|

市場調查報告書

商品編碼

2061388

2026 年至 2035 年尿液檢查的市場機會、成長要素、產業趨勢分析與預測。Urinalysis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

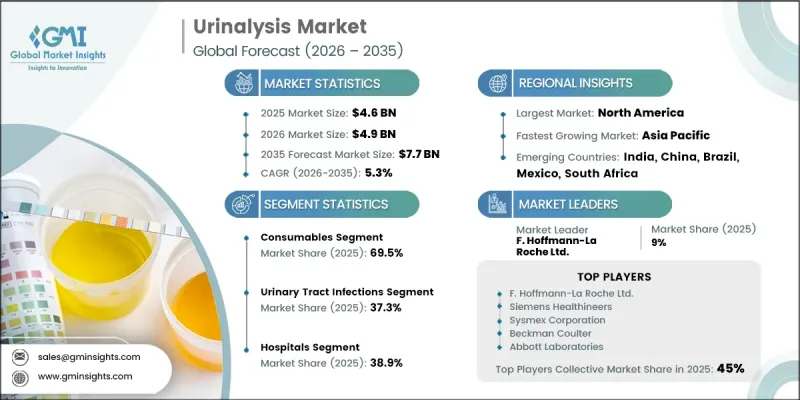

全球尿液檢查市場預計到 2025 年將價值 46 億美元,預計到 2035 年將以 5.3% 的複合年成長率成長至 77 億美元。

發展中地區尿道感染負擔日益加重、全球慢性腎臟病盛行率不斷上升、人口快速老化是推動市場擴張的主要因素。這些因素共同促使人們對定期診斷篩檢和疾病早期發現的需求不斷成長。尿液檢查透過評估尿液的物理、化學和顯微鏡特性,仍然是識別和監測尿道感染、腎臟疾病、糖尿病和各種代謝紊亂的基本診斷方法。開發中國家條件差、清潔飲用水匱乏以及醫療基礎設施不足等風險因素的增加,進一步推高了感染率。同時,糖尿病等慢性疾病盛行率的上升增加了感染疾病的易感性,導致患者群體不斷擴大。隨著醫療系統日益重視早期診斷和預防醫學,尿液檢查正成為核心診斷工具。此外,全球慢性腎臟病負擔的加重也進一步推動了對基於尿液檢查的診斷解決方案的長期需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 46億美元 |

| 預測市場規模 | 77億美元 |

| 複合年成長率 | 5.3% |

到2025年,耗材市佔率將達到69.5%。此細分市場包括試紙、試劑、浸漬條以及其他用於常規尿液檢查的一次性檢測材料。由於醫院、臨床檢查室和照護現場機構的診斷檢測具有重複性,因此需求持續強勁。疾病監測需求和廣泛的篩檢檢測實踐推動了持續的使用週期,確保了穩定的重複消耗。尿道感染、腎臟疾病和慢性疾病發生率的上升進一步加劇了對這些耗材的持續需求。

到2025年,尿道感染(UTI)領域將佔據37.3%的市場。由於泌尿道感染疾病在不同族群中普遍存在,因此尿液檢查是該領域最重要的應用之一。尿液檢查是檢測細菌活性和相關感染標記的主要診斷方法,能夠快速可靠地識別尿道感染。感染率的上升,尤其是在女性、老年人和患有潛在疾病的患者中,持續推動全球尿路檢測量的成長。

到2025年,北美尿液檢查市場佔有率將達到35.7%。該地區持續保持強勁成長勢頭,這得益於先進的醫療基礎設施、較高的診斷意識以及完善的疾病篩檢流程。慢性腎臟病和其他長期健康問題的日益普遍是推動診斷檢測需求成長的主要因素。需要持續監測的患者群體不斷擴大,進一步提升了尿液檢查在常規醫療流程中的重要性。自動化、高通量診斷系統的普及提高了檢測的效率和準確性,有助於改善臨床決策,並推動了全部區域的市場成長。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 發展中地區尿道感染發生率增加

- 全球慢性腎臟病盛行率正在上升。

- 老年人口增加

- 高懷孕率

- 產業潛在風險與挑戰

- 對定期體檢重要性的認知不足

- 設備研發成本高昂

- 市場機遇

- 開發多參數、富含生物標記的診斷方法

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術展望

- 最新科技趨勢

- 新興技術

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 價格趨勢分析

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 消耗品

- 油尺

- 試劑

- 一次性產品

- 妊娠及不孕症檢測套組

- 裝置

- 尿液生化分析儀

- 自動尿沉渣分析儀

第6章 市場估計與預測:依測試類型分類,2022-2035年

- 尿液檢查

- 尿沉渣檢查

- 妊娠和不孕症檢查

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 尿道感染

- 腎臟疾病

- 懷孕

- 糖尿病

- 其他用途

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 臨床實驗室

- 醫院

- 家庭醫療保健

- 其他最終用戶

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- Abbott Laboratories

- ACON Laboratories

- ARKRAY Inc.

- Beckman Coulter

- Bio-Rad Laboratories

- Becton, Dickinson and Company(BD)

- Cardinal Health

- DIRUI Industrial

- QuidelOrtho Corporation

- Roche Diagnostics

- Siemens Healthineers

- Sysmex Corporation

- Thermo Fisher Scientific

- URIT Medical

- 77 Elektronika

The Global Urinalysis Market was valued at USD 4.6 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 7.7 billion by 2035.

Market expansion is supported by a rising burden of urinary tract infections across developing regions, increasing global prevalence of chronic kidney disease, and a rapidly growing elderly population. These factors are collectively strengthening the demand for routine diagnostic screening and early disease detection. Urinalysis, which evaluates the physical, chemical, and microscopic properties of urine, remains a fundamental diagnostic approach for identifying and monitoring urinary tract infections, kidney disorders, diabetes, and various metabolic abnormalities. Growing exposure to risk factors such as poor sanitation, limited access to clean drinking water, and inadequate healthcare infrastructure in developing economies is further increasing infection rates. At the same time, rising incidence of chronic diseases such as diabetes is contributing to higher susceptibility to infections, thereby expanding the patient pool. Healthcare systems are increasingly prioritizing early diagnosis and preventive care, positioning urinalysis as a core diagnostic tool. In addition, the rising global burden of chronic kidney disease is further reinforcing long-term demand for urinalysis-based testing solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.6 Billion |

| Forecast Value | $7.7 Billion |

| CAGR | 5.3% |

The consumables segment accounted for 69.5% share in 2025. This segment includes test strips, reagents, dipsticks, and other disposable testing materials used in routine urine analysis procedures. Demand remains consistently high due to the repetitive nature of diagnostic testing in hospitals, clinical laboratories, and point-of-care environments. Continuous usage cycles, driven by disease monitoring requirements and widespread screening practices, ensure stable and recurring consumption. The growing incidence of urinary tract infections, kidney-related disorders, and chronic illnesses further strengthens sustained demand for these consumable products.

The urinary tract infections segment held a share of 37.3% in 2025. This application area represents one of the most significant uses of urinalysis due to the widespread prevalence of infections across diverse population groups. Urinalysis serves as a primary diagnostic method for detecting bacterial activity and related infection markers, enabling fast and reliable identification of urinary tract infections. Rising infection rates, particularly among women, elderly individuals, and patients with underlying health conditions, continue to drive high testing volumes globally.

North America Urinalysis Market accounted for 35.7% share in 2025. The region continues to exhibit strong growth, supported by advanced healthcare infrastructure, high diagnostic awareness, and well-established disease screening practices. The growing prevalence of chronic kidney disease and other long-term health conditions is significantly contributing to increased diagnostic testing demand. A large patient base requiring continuous monitoring further reinforces the importance of urinalysis in routine healthcare workflows. The widespread availability of automated and high-throughput diagnostic systems enhances testing efficiency and accuracy, supporting improved clinical decision-making and strengthening market growth across the region.

Key players operating in the Global Urinalysis Industry include Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, Thermo Fisher Scientific, Beckman Coulter, Bio-Rad Laboratories, Becton, Dickinson and Company (BD), Sysmex Corporation, QuidelOrtho Corporation, ARKRAY Inc., ACON Laboratories, Cardinal Health, DIRUI Industrial, URIT Medical, and 77 Elektronika. Companies in the urinalysis market are focusing on the development of automated and high-throughput diagnostic systems to improve testing speed, accuracy, and workflow efficiency in clinical settings. They are investing in advanced reagent technologies and digital integration to enhance result interpretation and laboratory connectivity. Expansion of point-of-care testing solutions is another key strategy, enabling faster diagnostics outside traditional laboratory environments. Strategic partnerships with healthcare providers and diagnostic laboratories are strengthening product adoption and distribution reach. Manufacturers are also emphasizing cost-effective consumable innovations to support high-volume testing requirements. In addition, continuous research and development efforts are being directed toward improving sensitivity, reducing turnaround time, and expanding test menus to cover a wider range of diseases and metabolic conditions, thereby reinforcing competitive positioning in the global market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy and data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy and data integrity commitment

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Test type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.2.5 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of urinary tract infection in developing regions

- 3.2.1.2 Increasing prevalence of chronic kidney disease worldwide

- 3.2.1.3 Increasing geriatric population

- 3.2.1.4 High pregnancy rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Low awareness about routine check-ups

- 3.2.2.2 High R&D cost of developing instruments

- 3.2.3 Market opportunities

- 3.2.3.1 Development of multiparametric & biomarker-rich tests

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by primary research)

- 3.7 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.8 Pricing trend analysis (Driven by primary research)

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.2.1 Dipsticks

- 5.2.2 Reagents

- 5.2.3 Disposables

- 5.2.4 Pregnancy & fertility kits

- 5.3 Instruments

- 5.3.1 Biochemical urine analyzer

- 5.3.2 Automated urine sediment analyzer

Chapter 6 Market Estimates and Forecast, By Test Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Biochemical urinalysis

- 6.3 Sediment urinalysis

- 6.4 Pregnancy & fertility testing

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Urinary tract infections

- 7.3 Kidney disease

- 7.4 Pregnancy

- 7.5 Diabetes

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Clinical laboratories

- 8.3 Hospitals

- 8.4 Home healthcare

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 ACON Laboratories

- 10.3 ARKRAY Inc.

- 10.4 Beckman Coulter

- 10.5 Bio-Rad Laboratories

- 10.6 Becton, Dickinson and Company (BD)

- 10.7 Cardinal Health

- 10.8 DIRUI Industrial

- 10.9 QuidelOrtho Corporation

- 10.10 Roche Diagnostics

- 10.11 Siemens Healthineers

- 10.12 Sysmex Corporation

- 10.13 Thermo Fisher Scientific

- 10.14 URIT Medical

- 10.15 77 Elektronika

尿液檢查市場:依產品、應用和最終用途分類-2026-2032年全球市場預測

尿液檢查市場:依產品、應用和最終用途分類-2026-2032年全球市場預測 尿液檢查市場:依產品類型、檢測類型、應用和地區分類

尿液檢查市場:依產品類型、檢測類型、應用和地區分類 全球尿液檢查市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球尿液檢查市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 尿液尿液檢查市場規模、佔有率和成長分析:按檢測類型、應用、最終用戶、分銷管道、地區和行業預測,2026-2033年

尿液尿液檢查市場規模、佔有率和成長分析:按檢測類型、應用、最終用戶、分銷管道、地區和行業預測,2026-2033年 獸用尿液檢查產品市場規模、佔有率和成長分析:按產品類型、動物種類、應用、最終用戶、銷售管道和地區分類 - 2026-2033 年行業預測

獸用尿液檢查產品市場規模、佔有率和成長分析:按產品類型、動物種類、應用、最終用戶、銷售管道和地區分類 - 2026-2033 年行業預測 尿液檢查市場規模、佔有率和成長分析(按檢測方法、應用、最終用戶和地區分類)—產業預測(2026-2033 年)

尿液檢查市場規模、佔有率和成長分析(按檢測方法、應用、最終用戶和地區分類)—產業預測(2026-2033 年) 尿液檢查市場規模、佔有率和成長分析(按產品類型、檢測類型、應用、最終用戶和地區分類)-2026-2033年產業預測

尿液檢查市場規模、佔有率和成長分析(按產品類型、檢測類型、應用、最終用戶和地區分類)-2026-2033年產業預測 尿液分析儀:全球市佔率及排名、總收入及需求預測(2025-2031年)

尿液分析儀:全球市佔率及排名、總收入及需求預測(2025-2031年) 2025年全球尿沉渣檢測市場報告2025年全球尿液檢查市場報告

2025年全球尿沉渣檢測市場報告2025年全球尿液檢查市場報告