|

市場調查報告書

商品編碼

2045810

咖啡機市場機會、成長要素、產業趨勢分析及2026-2035年預測。Coffee Machines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

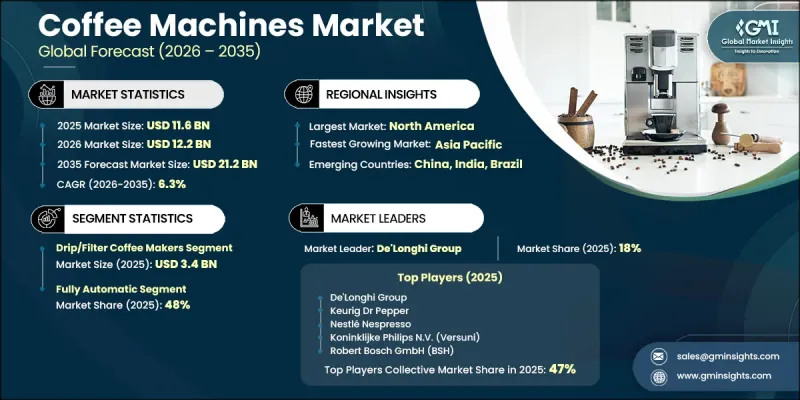

預計到 2025 年,全球咖啡機市場價值將達到 116 億美元,並以 6.3% 的複合年成長率成長,到 2035 年將達到 212 億美元。

隨著消費者生活方式的改變、咖啡文化的興起以及對高品質咖啡體驗日益成長的偏好,咖啡機產業正穩步發展,並持續改變全球消費者的購買行為。咖啡消費不再只是一項日常活動;如今,消費者將沖泡咖啡與舒適、便利、個人化和提升生活品質連結起來。這種轉變推動了對技術先進的咖啡機的需求,這些咖啡機能夠在從住宅到商業場所的各種環境中提供專業品質的飲料。都市化的加快、人們生活節奏的加快以及可支配收入的增加,進一步促進了緊湊型、自動化和節能型咖啡機的普及。在辦公室、餐廳、咖啡館和飯店等商業場所,咖啡機正日益成為提升客戶服務和員工便利性的必備解決方案。製造商也致力於永續發展,開發使用可回收零件、降低能耗和減少廢棄物的咖啡機。此外,消費者對可自訂沖泡設定、奶泡表單功能和智慧連接功能的日益成長的偏好,也持續加速全球咖啡機市場的創新。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 116億美元 |

| 預計金額 | 212億美元 |

| 複合年成長率 | 6.3% |

預計到2025年,滴濾式咖啡機的市場規模將達到34億美元。由於消費者持續青睞實用、可靠且易於操作的日常沖泡系統,此類咖啡機的需求仍然強勁。其受歡迎的原因在於功能簡單、經濟實惠,並且一次即可沖泡多杯咖啡。在住宅、職場和餐飲業,滴濾式咖啡機因其易用性和穩定的沖泡性能而備受青睞。製造商也不斷提升這些咖啡機的功能,以滿足現代消費者的需求,例如增加可編程功能、緊湊型設計、溫度控制系統和節能功能。隨著住宅和商業場所對便利咖啡沖泡解決方案的需求不斷成長,預計在預測期內,滴漏式咖啡機的需求將進一步擴大。

預計到2025年,全自動咖啡機市佔率將達到48%。隨著消費者越來越重視便利性、速度、精準度和穩定的飲品品質,全自動咖啡機持續獲得強勁支持。這些系統透過自動化研磨、沖泡、奶泡和清潔等功能,簡化了整個沖泡流程,最大限度地減少了手動操作。消費者對家庭高品質咖啡體驗的需求不斷成長,加上商業性食品服務的擴張,正顯著加速全自動咖啡機的普及。企業正加大對這類機器的投資,以提高營運效率、維持穩定的飲品品質並提升顧客滿意度。觸控螢幕介面、個人化沖泡方案、應用程式控制和智慧維護提醒等產品的不斷進步,進一步推動了市場需求。此外,辦公室、飯店和零售店對高階咖啡解決方案的偏好日益成長,預計也將支撐該細分市場的長期成長。

北美咖啡機市場佔74%的佔有率,預計2025年市場規模將達26億美元。全部區域根深蒂固的濃厚咖啡文化持續推動住宅和商用對先進咖啡機的穩定需求。北美消費者越來越傾向選擇兼具便利性、耐用性、易於維護性和高品質飲品的咖啡機。專門食品咖啡飲品的日益普及、在家工作的興起以及飯店基礎設施投資的增加,都促進了市場的擴張。在商業領域,高性能咖啡系統被優先考慮,以提升客戶體驗和營運效率。此外,技術創新、人們對永續家用電器的日益關注以及智慧咖啡機的普及,也進一步推動了美國和北美咖啡機產業的成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章:行業洞察

- 工業生態系分析

- 供應商情況

- 利潤率分析

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 按最終用途

- 住宅

- 商業的

- 按最終用途

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新技術

- 價格分析

- 對過去價格趨勢的分析

- 定價策略:按業務類型分類

- 監理情勢

- 標準和合規要求

- 區域監理框架

- 認證標準

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 基於分段的生成式人工智慧的應用案例和實施藍圖

- 風險、限制和監管考量

- 貿易分析

- 十大出口國

- 十大進口國

- 主要貿易路線及關稅的影響

- 生產能力和生產情況

- 按地區和主要生產商分類的已安裝產能

- 運轉率和擴張計劃

- 波特的分析

- PESTLE分析

- 消費行為分析

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務對購買決策的影響

- 各細分市場的市場動態

- 商用和傳統義濃縮咖啡的市場展望

- 產消者市場的市場動態

- 商業領域的成長軌跡

- 住宅與商業需求比較

- 製造商業績和銷售趨勢

- 全球生產商的銷售趨勢

- 按製造商規模分類的銷售成長

- 市佔率波動與產業結構調整趨勢

- 生產量區域趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 濃縮咖啡機

- 傳統/手動義濃縮咖啡機

- 半自動義式濃縮咖啡

- 全自動義式濃縮咖啡

- 面向濃縮咖啡的濃縮咖啡

- 滴漏式咖啡機

- 單份/膠囊式機器

- 從咖啡豆到咖啡的一體機

- 其他(法式濾壓壺、摩卡壺、滲濾壺、手沖咖啡器具)

第6章 市場估計與預測:依技術分類,2022-2035年

- 手動的

- 半自動

- 全自動/超自動

- 智慧/互聯

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 手動的

- 住宅

- 入門級/普通家庭用戶

- 產消者/愛好者

- 商業的

- 專門食品咖啡與飯店服務

- 適用於機構及一般餐飲服務業

- 住宅

- 半自動

- 住宅

- 入門級/普通家庭用戶

- 產消者/愛好者

- 商業的

- 專門食品咖啡與飯店服務

- 機構及一般餐飲服務業

- 住宅

- 全自動/超自動

- 住宅

- 入門級/普通家庭用戶

- 產消者/愛好者

- 商業的

- 專門食品咖啡與飯店服務

- 機構及一般餐飲服務業

- 住宅

- 智慧/互聯

- 住宅

- 入門級/普通家庭用戶

- 產消者/愛好者

- 商業的

- 專門食品咖啡與飯店服務

- 機構及一般餐飲服務業

- 住宅

第8章 市場估算與預測:依價格區間分類,2022-2035年

- 價格低廉(低於200美元)

- 中價位(200-1000美元)

- 高價位(超過1000美元)

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 住宅

- 入門級/普通家庭用戶

- 產消者/愛好者

- 商業的

- 專門食品咖啡與飯店服務

- 適用於機構及一般餐飲服務業

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 企業網站

- 離線

- 專門食品咖啡設備商店

- 零售/大型超市

- 直接B2B(製造商對企業買家)

- 其他(獨立零售商)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第12章:公司簡介

- 全球主要公司

- De'Longhi Group

- Keurig Dr Pepper

- Nestle Nespresso SA

- Koninklijke Philips NV

- Robert Bosch GmbH

- Groupe SEB

- Panasonic Corporation

- 該地區的領先企業

- La Cimbali(Gruppo Cimbali SpA)

- Nuova Simonelli

- Rancilio Group

- JURA Elektroapparate AG

- WMF Group

- Hamilton Beach Brands, Inc.

- BUNN(Bunn-O-Matic Corporation)

- Niche/Specialist Players

- Rocket Espresso Milano

- Victoria Arduino

- Bezzera Srl

- Eversys SA

- Thermoplan AG

- Franke Coffee Systems

- Breville Group

The Global Coffee Machines Market was valued at USD 11.6 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 21.2 billion by 2035.

The coffee machines industry is evolving steadily as changing consumer lifestyles, growing cafe culture, and increasing preference for premium coffee experiences continue to reshape purchasing behavior worldwide. Coffee consumption is no longer limited to a routine activity, as consumers now associate coffee preparation with comfort, convenience, personalization, and lifestyle enhancement. This shift has increased demand for technologically advanced coffee machines that can deliver professional-quality beverages across residential and commercial environments. Rising urbanization, fast-paced schedules, and increasing disposable income levels are further supporting the adoption of compact, automated, and energy-efficient coffee machines. In commercial spaces including offices, restaurants, cafes, and hotels, coffee machines are increasingly viewed as essential customer service and employee convenience solutions. Manufacturers are also focusing on sustainability initiatives by developing machines with recyclable components, lower energy consumption, and reduced waste generation. In addition, increasing consumer preference for customizable brewing settings, milk frothing options, and smart connectivity features continues to accelerate innovation across the global coffee machines market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.6 Billion |

| Forecast Value | $21.2 Billion |

| CAGR | 6.3% |

The drip and filter coffee maker segment accounted for USD 3.4 billion in 2025. Demand for these machines remains strong because consumers continue to favor practical, reliable, and easy-to-operate brewing systems suitable for everyday use. Their popularity is supported by straightforward functionality, cost efficiency, and the ability to prepare multiple servings in a single cycle. Residential consumers, workplaces, and hospitality establishments continue to prefer drip coffee systems due to their operational simplicity and consistent brewing performance. Manufacturers are also enhancing these machines with programmable features, compact designs, temperature control systems, and energy-saving capabilities to align with modern consumer expectations. The growing preference for convenient coffee preparation solutions across households and commercial establishments is expected to further strengthen demand for drip and filter coffee machines over the forecast period.

The fully automatic segment held a share of 48% in 2025. Fully automatic coffee machines continue to gain substantial traction as consumers increasingly prioritize convenience, speed, precision, and consistent beverage quality. These systems simplify the entire brewing process by automating grinding, brewing, milk frothing, and cleaning functions with minimal manual involvement. The growing demand for premium coffee experiences at home, combined with the expansion of commercial foodservice operations, has significantly accelerated the adoption of fully automatic systems. Businesses are increasingly investing in these machines to improve operational efficiency, maintain beverage consistency, and enhance customer satisfaction. Continuous product advancements, including touch-screen interfaces, personalized brewing profiles, app-based controls, and intelligent maintenance alerts, are further elevating product demand. In addition, the rising preference for sophisticated coffee solutions in offices, hotels, and retail establishments is expected to support long-term segment growth.

North America Coffee Machines Market held a 74% share, generating USD 2.6 billion in 2025. The strong coffee culture across the region continues to drive consistent demand for advanced brewing equipment in both residential and commercial settings. Consumers across North America increasingly prefer coffee machines that combine convenience, durability, ease of maintenance, and premium beverage quality. Growing adoption of specialty coffee beverages, increasing work-from-home trends, and rising investments in hospitality infrastructure are contributing to market expansion. Commercial establishments are also prioritizing high-performance coffee systems to improve customer experiences and operational productivity. Additionally, technological innovation, growing awareness regarding sustainable appliances, and the increasing availability of smart coffee machines are further supporting industry growth across the U.S. and the broader North American region.

Key participants operating in the Global Coffee Machines Market include De'Longhi Group, Panasonic Corporation, Groupe SEB, BUNN, Nuova Simonelli, Breville Group, Nestle Nespresso S.A., Robert Bosch GmbH, Thermoplan AG, WMF Group, Rocket Espresso Milano, Rancilio Group, Hamilton Beach Brands, Inc., Franke Coffee Systems, Victoria Arduino, Keurig Dr Pepper, Koninklijke Philips N.V., JURA Elektroapparate AG, Bezzera S.r.l., La Cimbali, and Eversys S.A. Companies operating in the coffee machines market are adopting multiple strategies to strengthen their market position and expand their customer base globally. Manufacturers are heavily investing in product innovation focused on automation, smart connectivity, energy efficiency, and personalized brewing technologies to enhance user experience and differentiate their offerings. Strategic partnerships with hospitality chains, offices, cafes, and retail distributors are helping companies increase product visibility and strengthen distribution networks. Many brands are also introducing sustainable coffee machines featuring recyclable materials, low-energy operations, and reduced waste systems to align with environmental goals and changing consumer preferences.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type trends

- 2.2.3 Technology trends

- 2.2.4 Price range trends

- 2.2.5 End use trends

- 2.2.6 Distribution channel trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Growth potential analysis

- 3.3.1 By End Use

- 3.3.1.1 Residential

- 3.3.1.2 Commercial

- 3.3.1 By End Use

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (driven by primary research)

- 3.6.2 Pricing strategy by player type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Impact of AI and generative AI on the market

- 3.8.1 AI driven disruption of existing business models

- 3.8.2 Generative AI use cases and adoption roadmap by segment

- 3.8.3 Risks, limitations, and regulatory considerations

- 3.9 Trade analysis (driven by paid database) (HS Code: 85167100)

- 3.9.1 Top 10 export countries

- 3.9.2 Top 10 import countries

- 3.9.3 Key trade corridors and tariff impact

- 3.10 Capacity and production landscape (driven by primary research)

- 3.10.1 Installed manufacturing capacity by region and key producer (driven by primary research)

- 3.10.2 Capacity utilization rates and expansion pipelines (driven by primary research)

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Consumer behavior analysis

- 3.13.1 Purchasing patterns

- 3.13.2 Preference analysis

- 3.13.3 Regional variations in consumer behavior

- 3.13.4 Impact of e-commerce on buying decisions

- 3.14 Segment-Specific Market Dynamics

- 3.14.1 Professional & Traditional Espresso Market Outlook

- 3.14.2 Prosumer Market Dynamics

- 3.14.3 Commercial Segment Growth Trajectory

- 3.14.4 Residential vs. Commercial Demand Comparison

- 3.15 Manufacturer Performance & Sales Trends

- 3.15.1 Global Producer Revenue Trends

- 3.15.2 Sales Growth by Manufacturer Tier

- 3.15.3 Market Share Shifts & Consolidation Trends

- 3.15.4 Production Volume Trends by Region

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Espresso Machines

- 5.2.1 Traditional/Manual Espresso

- 5.2.2 Semi-Automatic Espresso

- 5.2.3 Super-Automatic Espresso

- 5.2.4 Prosumer Espresso

- 5.3 Drip/Filter Coffee Makers

- 5.4 Single-Serve/Capsule Machines

- 5.5 Bean-to-Cup Machines

- 5.6 Others (French press, Moka pot, percolators, pour-over systems)

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-Automatic

- 6.4 Fully Automatic/Super-Automatic

- 6.5 Smart/Connected

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.2.1 Residential

- 7.2.1.1 Entry-Level/Mainstream Home Users

- 7.2.1.2 Prosumer/Enthusiast

- 7.2.2 Commercial

- 7.2.2.1 Specialty Coffee & Hospitality

- 7.2.2.2 Institutional & General Foodservice

- 7.2.1 Residential

- 7.3 Semi-Automatic

- 7.3.1 Residential

- 7.3.1.1 Entry-Level/Mainstream Home Users

- 7.3.1.2 Prosumer/Enthusiast

- 7.3.2 Commercial

- 7.3.2.1 Specialty Coffee & Hospitality

- 7.3.2.2 Institutional & General Foodservice

- 7.3.1 Residential

- 7.4 Fully Automatic/Super-Automatic

- 7.4.1 Residential

- 7.4.1.1 Entry-Level/Mainstream Home Users

- 7.4.1.2 Prosumer/Enthusiast

- 7.4.2 Commercial

- 7.4.2.1 Specialty Coffee & Hospitality

- 7.4.2.2 Institutional & General Foodservice

- 7.4.1 Residential

- 7.5 Smart/Connected

- 7.5.1 Residential

- 7.5.1.1 Entry-Level/Mainstream Home Users

- 7.5.1.2 Prosumer/Enthusiast

- 7.5.2 Commercial

- 7.5.2.1 Specialty Coffee & Hospitality

- 7.5.2.2 Institutional & General Foodservice

- 7.5.1 Residential

Chapter 8 Market Estimates & Forecast, By Price range, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Low (<$200)

- 8.3 Medium ($200-$1,000)

- 8.4 High (>$1,000)

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.2.1 Entry-Level/Mainstream Home Users

- 9.2.2 Prosumer/Enthusiast

- 9.3 Commercial

- 9.3.1 Specialty Coffee & Hospitality

- 9.3.2 Institutional & General Foodservice

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce

- 10.2.2 Company website

- 10.3 Offline

- 10.3.1 Specialty coffee equipment stores

- 10.3.2 Retail/Mega stores

- 10.3.3 Direct B2B (manufacturer to commercial buyers)

- 10.3.4 Others (independent retailers)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 De'Longhi Group

- 12.1.2 Keurig Dr Pepper

- 12.1.3 Nestle Nespresso S.A.

- 12.1.4 Koninklijke Philips N.V.

- 12.1.5 Robert Bosch GmbH

- 12.1.6 Groupe SEB

- 12.1.7 Panasonic Corporation

- 12.2 Regional Champions

- 12.2.1 La Cimbali (Gruppo Cimbali S.p.A.)

- 12.2.2 Nuova Simonelli

- 12.2.3 Rancilio Group

- 12.2.4 JURA Elektroapparate AG

- 12.2.5 WMF Group

- 12.2.6 Hamilton Beach Brands, Inc.

- 12.2.7 BUNN (Bunn-O-Matic Corporation)

- 12.3 Niche / Specialist Players

- 12.3.1 Rocket Espresso Milano

- 12.3.2 Victoria Arduino

- 12.3.3 Bezzera S.r.l.

- 12.3.4 Eversys S.A.

- 12.3.5 Thermoplan AG

- 12.3.6 Franke Coffee Systems

- 12.3.7 Breville Group

全球冷萃咖啡機市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球冷萃咖啡機市場規模、佔有率、趨勢和成長分析報告(2026-2034) 滴濾咖啡機市場商機、成長要素、產業趨勢分析及2026-2035年預測。冷萃咖啡機市場機會、成長要素、產業趨勢分析及2026-2035年預測

滴濾咖啡機市場商機、成長要素、產業趨勢分析及2026-2035年預測。冷萃咖啡機市場機會、成長要素、產業趨勢分析及2026-2035年預測 滴濾咖啡機市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、應用、分銷管道、地區和競爭對手分類,2021-2031年茶葉加工機械市場:商機、成長要素、產業趨勢分析及2026-2035年預測

滴濾咖啡機市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、應用、分銷管道、地區和競爭對手分類,2021-2031年茶葉加工機械市場:商機、成長要素、產業趨勢分析及2026-2035年預測 咖啡機市場:依產品類型、技術、應用、銷售管道和地區分類

咖啡機市場:依產品類型、技術、應用、銷售管道和地區分類 咖啡機市場:按產品類型、最終用戶和分銷管道分類的全球市場預測,2026-2032年咖啡機市場:按技術、分銷管道和最終用戶分類-2026-2032年全球預測從豆到杯:咖啡機市場按類型、材質、沖泡系統、最終用戶和銷售管道分類-2026-2032年全球預測

咖啡機市場:按產品類型、最終用戶和分銷管道分類的全球市場預測,2026-2032年咖啡機市場:按技術、分銷管道和最終用戶分類-2026-2032年全球預測從豆到杯:咖啡機市場按類型、材質、沖泡系統、最終用戶和銷售管道分類-2026-2032年全球預測 全球商用自動滴濾咖啡機市場:按產品類型、容量、分銷管道、技術、最終用途、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032)

全球商用自動滴濾咖啡機市場:按產品類型、容量、分銷管道、技術、最終用途、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032)