|

市場調查報告書

商品編碼

2061391

氫氣儲存槽及運輸市場機會、成長要素、產業趨勢分析及2026-2035年預測Hydrogen Storage Tanks and Transportation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

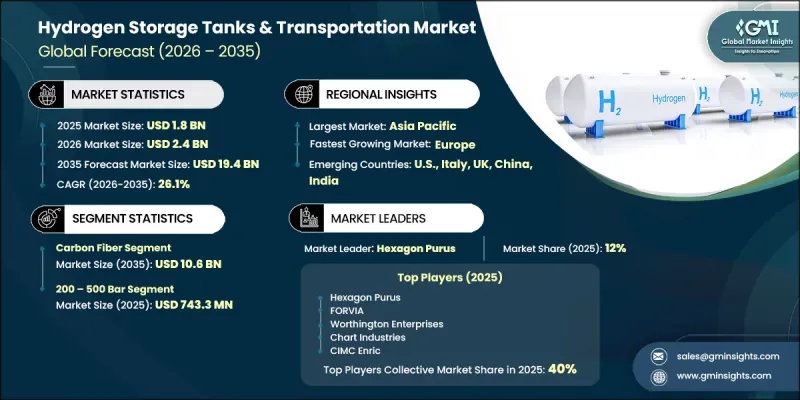

2025 年全球氫氣儲存槽和運輸市場價值 18 億美元,預計到 2035 年將達到 194 億美元,年複合成長率為 26.1%。

隨著全球脫碳進程的加速推進以及氫能作為清潔能源載體的日益受到關注,氫能產業正蓬勃發展。許多地區政府正積極推動氫能基礎設施建設,包括儲能和運輸系統,以支持燃料電池的普及和大規模清潔能源轉型舉措。動力來源交通解決方案的日益普及進一步推動了對安全、高效、大容量儲能系統的需求。同時,複合材料、高壓工程和低溫技術的進步正在提升儲能效率、安全性和成本效益。對氫能走廊、管道和加氫基礎設施投資的增加,正在加強全球供應鏈的互聯互通。此外,氫能在能源密集產業的工業應用日益廣泛,以及對支援分散式能源網路和遠端應用的模組化、可擴展運輸系統的需求不斷成長,也對市場產生了積極影響。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 18億美元 |

| 預計金額 | 194億美元 |

| 複合年成長率 | 26.1% |

氫氣儲存槽和運輸系統是指根據應用需求,以壓縮、液態或固體形式安全儲存和運輸氫氣的技術解決方案。這些系統採用特殊材料和結構設計,以確保在儲存和運輸過程中的效率和安全性,同時應對氫氣極高的易燃性。它們在推動氫氣在交通運輸、工業和能源領域的應用方面發揮著至關重要的作用,構成了全球新興氫能經濟的基礎。

預計到2035年,碳纖維儲存槽和運輸領域的市場規模將達到106億美元。該領域備受關注的原因在於,與傳統的金屬材料相比,碳纖維具有更高的強度重量比、更強的耐腐蝕性和更優異的耐極端壓力性能。其輕質特性也有助於提高運輸效率,並實現更安全的高壓氫氣處理。碳纖維系統在氫氣物流領域的日益普及,正在為整個供應鏈創造強勁的成長機遇,並推動氫氣供應網路的更廣泛應用。

預計到2025年,200-500巴氫氣儲存槽和運輸領域的市場規模將達到7.433億美元,到2035年將以26.2%的複合年成長率成長。該領域的成長主要得益於氫能交通應用的擴展、分散式供應系統的增加以及加氫基礎設施建設的進步。從傳統的鋼製系統向先進複合材料壓力容器(包括III型和IV型結構)的轉變正在加速這一領域的應用。高壓模組化運輸系統在燃料電池公車、卡車、鐵路系統以及管道輸送受限的工業應用中也越來越受歡迎,進一步推動了市場擴張。

預計到2035年,美國氫氣儲存槽和運輸市場規模將達22億美元。推動美國市場成長的主要動力來自聯邦政府大力推行清潔能源和工業脫碳的措施。對氫能交通基礎設施的投資增加以及燃料電池的普及,正在推動對先進儲氫系統的需求。複合複合材料高壓儲槽在運輸、氣體處理和加氫網路中的廣泛應用,進一步促進了市場成長。氫氣儲存和運輸技術正成為全部區域氫能樞紐建設和大規模工業脫碳工作的核心。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 氫氣儲存槽成本結構分析

- 貿易數據分析

- 進出口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對產業的影響

- 人工智慧驅動的產品最佳化

- 預測性維護和故障檢測

- 風險、限制和監管考量

- 投資分析及未來展望

- 數位化和物聯網整合

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 按公司規模進行基準測試

- 排名分類標準與遴選標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場規模及預測:依材料分類,2022-2035年

- 金屬

- 玻璃纖維

- 碳纖維

第6章 市場規模及預測:依儲槽分類,2022-2035年

- 1型

- 類型 2

- 3型

- 4型

第7章 市場規模與預測:依壓力類型分類,2022-2035年

- 小於 200 巴

- 200~500 bar

- 500巴或以上

第8章 市場規模及預測:依應用領域分類,2022-2035年

- 車輛

- 鐵路

- 海上

- 產業

- 其他

第9章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 荷蘭

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 世界其他地區

第10章:公司簡介

- Aciturri HyStorage

- BayoTech

- CATEC Gases

- CIMC Enric

- Chart Industries

- Chesterfield Special Cylinders

- FORVIA

- Faber Industrie

- Hexagon Purus

- Iljin Hysolus

- INOXCVA

- Kawasaki Heavy Industries

- Luxfer Gas Cylinders

- NPROXX

- OPmobility SE

- Quantum Fuel Systems

- Steelhead Composites

- Tenaris

- Umoe Advanced Composites

- Vitkovice Cylinders

- Voith HySTech

- Weldship Corporation

- Worthington Enterprises

The Global Hydrogen Storage Tanks and Transportation Market was valued at USD 1.8 billion in 2025 and is estimated to grow at a CAGR of 26.1% to reach USD 19.4 billion by 2035.

The industry is gaining strong momentum due to accelerating global decarbonization efforts and the rising focus on hydrogen as a clean energy carrier. Governments across multiple regions are actively promoting hydrogen infrastructure development, including storage and transportation systems, to support fuel cell adoption and large-scale clean energy transition initiatives. Growing deployment of hydrogen-powered mobility solutions is further increasing the need for safe, efficient, and high-capacity storage systems. At the same time, advancements in composite materials, high-pressure engineering, and cryogenic technologies are improving storage efficiency, safety, and cost-effectiveness. Expanding investments in hydrogen corridors, pipelines, and refueling infrastructure are strengthening global supply chain connectivity. The market is also benefiting from increasing industrial use of hydrogen in energy-intensive sectors, alongside rising demand for modular and scalable transport systems that support distributed energy networks and remote applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.8 Billion |

| Forecast Value | $19.4 Billion |

| CAGR | 26.1% |

Hydrogen storage tanks and transportation systems refer to engineered solutions designed to safely store and transport hydrogen in compressed, liquefied, or solid-state forms depending on application requirements. These systems are built with specialized materials and structural designs to manage hydrogen's highly flammable nature while ensuring efficiency and safety during storage and movement. They play a crucial role in enabling hydrogen distribution for mobility, industrial usage, and energy applications, forming a backbone for emerging hydrogen economies worldwide.

The carbon fiber hydrogen storage tanks and transportation segment is expected to reach USD 10.6 billion by 2035. This segment is favored due to carbon fiber's high strength-to-weight ratio, strong corrosion resistance, and superior ability to withstand extreme pressure conditions compared to conventional metal alternatives. Its lightweight properties also improve transport efficiency and enable safer handling of high-pressure hydrogen. Increasing utilization of carbon fiber-based systems in hydrogen logistics is creating strong growth opportunities across the supply chain and supporting broader adoption in hydrogen distribution networks.

The 200-500 bar hydrogen storage tanks and transportation segment was valued at USD 743.3 million in 2025 and is projected to grow at 26.2% by 2035. Growth in this segment is driven by expanding hydrogen mobility applications, increasing decentralized distribution systems, and rising development of refueling infrastructure. The transition from traditional steel-based systems to advanced composite pressure vessels, including type III and type IV configurations, is accelerating adoption. High-pressure modular transport systems are also gaining traction across fuel-cell buses, trucks, rail systems, and industrial applications where pipeline access is limited, further supporting market expansion.

U.S. Hydrogen Storage Tanks and Transportation Market is anticipated to reach USD 2.2 billion by 2035. Market growth in the country is supported by strong federal initiatives promoting clean energy deployment and decarbonization across industrial sectors. Increasing investment in hydrogen mobility infrastructure and fuel cell adoption is driving demand for advanced storage systems. Rising use of composite high-pressure tanks across transportation, gas handling, and refueling networks is further strengthening market expansion. Hydrogen storage and transportation technologies are becoming central to the development of hydrogen hubs and large-scale industrial decarbonization efforts across the region.

Prominent players operating in the Global Hydrogen Storage Tanks And Transportation Industry include Hexagon Purus, Chart Industries, CIMC Enric, NPROXX, Luxfer Gas Cylinders, Worthington, Tenaris, Kawasaki Heavy Industries, Iljin Hysolus, INOXCVA, Faber Industrie, Steelhead Composites, Quantum Fuel Systems, Umoe Advanced Composites, Voith HySTech, BayoTech, OPmobility, FORVIA, Chesterfield Special Cylinders, Aciturri HyStorage, Weldship, and CATEC Gases. Companies in the hydrogen storage tanks and transportation market are focusing on advanced material innovation and structural engineering improvements to enhance safety and storage efficiency. A major strategy involves increasing investment in carbon fiber composite technologies to reduce weight while improving pressure resistance. Firms are also expanding production capacities to meet rising global hydrogen infrastructure demand. Strategic partnerships with energy companies, automotive manufacturers, and government programs are helping accelerate deployment across mobility and industrial applications. Many players are also investing in cryogenic and high-pressure storage innovations to improve performance across varied use cases. Expansion into hydrogen corridor and refueling infrastructure projects is further strengthening supply chain integration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates and forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Material trends

- 2.4 Tank type trends

- 2.5 Pressure trends

- 2.6 Application trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

- 3.7 Cost structure analysis of hydrogen storage tank

- 3.8 Trade data analysis (Driven by Primary Research)

- 3.8.1 Import/export value trends (Driven by Primary Research)

- 3.8.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.9 Impact of AI & Gen AI on the industry

- 3.9.1 AI driven product optimization

- 3.9.2 Predictive maintenance & fault detection

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Investment analysis & future outlook

- 3.11 Digitalization & IoT integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Material, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Metals

- 5.3 Glass fibers

- 5.4 Carbon fibers

Chapter 6 Market Size and Forecast, By Tank, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Type 1

- 6.3 Type 2

- 6.4 Type 3

- 6.5 Type 4

Chapter 7 Market Size and Forecast, By Pressure, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Below 200 bar

- 7.3 200 - 500 bar

- 7.4 Above 500 bar

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Vehicles

- 8.3 Railways

- 8.4 Marine

- 8.5 Industrial

- 8.6 Others

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Netherlands

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.5 Rest of World

Chapter 10 Company Profiles

- 10.1 Aciturri HyStorage

- 10.2 BayoTech

- 10.3 CATEC Gases

- 10.4 CIMC Enric

- 10.5 Chart Industries

- 10.6 Chesterfield Special Cylinders

- 10.7 FORVIA

- 10.8 Faber Industrie

- 10.9 Hexagon Purus

- 10.10 Iljin Hysolus

- 10.11 INOXCVA

- 10.12 Kawasaki Heavy Industries

- 10.13 Luxfer Gas Cylinders

- 10.14 NPROXX

- 10.15 OPmobility SE

- 10.16 Quantum Fuel Systems

- 10.17 Steelhead Composites

- 10.18 Tenaris

- 10.19 Umoe Advanced Composites

- 10.20 Vitkovice Cylinders

- 10.21 Voith HySTech

- 10.22 Weldship Corporation

- 10.23 Worthington Enterprises