|

市場調查報告書

商品編碼

2045849

烤箱市場機會、成長要素、產業趨勢分析及2026-2035年預測。Oven Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

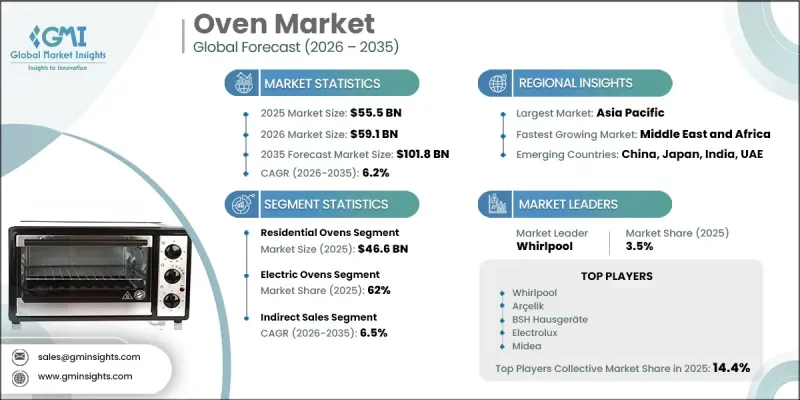

2025年全球烤箱市場價值555億美元,預計年複合成長率為6.2%,到2035年將達到1,018億美元。

隨著消費者越來越傾向於選擇兼具便利性、節能性和現代功能的先進廚房電器,烤箱產業正在蓬勃發展。可支配收入的成長以及消費者對高階廚房設備日益成長的興趣,推動了住宅和商用領域對高科技烤箱的普及。製造商不斷推出創新功能,例如觸控操作、無線連接和多功能烹飪功能,以滿足消費者不斷變化的需求。此外,偏好的改變和人們對智慧廚房技術的日益了解,也促進了家庭烹飪和烘焙的興起,這極大地推動了市場擴張。在包括餐飲服務和旅館業在內的商業環境中,對大容量、高能源效率烤箱的需求依然強勁,以提高營運效率。政府推廣節能環保電器的措施正在加速環保烤箱技術的普及。人工智慧和物聯網功能的整合進一步提升了使用者體驗、烹飪精度和能源管理能力。然而,由於安裝和維護成本較高,在對成本較為敏感的市場,烤箱的普及可能仍然有限。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 555億美元 |

| 預計金額 | 1018億美元 |

| 複合年成長率 | 6.2% |

預計到2025年,住宅烤箱市場規模將達到466億美元,並在2035年之前以6.3%的複合年成長率成長。住宅烤箱市場的成長主要受快速都市化、家庭收入成長以及對先進廚房電器需求增加的驅動。消費者越來越傾向於選擇既能提供便利烹飪體驗又符合永續性概念的先進烤箱。節能型和多功能烤箱因其能夠透過一台設備處理多種烹飪方式而備受住宅青睞。智慧控制和Wi-Fi連接等技術進步也提升了使用者體驗,並推動了家用烤箱系統在全球的普及。

預計到2025年,電烤箱市佔率將達到62%,並在2026年至2035年間以6.4%的複合年成長率成長。消費者對便利、高效、多功能烹飪解決方案的偏好不斷成長,持續推動全球對電烤箱的需求。電烤箱因其穩定的加熱性能和支援多種烹飪功能(包括烘烤、燒烤和烘焙)而廣受歡迎。不斷擴展的智慧廚房生態系統以及物聯網技術在家用電器中日益普及,進一步促進了電烤箱在住宅和商用應用領域的成長。

美國烤箱市場佔全球80%的佔有率,預計2025年市場規模將達到138億美元。推動全美市場成長的因素包括消費者偏好的轉變、技術的快速創新以及節能家電的日益普及。隨著消費者越來越重視便利性、能源效率和最新的烹飪技術,家庭和商用場所對先進烤箱系統的需求都在增加。製造業的擴張和成熟的家電生產設施也促進了美國烤箱市場的持續發展。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 原物料供應商

- 製造商

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 供應鏈分析

- 原料和零件來源

- 製造和組裝基地

- 按應用分類的分銷管道

- 供應鏈風險和依賴性

- 區域供應鏈趨勢

- 成長潛力分析

- 2025年價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 產品類型和技術世代導致的價格波動

- 消費者價格敏感度分析

- 監理情勢

- 全球法規結構概述

- 歐洲 - CE 標誌、能源效率指令、ATEX 合規。

- 北美 - UL/CSA 標準、EPA排放氣體法規、能源之星

- 南美洲 - INMETRO(巴西),區域標準

- 亞太地區 - 各國特定標準(中國 GB、印度 BIS、日本 JIS)

- MEA-GCC標準、SASO(沙烏地阿拉伯)、區域協調

- 依申請方式符合合規要求

- 全球法規結構概述

- 波特的分析

- PESTLE分析

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 未來市場趨勢

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 按技術類型和產品類型的貿易趨勢

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 目前分銷基礎設施和通路滲透情況

- 按地區與業態(現代零售與傳統零售)分類的通路覆蓋率

- 缺乏最後一公里基礎設施和不斷變化的管道

- 消費者購買行為

- 購買模式

- 偏好分析

- 不同地區的消費者行為差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依應用領域分類,2022-2035年

- 工業烤箱

- 批量烤箱

- 連續烤箱

- 熱處理爐

- 無塵室烤箱

- 其他(例如,實驗室/研究用烘箱)

- 住宅烤箱

- 微波爐

- 嵌入式烤箱

- 桌上型/小型烤箱

第6章 市場估價與預測:依暖氣技術分類,2022-2035年

- 傳統烤箱

- 對流烤箱

- 組合式烤箱

- 蒸氣烤箱

- 微波技術

第7章 市場估算與預測:依燃料類型分類,2022-2035年

- 瓦斯烤箱

- 電烤箱

第8章 市場估算與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- 全球主要公司

- BSH Hausgerate

- Electrolux AB

- Haier Group

- LG Electronics

- Midea Group

- Samsung Electronics

- Whirlpool Corporation

- 當地公司

- Arcelik AS

- Bertazzoni

- Blodgett Oven Company

- Robam Appliances

- Smeg

- Sub-Zero Group

- Viking Range

- Emerging/Niche Specialist

- Baxter Manufacturing

- Despatch Industries

- Doyon Equipment

- Grieve Corporation

- UNOX

- Wisconsin Oven Corporation

- Wood Stone Corporation

The Global Oven Market was valued at USD 55.5 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 101.8 billion by 2035.

The oven industry is witnessing growth as consumers increasingly prefer advanced cooking appliances that combine convenience, energy efficiency, and modern functionality. Rising disposable incomes and growing interest in premium kitchen infrastructure are encouraging the adoption of technologically advanced ovens across residential and commercial sectors. Manufacturers are continuously introducing innovative features such as touch-enabled controls, wireless connectivity, and multifunctional cooking capabilities to meet changing consumer expectations. Increasing interest in home cooking and baking activities is also contributing significantly to market expansion, supported by evolving lifestyle preferences and greater awareness of smart kitchen technologies. Commercial establishments, including food service businesses and hospitality facilities, continue to generate strong demand for high-capacity and energy-efficient ovens to improve operational productivity. In addition, government initiatives promoting energy conservation and environmentally sustainable appliances are accelerating the adoption of eco-friendly oven technologies. The integration of AI and IoT-enabled functionalities is further enhancing user convenience, cooking precision, and energy management capabilities. However, high installation and maintenance expenses may continue to limit adoption in cost-sensitive markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $55.5 Billion |

| Forecast Value | $101.8 Billion |

| CAGR | 6.2% |

The residential ovens segment generated USD 46.6 billion in 2025 and is expected to grow at a CAGR of 6.3% throughout 2035. Market growth within the residential category is being fueled by rapid urbanization, increasing household incomes, and rising demand for modern kitchen appliances. Consumers are increasingly seeking advanced ovens that support convenient cooking experiences while aligning with sustainability preferences. Energy-efficient models and multifunctional ovens are gaining significant traction among homeowners due to their ability to support multiple cooking methods within a single appliance. Technological advancements, including smart controls and Wi-Fi-enabled functionality, are also improving user experience and encouraging wider adoption of residential oven systems globally.

The electric ovens segment accounted for 62% share in 2025 and is projected to grow at a CAGR of 6.4% from 2026 to 2035. Rising consumer preference for convenient, efficient, and versatile cooking solutions continues to drive demand for electric ovens worldwide. These ovens are widely favored for their consistent heating performance and ability to support various cooking functions, including roasting, grilling, and baking. Growing adoption of smart kitchen ecosystems and increasing integration of IoT-based technologies into electric appliances are further contributing to segment growth across residential and commercial applications.

United States Oven Market held 80% share, generating USD 13.8 billion in 2025. Market growth across the country is supported by evolving consumer preferences, rapid technological innovation, and increasing adoption of energy-efficient appliances. Demand for advanced oven systems is rising across both household and commercial environments as consumers prioritize convenience, energy savings, and modern cooking technologies. Expanding manufacturing activities and the presence of established appliance production facilities are also contributing to the continued development of the oven market throughout the United States.

Major companies operating in the Global Oven Market include BSH Hausgerate, Electrolux AB, Haier Group, LG Electronics, Midea Group, Samsung Electronics, Whirlpool Corporation, Arcelik A.S., Bertazzoni, Blodgett Oven Company, Robam Appliances, Smeg, Sub-Zero Group, Viking Range, Baxter Manufacturing, Despatch Industries, Doyon Equipment, Grieve Corporation, UNOX, Wisconsin Oven Corporation, and Wood Stone Corporation. Companies operating in the oven market are implementing various strategic initiatives to strengthen their market position and enhance competitive advantage. Leading manufacturers are investing heavily in research and development to introduce technologically advanced ovens featuring AI integration, smart connectivity, and improved energy efficiency. Businesses are also expanding product portfolios with multifunctional and eco-friendly appliances designed to meet evolving consumer preferences. Strategic partnerships, mergers, and collaborations with technology providers and retail channels are helping companies broaden their market reach and improve customer engagement. In addition, manufacturers are increasing investments in automation and smart manufacturing technologies to enhance production efficiency and product quality.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Application

- 2.2.3 Heating Technology

- 2.2.4 Fuel Type

- 2.2.5 Distribution Channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Manufacturers

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Market opportunities

- 3.3 Supply Chain Analysis

- 3.3.1 Raw material and component sources

- 3.3.2 Manufacturing and assembly locations

- 3.3.3 Distribution channels by application type

- 3.3.4 Supply chain risks and dependencies

- 3.3.5 Regional supply chain dynamics

- 3.4 Growth potential analysis

- 3.5 Pricing analysis, 2025 (driven by primary research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.5.3 Price variation by product type & technology generation

- 3.5.4 Consumer price sensitivity analysis

- 3.6 Regulatory landscape

- 3.6.1 Global regulatory framework overview

- 3.6.1.1 Europe - CE Marking, Energy Efficiency Directives, ATEX Compliance

- 3.6.1.2 North America - UL/CSA Standards, EPA Emissions, Energy Star

- 3.6.1.3 South America - INMETRO (Brazil), Regional Standards

- 3.6.1.4 APAC - Country-Specific Standards (China GB, India BIS, Japan JIS)

- 3.6.1.5 MEA - GCC Standards, SASO (Saudi), Regional Harmonization

- 3.6.2 Compliance requirements by application type

- 3.6.1 Global regulatory framework overview

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technological and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Future market trends

- 3.11 Trade data analysis (driven by paid database) (HS Code: 8516.60)

- 3.11.1 Import/export volume & value trends

- 3.11.2 Key trade corridors & tariff impact

- 3.11.3 Trade flow by technology type & product category

- 3.12 Impact of AI & generative ai on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.13.1 Channel coverage by region & format (modern vs. traditional trade)

- 3.13.2 Last-mile infrastructure gaps & emerging channel shifts

- 3.14 Consumer buying behaviour

- 3.14.1 Purchasing patterns

- 3.14.2 Preference analysis

- 3.14.3 Regional variations in consumer behaviour

- 3.14.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Application, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Industrial ovens

- 5.2.1 Batch ovens

- 5.2.2 Continuous process ovens

- 5.2.3 Heat-treating ovens

- 5.2.4 Cleanroom ovens

- 5.2.5 Others (laboratory & research ovens etc.)

- 5.3 Residential ovens

- 5.3.1 Range ovens

- 5.3.2 Wall ovens

- 5.3.3 Countertop/compact ovens

Chapter 6 Market Estimates & Forecast, By Heating Technology, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Conventional/traditional ovens

- 6.3 Convection ovens

- 6.4 Combination ovens

- 6.5 Steam ovens

- 6.6 Microwave technology

Chapter 7 Market Estimates & Forecast, By Fuel Type, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Gas ovens

- 7.3 Electric ovens

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 BSH Hausgerate

- 10.1.2 Electrolux AB

- 10.1.3 Haier Group

- 10.1.4 LG Electronics

- 10.1.5 Midea Group

- 10.1.6 Samsung Electronics

- 10.1.7 Whirlpool Corporation

- 10.2 Regional Players

- 10.2.1 Arcelik A.S.

- 10.2.2 Bertazzoni

- 10.2.3 Blodgett Oven Company

- 10.2.4 Robam Appliances

- 10.2.5 Smeg

- 10.2.6 Sub-Zero Group

- 10.2.7 Viking Range

- 10.3 Emerging/Niche Specialist

- 10.3.1 Baxter Manufacturing

- 10.3.2 Despatch Industries

- 10.3.3 Doyon Equipment

- 10.3.4 Grieve Corporation

- 10.3.5 UNOX

- 10.3.6 Wisconsin Oven Corporation

- 10.3.7 Wood Stone Corporation

高速烤箱全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球商用組合烤箱市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

高速烤箱全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球商用組合烤箱市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 商用組合式烤箱市場:按系統、控制方式、容量、最終用戶、應用和分銷管道分類-2026-2032年全球市場預測

商用組合式烤箱市場:按系統、控制方式、容量、最終用戶、應用和分銷管道分類-2026-2032年全球市場預測 真空烘箱市場報告:按產品類型、應用和地區分類(2026-2034 年)輸送機烤箱市場規模、佔有率、趨勢和預測:按類型、技術、動力來源、分銷管道、最終用途和地區分類,2026-2034年輸送機烘箱市場:依技術、運作模式、溫度範圍、輸送帶材質及應用分類-2026-2032年全球市場預測電動旋轉烤箱市場按產品類型、價格範圍、功率等級、最終用戶和分銷管道分類-全球預測,2026-2032年

真空烘箱市場報告:按產品類型、應用和地區分類(2026-2034 年)輸送機烤箱市場規模、佔有率、趨勢和預測:按類型、技術、動力來源、分銷管道、最終用途和地區分類,2026-2034年輸送機烘箱市場:依技術、運作模式、溫度範圍、輸送帶材質及應用分類-2026-2032年全球市場預測電動旋轉烤箱市場按產品類型、價格範圍、功率等級、最終用戶和分銷管道分類-全球預測,2026-2032年 商用組合烤箱市場規模、佔有率和成長分析(按類型、操作方式、應用、最終用戶和地區分類)—2026-2033年產業預測小型真空乾燥機市場按類型、技術、溫度範圍、銷售管道、應用和最終用戶分類,全球預測(2026-2032年)電池真空乾燥箱市場按類型、熱源、技術、容量和最終用途產業分類-2026-2032年全球預測

商用組合烤箱市場規模、佔有率和成長分析(按類型、操作方式、應用、最終用戶和地區分類)—2026-2033年產業預測小型真空乾燥機市場按類型、技術、溫度範圍、銷售管道、應用和最終用戶分類,全球預測(2026-2032年)電池真空乾燥箱市場按類型、熱源、技術、容量和最終用途產業分類-2026-2032年全球預測