|

市場調查報告書

商品編碼

2061375

抗憂鬱症市場商機、成長要素、產業趨勢分析及2026-2035年預測。Antidepressant Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

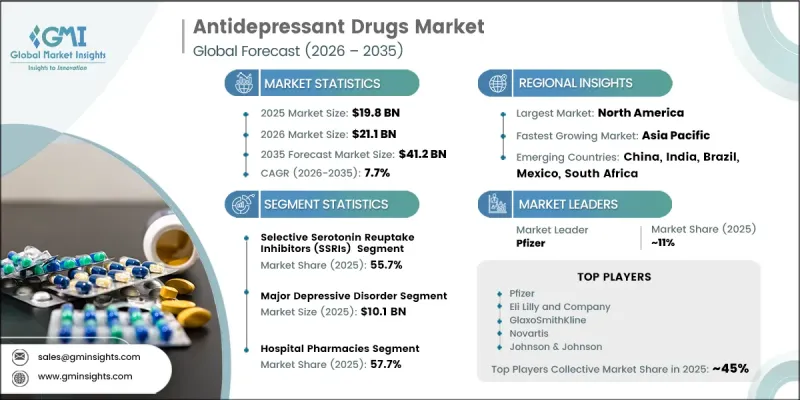

預計到 2025 年,全球抗憂鬱症市場價值將達到 198 億美元,並有望以 7.7% 的複合年成長率成長,到 2035 年達到 412 億美元。

由於全球憂鬱症、焦慮症及其他精神疾病盛行率的上升,市場正經歷顯著成長。人們對精神健康治療的認知不斷提高,以及對藥物治療的接受度日益增強,是推動產業擴張的主要因素。此外,藥物研發的持續進步,促使更有效的抗憂鬱症療法問世,旨在改善患者的長期治療效果。對難治性精神疾病治療的日益關注,也推動了具有更佳臨床療效的創新治療方法的研發。此外,價格低廉的非專利抗憂鬱症的廣泛普及,也改善了新興開發中國家獲得治療的機會。遠端醫療服務和數位醫療平台的擴展,進一步改善了服務不足人口獲得精神科護理的機會。抗憂鬱症被廣泛用於治療多種精神疾病,並在全球醫療保健系統中繼續發揮維護精神健康和長期管理精神疾病的重要作用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 198億美元 |

| 預測金額 | 412億美元 |

| 複合年成長率 | 7.7% |

抗憂鬱症市場持續受益於全球醫療保健投資的增加和精神健康支持基礎設施的不斷完善。旨在消除精神疾病污名化的宣傳宣傳活動和公共衛生舉措的不斷擴大,促使更多人尋求專業治療和藥物療法。日益加劇的精神壓力、生活方式相關的精神疾病以及慢性精神健康問題負擔的加重,進一步強化了對抗抗憂鬱症藥物的需求。製藥公司正日益致力於研發安全性更高、耐受性更好、起效更快的先進製劑,這將支撐市場在預測期內的持續成長。

預計到2025年,選擇性血清素再回收抑制劑(SSRI)將佔據55.7%的市場。 SSRI的強勢市場地位主要得益於其已證實的療效、良好的安全性以及相比傳統抗憂鬱症藥物更高的患者耐受性。由於副作用風險較低且適用於多種患者群體,這些治療方法被廣泛用作憂鬱症和焦慮症的第一線治療方案。醫生對更安全、更有效治療方法的日益青睞也進一步推動了該細分市場在全球範圍內的成長。

預計到2035年,口服藥物市場規模將達328億美元。此市場成長的主要驅動力是患者對口服製劑的強烈偏好,因為口服製劑具有方便、價格實惠、易於服用且非侵入性等優點。品牌和非專利口服抗憂鬱症的廣泛普及也提高了不同醫療機構和患者群體獲得藥物的機會。此外,口服抗憂鬱症在治療精神疾病方面已確立的長期療效和良好的安全性記錄,也持續維持其較高的使用率。

預計到2025年,北美抗憂鬱症市佔率將達到39.9%。該地區持續推動市場成長,主要得益於其精神疾病高發、醫療保健支出強勁以及先進精神治療方案的廣泛應用。完善的醫療保健基礎設施、優惠的報銷政策以及人們對精神健康管理意識的不斷提高,都顯著促進了北美市場的擴張。診斷率的上升和專業精神科服務的普及,將在整個預測期進一步鞏固該地區的市場地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 憂鬱症和焦慮症盛行率增加

- 加大研發投入

- 人們對治療方法和心理健康的認知不斷提高

- 個人化醫療的進展

- 產業潛在風險與挑戰

- 某些抗憂鬱症的副作用

- 顧客往往更傾向於非藥物療法而非藥物療法。

- 市場機遇

- 遠距精神科護理和數位健康平台的廣泛應用。

- 人們越來越關注兒童和青少年的心理健康。

- 促進因素

- 成長潛力分析

- 監理情勢

- 管道分析

- 未來市場趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 消費行為分析

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依藥物類別分類,2022-2035年

- 選擇性血清素再回收抑制劑(SSRIs)

- 血清素-正腎上腺素再回收抑制劑(SNRIs)

- 三環抗憂鬱藥物(TCAs)

- 非典型抗憂鬱症

- 去甲腎上腺素-多巴胺再回收抑制劑(NDRIs)

- 單胺氧化酵素抑制劑(MAOIs)

- 其他藥物類別

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 重度憂鬱症

- 整體焦慮症

- 強迫症

- 恐慌症

- 其他用途

第7章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 注射藥物

- 鼻腔

- 經皮

第8章 市場估算與預測:依藥物類型分類,2022-2035年

- 品牌

- 非專利的

第9章 市場估價與預測:依通路分類,2022-2035年

- 醫院藥房

- 零售藥房

- 網路藥房

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第11章:公司簡介

- Bristol-Myers Squibb

- Eli Lilly and Company

- GlaxoSmithKline

- H. Lundbeck

- Johnson &Johnson

- NV Organon

- Novartis

- Opko Health

- Otsuka Pharmaceutical

- Patheon

- Pfizer

- Sandoz

- Sun Pharmaceuticals

- Taj Pharma

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- Zhejiang NHU Company

The Global Antidepressant Drugs Market was valued at USD 19.8 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 41.2 billion by 2035.

The market is witnessing substantial growth due to the increasing incidence of depression, anxiety-related disorders, and other psychiatric conditions worldwide. Rising awareness regarding mental health treatment and growing acceptance of pharmacological therapies are significantly supporting industry expansion. Continuous advancements in pharmaceutical research are also contributing to the introduction of more effective antidepressant therapies designed to improve long-term patient outcomes. The growing focus on managing treatment-resistant mental health conditions is encouraging the development of innovative therapeutic solutions with improved clinical performance. In addition, broader availability of affordable generic antidepressants is increasing treatment accessibility across emerging and developing economies. The expansion of telehealth services and digital healthcare platforms is further improving access to psychiatric care among underserved populations. Antidepressant medications are widely utilized for the treatment of multiple mental health disorders and continue to play a critical role in supporting emotional wellbeing and long-term psychiatric disease management across global healthcare systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $19.8 Billion |

| Forecast Value | $41.2 Billion |

| CAGR | 7.7% |

The antidepressant drugs market continues to benefit from increasing healthcare investments and expanding mental health support infrastructure worldwide. Growing awareness campaigns and public health initiatives focused on reducing the stigma associated with mental illness are encouraging more individuals to seek professional treatment and medication-based therapy solutions. The rising burden of emotional stress, lifestyle-related psychological disorders, and chronic mental health conditions is further strengthening demand for antidepressant therapies. Pharmaceutical companies are increasingly focusing on the development of advanced formulations with improved safety, tolerability, and faster therapeutic response rates, supporting continued market growth throughout the forecast period.

The Selective Serotonin Reuptake Inhibitors (SSRIs) segment accounted for a share of 55.7% in 2025. The strong market position of SSRIs is primarily supported by their proven therapeutic effectiveness, favorable safety profile, and improved patient tolerability compared to conventional antidepressant drug classes. These therapies are widely preferred as first-line treatment options for depression and anxiety-related conditions due to their lower risk of adverse effects and broader suitability across diverse patient populations. Increasing physician preference for safer and more effective treatment approaches is further contributing to segment growth worldwide.

The oral segment is projected to reach USD 32.8 billion by 2035. Segment growth is mainly driven by strong patient preference for oral dosage forms due to their convenience, affordability, ease of administration, and non-invasive nature. The widespread availability of both branded and generic oral antidepressant medications has also improved accessibility across various healthcare settings and patient demographics. In addition, oral antidepressants continue to maintain high adoption rates due to their established long-term efficacy and favorable safety records in the treatment of psychiatric disorders.

North America Antidepressant Drugs Market accounted for 39.9% share in 2025. The region continues to lead the market due to the high prevalence of mental health disorders, strong healthcare spending, and broad adoption of advanced psychiatric treatment solutions. Well-developed healthcare infrastructure, favorable reimbursement policies, and growing awareness regarding mental health management are contributing significantly to market expansion across North America. Rising diagnosis rates and increasing access to specialized psychiatric care services are further strengthening the region's market position throughout the forecast period.

Major companies operating in the Antidepressant Drugs Market include Bristol-Myers Squibb, Eli Lilly and Company, GlaxoSmithKline, H. Lundbeck, Johnson & Johnson, N.V. Organon, Novartis, Opko Health, Otsuka Pharmaceutical, Patheon, Pfizer, Sandoz, Sun Pharmaceuticals, Taj Pharma, Takeda Pharmaceuticals, Teva Pharmaceutical Industries, and Zhejiang NHU Company. Companies operating in the Antidepressant Drugs Market are implementing several strategic initiatives to strengthen their market presence and improve competitive positioning globally. Leading pharmaceutical companies are investing heavily in research and development activities to introduce innovative antidepressant therapies with enhanced efficacy, improved safety profiles, and faster therapeutic outcomes. Strategic collaborations, licensing agreements, and mergers are helping organizations expand product portfolios and accelerate drug commercialization across international markets. Companies are also focusing on increasing generic drug production to improve affordability and broaden patient access to antidepressant medications. Expanding digital healthcare integration, telemedicine partnerships, and online pharmacy distribution channels are further supporting market penetration. In addition, industry participants are prioritizing regulatory approvals, advanced formulation technologies, and awareness initiatives to strengthen brand visibility and reinforce their foothold within the global antidepressant drugs industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Application trends

- 2.2.4 Route of administration trends

- 2.2.5 Medication type trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of depression and anxiety disorders

- 3.2.1.2 Increasing investment in research and development

- 3.2.1.3 Growing awareness regarding treatment therapies and mental health

- 3.2.1.4 Advancements in personalized medicine

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects associated with some antidepressant drugs

- 3.2.2.2 Customer preference for non-pharmacological therapeutics over pharmacological therapeutics

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of telepsychiatry and digital health platforms

- 3.2.3.2 Increasing focus on pediatric and adolescent mental health

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Pipeline analysis (Driven by Primary Research)

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Impact of AI and generative AI on the market (Driven by Primary Research)

- 3.8 Consumer behaviour analysis (Driven by Primary Research)

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Selective serotonin reuptake inhibitors (SSRIs)

- 5.3 Serotonin and noradrenaline reuptake inhibitors (SNRIs)

- 5.4 Tricyclic antidepressants (TCAs)

- 5.5 Atypical antidepressants

- 5.6 Norepinephrine-dopamine reuptake inhibitor (NDRI)

- 5.7 Monoamine oxidase inhibitors (MAOIs)

- 5.8 Other drug classes

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Major depressive disorder

- 6.3 Generalized anxiety disorder

- 6.4 Obsessive-compulsive disorder

- 6.5 Panic disorder

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

- 7.4 Nasal

- 7.5 Transdermal

Chapter 8 Market Estimates and Forecast, By Medication Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Branded

- 8.3 Generic

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Bristol-Myers Squibb

- 11.2 Eli Lilly and Company

- 11.3 GlaxoSmithKline

- 11.4 H. Lundbeck

- 11.5 Johnson & Johnson

- 11.6 N.V. Organon

- 11.7 Novartis

- 11.8 Opko Health

- 11.9 Otsuka Pharmaceutical

- 11.10 Patheon

- 11.11 Pfizer

- 11.12 Sandoz

- 11.13 Sun Pharmaceuticals

- 11.14 Taj Pharma

- 11.15 Takeda Pharmaceuticals

- 11.16 Teva Pharmaceutical Industries

- 11.17 Zhejiang NHU Company