|

市場調查報告書

商品編碼

2061306

音響市場機會、成長要素、產業趨勢分析及2026-2035年預測Audio Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

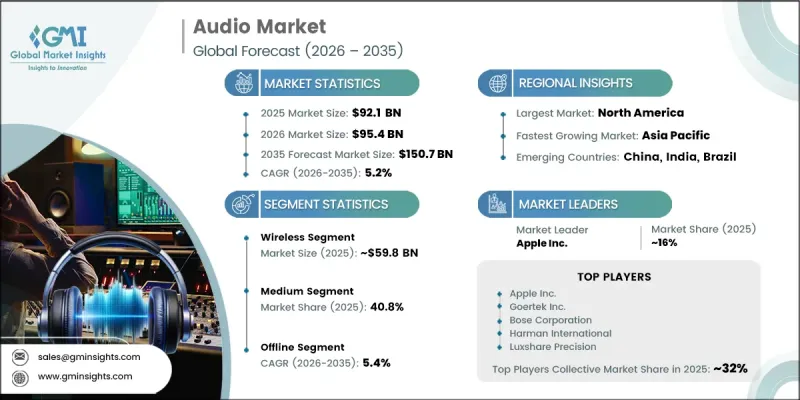

2025年全球音響市場價值921億美元,預計將以5.2%的複合年成長率成長,到2035年達到1507億美元。

市場擴張的驅動力在於音訊消費方式的快速轉變,數位音訊已成為現代娛樂習慣的核心,包括串流平台、播客和有聲讀物。高速網際網路的普及和數位生態系統的持續發展改變了用戶發現、獲取和使用音訊內容的方式。使用者對個人化、點播式聆聽體驗日益成長的需求,正在進一步改變全球用戶的消費模式。 Apple Music、Spotify 和 Amazon Music 等主流串流服務透過為數十億用戶提供龐大的音樂庫、音訊內容和精選音訊體驗,持續推動市場成長。同時,兼具連接性、便利性和更佳音質的智慧無線音訊設備的需求也不斷成長。 Wi-Fi 音箱、藍牙音訊系統和真無線立體聲耳機等產品正擴大應用於住宅和商業環境中,反映出使用者對連網沉浸式音訊體驗的廣泛需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 921億美元 |

| 預測金額 | 1507億美元 |

| 複合年成長率 | 5.2% |

預計到2025年,無線市場規模將達到598億美元,並在2026年至2035年間以6.3%的複合年成長率成長。無線音訊解決方案持續推動市場成長,這主要得益於消費者對行動性、便利性和無線使用的強勁需求。真無線立體聲耳機、藍牙音箱和Wi-Fi智慧音訊系統等設備在家庭和商用環境中均已廣泛應用。電池性能、訊號穩定性和低延遲傳輸的提升顯著提高了產品的可靠性,使無線連接成為現代音訊應用的標準選擇。

2025年,中階價位音訊產品將佔據40.8%的市場佔有率,並持續保持其在全球音訊產業的主導地位。該細分市場憑藉其價格適中且性能卓越的特點,吸引了許多消費者,從而確立了穩固的地位。這一價位的消費者重視清晰的音質、長久的使用壽命以及降噪、無線連接和智慧整合等先進功能,而無需投入過多的高階產品。中階價位產品廣泛應用於耳機、揚聲器、條形音箱和家庭音響系統,也深受追求價格實惠且性能可靠的半專業用戶和內容創作者的青睞。

美國音響市場預計到2025年將達到283億美元,並在2026年至2035年間以4%的複合年成長率成長。該市場高度發達,高度重視創新,並受到家用電子電器、專業音訊和內容創作領域強勁需求的支撐。串流媒體服務、遊戲平台和智慧家居技術的日益普及持續推動著對無線耳機、智慧音箱和家庭劇院系統等先進音訊設備的需求。包括錄音室、廣播公司和內容創作者在內的成熟專業音訊生態系統進一步促進了市場擴張。此外,內容創作經濟和播客產業的成長也增加了對麥克風、音訊介面和錄音室級設備的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 零件供應商和原料

- OEM製造商和契約製造

- 配電網路

- 系統整合商和安裝合作夥伴

- 最終用戶群涵蓋消費者、專業人士和商業領域。

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 串流服務和內容消費的普及

- 智慧家庭與物聯網生態系統的融合

- 對優質音訊體驗(消費者和專業人士)的需求日益成長

- 加速在家工作和混合辦公模式的推廣

- 產業潛在風險與挑戰

- 專業和高級系統高成本

- 成熟消費市場飽和

- 機會

- 進入新興市場

- 專業消費級與家庭工作室市場的成長

- 模組化、可擴展的音訊系統解決方案

- 用於健康、保健和輔助的音訊應用程式

- 促進因素

- 成長潛力分析

- 監理框架

- 產品安全和認證標準

- 區域無線通訊法規

- 環境合規性(RoHS、WEEE、REACH、衝突礦產)

- 專業音訊標準

- 汽車音響系統的安全標準

- 智慧財產權和專利保護

- 關鍵市場趨勢與顛覆性因素

- 技術與創新展望

- 空間音訊與身臨其境型聲音技術

- 主動降噪 (ANC) 與環境音管理

- 音訊轉碼器(LDAC、aptX、LC3、Hi-Res Audio)的進步

- 網路音訊協定(Dante、AES67、AVB、SMPTE 2110)

- 數位訊號處理和音訊處理領域的創新

- 電池和電源管理技術

- 材料科學與聲學

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 價格彈性與價值感知分析

- 未來市場趨勢

- 供應鏈分析

- 關鍵部件的依賴性

- 區域製造地

- 供應鏈韌性與風險因素

- 垂直整合趨勢

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 區域間貿易依賴與多元化趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 人工智慧驅動的音訊處理和個人化

- 風險、限制和監管考量

- 波特的分析

- PESTLE分析

- 市場基礎設施和生產能力概述

- 按地區和產品類型的產能

- 產能運轉率及擴建計劃

- 按應用程式分發基礎設施

- 消費行為分析

- 購買模式

- 偏好分析

- 不同地區的消費者行為差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 感應器

- 麥克風

- 動圈麥克風

- 電容式麥克風

- 帶狀麥克風

- 領夾式麥克風

- 槍式麥克風

- USB麥克風

- 無線麥克風系統

- 揚聲器和驅動單元

- 低音單體和超低音揚聲器單元

- 中階單元

- 高音喇叭和高頻驅動器

- 全頻驅動

- 同軸和三軸揚聲器

- 耳機和耳塞

- 頭戴式耳機

- 貼耳式耳機

- 入耳式監聽耳機(IEM)

- 真無線立體聲(TWS)耳機

- 開放式耳機

- 專業錄音室耳機

- 遊戲耳機

- 麥克風

- 訊號處理和放大

- 混合器

- 類比混音器

- 數位混音器

- 電動攪拌機

- DJ混音器

- 廣播混音器

- 擴大機

- 功率放大器

- 綜合整合式機

- 前級擴大機

- AV接收器

- 吉他、貝斯和鍵盤擴大器

- 汽車音響擴大機

- 訊號處理器

- 均衡器(圖形、參數)

- 壓縮器和限幅器

- 效果處理器

- DSP單元和音訊處理器

- 分音器和揚聲器管理系統

- 混合器

- 音訊介面和轉換器

- USB音訊介面(2聲道、多聲道)

- Thunderbolt 音訊介面

- 網路音訊介面(Dante、AVB)

- 獨立式類比數位轉換器

- 完整音響系統(整合產品)

- 有源/主動揚聲器系統

- 可攜式藍牙音箱

- 智慧音箱(支援語音功能)

- 條形音箱

- 有源監聽音箱

- 公共廣播揚聲器和線陣列

- 有源重低音

- 家庭劇院系統

- 2.1聲道系統

- 5.1聲道系統

- 7.1聲道或更高系統

- 杜比全景聲/物件式的系統

- 汽車音響系統

- OEM整合系統

- 售後市場組件系統

- 高級/豪華汽車音響

- 固定聲學系統

- 商業背景音樂系統

- 會議室音響系統

- 公共廣播(PA)系統

- 禮拜場所的音響系統

- 體育場館音響系統

- 播放及錄音設備

- 有源/主動揚聲器系統

- 唱盤和唱片機

- 手動轉盤

- 自動轉盤

- DJ唱盤(直驅式)

- 皮帶傳動與直接傳動

- 數位音訊播放器

- 可攜式高解析度音訊播放器

- 網路音訊播放器

- CD播放器和傳輸系統

- 記錄系統

- 可攜式錄音機(現場錄音)

- 多軌錄音機

- DAW 控制器硬體

第6章 市場估算與預測:技術與互聯互通,2022-2035年

- 限有線設備

- 模擬有線

- 數位有線

- 無線支援裝置

- 僅限無線連接(無有線連接)

- 真無線立體聲(TWS)耳機

- 僅限無線揚聲器

- 無線連接,有線備用(雙模)

- 耳機(無線+3.5mm有線)

- 揚聲器(無線+AUX輸入)

- 透過主要無線協議

- 基於藍牙

- 基於Wi-Fi

- 射頻/專有無線電

- 網路音訊(商用)

- 僅限無線連接(無有線連接)

第7章 市場估計與預測:依價格區間分類,2022-2035年

- 低的

- 中等的

- 高的

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 供住宅使用

- 家庭娛樂

- 個人音訊

- 遊戲和電子競技

- 健身與健康

- 家庭娛樂

- 專業消費者與內容創作者

- 家庭工作室和專案工作室

- 播客和串流媒體

- 內容創作者(YouTube、社群媒體)

- 音樂家和樂隊(非商業用途)

- 專業音訊製作

- 商業錄音棚

- 廣播公司/廣播站

- 後製設施

- 電影和電視製作

- 現場音響表演

- 音樂會和節日製作

- 戲劇與表演藝術

- 公司活動和會議

- 禮拜場所

- 固定安裝商用音響系統(B2B - 固定安裝)

- 公司總部

- 會議室與會客空間

- 禮堂及市政廳

- 開放式辦公室中的背景噪音掩蔽

- 飯店業

- 飯店

- 餐廳和酒吧

- 零售

- 教育

- 衛生保健

- 醫院

- 診所和醫療辦公室

- 治療和復健中心

- 交通樞紐

- 飛機場

- 火車站

- 客運站

- 體育設施和體育場

- 電影院及娛樂中心

- 電影院

- IMAX影院與特色影院

- 娛樂設施

- 車

- 原廠汽車音響

- 汽車音響改裝市場

- 商用車音訊

- 公司總部

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 品牌官方網站

- 電子商務平台

- 離線

- 量販店

- 音響專賣店

- 百貨公司

- 倉儲式會員俱樂部

- 免稅和旅遊零售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- UAE

- 南非

第11章:公司簡介

- 世界公司

- Sony Corporation

- Apple Inc.

- Bose Corporation

- Harman International(Samsung)

- Yamaha Corporation

- Sennheiser

- Logitech International

- Shure Incorporated

- Goertek Inc.

- Luxshare Precision

- 當地公司

- Bang & Olufsen

- Audio-Technica

- Focal-JMlab

- Bowers & Wilkins

- Jabra(GN Audio)

- QSC Audio Products

- Genelec

- 新興企業

- Anker Innovations(Soundcore)

- Edifier International

- Sonos Inc.

- Razer Inc.

The Global Audio Market was valued at USD 92.1 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 150.7 billion by 2035.

Market expansion is driven by the rapid shift toward digital audio consumption, including streaming platforms, podcasts, and audiobooks, which have become central to modern entertainment habits. Widespread high-speed internet access and continuous advancements in digital ecosystems have transformed how users discover, access, and engage with audio content. Rising demand for personalized and on-demand listening experiences is further reshaping consumption patterns across global audiences. Major streaming services such as Apple Music, Spotify, and Amazon Music continue to influence market growth by offering extensive libraries of music, spoken-word content, and curated audio experiences to billions of users. At the same time, demand is rising for smart and wireless audio devices that combine connectivity, convenience, and enhanced sound performance. Products such as Wi-Fi-enabled speakers, Bluetooth audio systems, and true wireless stereo earbuds are increasingly integrated into both residential and commercial environments, reflecting a broader shift toward connected and immersive audio experiences.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $92.1 Billion |

| Forecast Value | $150.7 Billion |

| CAGR | 5.2% |

The wireless segment generated USD 59.8 billion in 2025 and is expected to grow at a CAGR of 6.3% from 2026 to 2035. Wireless audio solutions continue to lead the market due to strong consumer preference for mobility, convenience, and cable-free usage. Devices such as true wireless stereo earbuds, Bluetooth-enabled speakers, and Wi-Fi-connected smart audio systems are widely adopted across both home and professional environments. Improvements in battery performance, signal stability, and low-latency transmission have significantly strengthened product reliability, making wireless formats the preferred standard for modern audio consumption.

The medium price segment accounted for 40.8% share in 2025, maintaining a leading position across the global audio industry. This segment is strongly positioned due to its ability to balance affordability with high-performance features, attracting a broad base of consumers. Buyers in this category prioritize clear sound quality, long-lasting durability, and advanced capabilities such as noise reduction, wireless connectivity, and smart integration, without entering premium pricing tiers. It is widely adopted across headphones, speakers, soundbars, and home audio systems, and is also favored by semi-professional users and creators who require dependable performance at reasonable cost levels.

United States Audio Market reached USD 28.3 billion in 2025 and is projected to grow at a CAGR of 4% from 2026 to 2035. The market is highly developed and innovation-focused, supported by strong demand across consumer electronics, professional audio, and content creation segments. Widespread adoption of streaming services, gaming platforms, and smart home technologies continues to drive demand for advanced audio devices such as wireless headphones, smart speakers, and home theater systems. A well-established professional audio ecosystem, including studios, broadcasters, and creators, further supports market expansion. Growth in the creator economy and podcasting sector is also increasing demand for microphones, audio interfaces, and studio-grade equipment.

Major companies operating in the Global Audio Market include Apple Inc., Sony Corporation, Bose Corporation, Yamaha Corporation, Harman International, Sennheiser, Logitech International, Shure Incorporated, Goertek Inc., and Luxshare Precision. Additional key regional participants include Bang & Olufsen, Bowers & Wilkins, Audio-Technica, Focal-JMlab, Jabra (GN Audio), QSC Audio Products, and Genelec. Emerging and innovation-driven players include Sonos Inc., Edifier International, Anker Innovations (Soundcore), and Razer Inc. Companies in the audio market are actively strengthening their competitive positioning through continuous innovation in wireless and smart audio technologies, with a strong focus on improving sound quality, connectivity, and battery efficiency. Many players are expanding product ecosystems that integrate headphones, speakers, and smart home devices to enhance user experience and brand loyalty. Strategic partnerships with streaming platforms, smartphone manufacturers, and gaming companies are helping improve product integration and market reach. Firms are also investing heavily in R&D to develop immersive audio technologies such as spatial sound and AI-powered personalization.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Region

- 2.2.2 Product type

- 2.2.3 Technology and connectivity

- 2.2.4 Price

- 2.2.5 End Use Application

- 2.2.6 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Component suppliers & raw materials

- 3.1.2 OEM manufacturers & contract manufacturing

- 3.1.3 Distribution networks

- 3.1.4 Systems integrators & installation partners

- 3.1.5 End-user segments across consumer, professional, commercial

- 3.1.6 Profit margin

- 3.1.7 Value addition at each stage

- 3.1.8 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Proliferation of streaming services & content consumption

- 3.2.1.2 Smart home & iot ecosystem integration

- 3.2.1.3 Rising demand for premium audio experiences (consumer & professional)

- 3.2.1.4 Work-from-home & hybrid workplace acceleration

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of professional & premium systems

- 3.2.2.2 Market saturation in mature consumer segments

- 3.2.3 Opportunities

- 3.2.3.1 Emerging markets penetration

- 3.2.3.2 Prosumer & home studio market growth

- 3.2.3.3 Modular & scalable audio system solutions

- 3.2.3.4 Health, wellness & assistive audio applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 Product safety & certification standards

- 3.4.2 Wireless communication regulations by region

- 3.4.3 Environmental compliance (RoHS, WEEE, REACH, Conflict Minerals)

- 3.4.4 Professional audio standards

- 3.4.5 Automotive audio safety standards

- 3.4.6 Intellectual property & patent protection

- 3.5 Major market trends and disruptions

- 3.6 Technological and innovation landscape

- 3.6.1 Spatial audio & immersive sound technologies

- 3.6.2 Active noise cancellation (ANC) & environmental sound management

- 3.6.3 Audio codec advancements (LDAC, aptX, LC3, Hi-Res Audio)

- 3.6.4 Networked audio protocols (Dante, AES67, AVB, SMPTE 2110)

- 3.6.5 DSP & audio processing innovations

- 3.6.6 Battery & power management technologies

- 3.6.7 Materials science & acoustic engineering

- 3.7 Pricing Analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7.3 Price elasticity & value perception analysis (Driven by Primary Research)

- 3.8 Future market trends

- 3.9 Supply Chain Analysis

- 3.9.1 Critical component dependencies

- 3.9.2 Regional manufacturing hubs

- 3.9.3 Supply chain resilience & risk factors

- 3.9.4 Vertical integration trends

- 3.10 Trade data analysis (driven by paid database) (HS Code- 85182200)

- 3.10.1 Import/export volume & value trends (driven by primary research)

- 3.10.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10.3 Regional Trade Dependencies & Diversification Trends

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 Gen-AI use cases & adoption roadmap by segment

- 3.11.3 AI-Enhanced Audio Processing & Personalization

- 3.11.4 Risks, limitations & regulatory considerations

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Market infrastructure & production capacity landscape (driven by primary research)

- 3.14.1 Manufacturing capacity by region & product category

- 3.14.2 Production capacity utilization & expansion pipelines

- 3.14.3 Distribution infrastructure by end-use segment

- 3.15 Consumer behaviour analysis

- 3.15.1 Purchasing patterns

- 3.15.2 Preference analysis

- 3.15.3 Regional variations in consumer behaviour

- 3.15.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Transducers

- 5.2.1 Microphones

- 5.2.1.1 Dynamic Microphones

- 5.2.1.2 Condenser Microphones

- 5.2.1.3 Ribbon Microphones

- 5.2.1.4 Lavalier/Lapel Microphones

- 5.2.1.5 Shotgun Microphones

- 5.2.1.6 USB Microphones

- 5.2.1.7 Wireless Microphone Systems

- 5.2.2 Loudspeakers & Drivers

- 5.2.2.1 Woofers & Subwoofer Drivers

- 5.2.2.2 Midrange Drivers

- 5.2.2.3 Tweeters & High-Frequency Drivers

- 5.2.2.4 Full-Range Drivers

- 5.2.2.5 Coaxial & Triaxial Speakers

- 5.2.3 Headphones & Earphones

- 5.2.3.1 Over-Ear Headphones

- 5.2.3.2 On-Ear Headphones

- 5.2.3.3 In-Ear Monitors (IEMs)

- 5.2.3.4 True Wireless Stereo (TWS) Earbuds

- 5.2.3.5 Open-Ear Earbuds

- 5.2.3.6 Professional Studio Headphones

- 5.2.3.7 Gaming Headsets

- 5.2.1 Microphones

- 5.3 Signal Processing & Amplification

- 5.3.1 Mixers

- 5.3.1.1 Analog Mixers

- 5.3.1.2 Digital Mixers

- 5.3.1.3 Powered Mixers

- 5.3.1.4 DJ Mixers

- 5.3.1.5 Broadcast Mixers

- 5.3.2 Amplifiers

- 5.3.2.1 Power Amplifiers

- 5.3.2.2 Integrated Amplifiers

- 5.3.2.3 Pre-Amplifiers

- 5.3.2.4 AV Receivers

- 5.3.2.5 Guitar/Bass/Keyboard Amplifiers

- 5.3.2.6 Car Audio Amplifiers

- 5.3.3 Signal Processors

- 5.3.3.1 Equalizers (Graphic, Parametric)

- 5.3.3.2 Compressors & Limiters

- 5.3.3.3 Effects Processors

- 5.3.3.4 DSP Units & Audio Processors

- 5.3.3.5 Crossovers & Speaker Management Systems

- 5.3.1 Mixers

- 5.4 Audio Interfaces & Converters

- 5.4.1 USB Audio Interfaces (2-channel, Multi-channel)

- 5.4.2 Thunderbolt Audio Interfaces

- 5.4.3 Networked Audio Interfaces (Dante, AVB)

- 5.4.4 Standalone A/D-D/A Converters

- 5.5 Complete Audio Systems (Integrated Products)

- 5.5.1 Active/Powered Speaker Systems

- 5.5.1.1 Portable Bluetooth Speakers

- 5.5.1.2 Smart Speakers (Voice-Enabled)

- 5.5.1.3 Soundbars

- 5.5.1.4 Active Studio Monitors

- 5.5.1.5 PA Speakers & Line Arrays

- 5.5.1.6 Powered Subwoofers

- 5.5.2 Home Theater Systems

- 5.5.2.1 2.1 Channel Systems

- 5.5.2.2 5.1 Channel Systems

- 5.5.2.3 7.1+ Channel Systems

- 5.5.2.4 Dolby Atmos/Object-Based Systems

- 5.5.3 Car Audio Systems

- 5.5.3.1 OEM Integrated System

- 5.5.3.2 Aftermarket Component Systems

- 5.5.3.3 Premium/Luxury Car Audio

- 5.5.4 Installed Sound Systems

- 5.5.4.1 Commercial Background Music Systems

- 5.5.4.2 Conference Room Audio Systems

- 5.5.4.3 Public Address (PA) Systems

- 5.5.4.4 House of Worship Sound Systems

- 5.5.4.5 Stadium & Arena Audio Systems

- 5.5.4.6 Playback & Recording Devices

- 5.5.1 Active/Powered Speaker Systems

- 5.6 Turntables & Record Players

- 5.6.1 Manual Turntables

- 5.6.2 Automatic Turntables

- 5.6.3 DJ Turntables (Direct-Drive)

- 5.6.4 Belt-Drive vs Direct-Drive

- 5.7 Digital Audio Players

- 5.7.1 Portable Hi-Res Audio Players

- 5.7.2 Network Audio Players

- 5.7.3 CD Players & Transport Systems

- 5.8 Recording Systems

- 5.8.1 Portable Recorders (Field Recording)

- 5.8.2 Multi-Track Recorders

- 5.8.3 DAW Controller Hardware

Chapter 6 Market Estimates & Forecast, By Technology and Connectivity, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Wired-Only Devices

- 6.2.1 Analog Wired

- 6.2.2 Digital Wired

- 6.3 Wireless-Capable Devices

- 6.3.1 Wireless-Only (No Wired Option)

- 6.3.1.1 True Wireless Stereo (TWS) Earbuds

- 6.3.1.2 Wireless-Only Speakers

- 6.3.2 Wireless with Wired Backup (Dual-Mode)

- 6.3.2.1 Headphones (Wireless + 3.5mm Cable)

- 6.3.2.2 Speakers (Wireless + Aux Input)

- 6.3.3 By Primary Wireless Protocol

- 6.3.3.1 Bluetooth-Based

- 6.3.3.2 Wi-Fi-Based

- 6.3.3.3 RF/Proprietary Wireless

- 6.3.3.4 Networked Audio (Professional)

- 6.3.1 Wireless-Only (No Wired Option)

Chapter 7 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By End Use Application, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Residential Consumer

- 8.2.1 Home Entertainment

- 8.2.1.1 Personal Audio

- 8.2.1.2 Gaming & Esports

- 8.2.1.3 Fitness & Wellness

- 8.2.1 Home Entertainment

- 8.3 Prosumer & Content Creation

- 8.3.1 Home Studios & Project Studios

- 8.3.2 Podcasting & Streaming

- 8.3.3 Content Creators (YouTube, Social Media)

- 8.3.4 Musicians & Bands (Non-Commercial)

- 8.4 Professional Audio Production

- 8.4.1 Commercial Recording Studios

- 8.4.2 Broadcast & Radio Stations

- 8.4.3 Post-Production Facilities

- 8.4.4 Film & Television Production

- 8.5 Live Sound & Performance

- 8.5.1 Concert & Festival Production

- 8.5.2 Theater & Performing Arts

- 8.5.3 Corporate Events & Conferences

- 8.5.4 Houses of Worship

- 8.6 Installed Commercial Audio (B2B - Fixed Installation)

- 8.6.1 Corporate Offices

- 8.6.1.1 Conference Rooms & Meeting Spaces

- 8.6.1.2 Auditoriums & Town Halls

- 8.6.1.3 Open Office Background Sound Masking

- 8.6.2 Hospitality

- 8.6.2.1 Hotels

- 8.6.2.2 Restaurants & Bars

- 8.6.3 Retail

- 8.6.4 Education

- 8.6.5 Healthcare

- 8.6.6 Hospitals

- 8.6.6.1 Clinics & Medical Offices

- 8.6.6.2 Therapy & Rehabilitation Centers

- 8.6.7 Transportation Hubs

- 8.6.7.1 Airports

- 8.6.7.2 Train Stations

- 8.6.7.3 Bus Terminals

- 8.6.8 Sports Venues & Stadiums

- 8.6.8.1 Cinema & Entertainment Complexes

- 8.6.8.2 Movie Theaters

- 8.6.8.3 IMAX & Specialty Theaters

- 8.6.8.4 Entertainment Centers

- 8.6.9 Automotive

- 8.6.9.1 OEM Car Audio

- 8.6.9.2 Aftermarket Car Audio

- 8.6.9.3 Commercial Vehicle Audio

- 8.6.1 Corporate Offices

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 Brand websites

- 9.2.2 E-commerce platforms

- 9.3 Offline

- 9.3.1 Consumer electronics retailers

- 9.3.2 Specialty audio stores

- 9.3.3 Department stores

- 9.3.4 Warehouse clubs

- 9.3.5 Duty-free & retail travel

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Sony Corporation

- 11.1.2 Apple Inc.

- 11.1.3 Bose Corporation

- 11.1.4 Harman International (Samsung)

- 11.1.5 Yamaha Corporation

- 11.1.6 Sennheiser

- 11.1.7 Logitech International

- 11.1.8 Shure Incorporated

- 11.1.9 Goertek Inc.

- 11.1.10 Luxshare Precision

- 11.2 Regional Players

- 11.2.1 Bang & Olufsen

- 11.2.2 Audio-Technica

- 11.2.3 Focal-JMlab

- 11.2.4 Bowers & Wilkins

- 11.2.5 Jabra (GN Audio)

- 11.2.6 QSC Audio Products

- 11.2.7 Genelec

- 11.3 Emerging Players

- 11.3.1 Anker Innovations (Soundcore)

- 11.3.2 Edifier International

- 11.3.3 Sonos Inc.

- 11.3.4 Razer Inc.

家庭音響系統市場預測至2034年:按產品、通路、最終用戶和地區分類的全球分析

家庭音響系統市場預測至2034年:按產品、通路、最終用戶和地區分類的全球分析 定向揚聲器市場按產品類型、技術、應用、分銷管道和最終用戶分類,全球預測(2026-2032年)專業音訊混音主機市場:按主機類型、通道數、應用、分銷管道和最終用戶分類 - 全球預測(2026-2032 年)按播放器類型、唱頭類型、分銷管道和最終用戶分類的黑膠唱片播放系統市場—2026-2032年全球預測模擬機架式混音器市場:全球預測(2026-2032 年),按通道數、價格範圍、應用、分銷管道和最終用戶分類類比混音器市場按產品類型、通道數、應用、最終用戶和分銷管道分類 - 全球預測 2026-20322032 年卡帶錄音機和播放器市場預測:按產品類型、功能、通路、通路、應用程式、最終用戶和地區進行分析

定向揚聲器市場按產品類型、技術、應用、分銷管道和最終用戶分類,全球預測(2026-2032年)專業音訊混音主機市場:按主機類型、通道數、應用、分銷管道和最終用戶分類 - 全球預測(2026-2032 年)按播放器類型、唱頭類型、分銷管道和最終用戶分類的黑膠唱片播放系統市場—2026-2032年全球預測模擬機架式混音器市場:全球預測(2026-2032 年),按通道數、價格範圍、應用、分銷管道和最終用戶分類類比混音器市場按產品類型、通道數、應用、最終用戶和分銷管道分類 - 全球預測 2026-20322032 年卡帶錄音機和播放器市場預測:按產品類型、功能、通路、通路、應用程式、最終用戶和地區進行分析