|

市場調查報告書

商品編碼

2045841

動脈粥狀硬化斑塊切除術器械市場機會、成長要素、產業趨勢分析及2026-2035年預測Atherectomy Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

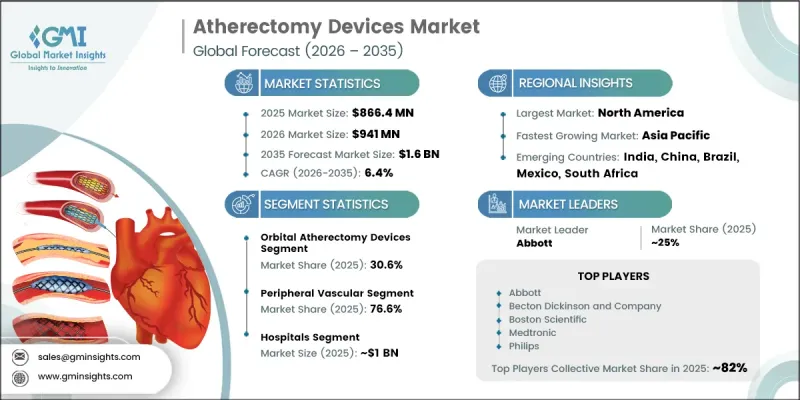

預計到 2025 年,全球動脈粥狀硬化斑塊切除術器械市場價值將達到 8.664 億美元,年複合成長率為 6.4%,到 2035 年將達到 16 億美元。

市場擴張的促進因素包括周邊動脈疾病動脈疾病和冠狀動脈疾病發生率的上升,以及全球人口老化、肥胖和糖尿病病例的增加。生活方式的改變,例如體力活動減少和不健康的飲食習慣,也加劇了心血管疾病的負擔,從而增加了對微創血管治療方案的需求。動脈粥狀硬化斑塊切除術裝置因其能夠有效清除斑塊並最大限度地減少侵入性手術的需求而廣泛應用。介入性心臟病學技術的不斷進步,以及醫生對精準血管治療日益成長的偏好,進一步推動了產品的普及。此外,醫療機構越來越注重以病人為中心的治療方案,以縮短住院時間和復健期。越來越多的臨床證據支持先進動脈粥狀硬化斑塊切除術系統的安全性和有效性,以及產品核可的增加,進一步增強了全球動脈粥狀硬化斑塊切除術裝置產業的正面前景。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 8.664億美元 |

| 預計金額 | 16億美元 |

| 複合年成長率 | 6.4% |

動脈動脈粥狀硬化斑塊切除術裝置是一種專門用於清除血管疾病患者動脈內斑塊積聚的醫療設備,旨在恢復健康的血液循環。這些系統透過多種先進機制運行,包括研磨、刮削、切割和雷射斑塊清除技術,使醫生無需開胸手術即可疏通阻塞的血管。微創介入心臟病學需求的不斷成長,正在加速醫院和專科醫療機構對這些裝置的需求。醫療基礎設施投資的增加和導管技術的創新也推動了這些裝置的普及。此外,醫療保健系統日益重視血管疾病的早期診斷和及時治療,預計將為動脈動脈粥狀硬化斑塊切除術裝置市場帶來長期成長機會。手術效率的提高、病患併發症的減少以及治療效果的改善,不斷鞏固了動脈粥狀硬化斑塊切除術解決方案作為現代心血管醫學重要組成部分的地位。

預計2025年,軌道式動脈粥狀硬化斑塊切除術器械市佔率將達到30.6%,2035年將達到4.958億美元,預測期內複合年成長率(CAGR)為6.3%。此品類的強勁成長主要歸功於軌道式動脈粥狀硬化斑塊切除術系統能夠實現可控且均勻的斑塊清除,尤其是在複雜鈣化病灶中。這些器械採用先進的旋轉冠狀技術,可在保護周圍動脈結構的同時,精準地清除硬化斑塊,在冠狀動脈和周邊血管手術中均展現出極高的療效。臨床醫師對精準斑塊清除技術的日益青睞也進一步推動了該品類的成長。器械柔軟性、導航精度和手術安全性方面的技術進步也加速了其在醫療機構中的應用。

預計到2025年,周邊血管領域將佔據76.6%的市場佔有率,繼續保持主導在動脈動脈粥狀硬化斑塊切除術器械市場的領先地位。全球周邊動脈疾病(PAD)負擔的不斷加重,持續推動著對高效血管成形術和斑塊管理技術的巨大需求。吸菸、糖尿病、肥胖和老齡化等因素導致血管併發症發生率上升,進一步加劇了PAD的盛行率,從而推動了市場擴張。動脈粥狀硬化斑塊切除術術在周邊血管治療中日益重要,因為它能夠改善血流,減輕動脈阻塞的嚴重程度。此外,這些器械因其微創治療、恢復時間短、患者預後好等優點,也備受醫師青睞。

預計2025年,北美動脈動脈粥狀硬化斑塊切除術器械市佔率將達到58.8%。該地區對先進心血管治療技術的需求仍然強勁,尤其是在美國,周邊動脈疾病疾病和冠狀動脈疾病的發生率仍然很高。肥胖、糖尿病和久坐不動的生活方式導致需要血管介入治療的患者人數不斷增加。該地區受益於高度發展的醫療基礎設施、健全的保險報銷體係以及創新醫療技術的快速普及。北美各地的醫療機構擴大採用微創手術來提高治療效率和患者復原效果。此外,對心血管研究投入的增加、先進介入治療的普及以及人們對血管疾病管理意識的提高,都將繼續推動區域市場的成長。

目錄

第1章:調查方法

第2章執行摘要

第3章:行業洞察

- 工業生態系分析

- 影響產業的因素

- 促進因素

- 人們越來越傾向微創手術

- 擴大目標患者群

- 動脈粥狀硬化斑塊切除術裝置的技術進步

- 周邊動脈疾病(PAD)盛行率增加

- 產業潛在風險與挑戰

- 醫療設備及相關手術高成本

- 學習曲線陡峭,且依賴服務提供者。

- 市場機遇

- 新興市場的地域擴張

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術展望

- 最新科技趨勢

- 新技術

- 價格分析

- 未來市場趨勢

- 波特的分析

- PESTLE分析

- 人工智慧和生成式人工智慧對市場的影響

- 價值鏈分析

- 客戶洞察

- 創業場景

- 投資與資金籌措分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 軌道動脈動脈粥狀硬化斑塊切除術裝置

- 雷射動脈動脈粥狀硬化斑塊切除術裝置

- 定向斑塊動脈粥狀硬化斑塊切除術裝置

- 旋轉式動脈粥狀硬化斑塊切除術裝置

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 周邊血管應用

- 冠狀動脈的使用

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 醫院

- 門診手術中心

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Abbott

- angiodynamics

- AVINGER

- Becton Dickinson and Company

- Boston Scientific

- Cardio Flow

- Medtronic

- MicroPort

- Nipro

- Philips

- Ra Medical Systems

- Rex Medical

The Global Atherectomy Devices Market was valued at USD 866.4 million in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 1.6 billion by 2035.

Market expansion is fueled by the increasing incidence of peripheral artery disease and coronary artery disease, along with the rising global elderly population and growing cases of obesity and diabetes. Changing lifestyles, including reduced physical activity and unhealthy dietary patterns, are also contributing to the increasing burden of cardiovascular disorders, thereby strengthening demand for minimally invasive vascular treatment solutions. Atherectomy devices are gaining wider acceptance because they support effective plaque removal while minimizing the need for invasive surgical procedures. Continuous technological advancements in interventional cardiology, combined with increasing physician preference for precision-based vascular treatments, are further supporting product adoption. In addition, healthcare providers are increasingly focusing on patient-centered procedures that reduce hospital stays and recovery time. Rising clinical evidence validating the safety and performance of advanced atherectomy systems, along with a growing number of product approvals, continues to reinforce the positive outlook for the global atherectomy devices industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $866.4 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 6.4% |

Atherectomy devices are specialized medical instruments designed to eliminate plaque accumulation from arteries and restore healthy blood circulation in patients diagnosed with vascular disorders. These systems operate through several advanced mechanisms, including sanding, shaving, cutting, and laser-based plaque removal technologies, allowing physicians to address blocked vessels without open surgery. Growing preference for minimally invasive cardiovascular interventions is accelerating demand for these devices across hospitals and specialty care facilities. Increasing investments in healthcare infrastructure and innovation in catheter-based technologies are also encouraging broader adoption. Furthermore, healthcare systems are prioritizing early diagnosis and timely treatment of vascular diseases, which is expected to create long-term growth opportunities for the atherectomy devices market. Enhanced procedural efficiency, reduced patient complications, and improved treatment outcomes continue to position atherectomy solutions as a critical component of modern cardiovascular care.

The orbital atherectomy devices segment accounted for a share of 30.6% in 2025 and is anticipated to reach USD 495.8 million by 2035, expanding at a CAGR of 6.3% over the forecast period. Strong growth within this category is largely linked to the ability of orbital atherectomy systems to deliver controlled and uniform plaque modification, particularly in complex calcified lesions. These devices utilize advanced rotating crown technology that carefully sands hardened plaque while preserving the surrounding arterial structure, making them highly effective in both coronary and peripheral vascular procedures. Increasing preference among clinicians for precision-driven plaque removal techniques is further supporting segment growth. Technological improvements in device flexibility, navigation accuracy, and procedural safety are also encouraging adoption across healthcare facilities.

The peripheral vascular segment captured a share of 76.6% in 2025, maintaining its leading position within the atherectomy devices market. The growing global burden of peripheral artery disease continues to create significant demand for effective vessel preparation and plaque management technologies. Increasing rates of smoking, diabetes, obesity, and aging-related vascular complications are contributing to the rising prevalence of PAD, thereby supporting market expansion. Atherectomy procedures are becoming increasingly important in peripheral vascular treatments due to their ability to improve blood flow and reduce the severity of arterial blockages. Physicians are also favoring these devices because they offer minimally invasive treatment options with shorter recovery periods and improved patient outcomes.

North America Atherectomy Devices Market held a share of 58.8% in 2025. The region continues to experience strong demand for advanced cardiovascular treatment technologies, particularly in the United States, where cases of peripheral artery disease and coronary artery disease remain high. The increasing prevalence of obesity, diabetes, and sedentary lifestyles has contributed to the growing patient population requiring vascular interventions. The region benefits from a highly developed healthcare infrastructure, strong reimbursement systems, and rapid adoption of innovative medical technologies. Healthcare providers across North America are increasingly utilizing minimally invasive procedures to improve treatment efficiency and patient recovery outcomes. In addition, growing investments in cardiovascular research, expanding access to advanced interventional care, and rising awareness regarding vascular disease management continue to reinforce regional market growth.

Key companies operating in the Global Atherectomy Devices Market include Abbott, Medtronic, Boston Scientific, Philips, Becton Dickinson and Company, AVINGER, MicroPort, Nipro, Angiodynamics, Ra Medical Systems, Rex Medical, and Cardio Flow. These companies are actively focusing on product innovation, strategic partnerships, and expansion of their cardiovascular treatment portfolios to strengthen their market presence and improve competitive positioning within the global atherectomy devices industry. Companies operating in the atherectomy devices market are increasingly adopting strategic initiatives focused on innovation, geographic expansion, and portfolio diversification to strengthen their competitive position. Major industry participants are investing heavily in research and development activities to introduce technologically advanced devices with improved precision, safety, and procedural efficiency. Partnerships with hospitals, cardiovascular centers, and healthcare providers are helping companies expand product accessibility and improve physician adoption rates. Many manufacturers are also focusing on regulatory approvals and clinical trials to validate product performance and accelerate commercialization opportunities. In addition, businesses are expanding their distribution networks across emerging economies to capture growing demand for minimally invasive vascular treatments.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in preference for minimally invasive procedures

- 3.2.1.2 Growing target patient population

- 3.2.1.3 Technological advancements in atherectomy devices

- 3.2.1.4 Rising prevalence of peripheral arterial diseases (PAD)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and associated procedures

- 3.2.2.2 Steep learning curve and operator dependency

- 3.2.3 Market opportunities

- 3.2.3.1 Geographic expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by primary research)

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.11 Value chain analysis

- 3.12 Customer insights (Driven by primary research)

- 3.13 Start-up scenarios

- 3.14 Investment & funding analysis (Driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Products, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Orbital atherectomy devices

- 5.3 Laser atherectomy devices

- 5.4 Directional atherectomy devices

- 5.5 Rotational atherectomy devices

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Peripheral vascular applications

- 6.3 Coronary applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 angiodynamics

- 9.3 AVINGER

- 9.4 Becton Dickinson and Company

- 9.5 Boston Scientific

- 9.6 Cardio Flow

- 9.7 Medtronic

- 9.8 MicroPort

- 9.9 Nipro

- 9.10 Philips

- 9.11 Ra Medical Systems

- 9.12 Rex Medical

動脈粥狀硬化斑塊切除術器械市場:全球市場預測,2026-2032年

動脈粥狀硬化斑塊切除術器械市場:全球市場預測,2026-2032年 動脈粥狀硬化斑塊切除術器械市場:按器械類型、應用、最終用戶和地區分類

動脈粥狀硬化斑塊切除術器械市場:按器械類型、應用、最終用戶和地區分類 AsetoMe設備市場規模、佔有率和成長分析:按設備類型、應用、最終用戶、材料和地區分類-2026年至2033年產業預測

AsetoMe設備市場規模、佔有率和成長分析:按設備類型、應用、最終用戶、材料和地區分類-2026年至2033年產業預測 動脈動脈粥狀硬化斑塊切除術器械市場報告:按產品應用、最終用戶和地區分類(2026-2034 年)

動脈動脈粥狀硬化斑塊切除術器械市場報告:按產品應用、最終用戶和地區分類(2026-2034 年) 全球動脈動脈粥狀硬化斑塊切除術器械市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球動脈動脈粥狀硬化斑塊切除術器械市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 斑塊改良設備市場:市場洞察、競爭格局及市場預測(至2034年)

斑塊改良設備市場:市場洞察、競爭格局及市場預測(至2034年) 2026年全球冠狀動脈動脈粥狀硬化斑塊切除術器械市場報告2026年全球動脈粥狀硬化斑塊切除術器械市場報告2026年全球斑塊改良設備市場報告2026年全球雷射動脈動脈粥狀硬化斑塊切除術設備市場報告

2026年全球冠狀動脈動脈粥狀硬化斑塊切除術器械市場報告2026年全球動脈粥狀硬化斑塊切除術器械市場報告2026年全球斑塊改良設備市場報告2026年全球雷射動脈動脈粥狀硬化斑塊切除術設備市場報告