以4.2%的複合年成長率成長。實體零售仍然是主要的銷售管道,因為品牌持續增加對身臨其境型購物環境的投資,以增強客戶參與。這些零售模式強調產品個人化、體驗式互動和社群主導的交流,從而在傳統購買行為之外,加強品牌忠誠度和消費者聯繫。

美國運動鞋市場預計到2025年將達到378億美元,並在2026年至2035年間以3.8%的複合年成長率成長。由於美國人均運動鞋支出極高,美國仍是全球最大的運動鞋市場貢獻者。該市場深受知名國際品牌的影響,主要參與者透過創新、D2C(直接面對消費者)擴張和成熟的產品差異化策略來塑造競爭格局。美國在鞋類設計、創新和製造方面的高度集中的專業技術進一步鞏固了其在全球市場的主導地位。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 製造商

- 中斷

- 零售商

- 利潤率分析

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 健康意識的提高和運動參與度的提高

- 鞋類技術與設計創新

- 拓展電子商務和直接面對消費者(DTC)管道

- 產業潛在風險與挑戰

- 仿冒品的擴散

- 原物料價格波動

- 機會

- 促進因素

- 成長潛力分析

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 貿易數據分析

- 監理情勢

- 標準和合規要求

- 區域監理框架

- 認證標準

- 波特的分析

- PESTLE分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 消費行為分析

- 人口趨勢

- 影響購買決策的因素

- 消費者產品採納

- 首選分銷管道

- 理想價格範圍

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 跑鞋

- 生活風格/休閒運動

- 訓練與健身

- 運動鞋

- 戶外與步道

- 其他

第6章 市場估算與預測:依最終用戶分類,2022-2035年

- 男性

- 女士

- 孩子們

第7章 市場估計與預測:依價格分類,2022-2035年

- 低價位

- 中價位

- 優質的

第8章 市場估算與預測:依通路分類,2022-2035年

- 線上

- 企業網站

- 電子商務網站

- 離線

- 超級市場和大賣場

- 專賣店

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 瑞典

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- UAE

- 南非

第10章:公司簡介

- 世界公司

- Nike Inc

- Adidas AG

- Puma SE

- New Balance Athletics Inc

- Under Armour Inc

- Skechers USA Inc

- ASICS Corporation

- Decathlon SA

- Yonex Co Ltd

- 當地公司

- Mizuno Corporation

- On Holding AG

- Deckers Outdoor Corporation

- FILA Holdings Corporation

- VF Corporation

- Columbia Sportswear Company

- Li-Ning Company Limited

-

- ANTA Sports Products Limited

- Xtep International Holdings Limited

- Lululemon Athletica Inc

- Wolverine World Wide Inc

- Brooks Sports Inc

The Global Athletic Footwear Market was valued at USD 130.1 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 209.7 billion in 2035.

Market growth is being driven by rising participation in sports and fitness activities, which continues to expand the global consumer base for performance and lifestyle footwear. Running and jogging represent the largest contributors to category demand, supported by tens of millions of active participants in the United States alone. In mature economies, spending on physical wellness has remained stable even during economic fluctuations, while emerging economies are seeing rapid adoption as urban populations increasingly engage in recreational sports. At the same time, continuous advancements in performance materials and footwear engineering are reshaping consumer expectations across running, training, and outdoor categories. Innovation intensity has increased significantly, particularly in performance running footwear, where material science and design integration are directly influencing purchasing behavior. Breakthroughs in midsole engineering, including carbon-fiber plate integration pioneered by major global brands, have demonstrated measurable performance gains, reinforcing consumer willingness to pay premium prices. Academic and sports performance research has also linked advanced running footwear designs to improved running efficiency, strengthening their value proposition in the premium segment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $130.1 Billion |

| Forecast Value | $209.7 Billion |

| CAGR | 4.9% |

The running footwear segment generated USD 44.5 billion in 2025 and is projected to grow at a CAGR of 5.1% through 2035. This segment's expansion is supported by its dual role in both competitive athletics and everyday lifestyle usage, making it one of the most versatile categories in the broader market. Leading product lines from global brands consistently maintain high sales volumes due to their blend of performance credibility and fashion-oriented appeal.

The offline distribution segment accounted for 61.8% share in 2025 and is expected to grow at a CAGR of 4.2% through 2035. Physical retail remains a dominant channel as brands continue to invest heavily in immersive shopping environments that enhance customer engagement. These retail formats emphasize product personalization, experiential engagement, and community-driven interactions that strengthen brand loyalty and consumer connection beyond traditional purchasing.

U.S. Athletic Footwear Market reached USD 37.8 billion in 2025 and is expected to grow at a CAGR of 3.8% from 2026 to 2035. The country remains the largest contributor due to exceptionally high per-capita spending on athletic footwear. The market is strongly influenced by established global brands, with major companies shaping competitive dynamics through innovation, direct-to-consumer expansion, and advanced product differentiation strategies. A strong concentration of footwear design, innovation, and manufacturing expertise further reinforces the country's leadership position within the global landscape.

Major companies operating in the Global Athletic Footwear Industry include Nike Inc, Adidas AG, Puma SE, New Balance Athletics Inc, ASICS Corporation, Under Armour Inc, Skechers USA Inc, Decathlon S.A, Yonex Co Ltd, Mizuno Corporation, On Holding AG, VF Corporation, Deckers Outdoor Corporation, FILA Holdings Corporation, Columbia Sportswear Company, Li-Ning Company Limited, ANTA Sports Products Limited, Xtep International Holdings Limited, Lululemon Athletica Inc, Wolverine World Wide Inc, and Brooks Sports Inc. Companies in the athletic footwear market are increasingly focusing on performance-driven innovation, integrating advanced materials, lightweight construction, and energy-return technologies to enhance product differentiation. They are expanding direct-to-consumer ecosystems to improve margin control, strengthen customer engagement, and collect real-time consumer insights. Brand diversification strategies are also being deployed, with firms extending their offerings across performance, lifestyle, and hybrid segments to capture wider demographics. Strategic collaborations with athletes, designers, and sports organizations are reinforcing brand visibility and credibility. At the same time, companies are investing heavily in sustainability initiatives, including recycled materials and circular product design, to align with evolving consumer expectations and regulatory pressures.

Table of Contents

Chapter 1 Research methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Business trends

- 2.3 Regional

- 2.4 Product type

- 2.5 End user

- 2.6 Price

- 2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Manufacturers

- 3.1.3 Distributors

- 3.1.4 Retailers

- 3.1.5 Profit margin analysis

- 3.1.6 Value addition at each stage

- 3.1.7 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising health consciousness & growing sports participation

- 3.2.1.2 Innovation in footwear technology & design

- 3.2.1.3 Expansion of e-commerce & Direct-to-Consumer (DTC) channels

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Proliferation of counterfeit products

- 3.2.2.2 Volatile raw material prices

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Price trends

- 3.5.1 By region

- 3.5.2 By product type

- 3.6 Trade data analysis

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Consumer behavior analysis

- 3.11.1 Demographic trends

- 3.11.2 Factors affecting buying decision

- 3.11.3 Consumer product adoption

- 3.11.4 Preferred distribution channel

- 3.11.5 Preferred price range

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Running Shoes

- 5.3 Lifestyle/Casual Athletic

- 5.4 Training & Fitness

- 5.5 Sports Shoes

- 5.6 Outdoor & Trail

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Men

- 6.3 Women

- 6.4 Kids

Chapter 7 Market Estimates & Forecast, By Price, 2022 - 2035, (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Economy

- 7.3 Mid-range

- 7.4 Premium

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 Company Websites

- 8.2.2 E-commerce Websites

- 8.3 Offline

- 8.3.1 Supermarkets and Hypermarkets

- 8.3.2 Specialty Stores

- 8.3.3 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Sweden

- 9.3.7 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Nike Inc

- 10.1.2 Adidas AG

- 10.1.3 Puma SE

- 10.1.4 New Balance Athletics Inc

- 10.1.5 Under Armour Inc

- 10.1.6 Skechers USA Inc

- 10.1.7 ASICS Corporation

- 10.1.8 Decathlon S.A

- 10.1.9 Yonex Co Ltd

- 10.2 Regional Players

- 10.2.1 Mizuno Corporation

- 10.2.2 On Holding AG

- 10.2.3 Deckers Outdoor Corporation

- 10.2.4 FILA Holdings Corporation

- 10.2.5 VF Corporation

- 10.2.6 Columbia Sportswear Company

- 10.2.7 Li-Ning Company Limited

- 10.3 Emerging Players & Innovators

- 10.3.1 ANTA Sports Products Limited

- 10.3.2 Xtep International Holdings Limited

- 10.3.3 Lululemon Athletica Inc

- 10.3.4 Wolverine World Wide Inc

- 10.3.5 Brooks Sports Inc

運動鞋市場-2026-2032年全球市場預測

運動鞋市場-2026-2032年全球市場預測 2026-2030年全球健行和越野鞋類市場

2026-2030年全球健行和越野鞋類市場 運動鞋市場規模、佔有率、趨勢和預測:按產品類型、分銷管道、最終用戶和地區分類,2026-2034 年

運動鞋市場規模、佔有率、趨勢和預測:按產品類型、分銷管道、最終用戶和地區分類,2026-2034 年 運動鞋市場:按類別、消費者群體、零售分銷管道和地區分類。

運動鞋市場:按類別、消費者群體、零售分銷管道和地區分類。 運動鞋市場規模、市場佔有率、成長率、全球產業分析,按類型、應用和地區的考察,未來預測(2026-2034年)

運動鞋市場規模、市場佔有率、成長率、全球產業分析,按類型、應用和地區的考察,未來預測(2026-2034年) 全球運動鞋市場報告:實際結果與預測,2021-2032年

全球運動鞋市場報告:實際結果與預測,2021-2032年 運動鞋市場分析及預測(至2035年):依類型、產品類型、材料類型、應用、技術、最終用戶、安裝類型及功能分類全球運動鞋市場規模、佔有率、趨勢和成長分析報告(2026-2034年)輕量緩震低筒跑步襪市場:2026-2032年全球預測(依材質、價格範圍、性能特性、色彩、通路和最終用戶分類)

運動鞋市場分析及預測(至2035年):依類型、產品類型、材料類型、應用、技術、最終用戶、安裝類型及功能分類全球運動鞋市場規模、佔有率、趨勢和成長分析報告(2026-2034年)輕量緩震低筒跑步襪市場:2026-2032年全球預測(依材質、價格範圍、性能特性、色彩、通路和最終用戶分類) 健行鞋市場規模、佔有率及成長分析(按產品類型、材料、通路、性別及地區分類)-2026-2033年產業預測

健行鞋市場規模、佔有率及成長分析(按產品類型、材料、通路、性別及地區分類)-2026-2033年產業預測