|

市場調查報告書

商品編碼

2061347

醫療保健追蹤溯源解決方案市場:市場機會、成長促進因素、產業趨勢分析及未來預測(2026-2035 年)Track and Trace Solutions in Healthcare Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

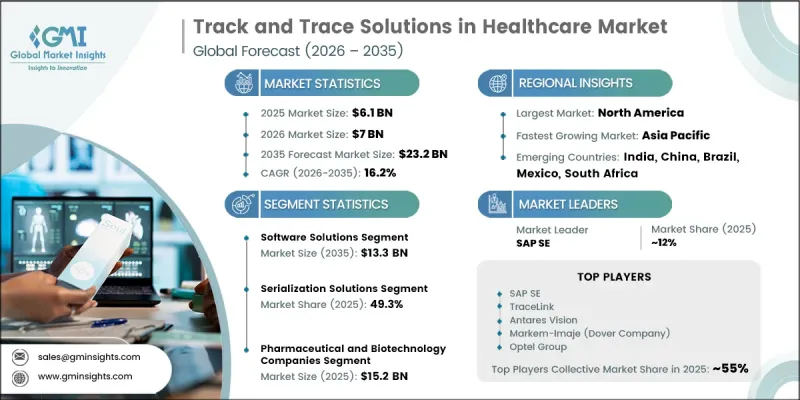

2025 年全球醫療保健追蹤與追溯解決方案市場價值 61 億美元,預計到 2035 年將達到 232 億美元,年複合成長率為 16.2%。

這一強勁的市場成長是由製藥、生物技術和醫療設備製造業日益成長的需求所驅動的。醫療保健追蹤溯源解決方案包含先進技術,旨在監控、驗證和管理整個供應鏈(從生產設施到終端用戶分銷管道)中的藥品和醫療設備。這些系統利用序列化、條碼標籤、RFID追蹤和整合資料管理軟體等技術,提高產品透明度,防止假冒偽劣產品,並確保符合監管要求。對供應鏈安全和產品真實性的日益關注正在顯著加速全球市場的普及。醫療保健公司擴大採用追蹤溯源系統,以確保即時產品可見性,增強庫存管理,提高召回效率,並減少假藥流通。隨著對監管合規性、病患安全和藥品物流管理的要求不斷提高,追蹤溯源技術正日益成為現代醫療保健供應鏈營運的關鍵要素。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 61億美元 |

| 市場規模預測 | 232億美元 |

| 複合年成長率 | 16.2% |

軟體解決方案市場預計在2025年將達到34億美元,到2035年將達到133億美元,預測期內複合年成長率(CAGR)為16.5%。隨著企業尋求能夠實現供應鏈數據分析、改善庫存管理和增強營運決策的整合系統,對先進軟體平台的需求持續成長。現代化的追蹤溯源軟體解決方案提供進階分析功能,使相關企業能夠最佳化工作流程效率、加強產品監控並提高整個供應鏈的透明度。此外,這些軟體平台可以與現有的ERP系統、倉庫管理解決方案和其他業務應用程式整合,從而提高營運效率和生產力。

預計到2025年,序列化解決方案市佔率將達到49.3%。序列化技術允許為整個供應鏈中的各個產品分配唯一的識別碼,其高普及率持續推動著該細分市場的成長。序列化能夠改善產品追蹤,提升庫存管理效率,並有助於快速識別和清除市場上的缺陷產品和仿冒品。日益嚴格的藥品可追溯性和供應鏈透明度監管要求,進一步加速了醫療產業對基於序列化的系統的需求。

到2025年,北美醫療保健追蹤溯源解決方案市佔率將達到37.7%。該地區憑藉健全的法規結構、先進的醫療保健基礎設施以及製藥和生物技術行業廣泛的技術應用,保持其主導地位。藥品可追溯性和產品序列化的嚴格監管要求,推動了先進追蹤溯源系統在整個醫療保健供應鏈中的大規模部署。此外,對數位化醫療保健基礎設施和供應鏈現代化的巨額投資也持續支撐著該地區的市場成長。

目錄

第1章:分析方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 假藥增多

- 醫療設備和製藥業的成長,以及序列化技術的日益普及。

- 製造商們正更加重視保護自己的品牌。

- 產業潛在風險與挑戰

- 前期成本高昂

- 序列化和聚合缺乏標準化

- 市場機遇

- 物聯網與即時狀態監測的整合

- 區塊鏈和分散式帳本技術能夠實現不可篡改的可追溯性

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術展望

- 最新科技趨勢

- 新興技術

- 價格趨勢分析

- 未來市場趨勢

- 波特五力分析

- PESTLE分析

- 專利分析

- 人工智慧和生成式人工智慧對市場的影響

- 價值鏈分析

- 差距分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 競爭定位矩陣

- 主要公司的競爭分析

- 主要趨勢

- 企業合併(M&A)

- 商業夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依組件分類(2022-2035 年)

- 軟體解決方案

- 工廠經理

- 捆綁追蹤解決方案

- 專案追蹤解決方案

- 倉庫和運輸經理

- 其他軟體解決方案

- 硬體

- 印刷設備

- 掃描器

- 標籤機

- 程式碼讀取器

- 其他硬體組件

- 服務

- 雲端管理

- 資料庫管理

- 網路解決方案

第6章 市場估計與預測:依應用領域分類(2022-2035 年)

- 序列化解決方案

- 瓶裝穀物

- 標籤序列化

- 紙箱序列化

- 醫療設備序列化

- 其他序列化

- 聚合解決方案

- 捆綁聚合

- 病例聚集

- 調色板聚合

- 其他用途

第7章 市場估計與預測:依技術分類(2022-2035 年)

- 條碼

- RFID

- 其他技術

第8章 市場估算與預測:依最終用途分類(2022-2035 年)

- 製藥和生物技術公司

- 醫療設備製造商

- 其他最終用戶

第9章 市場估計與預測:按地區分類(2022-2035 年)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- ACG Worldwide

- Adents

- Antares Vision

- Axway

- Kezzler

- Korber

- Markem-Imaje(Dover Company)

- Mettler-Toledo International

- OPTEL Vision

- Rfxcel Corporation

- SAP SE

- SEIDENADER MASCHINENBAU

- Siemens

- Syntegon Technology GmbH

- TraceLink

- VariTec Consulting

- Zetes

The Global Track and Trace Solutions in Healthcare Market was valued at USD 6.1 billion in 2025 and is estimated to grow at a CAGR of 16.2% to reach USD 23.2 billion by 2035.

Strong market growth is supported by rising demand across pharmaceutical manufacturing, biotechnology, and medical device production industries. Track and trace solutions in healthcare involve advanced technologies designed to monitor, authenticate, and manage pharmaceutical products and medical devices throughout the supply chain, from manufacturing facilities to end-user distribution channels. These systems utilize technologies such as serialization, barcode labeling, RFID tracking, and integrated data management software to improve product transparency, prevent counterfeiting, and maintain regulatory compliance. Increasing focus on supply chain security and product authenticity is significantly accelerating market adoption worldwide. Healthcare companies are increasingly implementing track and trace systems to achieve real-time product visibility, strengthen inventory management, improve recall efficiency, and reduce the circulation of falsified medicines. The growing need for regulatory compliance, enhanced patient safety, and improved pharmaceutical logistics management continues to position track and trace technologies as a critical component of modern healthcare supply chain operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.1 Billion |

| Forecast Value | $23.2 Billion |

| CAGR | 16.2% |

The software solutions segment generated USD 3.4 billion in 2025 and is projected to reach USD 13.3 billion by 2035, expanding at a CAGR of 16.5% during the forecast period. Demand for advanced software platforms continues to increase as organizations seek integrated systems capable of analyzing supply chain data, improving inventory management, and enhancing operational decision-making. Modern track and trace software solutions offer advanced analytics capabilities that allow healthcare companies to optimize workflow efficiency, strengthen product monitoring, and improve overall supply chain visibility. In addition, these software platforms can be integrated with existing enterprise resource planning systems, warehouse management solutions, and other business applications to streamline operations and improve productivity.

The serialization solutions segment held a 49.3% share in 2025. High adoption of serialization technologies continues to drive segment growth due to their ability to assign unique identification codes to individual products throughout the supply chain. Serialization improves product tracking, strengthens inventory control, and supports rapid identification and removal of defective or counterfeit products from the market. Increasing regulatory requirements surrounding pharmaceutical traceability and supply chain transparency are further accelerating demand for serialization-based systems across the healthcare industry.

North America Track and Trace Solutions in Healthcare Market accounted for 37.7% share in 2025. The region maintains a dominant position due to strong regulatory frameworks, advanced healthcare infrastructure, and widespread technology adoption across the pharmaceutical and biotechnology industries. Strict regulatory mandates regarding pharmaceutical traceability and product serialization are encouraging large-scale implementation of advanced track and trace systems throughout the healthcare supply chain. In addition, high investments in digital healthcare infrastructure and supply chain modernization continue to support regional market growth.

Major companies operating in the Global Track and Trace Solutions in Healthcare Market include SAP SE, Siemens, TraceLink, OPTEL GROUP, Antares Vision, Syntegon Technology GmbH, Axway, ACG Worldwide, Kezzler, Rfxcel Corporation, Zetes, Arvato Systems, VariTec Consulting, Markem-Imaje, and Mettler-Toledo International. Companies operating in the track and trace solutions in healthcare market are implementing several strategic initiatives to strengthen their market position and improve competitive advantage. Businesses are heavily investing in advanced serialization technologies, cloud-based platforms, and AI-driven analytics solutions to improve supply chain transparency and regulatory compliance. Strategic partnerships and collaborations with pharmaceutical manufacturers, biotechnology companies, and healthcare distributors are helping organizations expand their customer base and strengthen industry presence. Companies are also focusing on integrating track and trace systems with enterprise software platforms and warehouse management systems to provide seamless operational efficiency. Continuous investments in RFID technologies, blockchain-enabled traceability solutions, and real-time monitoring systems are further enhancing product security and inventory visibility.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Application trends

- 2.2.4 Technology trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing number of counterfeit drugs

- 3.2.1.2 Growth in the medical devices and pharmaceutical industries, coupled with rise in implementation of serialization

- 3.2.1.3 Increased focus on manufacturers on brand protection

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Substantial setup costs

- 3.2.2.2 Lack of standardization in serialisation and aggregation

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of IoT and real-time condition monitoring

- 3.2.3.2 Blockchain and distributed ledger technology for immutable traceability

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing trend analysis (Driven by primary research)

- 3.7 Future market trends (Driven by primary research)

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Patent analysis

- 3.11 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.12 Value chain analysis (Driven by primary research)

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Software solutions

- 5.2.1 Plant managers

- 5.2.2 Bundle tracking solutions

- 5.2.3 Case tracking solutions

- 5.2.4 Warehouse and shipment managers

- 5.2.5 Other software solutions

- 5.3 Hardware

- 5.3.1 Printing devices

- 5.3.2 Scanners

- 5.3.3 Labelers

- 5.3.4 Code readers

- 5.3.5 Other hardware components

- 5.4 Services

- 5.4.1 Cloud management

- 5.4.2 Database management

- 5.4.3 Networking solutions

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Serialization solutions

- 6.2.1 Bottle serialization

- 6.2.2 Label serialization

- 6.2.3 Carton serialization

- 6.2.4 Medical devices serialization

- 6.2.5 Other serializations

- 6.3 Aggregation solutions

- 6.3.1 Bundle aggregation

- 6.3.2 Case aggregation

- 6.3.3 Pallet aggregation

- 6.4 Other applications

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Barcodes

- 7.3 RFID

- 7.4 Other technologies

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical and biotechnology companies

- 8.3 Medical device companies

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ACG Worldwide

- 10.2 Adents

- 10.3 Antares Vision

- 10.4 Axway

- 10.5 Kezzler

- 10.6 Korber

- 10.7 Markem-Imaje (Dover Company)

- 10.8 Mettler-Toledo International

- 10.9 OPTEL Vision

- 10.10 Rfxcel Corporation

- 10.11 SAP SE

- 10.12 SEIDENADER MASCHINENBAU

- 10.13 Siemens

- 10.14 Syntegon Technology GmbH

- 10.15 TraceLink

- 10.16 VariTec Consulting

- 10.17 Zetes

醫院資產追蹤市場預測至2034年—按組件、技術、資產類型、部署模式、應用、最終用戶和地區分類的全球分析

醫院資產追蹤市場預測至2034年—按組件、技術、資產類型、部署模式、應用、最終用戶和地區分類的全球分析 2026年全球醫院資產管理系統市場報告

2026年全球醫院資產管理系統市場報告 全球醫院資產追蹤和庫存管理系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球醫院資產追蹤和庫存管理系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 醫院資產管理市場規模、佔有率及成長分析(按產品、應用及地區分類)-2026-2033年產業預測

醫院資產管理市場規模、佔有率及成長分析(按產品、應用及地區分類)-2026-2033年產業預測 醫院資產管理系統市場規模、佔有率及成長分析(按產品類型、應用、最終用戶和地區分類)-2026-2033年產業預測2025年人工智慧(AI)賦能的醫院資產租賃市場報告全球醫院資產管理市場預測至2032年:按產品、應用、最終用戶和地區分類的分析2025年全球醫院資產追蹤與庫存管理系統市場報告醫院資產管理市場規模(按產品、應用、最終用戶、區域範圍和預測)

醫院資產管理系統市場規模、佔有率及成長分析(按產品類型、應用、最終用戶和地區分類)-2026-2033年產業預測2025年人工智慧(AI)賦能的醫院資產租賃市場報告全球醫院資產管理市場預測至2032年:按產品、應用、最終用戶和地區分類的分析2025年全球醫院資產追蹤與庫存管理系統市場報告醫院資產管理市場規模(按產品、應用、最終用戶、區域範圍和預測)