|

市場調查報告書

商品編碼

2045753

1. 六角形化合物市場機會、成長要素、產業趨勢分析及2026-2035年預測1-Hexene Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

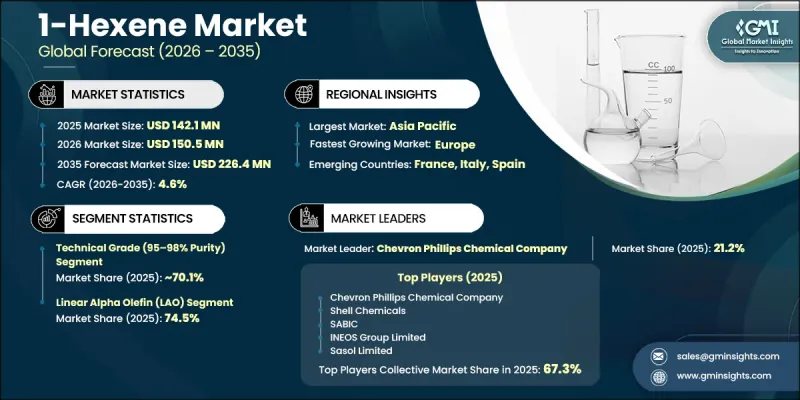

預計到 2025 年,全球 1-Hexene市場價值將達到 1.421 億美元,年複合成長率為 4.6%,到 2035 年將達到 2.264 億美元。

由於1-Hexene作為高密度聚苯乙烯(HDPE)和線性低密度聚乙烯(LLDPE)生產中的關鍵共聚物被廣泛應用,其產業持續穩定成長。這些聚乙烯材料廣泛應用於眾多工業領域,用於製造包裝產品、管道、工業容器和各種塑膠零件。汽車和建設產業對輕質耐用材料的需求不斷成長,而1-Hexene能夠提升聚乙烯基產品的強度、柔軟性和性能,這進一步推動了市場擴張。此外,由於1-Hexene的生產嚴重依賴原油和天然氣衍生的乙烯,原料供應和價格的波動也會影響市場成長。原料成本波動、地緣政治不穩定和供應鏈中斷等因素持續影響生產的整體經濟效益。同時,人們對永續生產實踐的日益關注以及聚合物技術的進步正在加速生物基替代品和高性能聚乙烯產品的開發,這為全球1-Hexene市場的長期成長提供了支持。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1.421億美元 |

| 預測金額 | 2.264億美元 |

| 複合年成長率 | 4.6% |

到2025年,純度為95-98%的技術級產品將佔據70.1%的市場。由於其在工業製造、化學加工和溶劑配方等許多領域有著廣泛的應用,且在這些領域對超高純度要求不高,因此該細分市場的需求持續強勁。其成本績效效益和對大規模工業應用的適用性也持續推動多個終端用戶產業的成長。

預計到2025年,線性α-烯烴(LAO)市佔率將達到74.5%。 LAO基1-Hexene產品憑藉其卓越的產品穩定性、高純度以及在下游化學加工和聚合應用中優異的性能,獲得了市場的強勁支持。 LAO的鎖狀分子結構有助於提高反應活性和加工效率,使其成為生產高品質聚合物和工業化學品的理想選擇。在塑膠製造、界面活性劑生產和工業化學品等領域的持續拓展應用,進一步鞏固了該細分市場的領先地位。

預計到2025年,北美1-Hexene市場規模將達到4,440萬美元,並在2026年至2035年間以4.7%的複合年成長率成長。該地區市場成長的主要驅動力是美國和加拿大活躍的化學品製造活動以及不斷成長的出口需求。工業塗料、黏合劑和特種化學品消費量的成長也促進了全部區域對1-己烯需求的擴大。此外,對永續化學加工技術和創新主導製造方法的投資增加,也對北美市場的發展產生了積極影響。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 包裝應用領域對高性能聚乙烯的需求不斷成長

- 亞太地區下游石化設施的擴張

- 包裝和汽車產業輕量化趨勢

- 產業潛在風險與挑戰

- 原物料價格(乙烯和原油)波動

- 特定地區存在供應過剩和需求疲軟的擔憂

- 市場機遇

- 多元化經營,進軍特殊化學品和高性能聚合物領域。

- 農業和先進包裝領域的新應用

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTLE分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 專利趨勢

- 貿易統計

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- LATAM

- 中東和非洲

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依純度分類,2022-2035年

- 技術級(純度 95-98%)

- 高純度等級(純度99%或更高)

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 線性α-烯烴(LAO)

- 支鏈烯烴

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 聚乙烯生產

- 庚醇生產

- 味道

- 香水

- 染料

- 樹脂

第8章 市場估算與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第9章 市場估計與預測:依最終用途產業分類,2022-2035年

- 化工

- 塑膠產業

- 包裝產業

- 軟包裝

- 硬包裝

- 電子商務與物流包裝

- 建設產業

- 消費品

- 家居用品和家用電器

- 個人護理和化妝品

- 玩具和休閒用品

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- UAE

- 其他中東和非洲國家

第11章:公司簡介

- Chevron Phillips Chemical Company

- SABIC

- Shell Chemicals

- INEOS Group Limited

- Sasol Limited

- Qatar Chemical Company(Q-Chem)

- Idemitsu Kosan Co., Ltd.

- SIBUR Holding

- Sinopec

- PetroChina

The Global 1-Hexene Market was valued at USD 142.1 million in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 226.4 million by 2035.

The 1-hexene industry continues to witness stable growth due to its extensive use as a key comonomer in the production of high-density polyethylene (HDPE) and linear low-density polyethylene (LLDPE). These polyethylene materials are widely utilized across multiple industrial sectors for manufacturing packaging products, pipes, industrial containers, and various plastic components. Rising demand from the automotive and construction industries for lightweight and durable materials is further supporting market expansion, as 1-hexene improves the strength, flexibility, and performance characteristics of polyethylene-based products. Market growth is also influenced by fluctuations in raw material availability and pricing, particularly because 1-hexene production depends heavily on ethylene derived from crude oil and natural gas sources. Variations in feedstock costs, geopolitical uncertainties, and supply chain disruptions continue to impact overall production economics. At the same time, increasing focus on sustainable manufacturing practices and advancements in polymer technologies are encouraging the development of bio-based alternatives and higher-performance polyethylene products, supporting long-term growth opportunities within the global 1-hexene market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $142.1 Million |

| Forecast Value | $226.4 Million |

| CAGR | 4.6% |

The technical grade segment with 95-98% purity accounted for 70.1% share in 2025. This segment continues to maintain strong demand due to its widespread utilization across industrial manufacturing operations, chemical processing activities, and solvent formulation applications where ultra-high purity specifications are not essential. Its cost-effectiveness and suitability for large-scale industrial usage continue to support growth across multiple end-use industries.

The linear alpha olefin (LAO) segment held a share of 74.5% in 2025. Strong market preference for LAO-based 1-hexene products is attributed to their superior product consistency, higher purity levels, and enhanced performance in downstream chemical processing and polymerization applications. The linear molecular structure of LAO supports improved reactivity and processing efficiency, making it highly suitable for producing high-quality polymers and industrial chemical products. Expanding utilization across plastic manufacturing, surfactant production, and industrial chemical applications continues to strengthen the segment's market leadership.

North America 1-Hexene Market was valued at USD 44.4 million in 2025 and is anticipated to grow at a CAGR of 4.7% between 2026 and 2035. Regional market growth is being supported by strong chemical manufacturing activities and increasing export demand across the United States and Canada. Rising consumption of industrial coatings, adhesives, and specialty chemical products is contributing to expanding demand for 1-hexene throughout the region. In addition, increasing investments in sustainable chemical processing technologies and innovation-driven manufacturing practices are positively influencing market development across North America.

Major companies operating in the Global 1-Hexene Market include Chevron Phillips Chemical Company, SABIC, Shell Chemicals, INEOS Group Limited, Sasol Limited, Qatar Chemical Company (Q-Chem), Idemitsu Kosan Co., Ltd., SIBUR Holding, Sinopec, and PetroChina. Companies operating in the 1-hexene market are adopting multiple strategies to strengthen their market position and improve long-term competitiveness. Leading manufacturers are increasing investments in research and development activities to enhance production efficiency, improve product purity, and support sustainable chemical manufacturing practices. Many companies are also focusing on expanding production capacities and strengthening supply chain networks to address rising global demand and minimize raw material supply disruptions. Strategic collaborations, joint ventures, and partnerships with downstream polymer manufacturers are helping businesses expand their market reach and improve customer relationships. In addition, organizations are prioritizing the development of bio-based and environmentally sustainable 1-hexene solutions to align with evolving environmental regulations and sustainability goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Purity

- 2.2.3 Product type

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.2.6 End use industry

- 2.2.7 Application

- 2.2.8 End use industry

- 2.2.9 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for high-performance polyethylene in packaging applications

- 3.2.1.2 Expansion of downstream petrochemical capacities in Asia Pacific

- 3.2.1.3 Lightweighting trend in packaging & automotive industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in raw material prices (ethylene & crude oil)

- 3.2.2.2 Oversupply concerns & weak demand in certain regions

- 3.2.3 Market opportunities

- 3.2.3.1 Diversification into specialty chemicals & high-performance polymers

- 3.2.3.2 Emerging applications in agriculture & advanced packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Purity, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Technical grade (95-98% purity)

- 5.3 Pure grade (≥99% purity)

Chapter 6 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Linear alpha olefin (LAO)

- 6.3 Branched olefin

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Polyethylene production

- 7.3 Heptanol production

- 7.4 Flavors

- 7.5 Perfumes

- 7.6 Dyes

- 7.7 Resins

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Chemical industry

- 9.3 Plastics industry

- 9.4 Packaging industry

- 9.4.1 Flexible packaging

- 9.4.2 Rigid packaging

- 9.4.3 E-commerce & logistics packaging

- 9.5 Construction industry

- 9.6 Consumer goods

- 9.6.1 Household products & appliances

- 9.6.2 Personal care & cosmetics

- 9.6.3 Toys & recreational products

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Chevron Phillips Chemical Company

- 11.2 SABIC

- 11.3 Shell Chemicals

- 11.4 INEOS Group Limited

- 11.5 Sasol Limited

- 11.6 Qatar Chemical Company (Q-Chem)

- 11.7 Idemitsu Kosan Co., Ltd.

- 11.8 SIBUR Holding

- 11.9 Sinopec

- 11.10 PetroChina

聚α烯烴市場:依產品類型、應用、終端用戶產業及銷售管道分類-2026-2032年全球市場預測

聚α烯烴市場:依產品類型、應用、終端用戶產業及銷售管道分類-2026-2032年全球市場預測 2026年全球功能性聚烯熱熔膠黏合劑報告α-烯烴市場:依產品類型、製造流程、應用和分銷管道分類-2026-2032年全球市場預測聚α烯烴潤滑脂市場依產品類型、黏度等級、應用、終端用戶產業及銷售管道,全球預測,2026-2032年

2026年全球功能性聚烯熱熔膠黏合劑報告α-烯烴市場:依產品類型、製造流程、應用和分銷管道分類-2026-2032年全球市場預測聚α烯烴潤滑脂市場依產品類型、黏度等級、應用、終端用戶產業及銷售管道,全球預測,2026-2032年 聚羥基烷酯酯 (PHA) 市場規模、佔有率和成長分析(按產品、PHA 類型、生產方法、應用和地區分類)—2026-2033 年產業預測

聚羥基烷酯酯 (PHA) 市場規模、佔有率和成長分析(按產品、PHA 類型、生產方法、應用和地區分類)—2026-2033 年產業預測 α-烯烴市場規模、佔有率和成長分析(按類型、應用和地區分類):產業預測(2026-2033 年)

α-烯烴市場規模、佔有率和成長分析(按類型、應用和地區分類):產業預測(2026-2033 年) 阿爾法烯烴市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年)

阿爾法烯烴市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年) 1-Hexene的全球市場全球非晶態α-烯烴共聚物市場

1-Hexene的全球市場全球非晶態α-烯烴共聚物市場 聚羥基烷酯(PHA) 薄膜市場規模、佔有率及趨勢分析報告:按應用、最終用途、地區及細分市場預測,2025-2030 年

聚羥基烷酯(PHA) 薄膜市場規模、佔有率及趨勢分析報告:按應用、最終用途、地區及細分市場預測,2025-2030 年