|

市場調查報告書

商品編碼

2045773

機器人吸塵器市場機會、成長要素、產業趨勢分析及2026-2035年預測Robotic Vacuum Cleaner Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

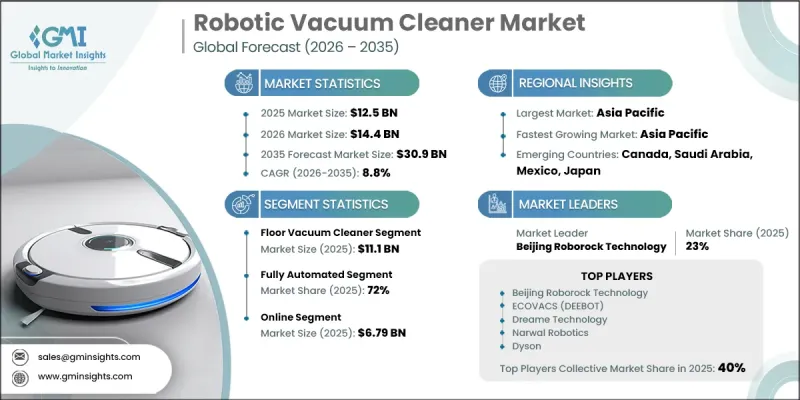

全球機器人吸塵器市場預計到 2025 年將價值 125 億美元,預計到 2035 年將以 8.8% 的複合年成長率成長至 309 億美元。

人們對室內清潔、更健康的居住環境和更佳空氣品質的日益重視是推動市場成長的主要動力。消費者擴大選擇使用掃地機器人來減少住宅中的灰塵、過敏原、寵物毛髮和空氣中的顆粒物,尤其是在通風條件住宅的人口密集都市區。配備高效能空氣微粒過濾器(HEPA)系統、增強吸力和自動清潔程序的先進掃地機器人越來越受歡迎,因為它們能讓使用者輕鬆保持所有地板的清潔。近年來,消費者對家居衛生的意識發生了顯著變化,他們更注重預防性和日常清潔,而不是偶爾的深度清潔。掃地機器人透過提供非接觸式清潔操作和定期維護,幫助人們最大限度地減少接觸灰塵和碎屑,從而順應了這一趨勢。隨著智慧家庭在全球的普及,掃地機器人不僅被視為便利的家用電器,更被視為對生活方式和健康的長期投資。導航系統、人工智慧地圖繪製、障礙物偵測和智慧連結等方面的技術進步,進一步增強了全球住宅市場對掃地機器人的需求。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 125億美元 |

| 預測市場規模 | 309億美元 |

| 複合年成長率 | 8.8% |

預計到2025年,地板吸塵器市場規模將達到111億美元。消費者對高效且便利的地板清潔解決方案的需求持續成長,涵蓋各種地板材料,包括硬木地板、瓷磚和地毯。儘管傳統吸塵器因其價格實惠和清潔性能出色而仍然被廣泛使用,但隨著都市化進程的加速和生活方式的改變,機器人吸塵器的普及速度正在迅速提升。公寓和緊湊型住宅的日益增加也促使消費者採用更快捷、更方便的日常清潔技術。

到2025年,全自動吸塵器將佔據72%的市場。消費者日益成長的減輕家務勞動負擔的需求,正強勁推動全自動掃地機器人的普及。這些產品利用智慧感測器、先進的地圖繪製技術、自主導航系統和自動調節功能,實現自主清潔。消費者越來越重視自動化清潔方案帶來的便利,無需定期監控或操作即可隨時保持清潔。

預計到2025年,美國機器人吸塵器市場將佔據77.9%的市場佔有率,市場規模將達到32億美元。在美國,市場需求依然強勁,這主要得益於消費者對便利、衛生、省時的家用電器日益成長的偏好。智慧家庭生態系統的普及以及消費者在連網家庭技術方面的支出增加,正在加速全部區域機器人吸塵器的銷售。美國消費者仍優先考慮性能可靠、操作簡單、功能多樣的住宅清潔產品。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 人們的健康和衛生意識增強

- 智慧家庭和物聯網生態系統的發展

- 機器人和人工智慧的進步

- 產業潛在風險與挑戰

- 對初始成本高度敏感

- 與維護和售後服務相關的挑戰

- 機會

- 產品客製化和本地化

- 與維護和售後服務相關的挑戰

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監理框架

- 安全和認證標準(UL、CE、FCC)

- 資料隱私法規(GDPR 和 CCPA 的影響)

- 電子廢棄物和環境合規性(WEEE、ROHS)

- 區域能源效率標準

- 智慧型裝置的網路安全法規

- 價格分析

- 2022-2025年歷史價格趨勢分析

- 按玩家類型(高階/中階/經濟型)分類的定價策略

- 需求價格彈性

- 區域價格波動分析

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 目前分銷基礎設施和通路滲透情況

- 按地區與業態(現代零售與傳統零售)分類的通路覆蓋率

- 缺乏最後一公里基礎設施和不斷變化的管道

- D2C 與零售夥伴關係模式

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 地板吸塵器

- 游泳池吸塵器

- 窗戶吸塵器

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅

- 商業的

- 產業

第7章 市場估計與預測:依營運模式分類,2022-2035年

- 全自動

- 遙控

第8章 市場估算與預測:依通路分類,2022-2035年

- 線上

- 企業網站

- 電子商務平台

- 離線

- 百貨公司

- 超級市場和大賣場

- 其他零售商店(如廚具專賣店)

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- 世界公司

- Beijing Roborock Technology

- ECOVACS(DEEBOT)

- Samsung Electronics

- LG Electronics

- Dyson

- SharkNinja

- Eufy

- 當地公司

- Haier Group

- Hoover(TTI)

- Bissell

- Vorwerk(Kobold)

- Miele

- Cecotec

- Viomi

- 新興企業

- Dreame Technology

- Narwal Robotics

- SwitchBot

- Wyze Labs

- ILIFE

- Proscenic

- Lefant

The Global Robotic Vacuum Cleaner Market was valued at USD 12.5 billion in 2025 and is estimated to grow at a CAGR of 8.8% to reach USD 30.9 billion by 2035.

Rising awareness regarding indoor cleanliness, healthier living environments, and improved air quality is significantly contributing to market growth. Consumers are increasingly adopting robotic vacuum cleaners to reduce dust accumulation, allergens, pet hair, and airborne particles inside residential spaces, particularly in densely populated urban homes with limited ventilation. Advanced robotic cleaning devices equipped with HEPA filtration systems, enhanced suction capabilities, and automated cleaning schedules are gaining widespread popularity for their ability to maintain consistent floor hygiene with minimal manual effort. Consumer attitudes toward home sanitation have shifted considerably in recent years, leading to stronger demand for proactive and routine cleaning solutions rather than occasional deep-cleaning practices. Automated robotic vacuum cleaners support this trend by offering touch-free cleaning operations and scheduled maintenance that help minimize exposure to dust and debris. As smart home adoption continues to rise globally, robotic vacuum cleaners are increasingly viewed as long-term lifestyle and wellness investments rather than simple convenience appliances. Technological advancements in navigation systems, AI-powered mapping, obstacle detection, and smart connectivity features are further strengthening product demand across residential markets worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.5 Billion |

| Forecast Value | $30.9 Billion |

| CAGR | 8.8% |

The floor vacuum cleaner segment accounted for USD 11.1 billion in 2025. Consumer demand for efficient and easy-to-operate floor cleaning solutions continues to rise across different flooring surfaces, including hardwood, tiles, and carpets. While conventional vacuum cleaners remain widely used because of their affordability and strong cleaning performance, robotic alternatives are rapidly gaining preference due to increasing urbanization and changing lifestyles. Growing numbers of apartment and compact housing developments are also encouraging consumers to adopt faster and more convenient cleaning technologies for daily use.

The fully automated segment held a 72% share in 2025. Rising consumer preference for reduced manual involvement in household cleaning activities is driving strong adoption of fully automated robotic vacuum cleaners. These products utilize intelligent sensors, advanced mapping technologies, autonomous navigation systems, and self-adjusting cleaning capabilities to complete cleaning tasks independently. Consumers are increasingly valuing the convenience of automated cleaning solutions that consistently maintain cleanliness without requiring regular supervision or operational effort.

United States Robotic Vacuum Cleaner Market accounted for 77.9% share and generated USD 3.2 billion in 2025. Demand across the country remains strong due to growing consumer preference for convenience-oriented, hygienic, and time-saving household appliances. Increasing adoption of smart home ecosystems and rising consumer spending on connected home technologies are accelerating sales of robotic vacuum cleaners throughout the region. Consumers in the United States continue to prioritize cleaning products that deliver reliable performance, user-friendly functionality, and versatile cleaning capabilities for residential applications.

Major companies operating in the Global Robotic Vacuum Cleaner Market include Beijing Roborock Technology, ECOVACS (DEEBOT), Samsung Electronics, LG Electronics, Dyson, SharkNinja, Eufy, Haier Group, Hoover (TTI), Bissell, Vorwerk (Kobold), Miele, Cecotec, Viomi, Dreame Technology, Narwal Robotics, SwitchBot, Wyze Labs, ILIFE, Proscenic, and Lefant. Companies operating in the robotic vacuum cleaner market are focusing heavily on product innovation, smart technology integration, and portfolio expansion to strengthen their market position. Manufacturers are investing in artificial intelligence, advanced navigation systems, LiDAR mapping, and self-emptying technologies to improve cleaning efficiency and user convenience. Businesses are also introducing connected features such as voice assistant compatibility, mobile app controls, and personalized cleaning schedules to enhance customer engagement. Strategic partnerships with smart home ecosystem providers and expansion into emerging markets are helping brands increase their global reach. In addition, companies are prioritizing sleek product designs, improved battery performance, and multi-surface cleaning capabilities to differentiate their offerings.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Operation mode

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing health & hygiene awareness

- 3.2.1.2 Growth of smart homes & IoT ecosystems

- 3.2.1.3 Advancements in robotics & AI

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost sensitivity

- 3.2.2.2 Maintenance & after-sales issues

- 3.2.3 Opportunities

- 3.2.3.1 Product customization & localization

- 3.2.3.2 Maintenance & after-sales issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory framework

- 3.7.1 Safety & certification standards (UL, CE, FCC)

- 3.7.2 Data privacy regulations (GDPR, CCPA impact)

- 3.7.3 E-waste & environmental compliance (WEEE, ROHS)

- 3.7.4 Energy efficiency standards by region

- 3.7.5 Cybersecurity regulations for smart devices

- 3.8 Pricing analysis

- 3.8.1 Historical price trend analysis (2022-2025)

- 3.8.2 Pricing strategy by player type (premium/mid-range/budget)

- 3.8.3 Price elasticity of demand

- 3.8.4 Regional price variation analysis

- 3.9 Trade data analysis (driven by paid data base)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.11.1 Channel coverage by region & format (modern vs. Traditional trade)

- 3.11.2 Last-mile infrastructure gaps & emerging channel shifts

- 3.11.3 Direct-to-consumer vs. retail partnership models

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Floor vacuum cleaner

- 5.3 Pool vacuum cleaner

- 5.4 Window vacuum cleaner

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Estimates and Forecast, By Operation Mode, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Fully automated

- 7.3 Remote control

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 Company websites

- 8.2.2 E-commerce platforms

- 8.3 Offline

- 8.3.1 Department stores

- 8.3.2 Supermarkets/hypermarkets

- 8.3.3 Other retail stores (specialty kitchenware stores, etc)

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Beijing Roborock Technology

- 10.1.2 ECOVACS (DEEBOT)

- 10.1.3 Samsung Electronics

- 10.1.4 LG Electronics

- 10.1.5 Dyson

- 10.1.6 SharkNinja

- 10.1.7 Eufy

- 10.2 Regional players

- 10.2.1 Haier Group

- 10.2.2 Hoover (TTI)

- 10.2.3 Bissell

- 10.2.4 Vorwerk (Kobold)

- 10.2.5 Miele

- 10.2.6 Cecotec

- 10.2.7 Viomi

- 10.3 Emerging players

- 10.3.1 Dreame Technology

- 10.3.2 Narwal Robotics

- 10.3.3 SwitchBot

- 10.3.4 Wyze Labs

- 10.3.5 ILIFE

- 10.3.6 Proscenic

- 10.3.7 Lefant

2026-2030年全球住宅機器人吸塵器市場

2026-2030年全球住宅機器人吸塵器市場 機器人吸塵器市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、應用、地區和競爭格局分類,2021-2031年

機器人吸塵器市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、應用、地區和競爭格局分類,2021-2031年 機器人吸塵器市場:2026-2032年全球市場預測(依產品類型、價格範圍、技術、應用、最終用戶和銷售管道)

機器人吸塵器市場:2026-2032年全球市場預測(依產品類型、價格範圍、技術、應用、最終用戶和銷售管道) 住宅機器人吸塵器市場:按機器人類型、充電方式和地區分類

住宅機器人吸塵器市場:按機器人類型、充電方式和地區分類 2026-2030年全球機器人吸塵器市場

2026-2030年全球機器人吸塵器市場 全球住宅機器人吸塵器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球住宅機器人吸塵器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 機器人吸塵器市場規模、佔有率、趨勢和預測(按類型、充電方式、分銷管道、應用、最終用戶和地區分類),2026-2034年住宅機器人吸塵器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按充電方式、類型、分銷管道、地區和競爭格局分類,2021-2031年全球自主城市吸塵器市場(按類型、組件、推進方式、應用、最終用戶和分銷管道分類)預測(2026-2032年)日本機器人吸塵器市場規模、佔有率、趨勢及預測(按類型、充電方式、分銷管道、應用、最終用戶和地區分類,2026-2034年)

機器人吸塵器市場規模、佔有率、趨勢和預測(按類型、充電方式、分銷管道、應用、最終用戶和地區分類),2026-2034年住宅機器人吸塵器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按充電方式、類型、分銷管道、地區和競爭格局分類,2021-2031年全球自主城市吸塵器市場(按類型、組件、推進方式、應用、最終用戶和分銷管道分類)預測(2026-2032年)日本機器人吸塵器市場規模、佔有率、趨勢及預測(按類型、充電方式、分銷管道、應用、最終用戶和地區分類,2026-2034年)